Unit–II

Module‐III

RatioAnalysis

PracticalProblems

(WithSolutions)

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Ratio Analysis of ITC Limited Company

Typology: Study Guides, Projects, Research

1 / 34

This page cannot be seen from the preview

Don't miss anything!

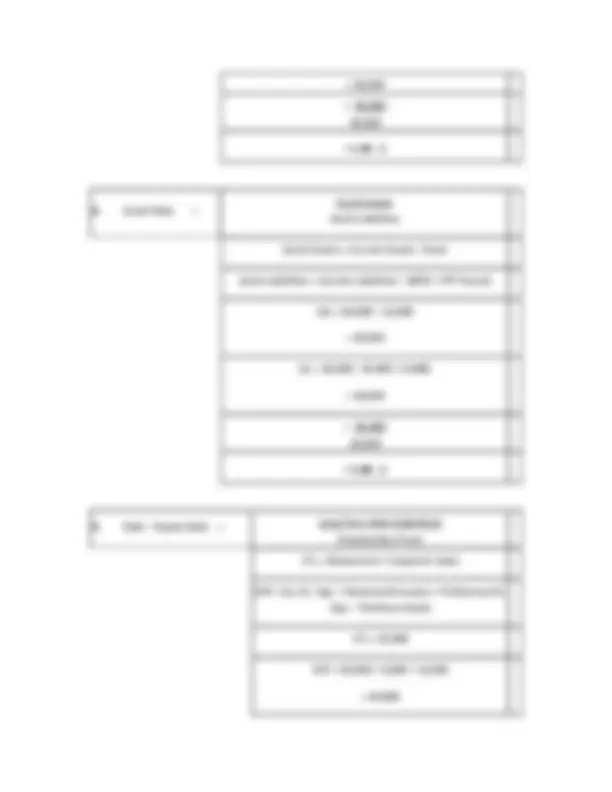

The following Trading and Profit and Loss Account of Fantasy Ltd. for the year 31 ‐ 3 ‐ 2000 is given below: Particular Rs. Particular Rs. To Opening Stock “ Purchases “ Carriage and Freight “ Wages “ Gross Profit b/d To Administration expenses “ Selling and Dist. expenses “ Non‐operating expenses “ Financial Expenses Net Profit c/d

By Sales “ Closing stock By Gross Profit b/d “ Non‐operating incomes: “ Interest on Securities “ Dividend on shares “ Profit on sale of shares

Calculate:

1. Gross Profit Ratio 2. Expenses Ratio 3. Operating Ratio 1. Net Profit Ratio 5. Operating (Net) Profit Ratio 6. Stock Turnover Ratio.

1. Gross Profit Margin = Gross profit Sales

2. Expenses Ratio = Op. Expenses Net Sales

6. Stock Turnover Ratio = Cost of goods sold Avg. Stock 3,00, 87, = 3.43 times

The Balance Sheet of Punjab Auto Limited as on 31 ‐ 12 ‐ 2002 was as follows: Particular Rs. Particular Rs. Equity Share Capital Capital Reserve 8% Loan on Mortgage Creditors Bank overdraft Taxation: Current Future Profit and Loss A/c

Plant and Machinery Land and Buildings Furniture & Fixtures Stock Debtors Investments (Short‐term) Cash in hand

From the above, compute (a) the Current Ratio, (b) Quick Ratio, (c) Debt‐Equity Ratio, and (d) Proprietary Ratio.

1. Current Ratio = Current Assets Current liabilities Current Assets = Stock + debtors + Investments (short term) + Cash In hand Current Liabilities = Creditors + bank overdraft + Provision for Taxation (current & Future) CA = 12000 + 12000 + 4000 + 12000 = 40, CL = 16000 + 4000 + 4000 + 4000

2. Quick Ratio = Quick Assets Quick Liabilities Quick Assets = Current Assets ‐ Stock Quick Liabilities = Current Liabilities – (BOD + PFT future) QA = 40,000 – 12, = 28, QL = 28,000 – (4,000 + 4,000) = 20, = 28, 20, = 1.40 : 1 3. Debt – Equity Ratio = Long^ Term^ Debt^ (Liabilities) Shareholders Fund LTL = Debentures + long term loans SHF = Eq. Sh. Cap. + Reserves & Surplus + Preference Sh. Cap. – Fictitious Assets LTL = 32, SHF = 40,000 + 8,000 + 12, = 60,

