STATE OF

THE U.S.

SEMICONDUCTOR

INDUSTRY

2021

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Semiconductor Technology & Semiconductor Electronics

Typology: Summaries

1 / 27

This page cannot be seen from the preview

Don't miss anything!

CHIPS FIGHTING COVID- THERE ARE A NUMBER OF WAYS SEMICONDUCTORS HAVE PROVEN ESSENTIAL IN SUPPORTING THE WORLD THROUGH THE PANDEMIC:

Medical Devices Virtual Everything Public Testing and Tracing Remote Healthcare and Vulnerable Populations Accelerating Vaccine Development 1 4 2 5 3 As the “brains” of electronic devices, semiconductors have been crucial to the pandemic response and recovery of the global economy. They have provided display, wireless connectivity, processing, storage, power management, and other essential functions to a wide array of essential products, life-saving equipment and critical infrastructure. This includes healthcare and medical devices, telecommunications, energy, finance, transportation, agriculture, manufacturing, aerospace, and defense. Semiconductors also underpin the IT systems that have made remote work and school possible and have provided access to essential services across every domain, including medicine, finance, education, government, food distribution, and more. Throughout this global pandemic, semiconductor-rich devices have become increasingly prevalent in developing solutions for numerous problems in the economic and public health sphere. The ability of semiconductors to drive performance in these critical sectors is tied to “Moore’s Law,” the observation that the capabilities of semiconductor chips will double roughly every two years, while the price goes down. Today, the most advanced microprocessors contain nearly 40 billion transistors.

CHIPS FIGHTING COVID- Semiconductors are an integral component of many medical devices used in hospitals and doctors’ offices today, including many devices that are critical to treating COVID-19 patients. Any medical device that can be plugged into an electric socket or has batteries depends on semiconductors to operate. Semiconductors provide functions such as operations control, data processing and storage, input and output management, sensing, wireless connectivity and power management. By enabling functions previously performed by non- semiconductor devices, semiconductors have often lowered costs and improved performance at the same time. This has proved critical to the COVID- response and improving health care in general. Two specific examples of semiconductors in medical devices helping in the COVID-19 fight are below: Portable Ultrasound Devices In a hospital setting, the first line of detection for COVID-19 is identifying recognizable symptoms of the virus such as lung lesions. Quickly identifying this trait of the severe acute pneumonia associated with the virus has allowed doctors to treat afflicted patients without having to wait for tests on viral infection. This rapid response is possible with handheld ultrasound devices and temperature screening. These portable ultrasound devices have transitioned from utilizing piezoelectric crystals to semiconductors, greatly reducing the cost and improving performance. Now, due to the utilization of semiconductors, hospitals have access to vastly more affordable and efficient technologies to assess internal injuries in patients. Ventilators Ventilators are utilized to treat patients with severe lung damage by assisting breathing and are controlled by semiconductor chips. The ventilator system uses semiconductor sensors and processors to monitor vital signals; determine the rate, volume, and amount of oxygen per breath; and accurately adjust oxygen levels according to the needs of the patient. These signals are read and interpreted by the machine’s semiconductor processors, which control the speed of the motor that translates to mechanized breathing to support a patient. Medical Devices

