Econometric Analysis of Panel Data

12. Random Parameter Models

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Random parameter models, specifically latent class models, and their estimation using docsity.com. The concept of parameter heterogeneity, discrete and continuous parameter variation, estimating an lc model, unmixing a mixed sample, and predicting class membership. The document also includes an example of banking data and its analysis using an lcm.

Typology: Slides

1 / 26

This page cannot be seen from the preview

Don't miss anything!

12. Random Parameter Models

Agenda

Discrete Parameter Variation

,j

The Latent Class Model

(1) Population is a (finite) mixture of J types of individuals.

j = 1,...,J. J 'classes' differentiated by ( , )

(a) Analyst does not know class memberships. ('latent

βj σ ε

J 1 J j=1 J

i,t it i,t ,j

.')

(b) 'Mixing probabilities' (from the point of view of the

analyst) are ,..., , with 1

(2) Conditional density is

P(y | class j) f(y | x , , (^) ε )

π π Σ π =

= = βj σ

Estimating an LC Model

i i

i,t it i,t ,j

i T i1 i2 i,T ,j (^) t 1 it i,t ,j

i

ε

ε (^) = ε

σ = (^) ∏ σ

j

i j j

i

J T i1 i2 i,T (^) j 1 j (^) t 1 it i,t ,j

= =

X (^) i = (^) ∑ π (^) ( βj σ )

( )

i

i

,1 ,J N J T i 1 j 1 j^ t 1 it^ i,t^ ,j

ε ε

= = = ε

∏

∑ ∑ (^) ∏

1 J

j

Mixture of Normals

2 it j it j it j j^ j^ j

T (^2)

T it j i1 iT t 1 j j

T N J (^) T it j i 1 j 1 j^ t 1 j j

=

= = =

Mixture of Normals

+---------------------------------------------+ | Latent Class / Panel LinearRg Model | | Dependent variable YLC | | Number of observations 2500 | | Iterations completed 15 | | Log likelihood function -4972.129 | | Number of parameters 5 | | Akaike IC= 9954.258 Bayes IC= 9983.378 | | Sample is 1 pds and 2500 individuals. | | LINEAR regression model | | Model fit with 2 latent classes. | +---------------------------------------------+ +---------+--------------+----------------+--------+---------+ |Variable | Coefficient | Standard Error |b/St.Er.|P[|Z|>z] | +---------+--------------+----------------+--------+---------+ Model parameters for latent class 1 Constant 4.98725355 .02868463 173.865. Sigma 1.01530880 .02232943 45.470. Model parameters for latent class 2 Constant .96832859 .04770253 20.299. Sigma 1.00358273 .03436303 29.205. Estimated prior probabilities for class membership Class1Pr .69545563 .01040892 66.813. Class2Pr .30454437 .01040892 29.258.

i

i

T (^) it j

j (^) t 1 j j

i J T it j

j 1 j t 1 j j

=

= =

Estimated Posterior Probabilities

Estimating β i

J

j=1 i

(1) Use ˆ from the class with the largest estimated probability

(2) Probabilistic

ˆ (^) = Posterior Prob[class=j|data ]ˆ ∑

j

i j

β

β β

How Many Classes?

(1) J is not a 'parameter' - can't 'estimate' J with

and

(2) Can't 'test' down or 'up' to J by comparing

log likelihoods. Degrees of freedom for J+

vs. J classes is not well define

π β

1

2

1

d.

(3) Use AKAIKE IC; AIC = -2 logL + 2#Parameters.

AIC 10827.

AIC 9954.

AIC 9958.

