QE: What have we learned?

Markus’ Academy, 3/24/2022

Arvind Krishnamurthy

Stanford University GSB, SIEPR, and NBER

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The impact of quantitative easing (QE) on the macroeconomy and the identification challenges associated with it. It explores the conventional and unconventional channels through which QE affects the economy and the impacts on output, inflation, financial stability, and fiscal consequences. The document also delves into the narrow channels of QE, such as impacts on liquidity, risk, and safety/scarcity premia. It provides evidence from different studies and models and discusses the user cost of capital and firm investment. useful for students studying macroeconomics, monetary policy, and financial markets.

Typology: Lecture notes

1 / 28

This page cannot be seen from the preview

Don't miss anything!

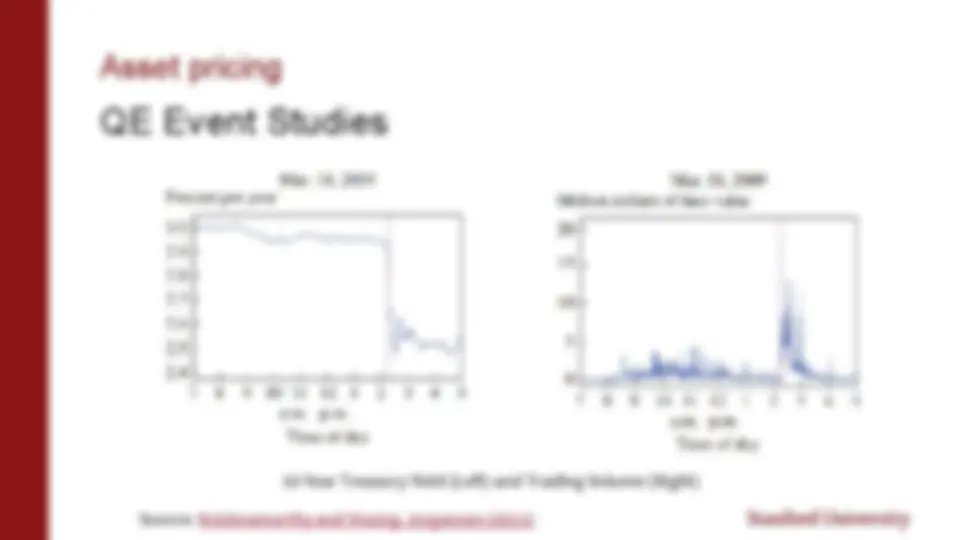

QE Event Studies

10 Year Treasury Yield (Left) and Trading Volume (Right)

Source: Krishnamurthy and Vissing-Jorgensen (2011)

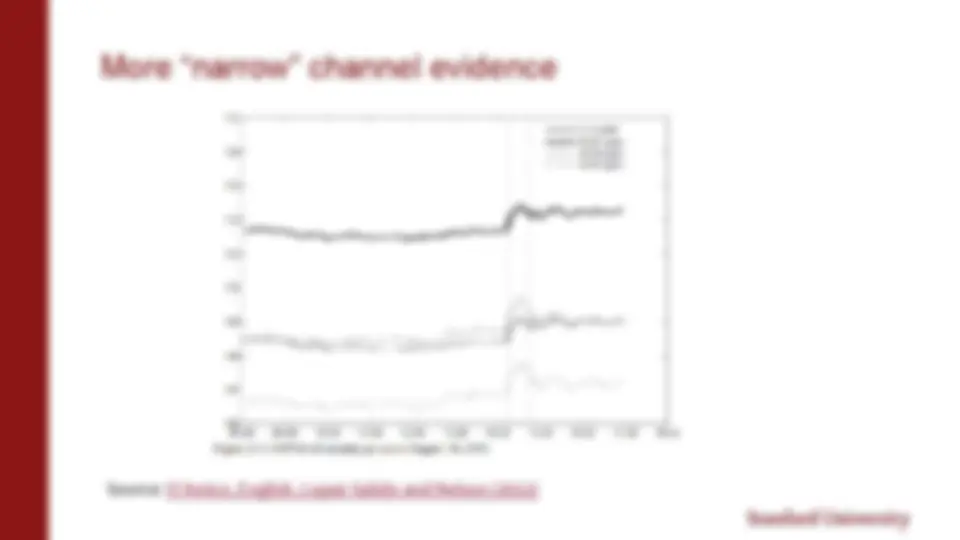

Source: Joyce, Lasaosa, Stevens and Tong (2011)

