Part II – Ratio Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Includes all types of ratios with appropriate equations.

Typology: Summaries

1 / 20

This page cannot be seen from the preview

Don't miss anything!

Inventory Turnover and DOH Inventory turnover indicates the resources tied up in inventory (i.e., the carrying costs) and, therefore, can be used to indicate inventory management effectiveness. In general, inventory turnover and DOH (days of inventory on hand) should be benchmarked against industry norms. Receivables Turnover and DSO The number of DSO (days of sales outstanding) reflects how fast the company collects cash from customers to whom it offers credit. Although limiting the numerator to sales made on credit in the receivables turnover would be more appropriate, credit sales information is usually not available to analysts; therefore, revenue as reported in the income statement is generally used. Payables Turnover and the Number of Days of Payables The number of days of payables reflects the average number of days the company takes to pay its suppliers, and the payables turnover ratio measures how many times per year the company theoretically pays off all its creditors.

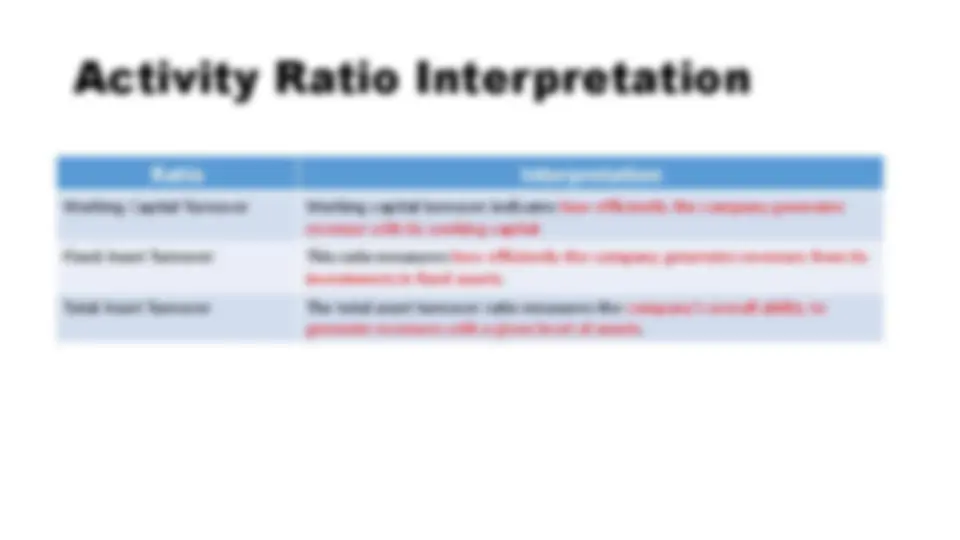

Working Capital Turnover Working capital turnover indicates how efficiently the company generates revenue with its working capital. Fixed Asset Turnover This ratio measures how efficiently the company generates revenues from its investments in fixed assets. Total Asset Turnover The total asset turnover ratio measures the company’s overall ability to generate revenues with a given level of assets.

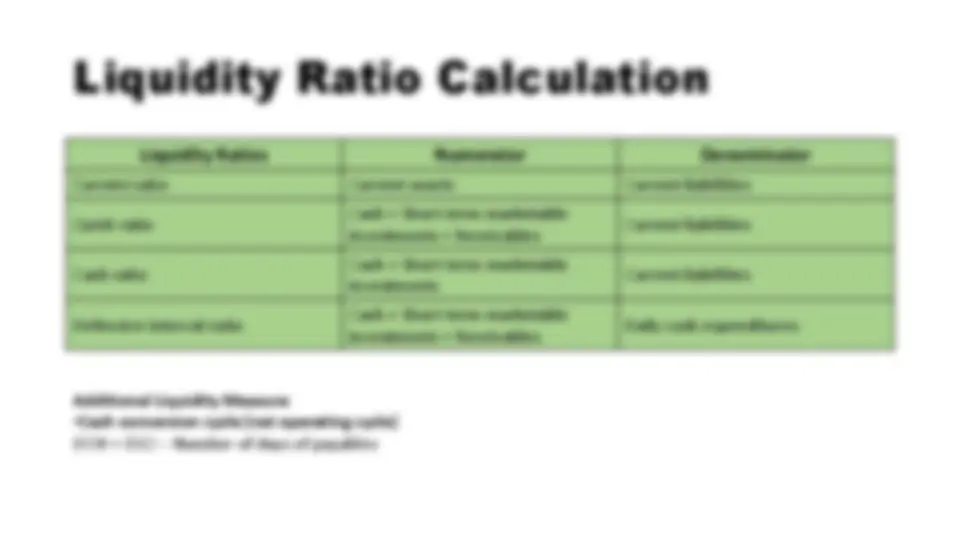

Current ratio Current assets Current liabilities Quick ratio Cash + Short-term marketable investments + Receivables Current liabilities Cash ratio Cash + Short-term marketable investments Current liabilities Defensive interval ratio Cash + Short-term marketable investments + Receivables Daily cash expenditures Additional Liquidity Measure

