Download SBA Microloan Program: Loan Side Basics and Requirements and more Study notes Business in PDF only on Docsity!

SBA MICROLOAN PROGRAM

Session: Loan Side Basics

Microloan Program Purpose

The Microloan Program assists women, low

income, veteran, and minority entrepreneurs,

and other small businesses in need of

financing in amounts of $50,000 or less and

business- based technical assistance.

SBA Loans to Intermediary Lenders

- Terms and Conditions, Rate Structure

- SBA Bank Account Requirements

- MRF and LLRF Permissions and Restrictions

- Disbursements

- Matching Funds

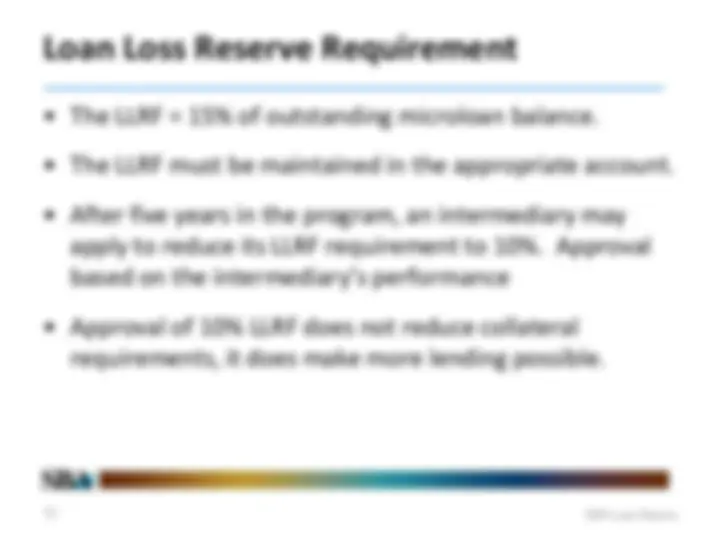

- LLRF Requirements

- Collateral Requirements

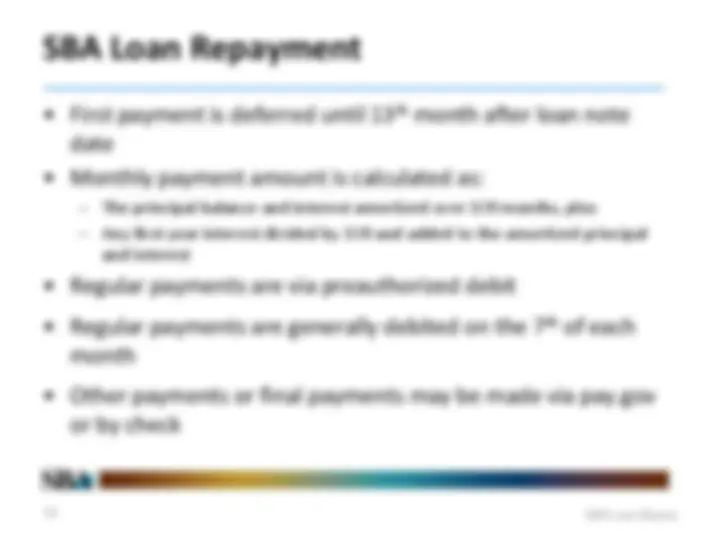

- Loan Repayment

- First Year Interest and Annual Loan Recasting

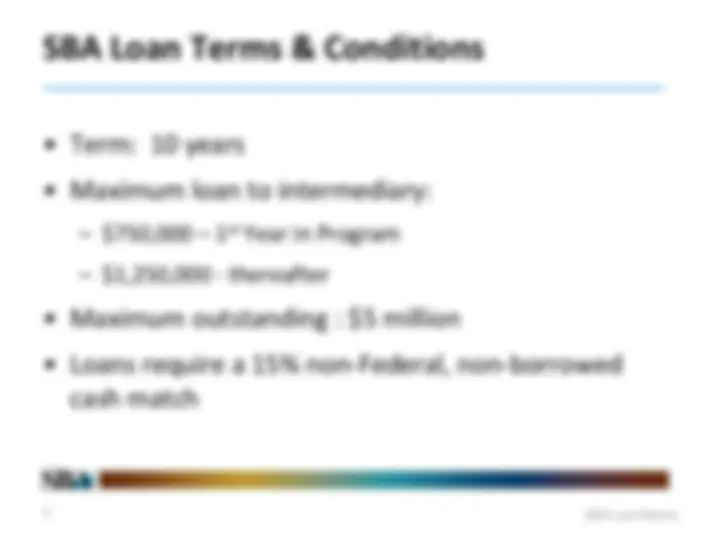

SBA Loan Terms & Conditions

- Term: 10 years

- Maximum loan to intermediary:

- $750,000 – 1st^ Year in Program

- $1,250,000 - thereafter

- Maximum outstanding : $5 million

- Loans require a 15% non-Federal, non-borrowed cash match

