Download Cost Accounting: Budgeting and Cost Control and more Assignments Strategic Management in PDF only on Docsity!

Chapter 1 MANAGEMENT ACCOUNTING - SolutionsManual

TABLE OF CONTENTS

MANAGEMENTACCOUNTING: ANOVERVIEW

1-1 – 1- 2 ManagementAccountingandtheBusinessEnvironment 2-1 –2 - 5

3 UnderstandingofFinancialStatements 3-1 –3 - 1 0

4 FinancialStatementsAnalysis–I 4-1 –4 - 9 5 FinancialStatementsAnalysis–II 5-1 –5- 6 CashFlowAnalysis 6-1 –6- 7 GrossProfitValuationAnalysisandEarningsPerShare Determination 7-1 –7 - 7 8 Cost ConceptsandClassifications 8-1 –8- 9 CostBehavior:AnalysisandUse 9-1 –9- 10 SystemsDesign:Job-OrderCostingandProcessCosting 10-1 –1 0-1 6 11 SystemsDesign:Activity-BasedCostingandManagement 11-1–11- 12 VariableCosting 12-1 –12-

13 Cost-Volume-ProfitRelationships 13-1 –13-

14 ResponsibilityAccountingandTransferPricing 15 Functional and Activity-BasedBudgeting 16 StandardCostsandOperatingPerformanceMeasures 17 ApplicationofQuantitativeTechniquesinPlanning,Controland 14-1 –14- 15-1 –15- 16-1 –16- Decision Making - I 17-1 – 17- 18 ApplicationofQuantitativeTechniquesinPlanning,ControlandDecision Making –II 18-1 – 18- 19 Relevant Costs for DecisionMaking 19-1 – 19- 20 Capital BudgetingDecisions 20-1 – 20- 21 DecentralizedOperationsandSegmentReporting 21-1 – 21- 22 BusinessPlanning 22-1 – 22-

Chapter 1 Management Accounting: An Overview 23 Strategic Cost Management; Balanced Scorecard 23-1 – 23- 24 AdvancedAnalysisandAppraisalofPerformance:FinancialandNonfina ncial 24-1 – 24- 25 Managing Productivity and Marketing Effectiveness 25-1 – 25- 26 Executive Performance Measures and Compensation 26-1 – 26- 27 Managing Accounting in a Changing Environment 27-1 – 27- CHAPTER 1 MANAGEMENT ACCOUNTING: AN OVERVIEW I. Questions

- Use of the word “need” in thequotedpassage is pejorative. Itimpliesanunlimited levelofdemandforinformation.However,rational managers apply acost-benefitcriterion toinformationandwillonly wantaccounting information if itsbenefits exceedits costs.Accountinginformation providesbenefitsbyimproving decision makingandcontrollingbehavior in organizations. In most organizations, accountinginformationis very prevalentwhich impliesthat itsbenefits exceedits costs.Hence,successful managerswillfind it in theirself-interestto learnhowto use accountinginformationin theseorganizations. Clearly, this statement is incurred in those firms where accounting information has very limited usefulness (e.g., if the accounting information is often wrong or is not produced in a timely fashion). In these organizations, managers do not find the accounting information to have benefits in excess of its costs, will not use it, do not need to know how to use it, and definitely do not need it.

- a. Historical costs are oflimiteduse inmakingplanningdecisionsin a rapidly changingenvironment. Withchanging products, processes and prices, the historical costs are inadequate approximations of the opportunity costs of usingresources.