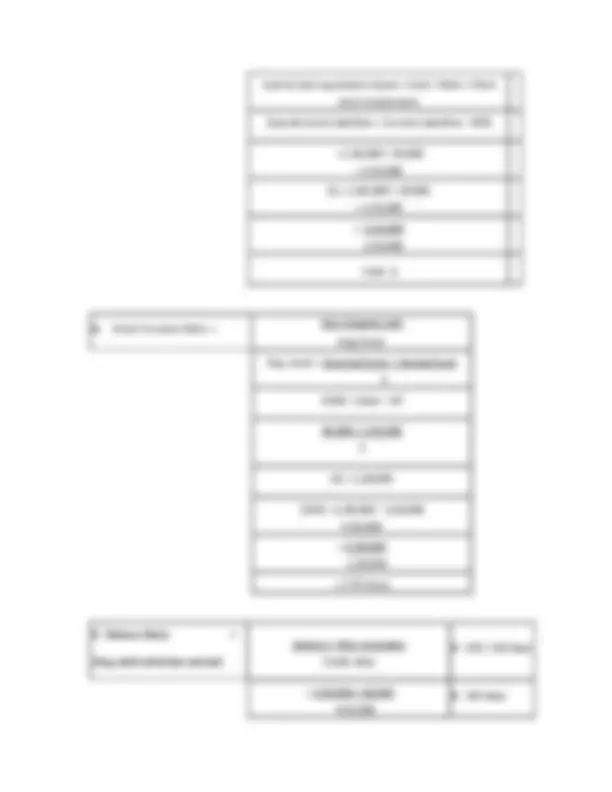

Balance Sheet Particular Rs. Particular Rs. Equity share capital 10% Preference share capital Reserves 10% Debentures Creditors Bank‐overdraft Bills payable Outstanding expenses

Fixed Assets Stock Debtors Bills receivable Cash Fictitious Assets

Beside the details mentioned above, the opening stock was of Rs. 3,25,000. Taking 360 days of the year, calculate the following ratios; also discuss the position of the company: (1) Gross profit ratio. (2) Stock turnover ratio. (3) Operating ratio. (4) Current ratio. (5) Liquid ratio. (6) Debtors ratio. (7) Creditors ratio. (8) Proprietary ratio. (9) Rate of return on net capital employed. (10) Rate of return on equity shares.

1. Gross Profit Margin = Gross profit Sales

2. Stock Turnover Ratio = Cost of goods sold Avg. Stock Avg. stock = Opening Stock + Closing Stock 2 COGS = Sales – GP 3,25,000 + 1,75, 2

= 3 times

3. Operating Profit Ratio = Op. Profit Net Sales

Operating Profit = Sales – (Op. Exp. + COGS.) OP = 15,00,000 – (7,50,000 + 1,25,000 + 25,000) = 6,00, (excluding Interest on Debentures) = 6,00, 15,00,

4. Current Ratio = Current Assets Current liabilities Current Assets = Stock + debtors + Bills receivable + Cash Current Liabilities = Creditors + bank overdraft + Bills payable + Outstanding expenses CA = 1,75,000 + 3,50,000 + 50,000 + 2,25, = 8,00,

7. Creditors Ratio = Creditors^ +^ Bills^ payable Credit Purchase X 365 / 360 days = 1,00,000 + 45, 7,50, Notes: If credit purchase could not find out at that point Cost of Goods sold consider Credit purchase X 360 days = 0.193 X 360 days = 69 days 8. Proprietary Ratio = Shareholders’ Funds Total Assets SHF = Eq. Sh. Cap. + Reserves & Surplus + Preference Sh. Cap. – Fictitious Assets Total Assets = Total Assets – Fictitious Assets SHF = 20,00,000 + 20,00,000 + 11,00,000 – 1,00, = 50,00, TA = 64,00,000 – 1,00, = 63,00, = 50,00, 63,00, = 0.79 : 1

