Download Recent Corporate Restructuring in China and more Schemes and Mind Maps Corporate Finance in PDF only on Docsity!

Corporate Restructuring in China

Cases of Listing as Consolidated Business Group

Re-Jin Guo Department of Finance College of Business Administration University of Illinois Chicago, IL 60607

and Visiting Financial Economist Research Center Shanghai Stock Exchange South Pudong Road Shanghai, P.R.China

August 2006 Abstract Recent regulatory changes in China have significantly increased the sensitivity of wealth of controlling shareholders to the market value of the firm. As a result, some controlling shareholders voluntarily engage in transactions which streamline and consolidate the business operations of firms within the same business group. This study makes a detailed analysis of three important corporate restructuring transactions. All three corporate restructuring transactions resulted/ will result in the listing of a consolidated business group. My analyses illustrate that those restructuring transactions, though initiated by large controlling shareholders, enhance firm value and benefit both large and minority shareholders at the same time within the framework of deal structure, market infrastructure, as well as the present regulation. Recommendations on changes of the marker regulation are made accordingly.

I would like to thank Ruyin Hu, Chun Chang, Fenghua Wang, Xiang Jian, Donghui Shi, Wen- Wei Zhou, Wen-Ying Lu, Huai-Zhong Yuan, and seminar participants at the Shanghai Stock Exchange for helpful comments and suggestions. All errors remain mine. Please contact Re-Jin Guo, Department of Finance, School of Business Administration, University of Illinois.

I. Introduction

Dated from the reopening of Shanghai Stock Exchange for trading in late 1990, the regulatory agency in China has stipulated that firm shares traded in local market be composed of multiple classes ( 股 权 分 置 ). Various governmental institutions jointly issued the Regulated Comments on Stock Corporation (股份公司规范意见) in May, 1992. This policy on multiple share classes is further reinforced in 1994 by various official documents stating, “The government needs to ensure a dominant and controlling ownership in corporations operating in specific, important, and influential industries for the domestic economy (through state shares/legal person shares)”;” … dominant and controlling ownership refers to a stock holdings of more than 50% ……”.

Multiple share classes in China consist of (1) state shares (2) legal person shares, and (3) common A shares^1. State shares are share holdings by the central government, local government, or government-owned enterprises. Legal person shares are ownership by business agencies, and enterprises of local governments that helped in starting up the public companies (Sun and Tong, 2003). These three multiple classes of stocks, distinctly different from stock classes in the other countries, carry the same cash flow and voting rights per share. It is the method of exchange/transfer which distinguishes the three classes of stocks: A-shares are floated in the stock market and traded among investors; while state and legal person shares are not publicly-traded and can only be held by corporate and legal-entity institutions. As a result, the state and RIS shares are fairly illiquid (Chen and Xiong, 2001), and the free float (freely tradable shares available to the investors) is extremely low in Chinese market. It is estimated that the free float ratio was 33.2% in 2001 in China, compared to 86.4% and 77.5% in developed and other emerging markets (Gao, 2002).

(^1) In addition to A shares, which are traded among domestic investors, there are B shares trading in China for foreign investors. There are also H, N, L, and S shares, available for investors in global markets and listed in Hong Kong, New York, London, and Singapore, respectively.

between tradable and non-tradable shares. It stipulated that all shares of listed firms shall be freely traded by the yearend of 2006. In effect, the new regulation has re-connected the important link between the wealth of large shareholders and firm value. In this article, I suggest that some firms respond to the reform on non-tradable shares (股权分置改革) by voluntarily engaging in transactions which streamline and consolidate the business operations of firms within the same business group. This paper exemplifies such cases of corporate restructuring and makes a detailed analysis of three important corporate restructuring transactions. All three corporate restructuring transactions resulted/ will result in the listing of a consolidated business group (整体上市).

My analyses illustrate that those restructuring transactions, though initiated by large controlling shareholders, enhance firm value and benefit both large and minority shareholders at the same time. In some cases, the parent business group voluntarily infuses good assets into its listed subsidiary to be traded as consolidated business group. Such transaction enhances both the wealth of large shareholders and firm value, while at the same time greatly reduces the potential tunneling channel through related party transactions. The restructuring of Angan New Steel is a good case of corporate consolidation via asset infusion^3.