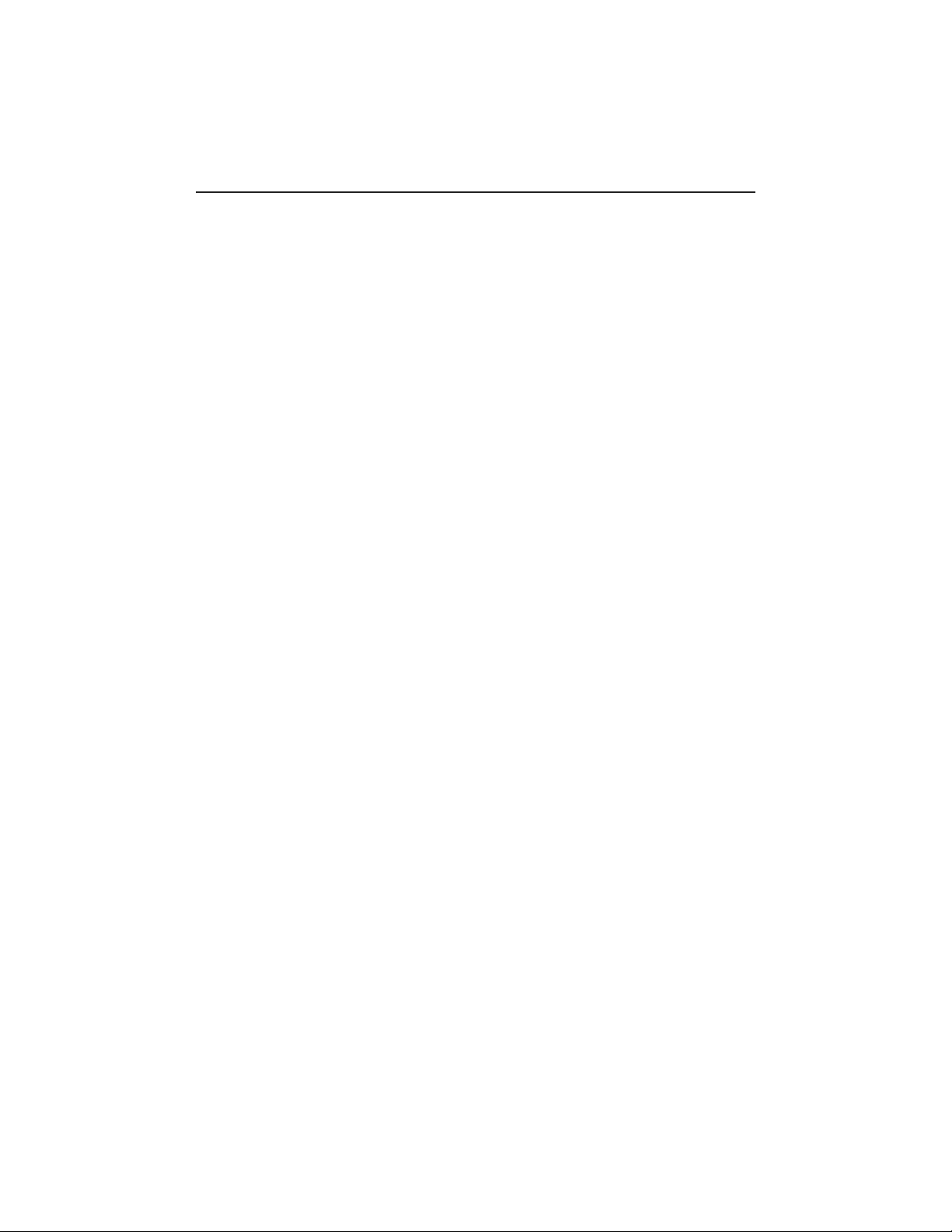

President Controller Treasurer VP, Production VP, Finance VP, Sales System & EDP Manager Cost Clerk Payroll ClerkAccounts ReceivableAccounts Clerk Payable ClerkBilling Clerk General Ledger Bookkeeper Internal Audit Manager General Accounting Manager Assistant Controller Assistant Treasurer Cost Systems AnalystBudget & Standard Cost Analyst Performance Analyst Special^ Chapter 1 Studies Manager Management Accounting: An Overview Cost Accounting Manager Tax Manager

8. BettinaCompany

- Management accountants contribute to strategicdecisionsby providing information about the sources ofcompetitiveadvantage and byhelpingmanagersidentifyand build acompany’sresources andcapabilities.

- In most organizations,managementaccountants performmultipleroles:problemsolving(comparative analyses fordecision making),scorekeeping(accumulating data and reporting reliable results), and attention directing(helpingmanagers properly focus theirattention).

- Threeguidelinesthathelp managementaccountants increase their value to managers are (a)employacost-benefitapproach, (b)recognizebehavioral aswellastechnicalconsiderations,and (c)identify differentcosts fordifferentpurposes.