1

A critical aspect of safely reopening economic sectors has been protecting vulnerable populations such as the elderly, diabetic, and hard of hearing. Managing contact with these populations is the first step, but real-time monitoring systems have allowed physicians access to information regarding the daily status of their patients both in-house and remotely. Semiconductors have played an important role in this. Remote healthcare, or telemedicine, has been necessary and highly beneficial during the COVID-19 crisis, and semiconductors are vital to IT infrastructure and to wearable medical technology for patient monitoring. This technology is especially helpful to the elderly population and patients with underlying health conditions. People with diabetes are also at higher risk from the coronavirus. This risk can be mitigated with new semiconductor-rich technologies that make use of advanced sensors such as continuous glucose monitoring (CGM) and wearable insulin pumps. CGM works by placing a sensor on your skin that transmits information to a device that will alert you if your blood sugar fluctuates greatly. Similarly, insulin pumps manage your glucose levels by releasing small doses of insulin according to your programmed schedule. For diabetic COVID-19 patients, access to such technologies has helped to prevent life-endangering complications. Semiconductors have also improved COVID- care for underserved and vulnerable populations in less well-known ways. Hard of hearing patients have been at a distinct disadvantage during the COVID-19 crisis, as medical masks degrade speech quality, making it difficult for hearing impaired patients to understand the advice given by health care professionals. A study in Hearing Review concluded, “Many of the people who have fallen victim to the virus have hearing loss, are unaccompanied by family members, are frail, have multiple chronic conditions and are likely without hearing assistance.” Hearing aids use semiconductors to filter, process, and amplify sound, all in a small package that fits discretely on or in the ear. To help patients acquire hearing aids, several hearing care firms have launched platforms to allow remote patient care. Other telemedicine platforms have seen a more than 700% increase in users in areas highly affected by the virus. Remote Healthcare and Vulnerable Populations CHIPS FIGHTING COVID- YEAR-OVER-YEAR MONTHLY CHIP SALES GROWTH TO MAJOR CONSUMER SECTORS RAPIDLY INCREASED

5 60% 50% 30% 40% 20% 10% 0% -10% Jan 2020 Jan 2021 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Feb Mar Apr May Jun Communication Computer Consumer

The shortage took hold in 2020, largely due to significant swings in demand caused by the COVID- pandemic as far back as Spring 2020. Some customers reduced production and chip purchases as the virus spread across the globe. In addition, a number of countries and regions went into lockdown in early 2020, which significantly interrupted semiconductor supply. Chipmakers, meanwhile, saw surging demand for semiconductors in other sectors used to enable remote healthcare, work-at-home, and virtual learning, which were needed during the pandemic. The shortage continues to affect a range of downstream sectors, including cars, consumer electronics, home appliances, industrial robotics, and many other key goods. The semiconductor industry has worked diligently to ramp up production to meet renewed demand during the shortage. First, the semiconductor industry worked hard to keep operations running globally, especially during the start of the pandemic in Spring 2020 when many foreign and state governments imposed lockdown orders on businesses. The semiconductor industry worked to classify its operations as “essential” so they could continue operations. For all quarters during the shortage, the industry has run fab utilization well above the normal utilization level of 80 percent. When market demand runs high, such as in a cyclical market upturn like the one the market is in now, front-end semiconductor fabrication facilities, or fabs, will typically run above 80 percent capacity utilization, with some individual fabs running as high as between 90-100 percent. As the table below shows, the industry has been steadily increasing overall fab utilization over the past two years and is estimated to increase utilization even more during most of 2021 to meet demand. Higher fab utilization will increase chip output and help the industry to meet the increased demand in the market. In short, the semiconductor industry has done precisely what is in its power to do in the short-term to meet the increase in demand, which is to expand fab utilization and run fabs at their highest capacity possible. THE GLOBAL CHIP SHORTAGE AND THE INDUSTRY’S RESPONSE One significant consequence of the pandemic over the past year has been the global chip shortage that has impacted a number of end markets, including the automotive market. The pandemic was a once-in-a-generation event that created substantial and unanticipated swings in demand.

Meanwhile, federal investments in chip research have held flat as a share of GDP, while other countries have significantly ramped up research investments. The dramatic decline in the U.S. share of global chip manufacturing, coupled with insufficient federal investments in semiconductor R&D, undermine our country’s long-term ability to manufacture, research, and design the advanced chips needed to support our economic recovery, power our military and critical infrastructure, create new high-paying jobs, reduce costs for clean energy technologies, and drive innovations in the must-win technologies of tomorrow. For our country to succeed in the future, we must continue to lead the world in semiconductor technology. To address this challenge, bipartisan legislation called the CHIPS for America Act was enacted in 2021. It authorizes investments in domestic chip manufacturing incentives and research initiatives, but funding must still be provided through congressional appropriations. Congress is also considering legislation called the FABS Act that would establish a semiconductor investment tax credit. The FABS Act should be expanded to include expenditures for both manufacturing and design to help strengthen the entire semiconductor ecosystem. By funding the CHIPS for America Act and expanding and enacting the FABS Act, leaders in Washington can usher in a historic resurgence of chip manufacturing in America, strengthen our country’s most critical industries, boost domestic chip research and design, and help ensure the U.S. leads in crucial, chip-enabled technologies — artificial intelligence, quantum computing, 5G/6G communications, and countless others. This resurgence will define America’s strength for decades to come. 40% 35% 30% 25% 20% 15% 10% 0% 5% CHIPS FOR AMERICA ACT/FABS ACT