In other cases, the business group conducts freeze-out transactions, in which the parent firm buys back the minority shares of subsidiary firm using a cash or stock offer. After the freeze-out, the subsidiary firm would be delisted from stock exchange, and would be dissolved and its assets absorbed by the parent. Consequently, the combined assets would be traded as a consolidated business group. In this paper, the restructuring of TCL Group is a case of freeze-out transaction using stock offer, while the restructuring of Sinopec is a case of freeze-out using a cash offer. Analysis of these two cases illustrates the legal and valuation process of freeze-out transactions in China.

(^3) How the restructuring transaction is formulated is related to implicit rules which the China Securities Regulatory Commission (中国证监会) would impose in reviewing the case at that time. It is noted that the public securities issuances are heavily regulated in China, and are subject to CSRC’s approval.

The remainder of this paper is organized as follows. Section two provides a review of how the judicial system place legal limits on controlling shareholders and discusses important cases on freeze-out transactions in the U.S. market. Section three describes the deal structure and implementation process of three transactions of corporate restructuring in China: Consolidation of TCL Group (TCL集团), now considered as a classical case of corporate restructuring in Chinese market; consolidation of An-Gang New Steel group (鞍钢新轧钢股份), as well as the on-going corporate restructuring for Sinopec (中石化集团). Section four provides the theoretical framework used in analyzing merger and acquisition transactions, and provide the valuation analysis for those three transactions. Section five provides recommendations on changes of the marker regulation and concludes the paper.

II. U.S. Judicial System on Controlling Shareholder Behavior

Presence of large shareholders could mitigate the agency conflict arising between mangers and shareholders. However, conflicts could also arise between controlling and non-controlling shareholders, as (private) benefits of control accrued to the controlling shareholders are not shared with the non-controlling shareholders. Controlling shareholders could extract their private benefits in the following three ways: by taking a disproportionate amount of firm’s assets/earnings; by selling their controlling ownership; or by freezing out the minority shareholders. The judicial system in every market imposes legal boundaries on extraction of private benefits by controlling shareholders, and provides protection on minority shareholders.

In a seminal paper by La Porta, Lopez-de-Silanes, Shleifer, and Vishny (LLSV, 2000), the authors discuss the difference in laws and the effectiveness of their enforcement across countries, and argue that legal approach of accessing how investors are protected by law from the expropriation by managers and large shareholders is important in evaluating corporate governance across markets. In a subsequent paper, LLSV further provide empirical evidence based on 539 firms in 27 wealthy economics that firm valuation is higher in countries with better protection of minority shareholders.

(2) The material facts as to the director’s or officer’s relationship or interest and as to the contract or transaction are disclosed or are known to the shareholders entitled to vote thereon, and the contract or transaction is specifically approved in good faith by vote of the shareholders; or (3) The contract or transaction is fair as to the corporation as of the time it is authorized, approved, or ratified, by board of directors, a committee or the shareholders.”

The U.S. Delaware Supreme Court further specifies two categories of private benefits. The first category considers the business and strategic decision of the controlled corporation. The court system refers to the decision in the first category as “business judgments”. The second category considers the controlling shareholder’s direct dealing with the controlled corporation (such as transfer pricing, transfer of assets, use of controlled firm’s assets as collateral for controlling shareholders’ debt). A higher legal standard is imposed on the transactions in the second category. If there is a chance that the controlling shareholders could benefit and disadvantage the controlled corporation in any way, the more rigorous “fairness standard” applies. If fairness standard applies, it would be at the controlling shareholders’ burden to prove that the transaction is fair. In effect, there is a limit on the private benefits for the controller associated with firm operation by the judicial system.

