Download Sensitivity of Disney's Value and Operating Income to Macroeconomic Factors and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

126

II. SensiGvity to Changes in GDP/ GNP

126

¨ How sensiGve is the firm’s value and operaGng income

to changes in the GNP/GDP?

¨ The answer to this quesGon is important because

¤ it provides insight into whether the firm’s cash flows are cyclical and ¤ whether the cash flows on the firm’s debt should be designed to protect against cyclical factors.

¨ If the cash flows and firm value are sensiGve to

movements in the economy, the firm will either have to

issue less debt overall, or add special features to the

debt to Ge cash flows on the debt to the firm’s cash

flows.

127

Regression Results

127

¨ Regressing changes in firm value against changes in the

GDP over this period yields the following regression –

Change in Firm Value = 0.0826 + 8.89 (GDP Growth) (0.65) (2.36)

Conclusion: Disney is sensiGve to economic growth

¨ Regressing changes in operaGng cash flow against

changes in GDP over this period yields the following

regression –

Change in OperaGng Income = 0.04 + 6.06 (GDP Growth) (0.22) (1.30)

Conclusion: Disney’s operaGng income is sensiGve to

economic growth as well.

129

Regression Results

129

¨ Regressing changes in firm value against changes in the dollar over this period yields the following regression – Change in Firm Value = 0.17 -‐2.04 (Change in Dollar) (2.63) (0.80) Conclusion: Disney’s value is sensiGve to exchange rate changes, decreasing as the dollar strengthens. ¨ Regressing changes in operaGng cash flow against changes in the dollar over this period yields the following regression – Change in OperaGng Income = 0.19 -‐1.57( Change in Dollar) (2.42) (1.73) Conclusion: Disney’s operaGng income is also impacted by the dollar. A stronger dollar seems to hurt operaGng income.

130

IV. SensiGvity to InflaGon

130

¨ How sensiGve is the firm’s value and operaGng

income to changes in the inflaGon rate?

¨ The answer to this quesGon is important, because

¤ it provides a measure of whether cash flows are posiGvely or negaGvely impacted by inflaGon. ¤ it then helps in the design of debt; whether the debt should be fixed or floaGng rate debt.

¨ If cash flows move with inflaGon, increasing

(decreasing) as inflaGon increases (decreases), the

debt should have a larger floaGng rate component.

132

Summarizing…

132

¨ Looking at the four macroeconomic regressions, we

would conclude that

¤ Disney’s assets collecGvely have a duraGon of about 3 years ¤ Disney is increasingly affected by economic cycles ¤ Disney is hurt by a stronger dollar ¤ Disney’s operaGng income tends to move with inflaGon

¨ All of the regression coefficients have substanGal

standard errors associated with them. One way to

reduce the error (a la boUom up betas) is to use

sector-‐wide averages for each of the coefficients.

133

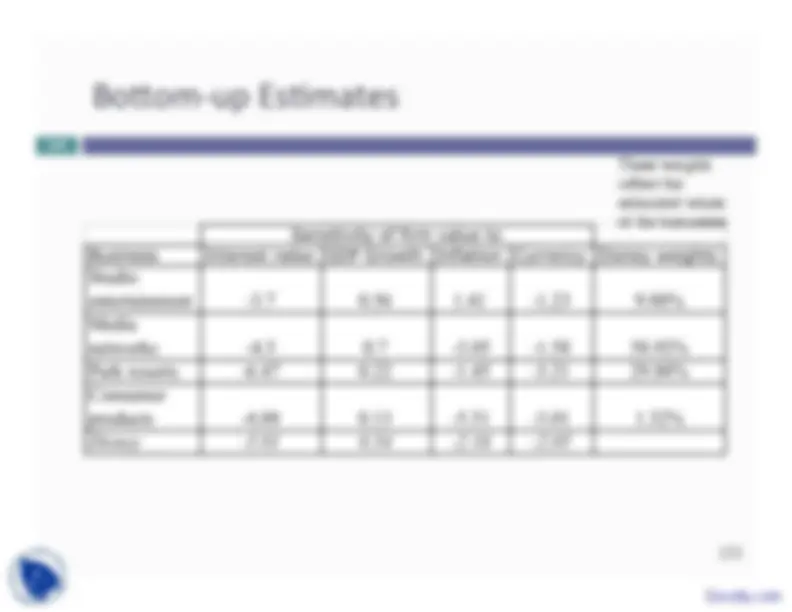

BoUom-‐up EsGmates

133 These weights reflect the estimated values of the businesses

135

Analyzing Disney’s Current Debt

135

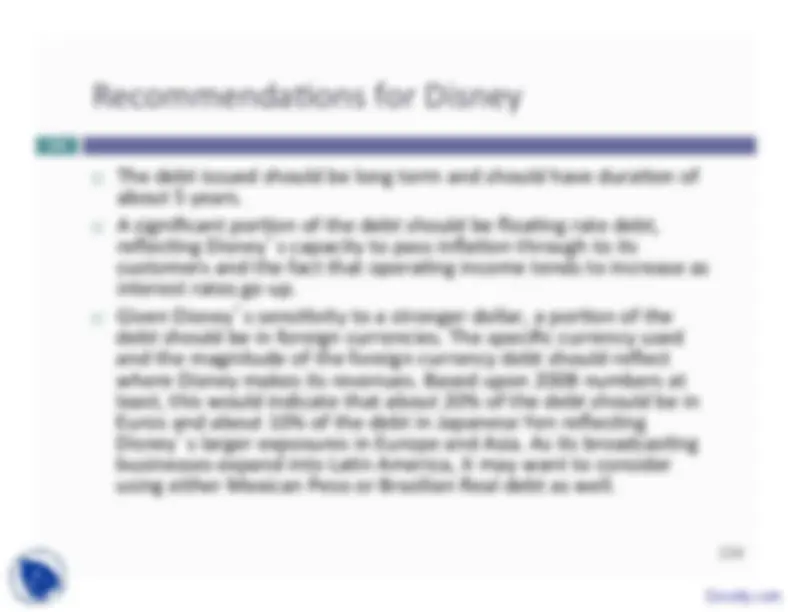

¨ Disney has $16 billion in debt with a face-‐value weighted average maturity of 5.38 years. Allowing for the fact that the maturity of debt is higher than the duraGon, this would indicate that Disney’s debt is of the right maturity. ¨ Of the debt, about 10% is yen denominated debt but the rest is in US dollars. Based on our analysis, we would suggest that Disney increase its proporGon of debt in other currencies to about 20% in Euros and about 5% in Chinese Yuan. ¨ Disney has no converGble debt and about 24% of its debt is floaGng rate debt, which is appropriate given its status as a mature company with significant pricing power. In fact, we would argue for increasing the floaGng rate porGon of the debt to about 40%.

136

AdjusGng Debt at Disney

136

¨ It can swap some of its exisGng fixed rate, dollar debt for

floaGng rate, foreign currency debt. Given Disney’s

standing in financial markets and its large market

capitalizaGon, this should not be difficult to do.

¨ If Disney is planning new debt issues, either to get to a

higher debt raGo or to fund new investments, it can use

primarily floaGng rate, foreign currency debt to fund

these new investments. Although it may be mismatching

the funding on these investments, its debt matching will

become beUer at the company level.