- Management accounting is an integral part of thecontroller’sfunction in an organization. Inmostorganizations, the controller reports to the chief financialofficer,whois akeymemberof the topmanagementteam.

Management Accounting: An Overview Chapter 1

- Management accountants have ethical responsibilities that are related tocompetence,confidentiality, integrity,andobjectivity.

- Byreportingandinterpretingrelevantdata,thecontrollerexertsaforceorinfluence thatimpels managementtowardmaking better-informed decisions. The controller ofonecompany described the job as “a business advisor to… helptheteamdevelopstrategyandfocustheteamallthewaythroughrecommendati onsandimplementation.” 15.15. FinancialAccounting Audience: External: shareholders, creditors, taxauthorities Purpose: Report on past performance to externalparties;basis ofcontractswithownersandlenders Timeliness: Delayed;historical Restrictions: Regulated; rulesdrivenbygenerallya c c e p t e d accounting principles and governmentauthorities TypeofInformation: Financialmeasurementsonly NatureofInformation: Objective, auditable, reliable, consistent, precise Scope: Highlyaggregate; report onentireorganization ManagerialAccounting Audience: Internal:Workers,managers,executives Purpose: Inform internaldecisionsmade byemployeesand managers;feedbackand control on operatingperformance Timeliness: Current, futureoriented Restrictions: No regulations; systems andinformation determined by management to meet strategic and operational needs Type of Information: Financial, plus operational and physical measurements on processes, technologies, suppliers customers, and competitors

Management Accounting: An Overview Chapter 1 a. (4)M a r k e t i n g b. (3)P r o d u c t i o n c. (6) Customerservice d. (5)D i s t r i b u t i o n Exercise 3 a. (4)M a r k e t i n g b. (3)P r o d u c t i o n c. (5)D i s t r i b u t i o n d. (4)M a r k e t i n g e. (5)D i s t r i b u t i o n f. (3)P r o d u c t i o n g. (1) Research anddevelopment h. (2)D e s i g n III. Problems Problem 1 (Problem Solving, Scorekeeping, and Attention Directing) Because the accountant’s duties are often not sharply defined, some of these answers might be challenged:

- Scorekeeping

- Attentiondirecting

- Scorekeeping

- Problemsolving

- Attentiondirecting

- Attentiondirecting

- Problemsolving

- Scorekeeping (dependingon the extent of the report) or attention getting

- This question isintentionallyvague. Thegive-and-takeof the budgetary process usuallyencompassesall three functions, but itemphasizes scorekeepingthe least. The main function is attention directing, but problemsolvingis alsoinvolved.

- Problemsolving Problem 2 (Management Accounting Information System)

- Inputs: b, g, i,m

- Processes: a, d, f,j

- Outputs: e, k,n

Chapter 1 Management Accounting: An Overview

- Systemobjectives:c, h,l Problem 3 (Role of Management Accountants) Planning. The management accountant gains an understanding of the impact on the organization of planned transactions (i.e., analyzing strengths and weaknesses) and economic events, both strategic and tactical, and sets obtainable goals for the organization. The development of budgets is an example of planning. Controlling. Themanagementaccountant ensures theintegrityof financial information,monitorsperformance against budgets and goals, and provides information internally fordecision making.Comparing actual performance against budgeted performance and taking corrective actionwherenecessary is an example ofcontrolling.Internal auditing is another example. Evaluating Performance. The management accountant judges and analyzes the implication of various past and expected events, and then chooses the optimum course of action. The management accountant also translates data and communicates the conclusions. Graphical analysis (such as trend, bar charts, or regression) and reports comparing actual costs with budgeted costs are examples of evaluating performance. Ensuring Accountability of Resources. The management accountant implements a reporting system closely aligned to organizational goals that contribute to the measurement of the effective use of resources and safeguarding of assets. Internal reporting such as comparison of actual to budget is an example of accountability. External Reporting. The management accountant prepares reports in accordance with generally accepted accounting principles and then disseminates this information to shareholders, creditors, and regulatory tax agencies. An annual report or a credit application are examples of external reporting. Problem 4 (Line Versus Staff) Jamie Reyes is staff. She is in a support role – she prepares reports and helps explain and interpret them. Her role is to help the line managers more effectively carry out their responsibilities. Stephen Santos is a line manager. He has direct responsibility for producing a garden hose. Clearly, one of the basic objectives for the existence of a