×

=

= <===

=

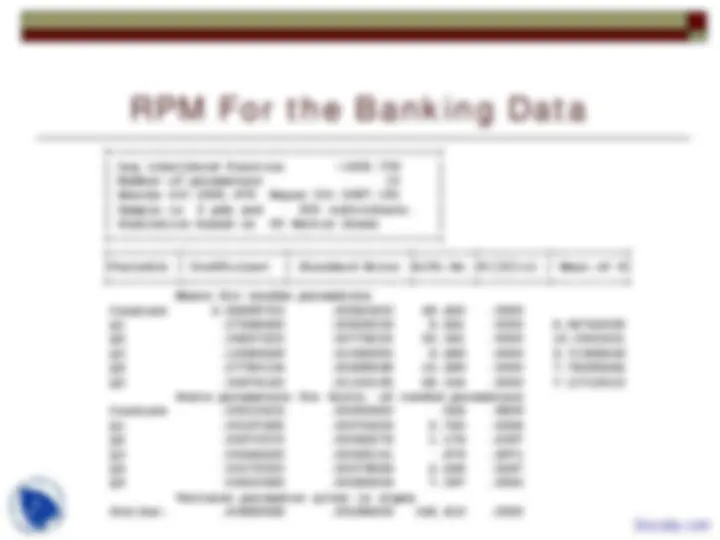

Banking Data

An LCM for US Banks

+---------------------------------------------+ | Latent Class / Panel LinearRg Model | | Number of observations 2500 | | Log likelihood function -722.4603 | | Number of parameters 23 | | Akaike IC= 1490.921 Bayes IC= 1624.874 | | Sample is 5 pds and 500 individuals. | +---------------------------------------------+ +---------+--------------+----------------+--------+---------+ |Variable | Coefficient | Standard Error |b/St.Er.|P[|Z|>z] | +---------+--------------+----------------+--------+---------+ Model parameters for latent class 1 Constant 2.12699463 .29651372 7.173. Q1 .12099446 .03964929 3.052. Q2 .36291987 .03752392 9.672. Q3 .10728655 .05245420 2.045. Q4 .12785217 .02482950 5.149. Q5 .39535779 .06081496 6.501. Sigma .71931764 .02537027 28.353. Model parameters for latent class 2 Constant 2.51877624 .06958519 36.197. Q1 .05918445 .00899501 6.580. Q2 .44083356 .00930001 47.401. Q3 .23897724 .01492919 16.007. Q4 .04896772 .00484760 10.101. Q5 .16105964 .01307985 12.314. Sigma .18434496 .00520057 35.447. Model parameters for latent class 3 Constant 3.83600468 .10233076 37.486. Q1 .08904293 .01502856 5.925. Q2 .33710302 .01266856 26.609. Q3 -.01256845 .01987228 -.632. Q4 .06333872 .00782013 8.099. Q5 .42847054 .02326421 18.418. Sigma .23914408 .00872954 27.395. Estimated prior probabilities for class membership Class1Pr .24778109 .02112395 11.730. Class2Pr .45386105 .03497825 12.976. Class3Pr .29835786 .03472726 8.591.

Implementing EM

0 0 0 0 j 1 2 J 0 0 0 0 j 1 1 1

0 j

1 N -1 N j i 1 i 1

N 1 2 i 1^ j ,j (^) N i 1 i

j ,j N j i=

= =

= ε =

ε

i i i i

i i

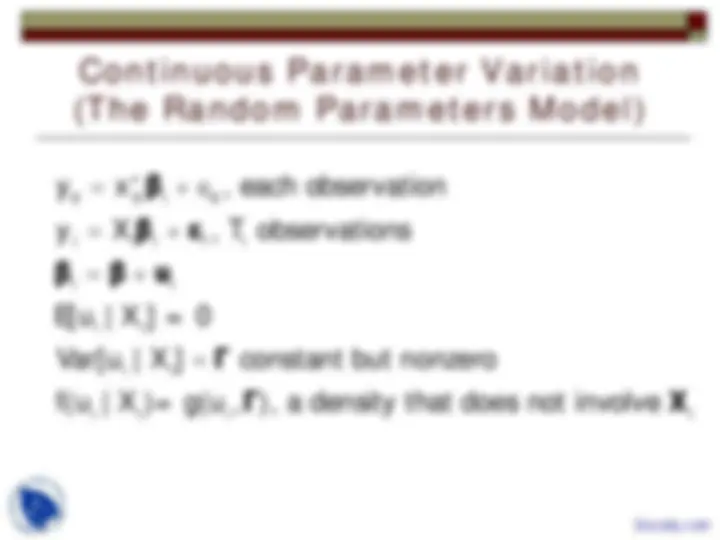

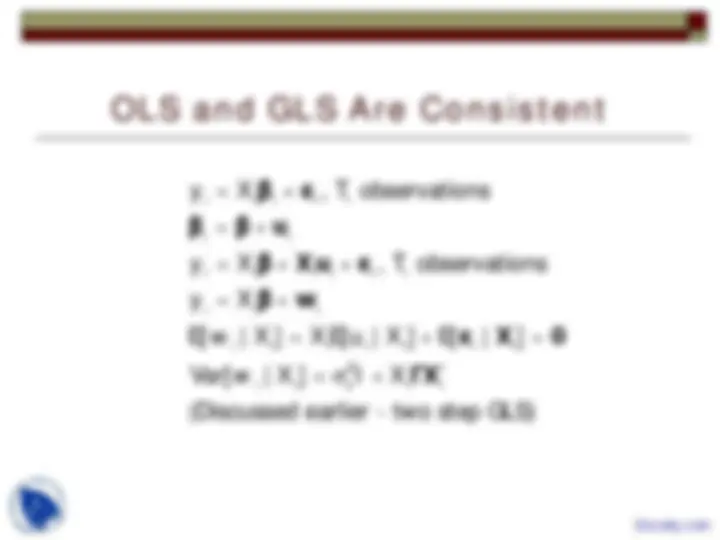

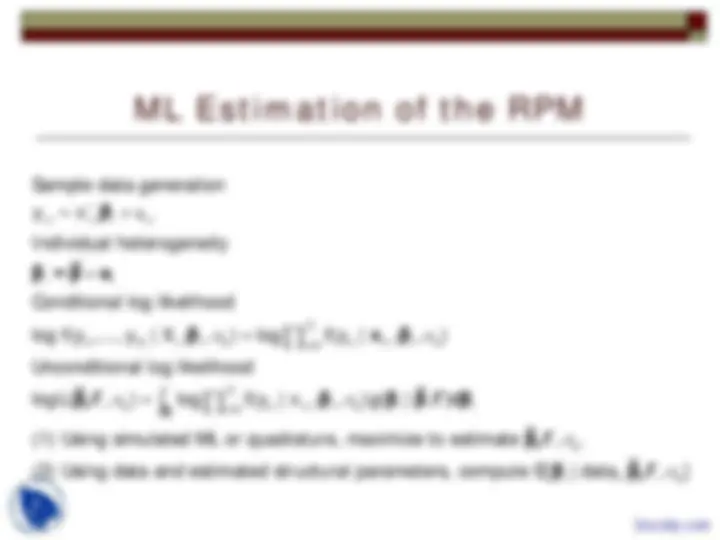

Continuous Parameter Variation

(The Random Parameters Model)

it it

i i

i

i i

i i

i i i i

y , each observation

, T observations

E[ | ] =

Var[ | ] constant but nonzero

f( | )= g( , ), a density that does not involve

= ′ + ε

= +

= +

=

it i

i i i

i

x β

y X β ε

β β u

u X 0

u X Γ

u X u Γ X