Alternatively, the controlling shareholder could wish to sells its control, usually at a premium reflecting the value of the private benefits from operating the controlled firm. There exists much less legal intervention in such transactions, based on the consideration that minority shareholders could share gains if the incoming controller would increase the (common) value of the firm 4. In addition, the private benefits from operating the controlled firm are presumably limited by legal rules. As a result, the value of control

(^4) There are exceptions. Rules exist to restrict controlling shareholders’ rights to sell their control at a premium if “(a) The controlling shareholder does not make disclosure concerning the transaction to other shareholders with whom the controlling shareholders deal in connection with the transaction; or (b) It is apparent from the circumstances that the purchaser is likely to violate the duty of fair dealing in such a way as to obtain a significant financial benefit from the purchaser or an associate.”

could be larger when capital markets are less developed. Dyck and Zingales (2004), based on 393 control transactions of 39 countries in 1990-2000, report an average 14% control premium for such transactions. The authors also report that a higher degree of statutory protection of minority shareholders and a higher degree of law enforcement are associated with a lower level of control premium.

Finally, the controlling shareholders may wish to freeze out minority shareholders. In such transactions, the controlling shareholder can easily benefit as the marker price of a controlled cooperation reflects a discount resulting from the controller’s private benefits. There exists intensive legal intervention should the controller takes the opportunities to expropriate minority shareholders such transactions in the U.S..

Freeze-outs are also called going-private transactions. In such transaction, a controlling stockholder typically acquires the shares of the minority shareholders in a public company in exchange for cash, debt or stock, resulting in the delisting of the company (McGuinness and Rehbock, 2005). There exist two approaches to implementing freeze-out transactions in the U.S. under its current judicial landscape. In the first (traditional) approach, the controlling shareholder announces its intention to acquire the publicly held minority shares, delivers a proposal to the target company, and files schedule 13D/13G with the Securities and Exchange Commission (SEC) describing it proposal. The target firm responds with establishing a special committee consisting only of independent directors to evaluate the delivered proposal on behalf of its minority shareholders. The special committee retains its own financial and legal advisors, and is authorized to negotiate with the controlling shareholder. If negotiation between the special committee and the controlling shareholder is successful, the determined price and other terms/conditions of the freeze-out offer would be announced and recommended by the special committee to the shareholders in a merger agreement. The transaction would be completed subsequently pursuant to the terms of the merger agreement.

Delaware Supreme Court’s decision in Weinberger v. UOP, Inc. in 1983 shaped the legal standard applied to the traditional freeze-outs. In this case, Signal corporation

In contrast, in the case of Weinberger v. UOP, Inc., the controller was subject to a class action in which the price exposure was substantial. The Delaware court determined that the freeze-out merger was not a fair transaction since there was a breach of fiduciary duty of loyalty by those affiliated directors to shareholders. The court’s judgment reads “ While a plaintiff’s monetary remedy ordinarily should be confined to more liberalized appraisal proceeding ….. the appraisal remedy we approve may not be adequate in certain cases, particularly where fraud, misrepresentation, self-dealing, deliberate waste of corporate assets, or gross and palpable overreaching are involved. Under such circumstances, the Chancellor’s powers are complete to fashion any form of equitable and monetary remedy as may be appropriate, including recissory damages”. In the end, the court found that the purchase price of UOP share should have been $22.

Dated from 2001 case of re Soliconix Inc. Shareholders Litigation, an alternative (unilateral) approach has been used in the U.S. freeze-outs. In this approach, the controlling shareholder determines the price and other terms/conditions of its cash offer unilaterally. The controlling stockholder publicly announces an intention to launch a tender offer. The target often responds with establishing a special committee consisting of only independent directors. The special committee retains independent financial and legal advisors, evaluate the controlling shareholder’s proposal, and publicly announce its recommendation of acceptance, rejection, or no position of the tender offer. If more than 90% of the shares of each class of voting stocks are tendered, the controlling shareholder then can conduct a short-form merger by filing a certificate with the State of Delaware to freeze out any non-tendering stockholders.

The Williams Act and 1934 Act require increased disclosure to prevent outsiders from taking advantage of ill-informed decisions:

- Under §14(d)(1), the party presenting a tender offer must disclose a. its identity and background b. the source of funds used to make the purchase, and

c. the purpose of the purchase, including any plans to liquidate or change corporate structure.