The U.S. share of global semiconductor manufacturing capacity has eroded from 37% in 1990 to 12% today, mostly because other countries’ governments have invested ambitiously in chip manufacturing incentives and the U.S. government has not. In fact, three-quarters of the world’s chip manufacturing capacity is now concentrated in East Asia, with China projected to command the largest share of global production by 2030, due to its government’s massive investments in this sector. 37% 10% 1990 2000 2010 2020E 2030E U.S.

Following weak sales of $412.3 billion in 2019, global sales in 2020 increased by 6.8 percent to $440. billion, due largely to demand growth spurred by the COVID-19 pandemic. The World Semiconductor Trade Statistics (WSTS) Semiconductor Market Forecast released in June 2021 projected worldwide semiconductor industry sales will increase significantly to $527 billion in 2021, an upward revision from its Fall 2020 forecast for 2021, due mainly to the continued strong demand growth in the overall market from 2020. In 2022, WSTS forecasts global sales will continue growing to $ billion. While 2020 market forecasts fluctuated throughout the year due to demand uncertainty caused by the COVID-19 pandemic, the global market actually increased in 2020, and the outlook for 2021 is very strong. 500 450 400 300 350 250 200 150 50 ’00 ’01 ’02 ’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15 ’16 ’17 ’18 ’19 ’ 0 100 +6.8% ‘19/’

THE GLOBAL SEMICONDUCTOR MARKET Over the past three decades, the semiconductor industry has experienced rapid growth and delivered enormous economic impact. Chip performance and cost improvements made possible the evolution from mainframes to PCs in the 1990s, the web and online services in the 2000s, and the smartphone revolution in the 2010s. Indeed, these chip-enabled innovations have created incredible economic benefits. For example, from 1995 to 2015, an estimated $3 trillion in global GDP has been directly attributed to semiconductor innovation, along with an additional $11 trillion in indirect impact. Semiconductors have become essential to our modern world, which is why long-term market demand for semiconductors remains strong. In the near-term, however, the COVID-19 pandemic and the global chip shortage present significant market challenges to the industry.

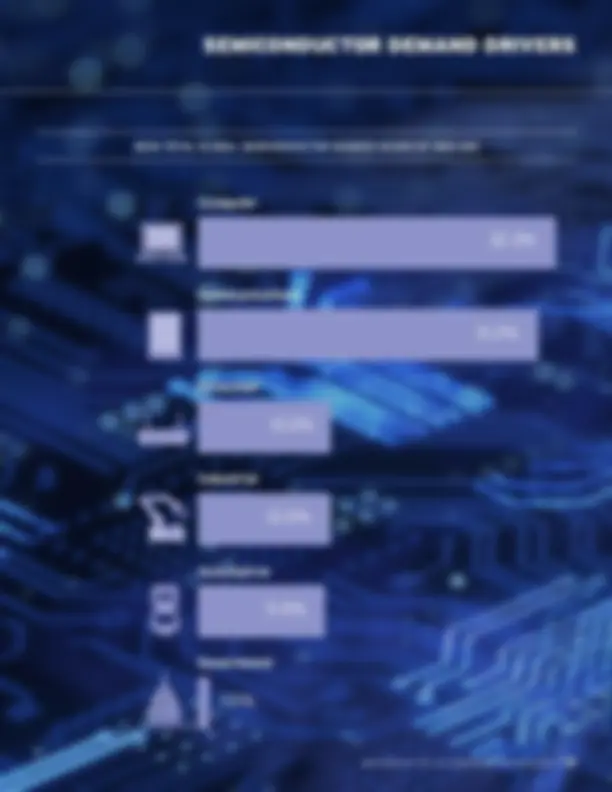

SEMICONDUCTOR DEMAND DRIVERS Communications 32.3% Computer 31.2% Consumer 12.0% Automotive 11.4% Government 1.0%