Source: D’Amico, English, Lopez-Salido and Nelson (2012)

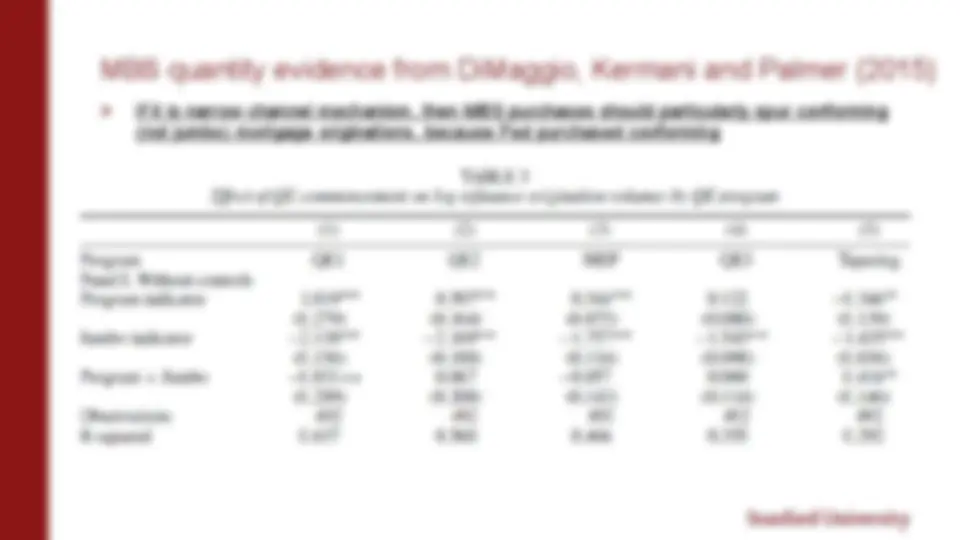

If it is narrow channel mechanism, then MBS purchases should particularly spur conforming (not jumbo) mortgage originations, because Fed purchased conforming

Model of the Treasury market yield curve delivering risk premia that are a function of supply

Players:

Preferred habitat investors (pension funds, insurance companies, bond mutual funds) Yield curve arbitrageurs (hedge funds, bond dealers/bond trading desks)

Arbitrageurs integrate the yield curve, demanding risk premia as compensation for interest rate shocks and future supply shocks:

Risk premium on interest rate shocks give a way of thinking about a duration risk premium

If arbitrageur risk aversion is high (e.g., balance sheet constraints) then risk premia are higher, and QE has a bigger impact Duration local effects come from risk premia to future supply shocks

Treasury yield also affected by safe asset demand effects.

If 10-year preferred habitat investors (e.g., insurance company demanding 10 year safe bonds) increase their demand for 10-year bonds … the 10-year yield will fall.

What is a pure duration risk-premium effect?

Look at yield change on an asset not demanded by safe asset investors, but has duration risk, which the arbitrageur also prices

E.g., non-investment grade corporate debt?

And this is related to spillovers: what else does the arbitrageur pricing kernel price?

QE Shock

Interest rate(s) in targeted market(s)

User cost of capital -> Investment

Household borrowing/saving rate -> consumption

Employment, Output

20

Corporate expenditures will only respond to QE if QE affects the user cost of capital on the marginal unit of capital

Suppose Google had two sources of capital Cash (it has a lot…) Corporate bond market

The marginal source of capital is almost surely cash, where the user cost of capital is the nominal interest rate

Corporate bond QE should be expected to have no effects on Google investment

Evidence for the “no effect”: Acharya and Steffen (2020), Darmouni and Siani (2022)

Google Bond Yield and CDS; Fed Bond Purchase Program Announced 3/