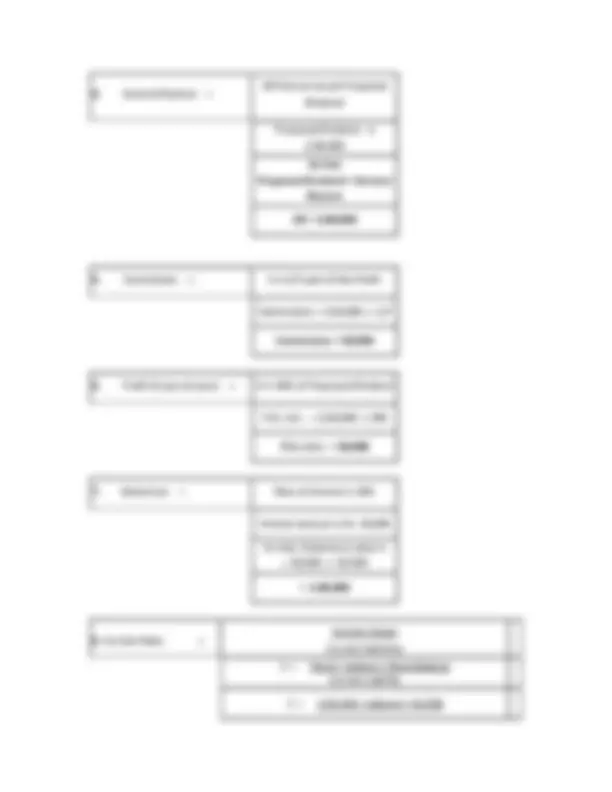

1. Gross Profit Margin = Gross profit Sales

Sales

Sales = 1,50, 25

Sales = 6,00,

2. Current Ratio = Current Assets Current liabilities Current Assets = Stock + debtors + Bills receivable + Cash + Bank Balance Current Liabilities = Creditors + Bills payable CA = 1,44,000 + 1,50,000 + 60,000 + 1,20,000 + 96, = 5,70, CL = 1,05,000 + 30, = 1,35, = 5,70, 1,35, = 4.22 : 1 3. Acid Test Ratio = Cash & Cash Equivalent Assets Liquid Liabilities

Cash & Cash equivalent Assets = Cash + Bank + Short term Investments (Liquid) Quick Liabilities = Current Liabilities – BOD = 1,20,000 + 96, = 2,16, QL = 1,05,000 + 30, = 1,35, = 2,16, 1,35, = 1.6 : 1

4. Stock Turnover Ratio = Cost of goods sold Avg. Stock Avg. stock = Opening Stock + Closing Stock 2 COGS = Sales – GP 96,000 + 1,44, 2 AS = 1,20, COGS = 6,00,000 – 1,50, 4,50, = 4,50, 1,20, = 3.75 times 5. Debtors Ratio = (Avg. debt collection period) Debtors + Bills receivable Credit sales X 365 / 360 days = 1,50,000 + 60, 4,56, X 365 days

2. Proprietary Ratio = Shareholders’ Funds Total Assets SHF = Eq. Sh. Cap. + Reserves & Surplus + Preference Sh. Cap. – Fictitious Assets Total Assets = Total Assets – Fictitious Assets SHF = 10,00,000 + 7,00,000 + 4,00,000 ‐ 20, = 20,80, TA = 30,00,000 – 20, = 29,80, = 20,80, 29,80, = 0.70 : 1 3. Debt – Equity Ratio = Long^ Term^ Debt^ (Liabilities) Shareholders Fund LTL = Debentures + long term loans SHF = Eq. Sh. Cap. + Reserves & Surplus + Preference Sh. Cap. – Fictitious Assets LTL = 5,00, SHF = 10,00,000 + 7,00,000 + 4,00,000 ‐ 20, = 20,80, = 5,00, 20,80, = 0.24 : 1 4. Capital Gearing Ratio = Fixed^ Interest^ or^ Dividend^ Securities Equity Shareholders Fund FIS = Debentures + Preference share capital

Additional Information: 2002 ‐'03 2003 ‐ 04 Rs. Rs. (1) Sales 3,65,000 2,19, (2) Cost of Goods sold 2,19,000 1,46, (3) Net profit (Before Pref. Dividend) 35,000 47, (4) Stock on 1 ‐ 4 ‐'02 71,000 ‐‐‐ Calculate following ratios and give your opinion about company position in 2003 ‐'04 in comparison with 2002 ‐'03. Whether it is positive or negative? (1) Current ratio (2) Liquid ratio (3) Debtors ratio (Take 365 days for calculations) (4) Gross profit ratio (5) Stock Turnover ratio (6) Rate of return on equity share‐holders' funds.

1. Current Ratio = Current Assets Current liabilities Current Assets = Stock + debtors + Bills receivable + Cash + Bank Balance Current Liabilities = Creditors + Bills payable 2002 ‐03: = 53,000 +20,000 + 75,000 + 15,000 + 2, 30,000 + 10,000 + 10,000 + 5, = 1,65, 55, = 3 : 2003 ‐04: = 30,000 + 12,000 + 90,000 + 35,000 + 13, 35,000 + 25,000 + 20,000 + 10, = 1,80, 90, = 2 : 1 2. Liquid Ratio = Liquid Assets Liquid liabilities

(Liquid) Quick Assets = Current Assets ‐ Stock (Liquid) Quick Liabilities = Current Liabilities – BOD 2002 ‐03: = 1,65,000 ‐ 75, 55,000 ‐ 10, = 90, 45, = 2 : 2003 ‐04: = 1,80,000 ‐ 90, 90,000 ‐ 20, = 90, 70, = 1.29 : 1

3. Debtors Ratio = (Avg. debt collection period) Debtors + Bills receivable Credit sales X 365 / 360 days 2002 ‐03: = 53,000 + 20, 3,65, X 365 days = 73, 3,65, X 365 days = 73 days 2003 ‐04: = 30,000 + 12, 2,19, X 365 days = 42, 2,19, X 365 days = 70 days