- a tender offer must remain open for 20 business days, blocking a bidder’s effort to force hasty decisions. SEC Rule 14e-1(a).

- if more shares are tendered than the bidder sought to purchase, the bidder must buy a pro rata portion from each shareholder. This prevents use of a first-come, first-served strategy to pressure shareholders. §14(d)(6) of the 1934 Act.

- Bidder must pay the same price for all shares purchased. §14(d)(7).

In re Soliconix Inc. Shareholders Litigation, Vishnay Intertechnology first announced the acquisition of 20% of Siliconix shares from minority shareholders with a cash tender offer. A special committee of Siliconix independent directors was established to respond to Vishnay’s proposal. Vishnay later decided to sidestep the Siliconix and replaced the cash offer with a stock-for-stock offer. The Siliconix special committee communicated its intention to reject the new offer, but however, did not make any public disclosure in SEC documents. A motion for injunction was brought to the court to intervene with the stock-for-stock offer.

The court determined that when a freeze-out transaction is executed using the unilateral approach, the business judgment rule (instead of the entire fairness standard) would be applied. It was determined that Vishnay had no obligation to demonstrate the “entire fairness” of its proposed tender offer, and that the Siliconix directors did not breach their duty of care of loyalty to minority shareholders. The Delaware court clearly distinguished the position of the board in a merger and a tender offer:

“[U]nder the corporation law, a board of directors which is given the critical role of initiating and recommending a merger to the shareholders traditionally has been accorded no statutory role whatsoever with respect to merger and tender offer is not satisfactory explained by the observation that the corporation law statues were basically designed in a

excluding gains associated with the appreciation of subsidiary shares, are statistically similar to the returns for acquirers in M&A transactions. The minority shareholders also received 11% more than their pro rata share during the announcement period. These results are consistent with the argument that the legal standard and economic incentives are sufficient in protecting minority share interests in the U.S. market.

We have not been able to observe judgments from the court system on freeze-out transactions from Chinese judiciary system. Therefore, judgement could not be made the effectiveness of judiciary system on the protection of minority interest in China. How the merger and acquisition market evolves in China would be closely related to the rules/regulations implemented by regulatory agencies and exchanges. Chapter 4 of the Securities Act covers the regulation on takeover of listed firms. The Regulation on Acquisition of Publicly Listed Firms ( 上 市 公 司 收 购 管 理 办 法 ), published in 2002, provides a set of guidelines of how to formulate a transaction structure and more detailed legal specifications on corporate acquisition than the Securities Act. These guidelines range from the declaration of basic principles behind the transaction (for example, Rule 4 states that the merger and acquisition transactions should be fair, and the agents involved in the transactions should be honest and trustworthy); to transaction specifics (for example, Chapter 3 of the Regulation on Acquisition of Publicly Listed Firms (上市公司 收购管理办法) specifies the rules for tender offers. Specifically related to freeze-out transactions, rule 27 requires special notice on the tender offer documents on the intended delisting after the completion of the tender offer. Rule 31 also specifies that the board of the tender-off target should hire independent financial advisor to provide profession opinions on the proposed transactions. Rule 34 also specifies that the purchase price in a tender offer should be the higher of purchase price paid in prior transactions within six months, or 90% of average stock price in the prior thirty days). The rules are comprehensive, but always subject to interpretation.

There are also related disclosure requirements for the tender offer report in China (contents and format rule #17 for public firms). The basic disclosure requirements include: (1) basic information on the party lunching the tender offer, (2) terms of the

tender offer, (3) acquirer’s change in target’s shares in the six prior to the tender offer, (4) source of the capital for share purchase, (4) operating plan on the target firm after the tender offer, (5) important related-party transactions between the acquirer and the target, (6) report from professional institutions, (7) other important items.

Currently, it seems to be the common practice that the target board would post a public notice with their recommendation, which include opinion from independent directors. There is a special procedure to be considered for a tender offer, when the tender offer becomes effective. Article 97 in Securities Law specify that, after the delisting of the target shares, holders of untendered shares could be sold back to the acquirer through the trading system of the stock exchange for a duration of two months. Afterwards, such service from the stock exchange would be discontinued and the holder of untendered shares may be subject to substantial loss.