Current Ratio The current ratio implicitly assumes that inventories and accounts receivable are indeed liquid. A higher current ratio indicates a higher level of liquidity. (i.e., a greater ability to meet short-term obligations) Quick Ratio The quick ratio is more conservative than the current ratio because it includes only the more liquid current assets (sometimes referred to as “quick assets”) in relation to current liabilities. Like the current ratio, a higher quick ratio indicates greater liquidity. Cash Ratio The cash ratio normally represents a reliable measure of an entity’s liquidity in a crisis situation. Only highly marketable short-term investments and cash are included. Defensive Interval Ratio The defensive interval ratio measures how long the company can continue to pay its expenses from its existing liquid assets without receiving any additional cash inflow. Cash Conversion Cycle (Net Operating Cycle) The cash conversion cycle metric indicates the amount of time that elapses from the point when a company invests in working capital until the point at which the company collects cash.

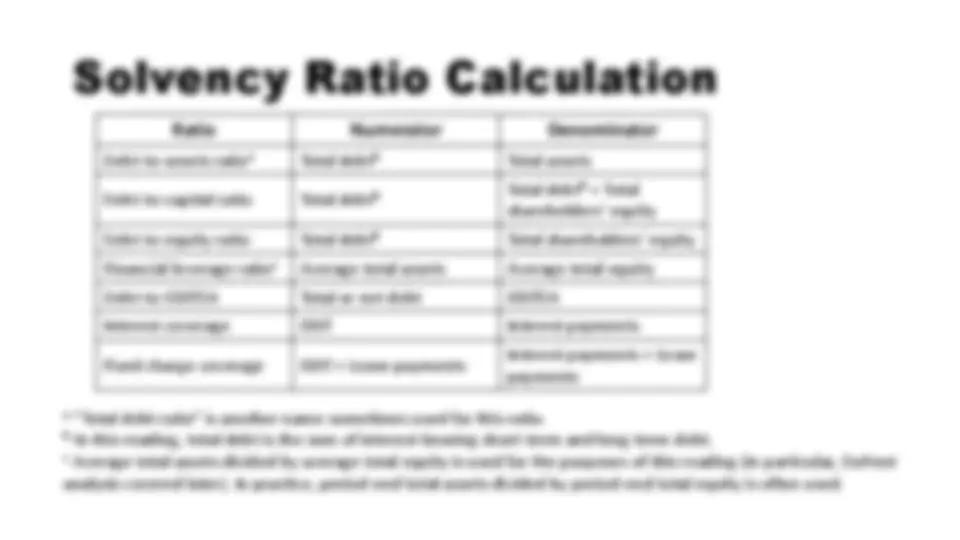

Debt-to-assets ratioᵃ Total debtᵇ Total assets Debt-to-capital ratio Total debtᵇ Total debtᵇ + Total shareholders’ equity Debt-to-equity ratio Total debtᵇ Total shareholders’ equity Financial leverage ratioᶜ Average total assets Average total equity Debt-to-EBITDA Total or net debt EBITDA Interest coverage EBIT Interest payments Fixed charge coverage EBIT + Lease payments Interest payments + Lease payments ᵃ “Total debt ratio” is another name sometimes used for this ratio. ᵇ In this reading, total debt is the sum of interest-bearing short-term and long-term debt. ᶜ Average total assets divided by average total equity is used for the purposes of this reading (in particular, DuPont analysis covered later). In practice, period-end total assets divided by period-end total equity is often used.