SBA Bank Account Requirements

- Three bank accounts must be set up when an intermediary enters the program:

- Microloan Revolving Fund (MRF) Account

- Loan Loss Reserve Fund (LLRF) Account

- Technical Assistance Account (TA) (may be general operating fund account but only one grant account per intermediary is permitted)

- Each subsequent loan from SBA requires two new accounts- a MRF and a LLRF account. Any new grant funds may be deposited to the existing TA Bank Account

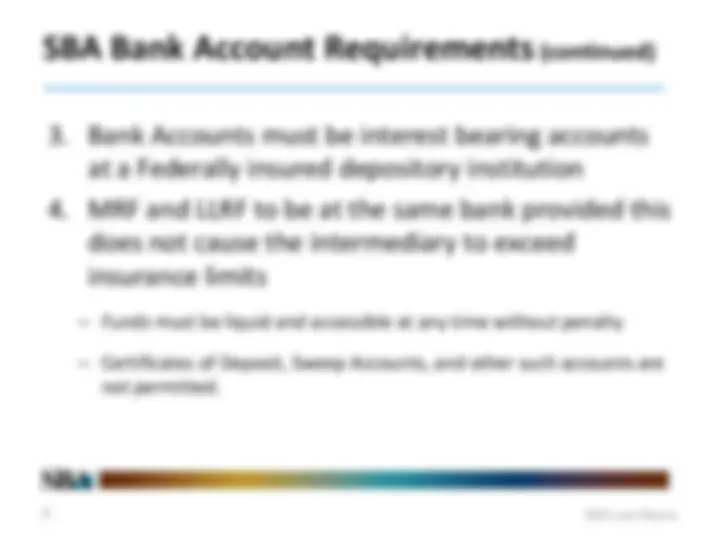

SBA Bank Account Requirements (continued)

- Bank Accounts must be interest bearing accounts at a Federally insured depository institution

- MRF and LLRF to be at the same bank provided this does not cause the intermediary to exceed insurance limits

- Funds must be liquid and accessible at any time without penalty

- Certificates of Deposit, Sweep Accounts, and other such accounts are not permitted.

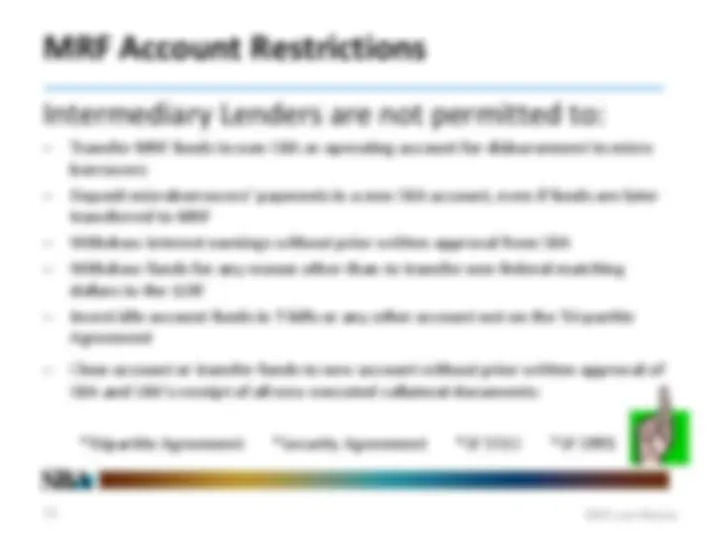

MRF Account Restrictions

Intermediary Lenders are not permitted to:

- Transfer MRF funds to non-SBA or operating account for disbursement to micro borrowers

- Deposit microborrowers’ payments in a non-SBA account, even if funds are later transferred to MRF

- Withdraw interest earnings without prior written approval from SBA

- Withdraw funds for any reason other than to transfer non-federal matching dollars to the LLRF

- Invest idle account funds in T-bills or any other account not on the Tri-partite Agreement

- Close account or transfer funds to new account without prior written approval of SBA and SBA’s receipt of all new executed collateral documents:

*Tripartite Agreement *Security Agreement *SF 5510 *SF 3881

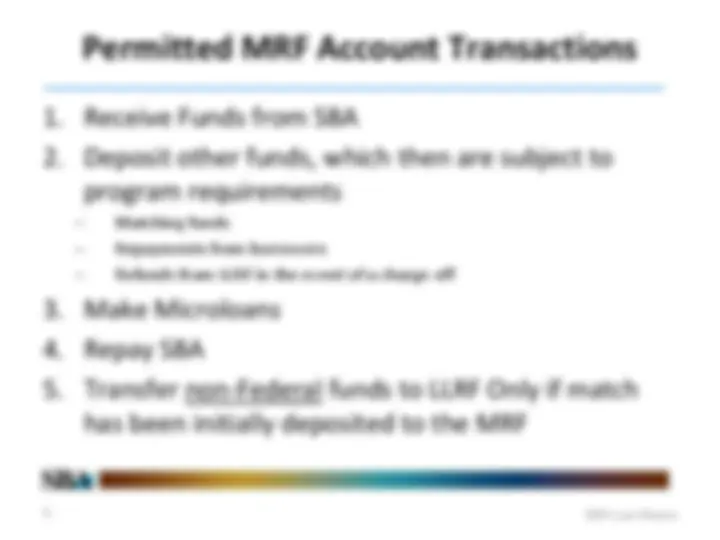

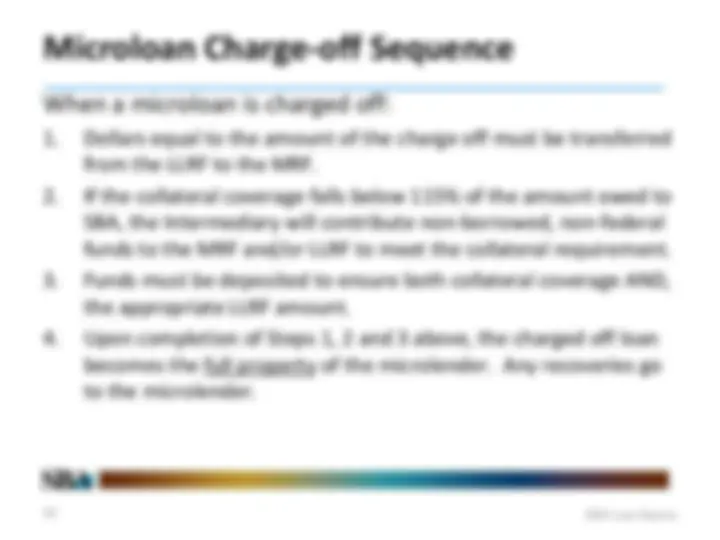

Permitted LLRF Account Transactions

- Deposit matching funds or other non-federal funds

- Transfer non-Federal funds from MRF to LLRF when LLRF is underfunded

- Transfer principal balance of charged off microloans from LLRF to MRF The LLRF must never go below 15% of the outstanding balance of microloans owed to the intermediary (with certain exceptions).