III. Cases of Listing as Consolidated Business Group

II.1: Consolidation of TCL Group (TCL集团):

The business of TCL Group was established jointly in 1981 with the Huizhou municipal government in Guangdong province to manufacture telephone sets, TVs, and other home appliances. In the year of 1993, the TCL Communication was carved out from the TCL business group to be listed as a separate firm at Shenzhen Stock Exchange. Also carved out from the group is TCL Multimedia Inc., which is listed and traded at Hong Kong Stock Exchange.

TCL Group is initiated as a state-own enterprise, but has been known to be under the strong leadership of a professional manager Mr. Dong-Shen Lee. In 1997, Mr. Lee and the Huizhou municipal government formulated probably one of the few first profit sharing contracts established in China. The contract stipulated an initial 100% ownership of TCL by Huizhou municipality, with an annual reward of ownership stakes for Mr. Lee

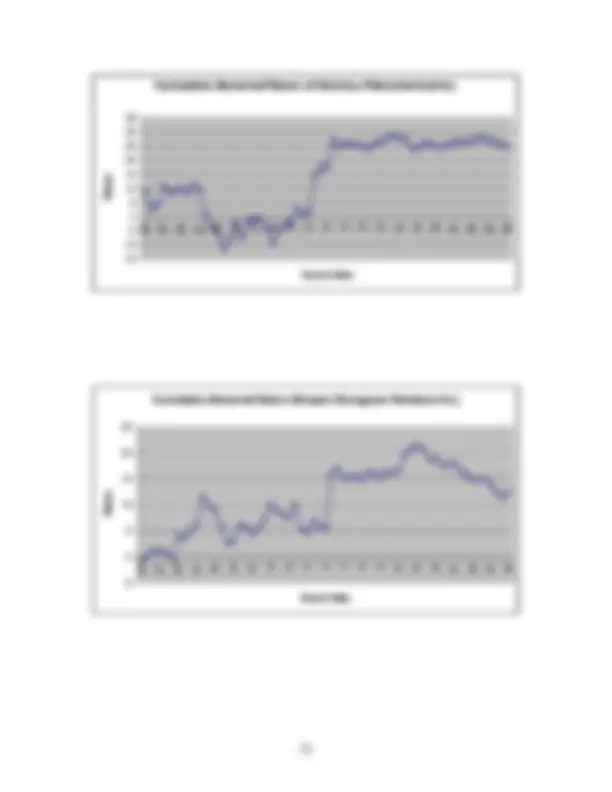

The trading of TCL communication was halted until October 9th. On the first day of resumed trading, the stock price of TCL Communication increased to 20.06 RMB, a 10% increase over its pre-announcement price^6. A calculation of cumulative abnormal returns (CARs) in the event window of [-30,30]^7 also indicates a 20.88% excess return for shareholders of TCL Communication. Figure 1-1 illustrates the pattern of the calculated CARs over the 2-month event window.

There existed many legal hurdles to overcome in such a stock-for-stock merger, and TCL proceeded with caution. The impending transaction, as required by law, has to be put to shareholders’ votes. Both TCL Group and TCL Communication called for shareholders’ meeting. First, as stipulated by Chinese Corporation Law( 公 司 法 ) , a merger has to be approved by over two-third of shareholders present at the shareholder meeting. In addition, if the transaction is considered a related party transaction (关联交易) (stipulated by Rules on Listed Firms in Shenzhen Stock Exchange (深圳证券交易所股票上 市规则),the controlling shareholders should not cast their votes at the meeting. In a

freeze-out transaction, this regulation ensures that the interests of minority shareholders are protected, and their votes determine whether such a transaction would be approved.

