Download Short-Term Financing Options and more Study notes Finance in PDF only on Docsity!

Short-term Financing Options

California Debt and Investment Advisory Commission

With

Betsy Kiehn,Vice President, Stifel Nicolaus & Co.

Debra Saunders,Vice President, Fidelity Capital Markets

Introduction: Short Term Financing Options

What is “short-term”?

− Obligations that are remarketed or become due over an interim period

• 397-day maximum to meet rule 2a-7 for money market fund eligibility

For what purpose is short-term debt issued?

− Cash flow financing

• Provide working capital to pay operating expenses

− Bridge financings

• Provide interim short term financing for capital projects

− Permanent financings

• Provide long-term project funding at short-term interest rates

TRANs, RANs, and GANs

Notes issued in anticipation of receiving future tax receipts or

revenues

− Purpose: used for cash flow or capital projects

− Benefit: smooth out inconsistent revenue streams like property tax receipts

or grants

− Risks: short term and fixed repayment require careful forecasting of future

cashflows

Bond Anticipation Notes

Notes issued for capital projects. Redeemed with proceeds from

the issuance of long-term bonds

− Purpose: source of interim financing, typically for capital projects

− Benefit: can provide seed financing in advance of a planned long-term

financing

− Risks: market access at maturity, most are structured to rely primarily on the

proceeds of future bonds or note sales for repayment

Variable Rate Debt & Commercial Paper

Variable Rate Demand Obligations (VRDOs or VRDBs)

− Floating rate obligations that have a nominal long-maturity, but a coupon that

resets periodically

- Purpose: used for capital projects

- Benefit: access rates on the short end of the yield curve, retain flexibility to pay off

or restructure debt at any time

- Risks: Third-party liquidity

Commercial Paper

− Short term, unsecured promissory notes, usually backed by a LOC bank, that mature

within 270 days.

Variable Rate Market Update

Market characterized by reduced issuance, historically low rates

Interest rate environment

− Extremely low short-term rates persist; SIFMA

resets at 0.06% week of Jan 11, an all-time low

− Steep yield curve in short end due to

accommodative Fed

Supply and demand

− Significantly diminished overall issuance volume;

indexed bonds increase market share

− Tax-exempt money fund assets decrease by a net

$9bn over past 26 weeks

Credit enhancement landscape

− Liquidity remains more scarce than pre-crisis

− Pricing likely to increase due to Basel III

− Number of providers diminishes and concentration

very high

− Fewer one-stop shops; many providers want

ancillary business

Tax-Exempt Money Market Funds Assets and Fund Flows as of 2/21/

Source: Bond Buyer, ICI & SIFMA. As of 2/21/2012.

0

100

200

300

400

500

600

0

5

10

15

20

25

Feb-08Apr-08Jun-08Aug-08Oct-08Dec-08Feb-09Apr-09Jun-09Aug-09Oct-09Dec-09Feb-10Apr-10Jun-10Aug-10Oct-10Dec-10Feb-11Apr-11Jun-11Aug-11Oct-11Dec-

Fund Assets ($ Billions)

Fund Flows ($ Billions)

Tax-Exempt Money Market Assets

Liquidity Market Update

2011 saw a diminished base of providers and a high volume of facility expirations

Municipal Credit Facilities Schedule of Expirations as of 12/31/

Source: SIFMA.

The field of credit enhancers has

declined from pre-crisis levels

− Major providers: BAML, Barclays, JP Morgan,

Citibank, US Bank, Wells Fargo

− Second tier: Bank of the West, City National,

Northern Trust, RBC, Scotia, Sumitomo

Some credit providers again extending

Standby Agreements in addition to

LOCs

$131 billion of credit facility expirations

in 2011; $68 billion scheduled for 2012

Basel III likely to result in higher costs

and greater scarcity 0

2

4

6

8

10

12

14

16

18

Jan 2011 Aug 2011 Mar 2012 Oct 2012 May 2013 Dec 2013

$ Billions

SBPA LOC

Liquidity Landscape Changes

Top 10 Letter of Credit Providers 2009

Top 10 Letter of Credit Providers 2010

Top 10 Letter of Credit Providers 2011

LOC Bank

Par Amount (Millions)

Number of Issues LOC Bank

Par Amount (Millions)

Number of Issues LOC Bank

Par Amount (Millions)