Industrial 12.0%

Since the late 1990s, the U.S. semiconductor industry has been the global sales market share leader with almost 50 percent annual global market share. In addition, U.S. semiconductor firms maintain a leading or highly competitive position in R&D, design, and manufacturing process technology. Global sales market share leadership also allows the U.S. semiconductor industry to benefit from a virtuous cycle of innovation; sales leadership enables the U.S. industry to invest more into R&D which in turn helps ensure continued U.S. sales leadership. As long as the U.S. semiconductor industry maintains global market share leadership, it will continue to benefit from this virtuous cycle of innovation. The U.S. semiconductor industry has nearly half the global market share and has displayed steady annual growth.

20%

47%

10%

10%

7%

5%

Semiconductors were invented in the United States, and the domestic industry remains the leader in the global market. While America’s position has been challenged many times over the decades, it has always prevailed due to its amazing resilience and ability to run faster. This does not mean the United States will go unchallenged in the future. The importance of semiconductors is so great that most Information-Age nations strive to be competitive in at least some aspect of this critical industry, and the world’s most ambitious nations seek to chase the U.S. H i g h e r re v e n u e a n d p o^ r t^ i^ f H s g i h e r R & D I^ n v e s t^ m e^ n t U.S. technology leadership U.S. INDUSTRY MARKET SHARE

Before a semiconductor is physically manufactured, it must first be designed. Semiconductors are highly complex products to design. Firms involved in semiconductor design develop the nanometer- scale integrated circuits that perform the critical tasks that make electronic devices work, such as connectivity to networks, computing, storage, and power management. Chip designers must use highly advanced electronic design automation (EDA) software and reusable architectural building blocks (“IP cores”) to do this task. Design activity is chiefly knowledge- and skill- intensive, accounting for 65% of the total industry R&D and 53% of the value added. By far, these represent the highest shares of R&D and value added of any stage of semiconductor fabrication. Companies focusing exclusively on semiconductor design typically invest 12-20% of their annual sales back into R&D. The development of modern complex chips, such as “system-on-chip” (SoC) processors that power today’s smartphones, requires many years of work by hundreds of engineers, sometimes leveraging external IP and design support services. As chips have become increasingly complex, development costs have rapidly risen. While both IDMs and fabless firms design semiconductors, fabless firms choose to focus exclusively on design and outsource fabrication, as well as assembly, packaging, and testing. Fabless firms typically outsource fabrication to pure-play foundries and outsourced assembly and test (OSAT) firms. The fabless model has grown along with the demand for semiconductors since the 1990s, as the pace of innovation made it increasingly difficult for many firms to manage both the capital intensity of manufacturing and the high levels of R&D spending for design. As technical difficulty and upfront investment soared with the migration to smaller manufacturing nodes, total semiconductor sales accounted for by fabless firms increased from less than 10% in 2000 to almost 30% in 2019. The U.S. semiconductor industry is a leader in chip design. U.S. fabless firms account for roughly 60% of all global fabless firm sales, and some of the largest IDMs, which do their own design, are also U.S. firms. In addition, the U.S. accounts for the largest share of the global design workforce, which highlights the strength of the U.S. industry and academic ecosystem for chip design. Given the importance of semiconductor design in terms of value added in the manufacturing process, it is critical that the U.S. industry has – and maintains – leadership in this stage of production. U.S. TECHNOLOGY COMPETITIVENESS The U.S. semiconductor industry is the global leader in semiconductor R&D and chip design. For U.S. companies, both fabless firms and integrated device manufacturers (IDMs), which have a combined share of almost 50 percent of global semiconductor sales, the critical success factors are access to highly skilled engineering talent and a thriving innovation ecosystem, particularly from leading universities. While the U.S. industry leads in R&D intensive activities, Asia leads in manufacturing process technology, supported by government incentives. When it comes to leading-edge logic capacity below 10 nanometers currently in operation, none is done in the United States. The United States is also well behind as a location for logic capacity 28 nanometers and above. The U.S. as leader in semiconductor design.

