Small Business Identification

How and Why

Richard Prisinzano

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

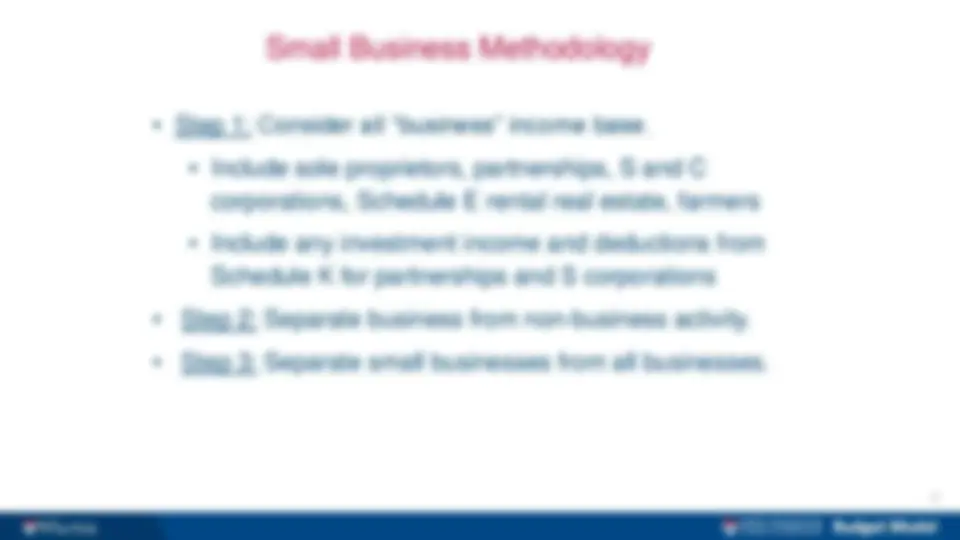

The challenges in defining small businesses for tax purposes based on the IRS tax code. It proposes a methodology for identifying small businesses by considering all business income, separating business from non-business activity, and separating small businesses from all businesses. The document also provides statistics on the number of small businesses and their employment and wages.

Typology: Lecture notes

1 / 18

This page cannot be seen from the preview

Don't miss anything!

Richard Prisinzano

Overview

Overview of Methodology

Small Business Methodology

Business Test

Identifying Businesses Thousands of Filers 0 5, 10, 15, 20, 25, 2007 Business 2010 Business 2014 Business 2007 Non 2010 Non 2014 Non C Corp S Corp Part Farm Renter Sole Prop

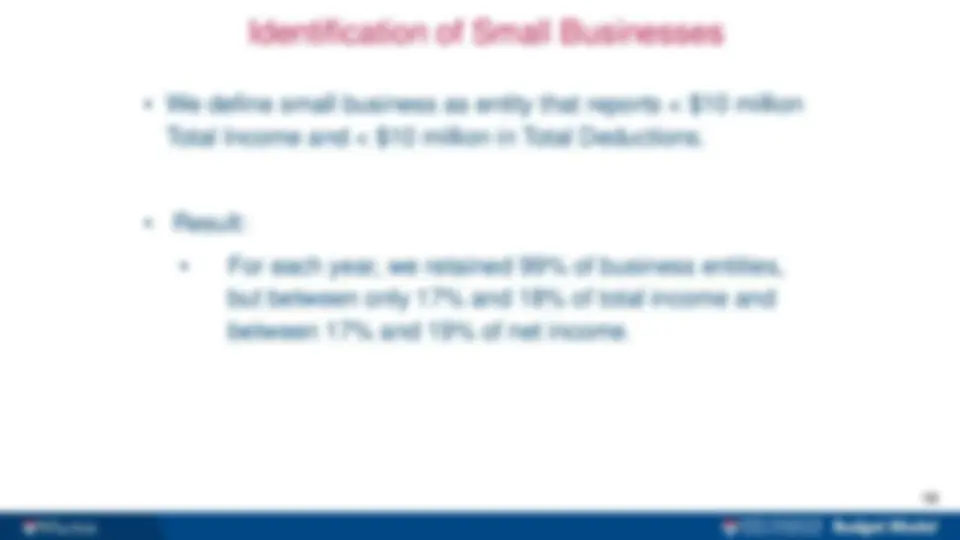

Identification of Small Businesses

Business vs. Small Business Thousands of Filers 0 5, 10, 15, 20, 25, 2007 Business 2010 Business 2014 Business 2007 Small 2010 Small 2014 Small C Corp S Corp Part Farm Renter Sole Prop