The process of TCL consolidation is well-articulated. The independent directors of TCL Communication played certain role in the TCL consolidation process. The board also issued a public statement addressing some frequently asked questions about the merger, including potential risk of the merger, proxy solicitation of proxies by independent directors, and the exclusion of votes from controlling shareholders. Three independent directors were also known to issue a public notice of their independent opinion, hire independent financial advisor on behalf of shareholders, and, with the approval from half of the independent directors, publicly solicited shareholders proxies to represent shareholders who are not able to attend the shareholder meeting. Anecdotal

(^6) On December 25th, the price of TCL Communication closed at 24.85 RMB, a 17.5% premium over the exchange value of 21.15 RMB. 7 The notation indicate an event window of measuring the cumulative return (CAR), which starts thirty days prior to the announcement date and lasts until the thirtieth days afterwards.

evidence also suggests that confidentiality of the TCL’s consolidation underwriting was well-kept, and partly contributed to the success of the transaction.

From a valuation perspective, the TCL consolidation is a well-packaged deal. TCL business group needed capital infusion to finance its fast growing segment, TCL Mobile. Raising fresh money was closed for both TCL Communication (from the capital market due to two consecutive years of accounting loss) and closed for TCL Group (from lenders due to high existing debt-to-asset ratio of 69%). The stock swap transaction opened a financing opportunity, with a much larger asset size of TCL Group than that of TCL Communication. It is essential to buy back shares from the minority shareholders of TCL Communication, as the assets in TCL Group (left behind by the carve-outs of TCL Communication and TCL Multimedia) are not as profitable. As illustrated in Table 1-1, TCL Group increased its ROA from 2.92% to 3.99%, and at the same time increased its holding of very profitable TCL Mobile from 48.59% to 58.39% by merging with TCL Communication.

The merger was approved by shareholders of both companies. TCL Communication was subsequently delisted on January 7th^ 2004. The IPO price of TCL was determined to 4.26 RMB, and went public at Shenzen Stock Exchange on January 30th^ 2004. The IPO offering raised 2,513,400,000 RMB new capital for TCL Group, with 590,000, shares issued to new investors, as well as 404,395,944 exchanged shares for shareholders of TCL Communication Inc (with the corresponding exchange ratio as one share of TCL Communication for 4.96 shares of TCL Group). On the first day of trading, the stock price closed at 6.88 RMB (a 61.50% increase from the offer price). Other examples of using similar approach of consolidation through share exchange include acquisition of Shanghai Hua Lian Co., (华联商厦^ )by Shanghai Bailian

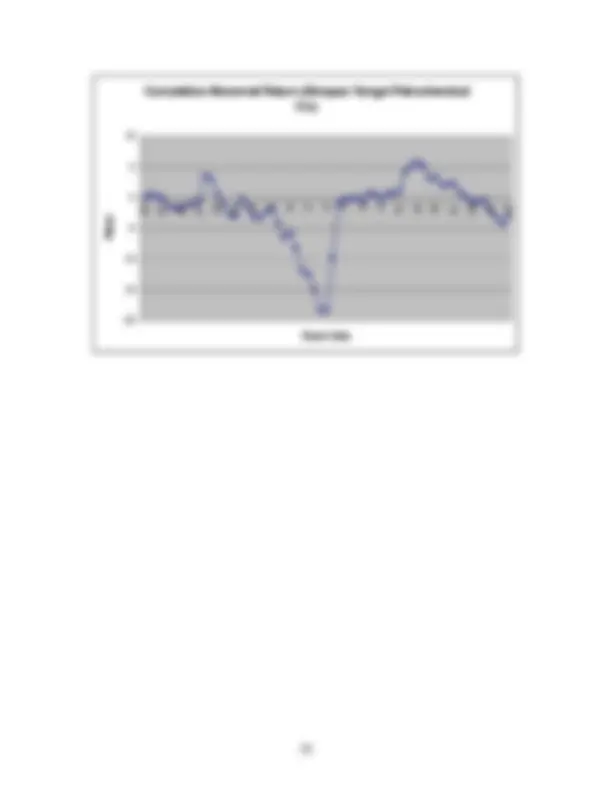

Group Co. ( 第 一 百 货 ) (announced on 4/7/2004) , and acquisition of Shanghai Port

Container Co., (G 上港) by Shanghai International Harbor Business Group (上港集团) (announced on 6/6/2006).

plates in the year of 2004. The business of the group as a whole generated an annual revenue of 50,142,107,000 RMB and net earnings of 6,486,284,200 RMB on an asset size of 70,672,048,400 RMB in 2004. However, as a carveout from the parent group, ANSC was allocated only retains the downstream manufacturing facilities with the more profitable upstream production line and iron ores retained by the parent. As a result, ANSC needs to purchase substantial amount of steel plates and molten steel as raw materials from affiliated companies affiliated companies, incurring 86.11% of its costs of good through related-party transactions.