U.S. semiconductor industry R&D expenditures grew at a compound annual growth rate of approximately 7.2 percent from 2000 to 2020. R&D expenditures by U.S. semiconductor firms tend to be consistently high, regardless of cycles in annual sales, which reflects the importance of investing in R&D to semiconductor production. In 2020, total U.S. semiconductor industry investment in R&D totaled $44.0 billion. U.S. TECHNOLOGY COMPETITIVENESS U.S. semiconductor industry R&D expenditures are consistently high, reflecting the inherent link between U.S. market share leadership and continued innovation. R&D EXPENDITURE ($B) Innovative uses of semiconductor technology have the potential to make significant contributions towards solutions to global climate change. The deployment of information and communications technology (ICT), enabled by semiconductors, throughout the economy can achieve dramatic improvements in energy efficiency and the production of clean energy. Moreover, while the number of semiconductors continues to grow as we fully digitize our economies, semiconductor- enabled technologies present opportunities to drive dramatic reductions in emissions from virtually all sectors of the economy, ranging from transportation and manufacturing to buildings, energy, and agriculture. According to the World Economic Forum, semiconductor-enabled technologies, such as digital technologies, can reduce greenhouse gas emissions by 15 percent - almost one-third of the 50 percent reduction required by 2030. Semiconductors serve as the backbone of the ICT industry: electronics, computing hardware, telecommunications, and connected devices such as sensors and thermostats. Connected devices that run on semiconductor chips (i.e., the Internet of Things (IoT)) numbered 22.6 billion in 2019 and are projected to grow to 75 billion by

50% 45% 30% 25% 40% 35% 20% 15% 10% 0% 5% ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19 ‘

While the U.S. leads in R&D intensive activities, it has fallen behind as a location for manufacturing technology.

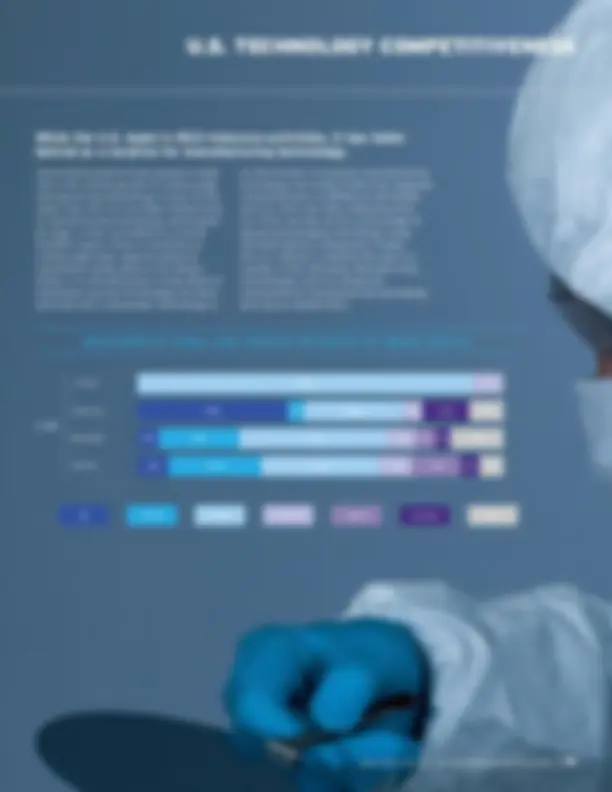

U.S. TECHNOLOGY COMPETITIVENESS Government policies have played a major role in the strong growth of cutting edge manufacturing technology in Asia. At the same time, the U.S. has fallen behind Asia in manufacturing technology particularly for logic. In fact, according to a recent SIA/BCG report, there is currently no cutting edge logic capacity below 10 nanometers being done in the United States. It is all being done in Asia where 5 nanometer process technology has been achieved and 3 nanometer technology is on the horizon. In memory manufacturing technology, the United States has regained competitiveness in DRAM and 3D-NAND, and U.S. firms are fully embracing EUV. U.S. firms are also at the cutting edge of advanced packaging technology using 3D-heterogenous integration. Finally, the U.S. industry is leading the way in a number of the emerging manufacturing technologies such as compound semiconductor manufacturing technology and silicon carbide (SiC). < 10 nm Logic 10-22 nm 28-45nm