Chapter 1 Management Accounting: An Overview The other“end-of-year games”occur in many organizations and may fall into the “gray” to “acceptable” area.However,muchdependson the circumstances surrounding eachone: (a) If theindependentcontractordoesnotdomaintenancework inDecember,there is no transaction regardingmaintenanceto record. The responsibility for ensuring that packagingequipmentiswell maintainedis that of the plantmanager.Thedivisioncontroller probably can do little morethanobservetheabsenceofaDecembermaintenancecharge. (d) Inmanyorganizations,salesareheavilyconcentratedinthefinalweeksof the fiscalyear-end.If the double bonus is approved by thedivisionmarketingmanager,thedivisioncontroller can do little more than observe the extra bonus paid inDecember. (e) If TV spots are reduced inDecember,the advertising cost inDecember willbe reduced. There is no record falsificationhere. (g) Muchdependson themeansof “persuading” carriers to accept themerchandise.Forexample,if anunder-the-tablepayment isinvolved,it is clearly unethical. If,however,the carrierreceivesno extraconsiderationandwillinglyagrees to accept theassignment,the transaction appears ethical. Each of the (a), (d),(e)and (g)“end-of- yeargames”maywelldisadvantageYummyFoods in the long run. For example, lack of routinemaintenancemay lead to subsequentequipmentfailure. Thedivisionalcontrolleriswelladvised to raise such issues inmeetingswith thedivisionpresident.However,ifYummyFoods has a rigid set ofline/staffdistinctions, thedivisionpresident is theonewhobears primary responsibility for justifyingdivisionactions toseniorcorporateofficers. Requirement 3 IfTanbelievesthatRyanwants her toengagein unethicalbehavior,she should first directly raise herconcernswithRyan.IfRyanisunwillingto change his request,Tanshould discussherconcerns withthe Corporate Controller ofYummyFoods.Tanalso maywellask for a transfer from the snack foodsdivisionif she perceivesRyanisunwillingto listen to pressure brought by the CorporateController,CFO, orevenPresident ofYummyFoods. In theextreme,she may want to resign if the corporate culture ofYummyFoods is to rewarddivisionmanagerswhoplay“end-of-yeargames”thatTanviewsas unethical and possiblyillegal. Problem 6

Management Accounting: An Overview Chapter 1 James Torres has come up with a scheme that involves a combination of data falsification and smoothing! Not only has he made up the revenue numbers, but also he has had the gall to defer some of them to the next period. Making up such numbers is clearly illegal. Smoothing, in this example is also illegal because the numbers are fictitious. Problem 7 Clearly thevice-president willlose his orher jobifyouturnhimorherin.Giventhat this is a majorviolationof the code ofethicsand aviolationpatentlaw,thevice- presidentcould go to jail.Yourbest course of action is tocheckyour information and if thevice-presidentisdefinitely involved,goimmediatelyto theVP’ssuperior(whois probably aseniorVP or thecompanypresident). Theorganization’sattorneyswilltake over fromthere. Problem 8 One option is to do nothing and ignore what you saw, however, this may violate your own code of ethics and your ethical responsibilities under the organization’s code of ethics. Given that you want to do something, it is probably best to start by talking to employees in your organization whose job it is to deal with ethical issues. If no such employees exist or are available, you might start by using a decision model. This model incorporated the following steps:

- Determinethe Facts – What, Who, Where,How

- Definethe EthicalIssue

- IdentifyMajor Principles, Rule,Values

- Specify theAlternatives.

- CompareValuesand Alternatives, See if ClearDecision

- Assess theConsequences.

- MakeYourDecision. IV. Cases Case 1 (Financial vs. Managerial Accounting) Requirement (a) Other forwardlookinginformationdesired in addition to theincomestatement information are

- Disclosure of thecomponentsof financial performance, i.e., nature and source ofrevenues,various activities, transactions, and other relevantevents affectingthecompany.