Number of Issues JP Morgan Chase $3,581.60 50 JP Morgan Chase $1,981.30 28 Citibank $3,618.00 4 Wells Fargo Bank 3,021.30 62 Bank of America 1,550.10 24 JP Morgan Chase 2,769.30 35 Bank of America 2,900.80 59 Wells Fargo Bank 561.2 17 Wells Fargo Bank 1,419.10 22 U.S. Bank 2,848.50 62 TD Bank 431.6 4 Bank of America 901.8 18

SunTrust Bank 1,064.50 16 Citibank 365 5

Gov’t Development Bank of Puerto Rico 699.2 3 BB & T 1,007.90 35 PNC Bank 287.1 9 US Bank 584.7 15 TD Bank 784.3 20 Union Bank 278.1 5 RBC 478.9 5 RBS Citizens 443.6 7 Barclays Bank 210 2 PNC Bank 257.7 11 Citibank 365.5 4 U.S. Bank 207.1 5 Northern Trust 234.4 7 Northern Trust 360 7 RBS Citizens 193.1 2 BNY Mellon 214.2 6

Source: Thomson Reuters

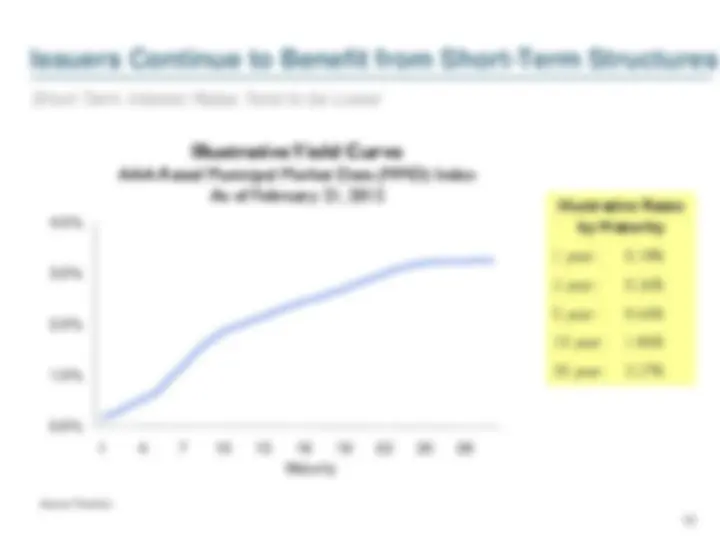

Issuers Continue to Benefit from Short-Term Structures

Illustrative Rates

by Maturity

1 year: 0.18%

2 year: 0.26%

5 year: 0.66%

10 year: 1.86%

30 year: 3.27%

Illustrative Yield Curve AAA-Rated Municipal Market Data (MMD) Index As of February 21, 2012

Source: Thomson.

Maturity

Short-Term Interest Rates Tend to be Lower

SIFMA Index vs. Revenue Bond Index (RBI)

Securities Industry & Financial Markets Association

(SIFMA) Index vs. Revenue Bond Index (RBI)

Source: SIFMA. All bonds in SIFMA Index must be tax-exempt, non-AMT, have $10mm or more outstanding and the highest short-term rating by Moody’s or S&P, and pay interest monthly with interest rate resets occurring on Wednesdays. RBI includes tax-exempt bonds maturing in 30 years with average rating of A1/A+. As of 2/21/2012.

Despite low long term rates, 30-year yield curve is extremely steep

1990 1995 2000 2005 2010

(%)

Bond Buyer 25-Bond Revenue Index SIFMA Index RBI Avg. Since 1989 SIFMA Avg. Since 1989

RBI Average = 5.67%

SIFMA Average = 2.65%

Current RBI = 4.74%

Current SIFMA = 0.17%

Strategies for Issuers of Short-Term Products

Continue to monitor cash positions and revenue trends

− Developing a strategy early on for TRAN issuance helps better position issuers

Evaluate Self-Liquidity Structures

− Market has proven that capacity exists for issuer-balance sheet secured obligations

− Significant cost advantage for strong credits

− Requires indenture flexibility for principal coming due (and put bonds)

− Proven market access required for structures that are remarketed

Continue to solicit new entrants to the credit market

− Fees have declined from peak, but remaining active participants face challenges

- Large market participants face credit capacity with large issuers and market saturation with

investors

- Smaller players can only take on $50-$75mm of any given credit