Download Risky Assets - E-Commerce - Lecture Slides and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

Moving Toward Many Risky Assets •

When the portfolio consists of many riskyassets, they form a plot similar to a broken eggshell shape

Each dot within the broken egg shell shaperepresents the risk/return profile for a singlerisky asset or portfolio of risky assets

To maximize return per unit of risk assumed, aninvestor would always choose an asset orportfolio that plots along the efficient frontier

Portfolios:

Many Risky Assets

R You would never choose Asset A, as you can earn ahigher return with similar risk by choosing the assetthat plots along the Efficient Frontier. A σ A Return Standard Deviation A

Introducing the Risk Free Security •

When a risk-free asset (Treasury Bill) isintroduced into the set of risky assets, a newefficient frontier emerges

This new efficient frontier is known as theCapital Market Line (CML)

The CML represents all possible portfolioscomprised of Treasury Bills and the MarketPortfolio

Adding the Risk-Free Asset

R M σ M Return Standard Deviation A R f Capital Market Line

What are we Missing? •

We know:

Investors should split their assets betweenTreasury bills and the market portfolio - To reduce risk, invest a greater proportion ofassets in Treasury bills - To enhance expected return, invest a greaterproportion of assets in the market portfolio

We do not know how to calculate the expected return (and hence the price) for a single riskyasset

The Capital Asset Pricing Model is needed

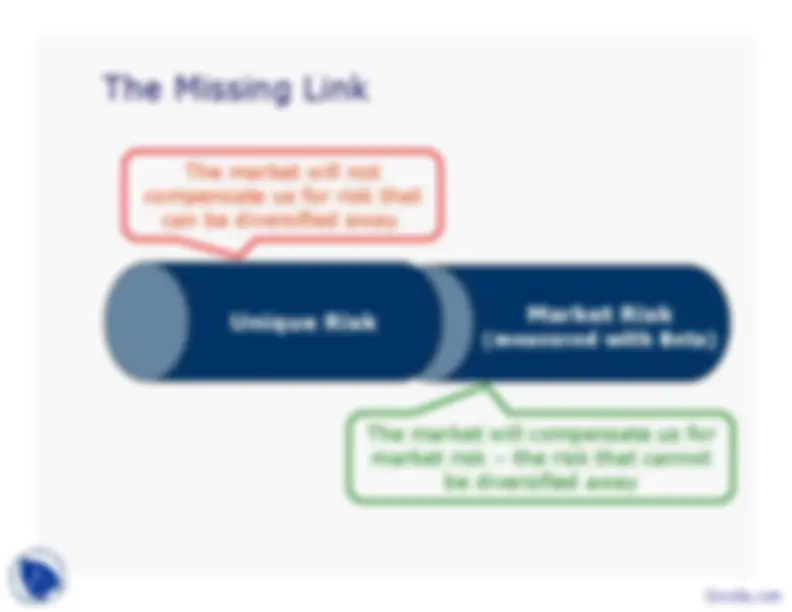

The Missing Link •

We need to measure the Market risk that cannotbe diversified away Unique or Non-systematic Risk Market or Systematic Risk Diversifiable Non- Diversifiable Total Standard Deviation (or Risk)

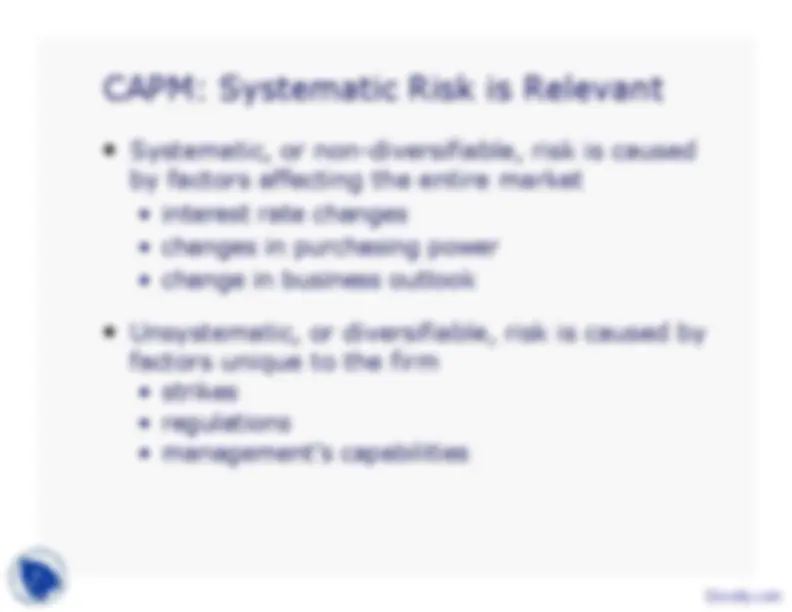

CAPM: Systematic Risk is Relevant •

Systematic, or non-diversifiable, risk is causedby factors affecting the entire market

interest rate changes - changes in purchasing power - change in business outlook

Unsystematic, or diversifiable, risk is caused byfactors unique to the firm

strikes - regulations - management’s capabilities