ANSC announced its purchase of the affiliated company New Steel Iron Inc. from the parent business group on February 6th, 2006. The asset value of New Steel Inc. is re- evaluated by an independent party as 36,447,966,500 RMB (an increase of 5,084,858, over the book value of 31,363,108,400), mainly from the appreciation in value of land, buildings, and equipment. The purchase would be partly paid for by a private placement of 2,970,000,000 new ANSC shares with the parent group, with an ANSC share value of 4.29 RMB. The remaining balance would be debt of ANSC to its parent group, scheduled to be repaid in three annual installments. With the completion of this transaction, the majority of assets of Angang Business Group would be traded under the umbrella of ANSC^9. The infused assets are highly profitable, bringing the ROE of 11.68% for unconsolidated ANSC to 22.34% of the combined firm. The transaction would also eliminate 34.27% of the related party transaction, enhancing the transparency of ANSC’s financial record. It is also believed that the transaction would increase the ANSC ability to withstand competition within the steel industry through larger size, higher profitability, and increased efficiency through integrating stages of steel manufacturing process.

In contrast to the TCL restructuring, the transaction costs for ANSC consolidation is minimal, mainly due to the non-cash payment to purchase assets through private

(^9) One very valuable assets maintained outside ANSC are the iron ores. However, it was disclosed in the purchase agreement that there has been an outstanding contract on the purchase price of iron ore from the Angang Parent Business Group. ANSC would benefit from this agreement which stipulates a 10% discount from the price quote of the imported steel ore as the purchase price.

placement^10. Rule 14 of the newly amended Securities Law (证券法)requires only a review of private placement transaction with the CSRC, without registration document such as prospectuses. Further, according to the Official Notice on Major Asset Purchase, Asset Sale, or Asset Swap (关于上市公司重大资产购买、出售、置换资产若干问题通知), the private placement transaction would be reviewed by the Corporate Restructuring Committee (重组审核委员) for timely decision. However, it is well-known in the market that CSRC would not grant approval to cases in which the profitability of the combined firms decreases after the restructuring transaction.

With a well-intended restructuring plan and the well-disclosed Report on Major Asset Acquisition address to the shareholders, the ANSC stock gained 10.07% on the date of announcement. The abnormal return accumulated for the two month event period [-30,30] is 24.68%^11. Figure 2 illustrates the pattern of the calculated ANSC’s CARs over the 2- month event window.

Other examples of using similar approach of purchasing assets from its parent firm through private placement of share issuance include Shanxi Taigang Stainless Steel Co. (G 太钢) (announced on 6/15/2006) , and Shanghai Automotive Co. (G 上汽) (announced

on 7/12/2006), Jiangxi Changli Automotive Spring Co. (G 长 力 )(announced on 5/25/2006).

II.3: Consolidation of China Petroleum & Chemical Group (中石化集团)

The oil/gas section is a heavily regulated market in China. The three major oil/gas companies (Sinopec, PetroChina, and China Oilfield Service) are all business entities carved out from the previous state-owned enterprises. While the domestic prices

(^10) CSRC issued a circular (关于进一步规范股票首次发行上市有关工作的通知) on September 18th, 2003; stipulating that for potential IPO issuing firms, there has to be at least three years of records dated from the business reorganization as a cooperation. CSRC would grant exception to this rule if the potential issuing firm is the consolidated business reorganized from previous state owned enterprises. This notice sent a signal to the market that CSRC encourages public listing of a consolidated business group. 11 In order to exclude the industry effect, I use the equal-weighted average return of Baoshan Iron and Steel Co. and Wuhan Steel Processing Co. as the measure of expected return in this CAR calculation.