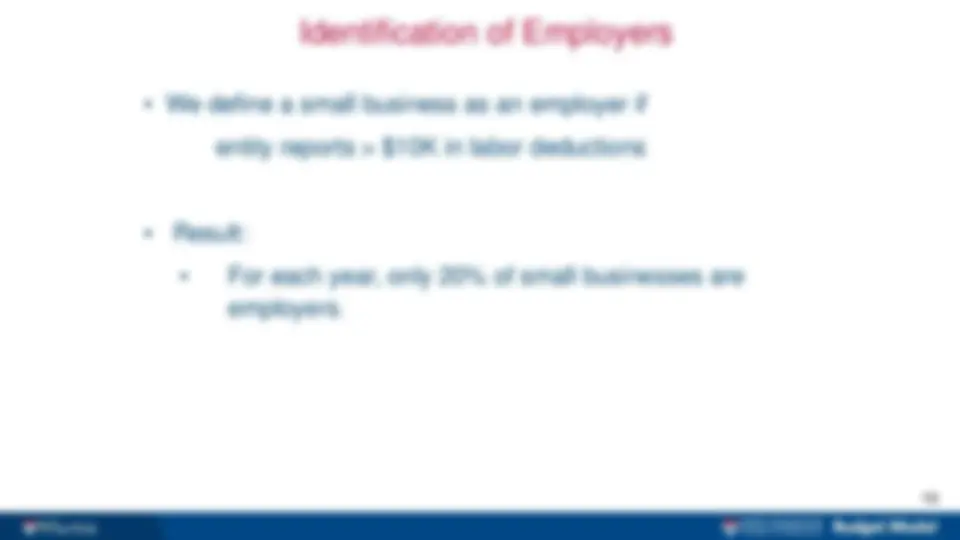

Identification of Employers

Small Business Employers Net Income, Billions of Dollars

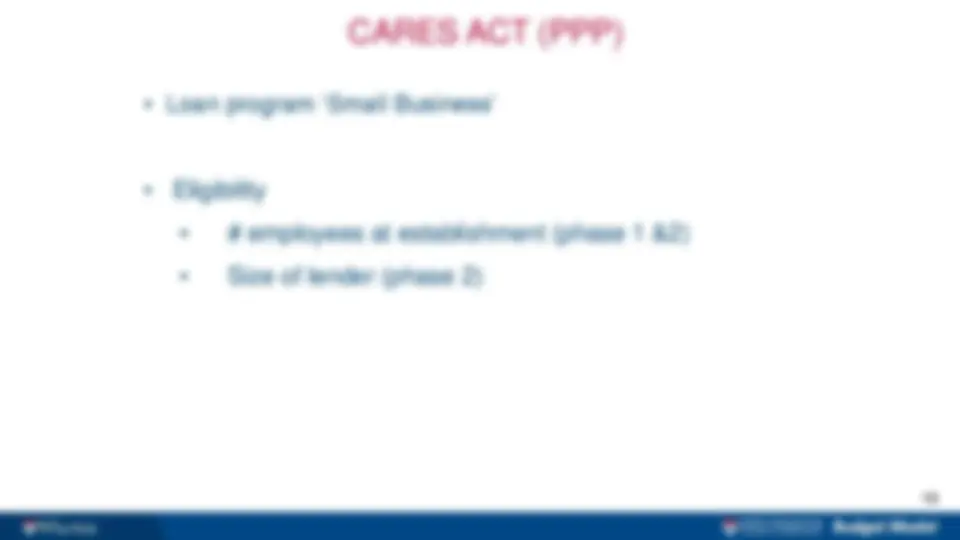

CARES ACT (PPP) Table 1. Characteristics by Firm Size, 2016 Number of Employees Number of Firms Employment Annual payroll ($1,000) 500 or more 0.3% 52.7% 59.3% Fewer than 500 99.7% 47.3% 40.7% 100 - 499 1.5% 14.0% 13.5% 20 - 99 9.0% 16.6% 14.0% 5 - 19 27.6% 11.9% 9.0% 0 - 4 61.6% 4.7% 4.2% Total 5,954,684 126,752,238 6,435,142, Source: U.S. Census Bureau, Statistics of U.S. Businesses 2016

CARES ACT (PPP) Table 2. Average Annual Growth in Wages and Employment by Size Category, 2012- 2016 Firm Size (Number of Employees) Wages Employment Percent Change Contribution to Percent Change Percent Change Contribution to Percent Change Total 4.3 4.3 2.1 2. 500 or more 4.8 2.7 2.6 1. 100 - 499 4.5 0.6 2.2 0. 50 - 99 3.4 0.2 1.8 0. 20 - 49 3.6 0.3 2.3 0. 0 - 19 3 0.4 0.7 0.