SBA Loan Disbursement

- Disbursements may be requested by email

- First disbursement on initial SBA loan < = 35% of approval

- Subsequent disbursements after excess cash is committed

- Generally, loans should be fully drawn down in no more than three requests

- Requests may take up to 10 days to process

- Disbursement request must include evidence of 15% matching fund deposit (to MRF or LLRF)

- 24 months from Date of Loan Authorization to take full disbursement

Matching Funds

- Matching funds of 15% must be deposited for each and every disbursement. - Exception: the intermediary may deposit the full match required at time of initial disbursement

- The matching fund deposit may be made into either the LLRF or MRF account associated with the SBA loan. - Acceptable proof: deposit slip receipt, on-line transfer receipt, or bank statement showing account activity - Not acceptable: bank account balance

- Intermediaries must meet the 15% matching fund requirement regardless of whether the intermediary has a 10% or 15% loan loss reserve requirement.

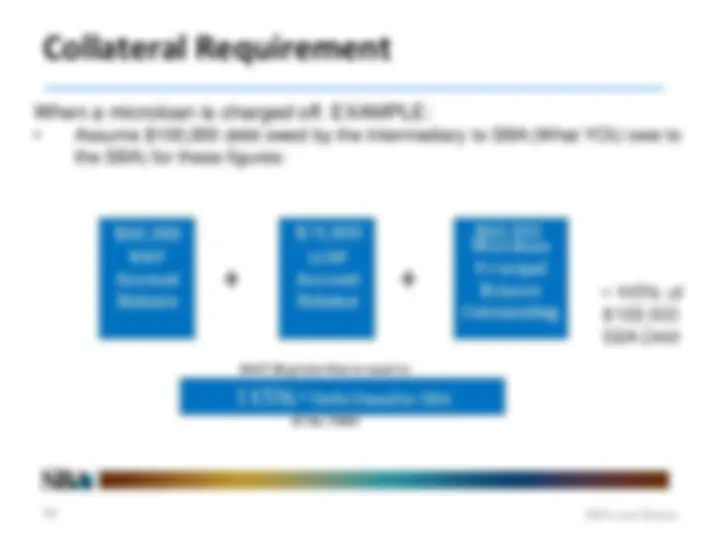

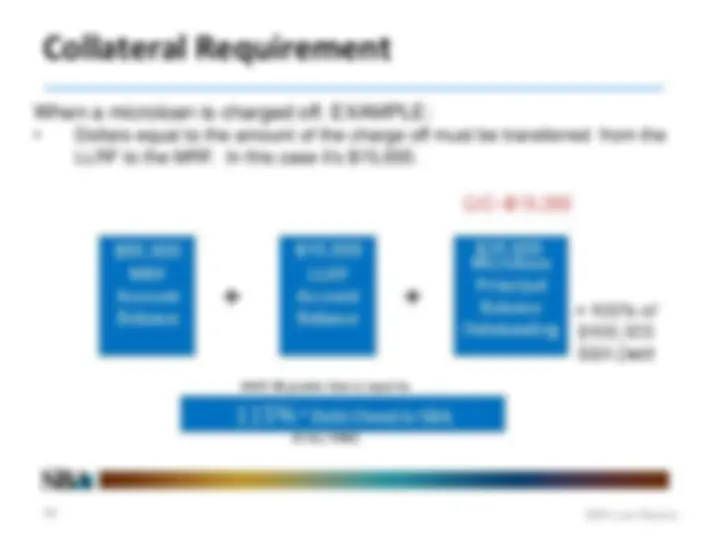

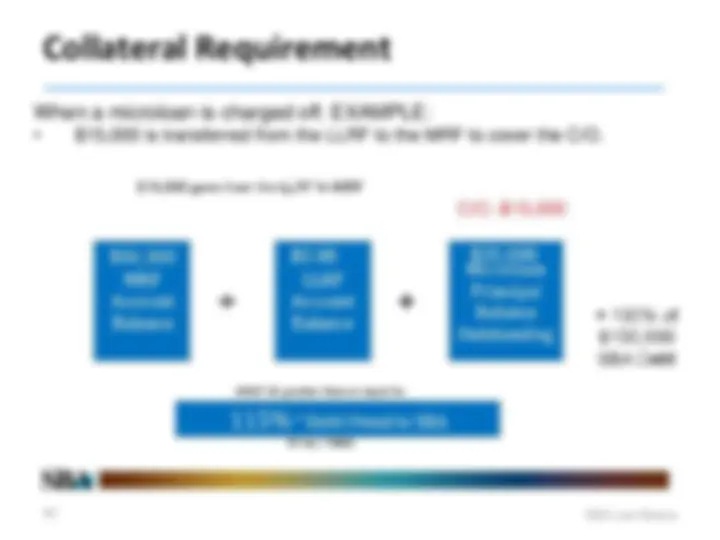

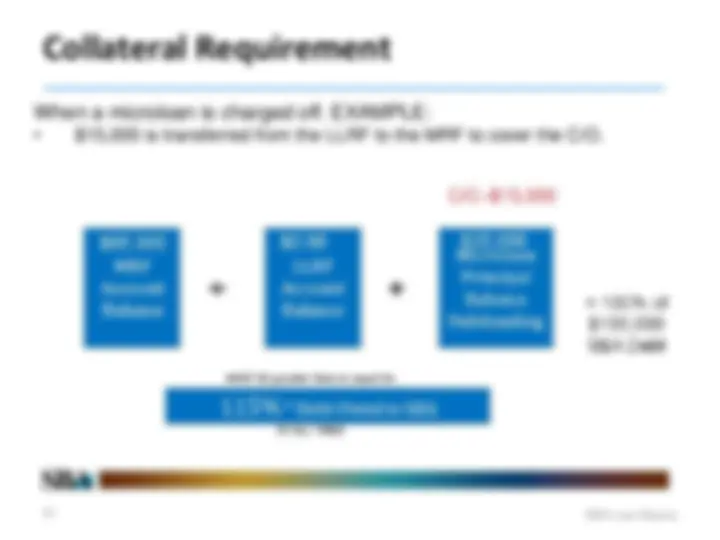

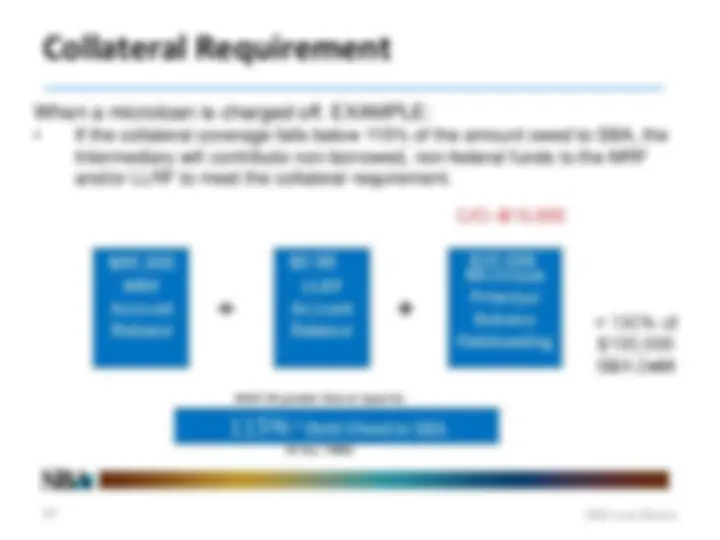

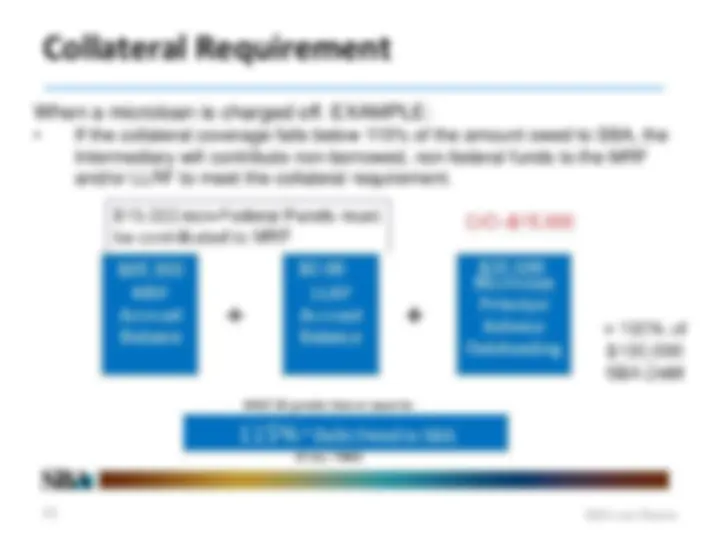

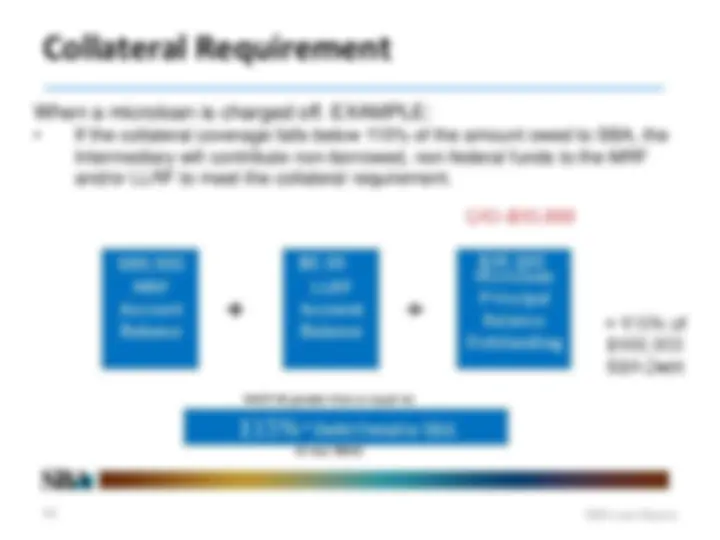

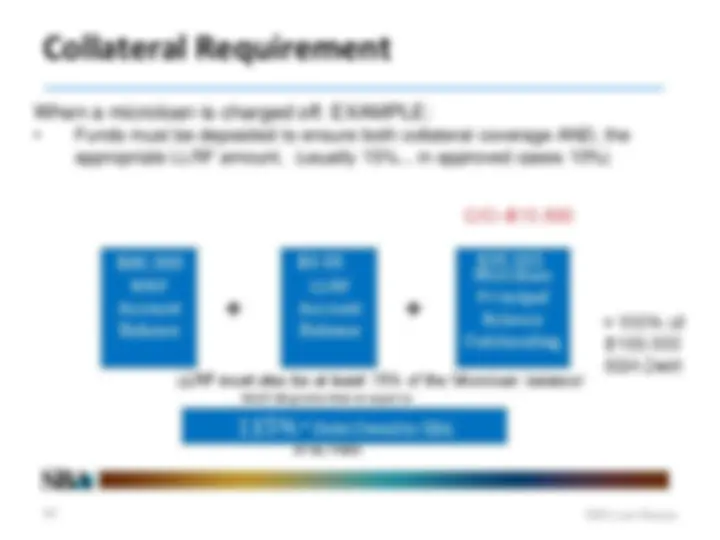

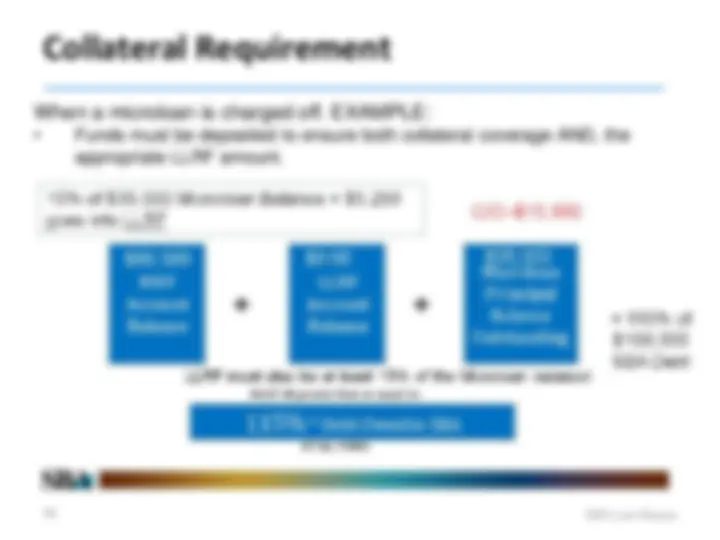

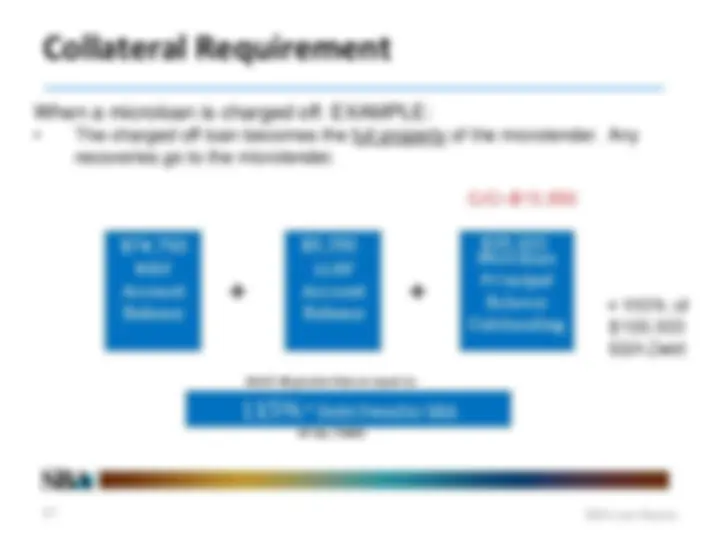

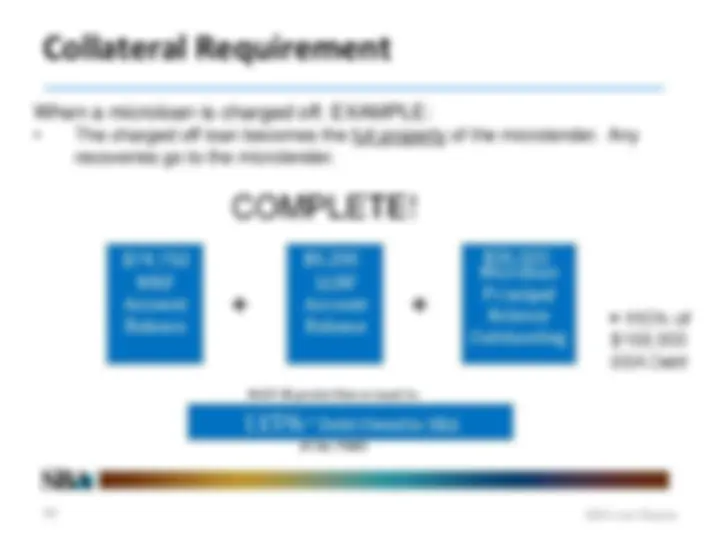

Collateral Requirement

Collateral Coverage Requirement (continued)

- Intermediaries with a 10% LLRF requirement must still maintain collateral coverage of 115%

- Intermediaries will be required to develop a plan of action to remove any collateral shortfall. This plan must be approved by SBA.

- Failure to maintain appropriate collateral, and meet MRF and LLRF requirements may result in limitations on: - Loan disbursements - New loan approvals - Reporting requirements - TA funding