Management Accounting: An Overview Chapter 1 existing customers. It is therefore possible to lose the business of several key accounts. Requirement (b) Decrease in cost of goods sold to sales This performance measure could create the following problems:

- Purchasing goods with poor quality atlowercost andsellingthem for the sameprice.

- Indiscriminatelyincreasingsellingprice towidenthe profitmarginwithout regard tocompetitor’scurrentprices.

- If the entity is manufacturing itsowngoods,managers could try toeconomizeon costs, i.e., buying poorer quality of materials,employingunskilledworkers, etc. thereby causing deterioration of the quality of thefinishedproducts. In all of the above situations, customer patronage could eventually be adversely affected. Requirement (c) Decrease in selling and administrative expense to sales Cost-cutting is generally advisable for as long as the quality of goods and services are not compromised. Likewise, certain cost-saving measures could demotivate sales people and other employees and could lead to counter- productive activities. Case 3 (The Roles ofManagers andManagementAccountants)

- Managerialaccounting,Financialaccounting

- Planning

- Directing andmotivating

- Feedback

- Decentralization

- Line

- Staff

- Controller

- Budgets

- Performancereport

- Chief FinancialOfficer

- Precision;Nonmonetarydata

Chapter 1 Management Accounting: An Overview Case 4 (Ethics in Business) If cashiers routinely short-changed customerswheneverthe opportunity presented itself,mostof uswouldbe careful to count our change beforeleavingthecounter.Imaginewhateffectthiswouldhave on the line at your favorite fast-food restaurant. Howwouldyouliketo wait inline whileeach andeverycustomer laboriously counts outhisor her change?Additionally,if you can’t trust the cashiers togive honestchange, can you trust the cooks to take the time tofollowhealth precautions such as washing their hands? Ifyoucan’t trustanyoneat the restaurant wouldyouevenwant to eat out? Generally, whenwebuygoodsand services in the free market,weassumeweare buying frompeoplewho have a certainlevelof ethical standards. If we couldnottrustpeopleto maintain those standards,we wouldbe reluctant tobuy.The net result ofwidespread dishonestywould be a shrunkeneconomywith alowergrowth rate andfewer goodsand services for sale at aloweroveralllevelofquality. Case 5 (Ethics and the Manager) Requirement 1 Failure to report the obsolete nature of the inventory would violate the Standards of Ethical Conduct as follows: Competence Perform duties in accordance withrelevant technicalstandards. Preparecompletereports using reliableinformation. By failing to write down the value of the obsolete inventory, Perez would not be preparing a complete report using reliable information. In addition, generally accepted accounting principles (GAAP) require the write-down of obsolete inventory. Integrity Avoidconflicts ofinterest. Refrain from activities that prejudice the ability to perform dutiesethically. Refrain from subverting thelegitimategoals of theorganization. Refrain fromdiscreditingtheprofession.

Chapter 1 Management Accounting: An Overview example, the manager of central purchasing wouldneedtoknowthelevelof currentinventoriesand budgeted allowances in various areas beforedoingany purchasing; the vice president foradmissionsand recordswould needto know the status of scholarship funds as students are admitted to the university; the dean of the businesscollegewould needto know his/her budget allowances in various areas, aswellasinformationon cost per student credit hour; and so forth. Case 7 (Ethics in Business) Requirement 1 No, Santos did not act in an ethicalmanner.Incomplyingwith thepresident’sinstructions toomitliabilities from thecompany’sfinancial statements he was in directviolationof theIMA’s Standards of Ethical Conduct forManagement Accountants. Heviolatedboth the “Integrity” and “Objectivity”guidelineson this code of ethical conduct. The fact that the president ordered theomissionof the liabilities isimmaterial. Requirement 2 No, Santos’ actions can’t be justified. Indealingwithsimilarsituations, the Securities and ExchangeCommission(SEC) has consistently ruled that “… corporateofficers…cannotescape culpability by asserting that they acted as ‘goodsoldiers’and cannot rely upon the fact that theviolativeconduct may have beencondonedor ordered by their corporate superiors.” (Quoted from: Gerald H.Lander,MichaelT.Cronin, and AlanReinstein,“InDefenseof the Management Accountant,” Management Accounting, May,1990, p. 55)Thus, Santosnotonly actedunethically,but he could beheld legallyliable ifinsolvencyoccurs and litigation is brought against thecompanyby creditors or others. It is important that students understand this point early in the course, since it iswidelyassumed that “goodsoldiers”are justified by the fact that they are justfollowingorders. In the case at hand, Santos should have resigned rather thanbecomea party to the fraudulent misrepresentation of thecompany’sfinancialstatements.

