Section 5.2 – Annuities 1

Section 5.2

Annuities

A sequence of equal periodic payments made at the end of each payment period is called

an ordinary annuity.

Examples of annuities:

1. Regular deposits into a savings account.

2. Monthly home mortgage payments.

3. Payments into a retirement account.

We will study annuities that are subject to the following conditions:

1. The terms are given by fixed time intervals.

2. The periodic payments are equal in size.

3. The payments are made at the end of the payment periods.

4. The payment periods coincide with the interest conversion periods.

The sum of all payment made and interest earned on an account is called the future value

of an annuity.

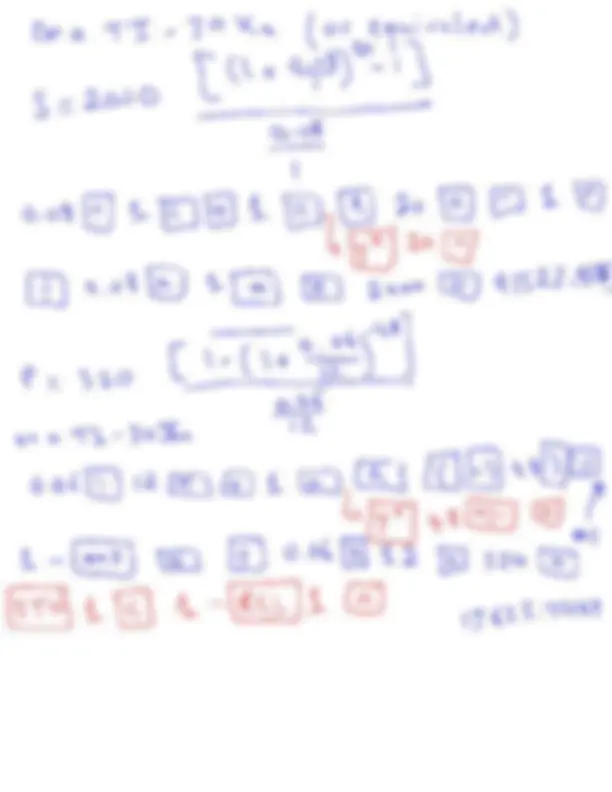

Future Value of an Annuity

The future value S of an annuity of n payments of R dollars each, paid at the end of each

investment period into an account that earns interest at the rate of i per period, is

⎥

⎦

⎤

⎢

⎣

⎡−+

=i

i

RS n1)1(

Present Value of an Annuity

The present value P of an annuity of n payments of R dollars each, paid at the end of each

investment period into an account that earns interest at the rate of i per period, is

⎥

⎦

⎤

⎢

⎣

⎡+−

=

−

i

i

RP n

)1(1