45 nm US China Taiwan S Korea Japan Europe Other 9% 23% 31% 10% 13% 6% 7% 6% 19% 47% 6% 5%4% 13% 43% 3% 28% 5% 12% 9% 92% 8%

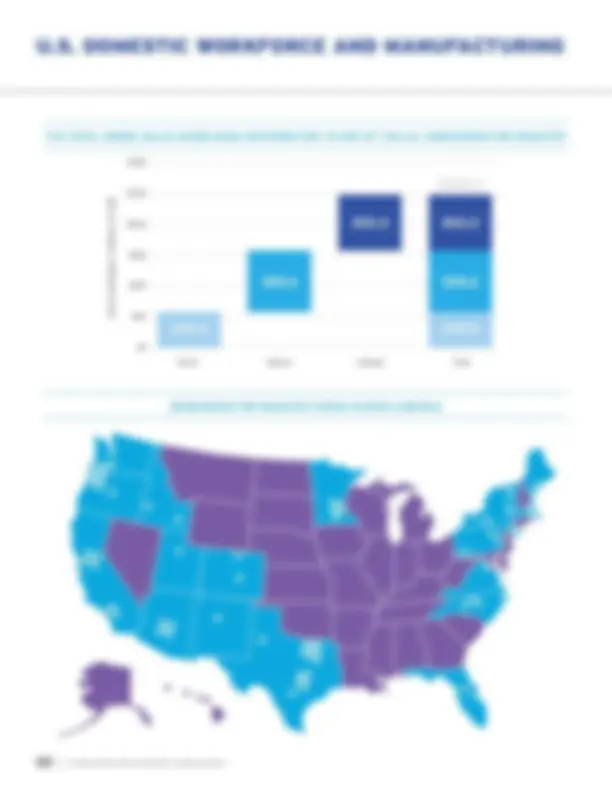

Beyond providing inputs to nearly every industry in the U.S. economy, the U.S. semiconductor industry is essential to the U.S. economy by stimulating jobs and paying income to workers. In total, the U.S. semiconductor industry supported 1.85 million U.S. jobs in 2020. The industry directly employs more than 277,000 domestic workers in R&D, design, and manufacturing activities, among others. In addition, for each U.S. worker directly employed by the semiconductor industry, an additional 5.7 jobs are supported in the wider U.S. economy, either in the supply chains of the semiconductor industry or through the wage spending of those employed by the firms themselves. In addition to job creation, the U.S. semiconductor industry has a significant impact on GDP and income. In 2020, the total impact of the U.S. semiconductor industry on GDP was $246. billion. In terms of the impact on income, the industry was responsible for generating $160. billion in income in 2020 in the United States. These benefits were distributed widely within the U.S. economy in terms of other sectors positively impacted. For example, in terms of the 1.85 million total direct and indirect jobs created by the industry, many were created in sectors as diverse as construction, financial activities, and leisure and hospitality. The positive impact of the semiconductor industry on the American workforce. U.S. DOMESTIC WORKFORCE AND MANUFACTURING Having a competitive domestic workforce and manufacturing capabilities are critical to America’s lead in semiconductors. In addition, a strong domestic semiconductor industry is essential to the U.S. economy. The semiconductor industry has a considerable economic footprint in the U.S. Nearly 277,000 people work in the industry, designing, manufacturing, testing, and conducting R&D on semiconductors throughout 49 states in the U.S. Over 300 downstream economic sectors, accounting for over 26 million U.S. workers, are consumers of and are therefore enabled by semiconductors for their sectors. I N^ D^ U^ C^ E^ D I^ N^ D^ I^ R^ E^ C^ T D^ I^ R^ E^ C^ T $47.1 $55. 277, $61.9 $98. 669, 905, $51.8 $92.0 $246. TOTAL $160. TOTAL 1,852, TOTAL GDP (US$, billions) Income (US$, billions) Employment