Case 6 Requirement 1 President Vice Presiden t, Auxiliary Services Vice President, Admissions & Records Academic Vice President Vice President, Financial Services (Controlle r) Vice President, Physical Plant Manager, Central Purchasing Manager, University Press Manager, University Bookstore Manager, Computer Services Manager, Accounting & Finance Manager, Grounds & Custodial Services Manager, Plant & Maintenance Dean, Business Dean, Humanities Dean, Fine Arts Dean, Engineering & Quantitative Dean, Law School (Departments) (Departments) (Departments) (Departments) 1-

Cost Concepts and Classifications Chapter 8 Requirement 3 Andres Romeroshouldfollowthe establishedpoliciesof the organization bearing on the resolution of suchconflict.If thesepoliciesdo not resolve the ethical conflict,Romeroshould report the problem to successivelyhigher levelsofmanagementup to the Board of Directors until it is satisfactorilyresolved.There is norequirementforRomerotoinformhisimmediatesuperior of this action because the superior isinvolvedin the conflict. If theconflictis not resolved after exhausting all courses of internalreview,Romeromayhavenootherrecoursethantoresignfromtheorganizationan dsubmitaninformative memorandumto an appropriatememberof theorganization. (CMA Unofficial Solution, adapted) V. Multiple ChoiceQuestions

- D 11. D 21. B 31. D 41. A 51. B

- D 12. D 22. B 32. C 42. C 52. B

- D 13. D 23. A 33. D 43. D 53. A

- B 14. A 24. A 34. B 44. B 54. C

- D 15. A 25. B 35. D 45. C 55. D

- A 16. A 26. C 36. B 46. B 56. C

- B 17. D 27. B 37. C 47. A 57. C

- D 18. A 28. D 38. B 48. B 58. C

- D 19. D 29. B 39. A 49. C 59. A

- A 20. D 30. C 40. A 50. D 60. B CHAPTER 2 MANAGEMENT ACCOUNTING AND THE BUSINESS ENVIRONMENT I. Questions

Chapter 8 Cost Concepts and Classifications

- Managerial accounting information often brings to the attention of managers important issues thatneedtheir managerialexperienceand skills. In many cases, managerial-accountinginformation willnot answer thequestionorsolvetheproblem,butrathermakemanagementawarethat the issue or problem exists. In this sense, managerial accountingsometimesis said to serve anattention-directingrole.

- Non-value-added costs are the costs of activities that can beeliminatedwithnodeteriorationofproductquality,performance,orperceivedv alue.

- Managers rely on many information systems in addition to managerial- accountinginformation.Examples of otherinformationsystemsincludeeconomicanalysis and forecasting, marketing research, legal research and analysis, andtechnicalinformation provided byengineersand production specialists.

- Becomingthelow-costproducer in an industry requires a clear understanding bymanagementof the costs incurred in its production process. Reports and analysis of these costs are a primary function of managerialaccounting.

- Someactivitiesinthevaluechainofamanufacturerofcottonshirtsareasfollows: (a) Growing and harvestingcotton (b) Transporting rawmaterials (c) Designingshirts (d) Weavingcottonmaterial (e) Manufacturingshirts (f) Transporting shirts toretailers (g) Advertisingcottonshirts Some activities in the value chain of an airline are as follows: (a) Making reservations andticketing (b) Designingthe routenetwork (c) Scheduling (d) Purchasingaircraft (e) Maintainingaircraft (f) Running airport operations,including handlingbaggage (g) Serving food andbeveragesinflight (h) Flying passengers andcargo