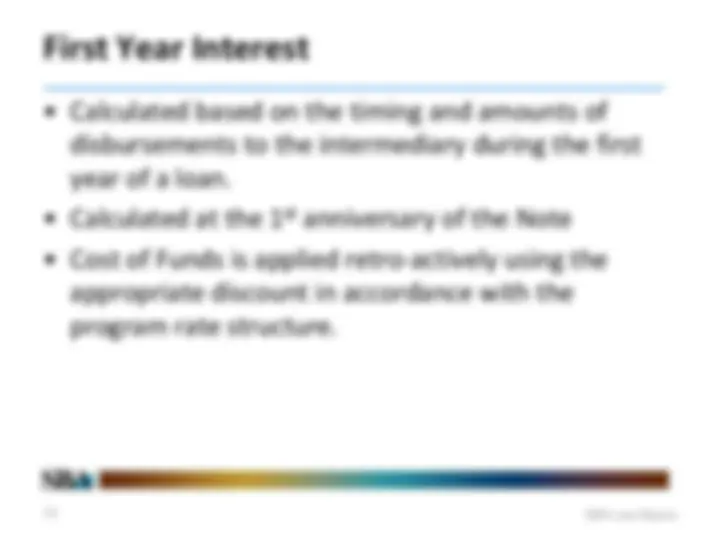

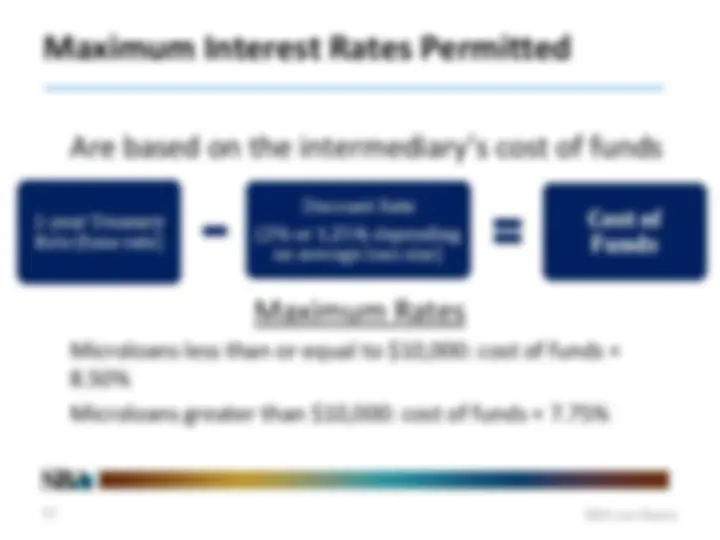

First Year Interest

- Calculated based on the timing and amounts of disbursements to the intermediary during the first year of a loan.

- Calculated at the 1st^ anniversary of the Note

- Cost of Funds is applied retro-actively using the appropriate discount in accordance with the program rate structure.

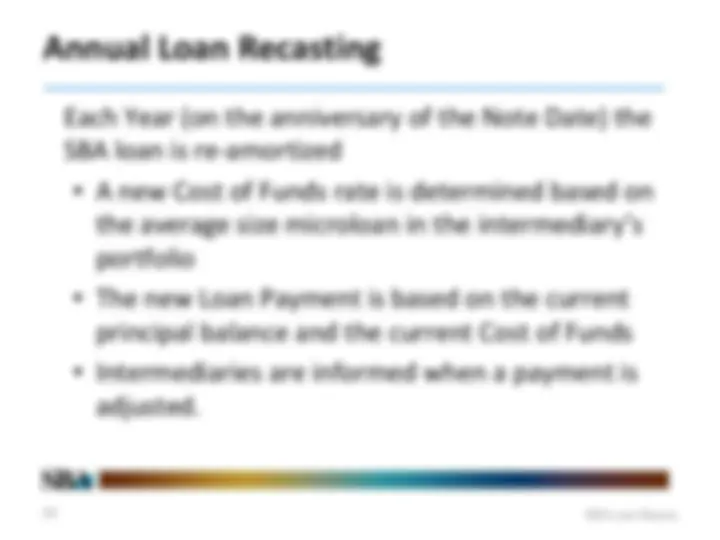

Annual Loan Recasting

Each Year (on the anniversary of the Note Date) the SBA loan is re-amortized

- A new Cost of Funds rate is determined based on the average size microloan in the intermediary’s portfolio

- The new Loan Payment is based on the current principal balance and the current Cost of Funds

- Intermediaries are informed when a payment is adjusted.