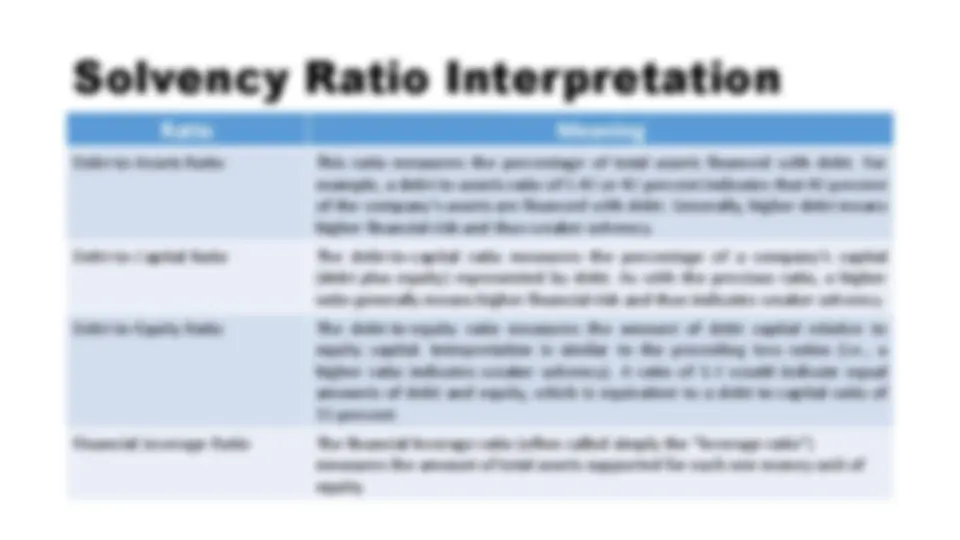

Debt-to-Assets Ratio This ratio measures the percentage of total assets financed with debt. For example, a debt-to-assets ratio of 0. 40 or 40 percent indicates that 40 percent of the company’s assets are financed with debt. Generally, higher debt means higher financial risk and thus weaker solvency. Debt-to-Capital Ratio The debt-to-capital ratio measures the percentage of a company’s capital (debt plus equity) represented by debt. As with the previous ratio, a higher ratio generally means higher financial risk and thus indicates weaker solvency. Debt-to-Equity Ratio The debt-to-equity ratio measures the amount of debt capital relative to equity capital. Interpretation is similar to the preceding two ratios (i.e., a higher ratio indicates weaker solvency). A ratio of 1. 0 would indicate equal amounts of debt and equity, which is equivalent to a debt-to-capital ratio of 50 percent. Financial Leverage Ratio The financial leverage ratio (often called simply the “leverage ratio”) measures the amount of total assets supported for each one money unit of equity.

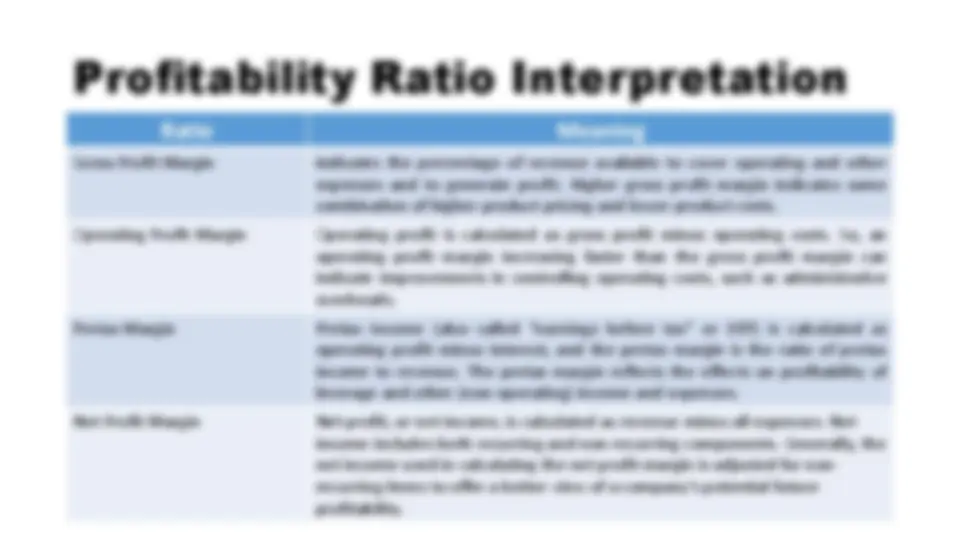

Profitability Ratios Numerator Denominator Return on Salesᵃ

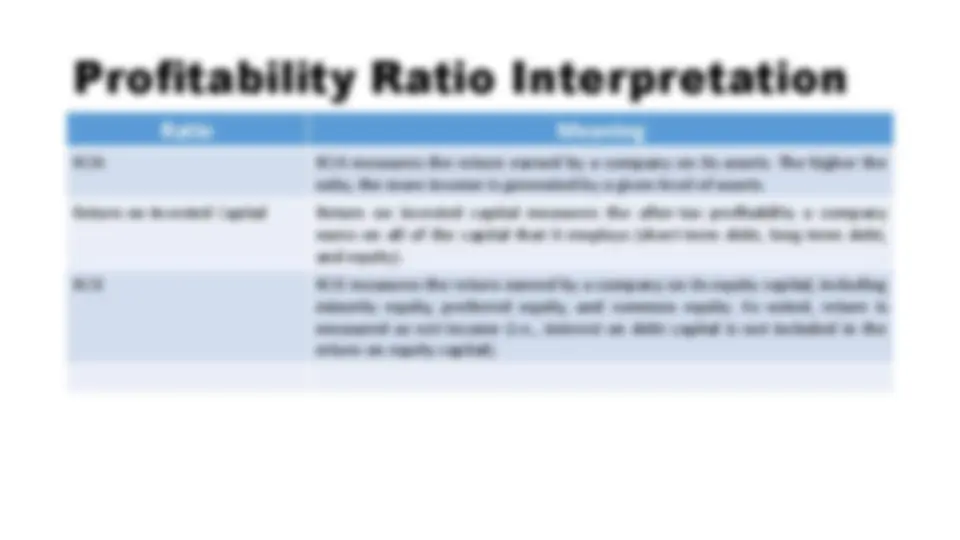

ROA ROA measures the return earned by a company on its assets. The higher the ratio, the more income is generated by a given level of assets. Return on Invested Capital Return on invested capital measures the after-tax profitability a company earns on all of the capital that it employs (short-term debt, long-term debt, and equity). ROE ROE measures the return earned by a company on its equity capital, including minority equity, preferred equity, and common equity. As noted, return is measured as net income (i.e., interest on debt capital is not included in the return on equity capital).