Download Solution managerial accounting and more Exercises Management Accounting in PDF only on Docsity!

CHAPTER 4

Process Costing and Hybrid Product-Costing

Systems

ANSWERS TO REVIEW QUESTIONS

4-1 In a job-order costing system, costs are assigned to batches or job orders of production. Job-order costing is used by firms that produce relatively small numbers of dissimilar products. In a process-costing system, costs are averaged over a large number of product units. Process costing is used by firms that produce large numbers of nearly identical products. 4-2 Process costing would be an appropriate product-costing system in the following industries: petroleum, food processing, lumber, chemicals, textiles, and electronics. Each of these industries is involved in the production of very large numbers of highly similar products. 4-3 Process costing could be used in the following nonmanufacturing enterprises: processing of tests in a medical diagnostic laboratory, processing of tax returns by the Internal Revenue Service, and processing of loan applications in a bank. 4-4 Product-costing systems are used for the following purposes: (a) In financial accounting: Product costs are needed to value inventory on the balance sheet and to compute the cost-of-goods-sold expense on the income statement. (b) In managerial accounting: Product costs are needed for planning, for cost control, and to provide managers with data for decision making. (c) In reporting to interested organizations: Product cost information is used to report on relationships between firms and various outside organizations. For example, hospitals keep track of the costs of medical procedures that are reimbursed by insurance companies or by the federal government under the Medicare program. Managerial Accounting, 11/e 4- 1 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

4-5 An equivalent unit is a measure of the amount of productive effort applied in the production process. In process costing, costs are assigned to equivalent units rather than to physical units. 4 - 2 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

4-10 The name ''weighted-average method'' comes from the fact that the cost per equivalent unit computed under this method is a weighted average of costs incurred during the current period and costs incurred during prior periods. 4-11 The difference between normal and actual costing lies in the calculation of the manufacturing-overhead cost of the current period. Under actual costing, the manufacturing-overhead cost of the current period is the actual overhead cost incurred during the period. Under normal costing, the current-period manufacturing overhead is computed as the product of the predetermined overhead rate and the actual level of the cost driver used to apply manufacturing overhead. 4 - 4 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

4-12 If manufacturing overhead were applied according to some activity base (or cost driver) other than direct labor, then direct-labor costs and manufacturing-overhead costs would be accounted for separately instead of being combined into one account called "conversion costs." Thus, instead of two columns for direct-material and conversion costs, there would be three columns: direct material, direct labor, and manufacturing overhead. 4-13 Operation costing is a hybrid product-costing system that is used when conversion activities are very similar across product lines, but the direct materials differ significantly. This is often the case in batch manufacturing operations. Conversion costs are accumulated by department, and process-costing methods are used to assign these costs to products. In contrast, direct-material costs are accumulated by job order or by batch, and job-order costing is used to assign direct-material costs to products. 4-14 The departmental production report is the key document in a process-costing system rather than the job-cost sheet used in job-order costing. The departmental production report shows the analysis of the physical flow of units, the calculation of equivalent units, the computation of the cost per equivalent unit, and the analysis of the total costs incurred in the production department. The report shows the cost of the ending work-in-process inventory as well as the cost of the goods completed and transferred out of the department. Managerial Accounting, 11/e 4- 5 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

EXERCISE 4-17 (15 MINUTES)

- 6,000 equivalent units (refer to (a) in the following table)

- 4,400 equivalent units (refer to (b) in the following table) CALCULATION OF EQUIVALENT UNITS: RAINBOW GLASS COMPANY Weighted-Average Method Physical Units Percentage of Completion with Respect to Conversion Equivalent Units Direct Material Conversion Work in process, October 1.... 1,000 60% Units started during October.. 5, Total units to account for........ 6, Units completed and transferred out during October........... 4,000 100% 4,000 4, Work in process, October 31.. 2,000 20% 2,000 400 Total units accounted for........ 6,000 _____ ____ Total equivalent units.............. (a) 6,000 (b) 4, Managerial Accounting, 11/e 4- 7 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

EXERCISE 4-18 (15 MINUTES)

CALCULATION OF EQUIVALENT UNITS: TERRA ENERGY COMPANY - LODI PLANT

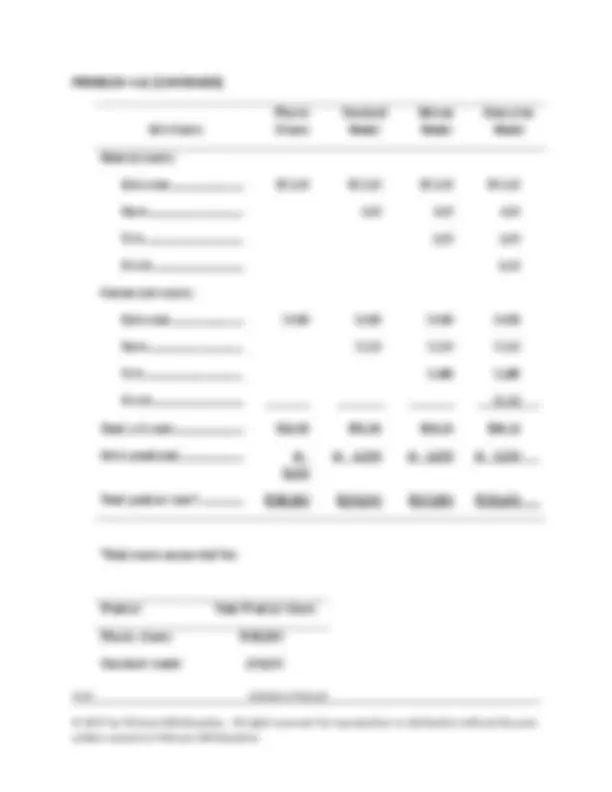

Weighted-Average Method Physical Units Percentage of Completion with Respect to Conversion Equivalent Units Direct Material Conversion Work in process, November 1................ 2,000,000 25% Units started during November............. 950, Total units to account for....................... 2,950, Units completed and transferred out during November......................... 2,710,000 100% 2,710,000 2,710, Work in process, November 30.............. 240,000 80% 240,000 192, Total units accounted for....................... 2,950,000 ________ ________ Total equivalent units............................. 2,950,000 2,902, EXERCISE 4-19 (20 MINUTES) CALCULATION OF EQUIVALENT UNITS: FIT-FOR-LIFE FOODS CORPORATION Weighted-Average Method 4 - 8 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

Costs incurred during November............. 425,000 690,000 1,115, Total costs to account for......................... $490,000 $870,000 $1,360, Equivalent units......................................... 7,000 1, Costs per equivalent unit.......................... $70* $500†^ $ *$70 = $490,000 ÷ 7, †$500 = $870,000 ÷ 1, 4 - 10 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

EXERCISE 4-21 (15 MINUTES)

CALCULATION OF COST PER EQUIVALENT UNIT: OTSEGO GLASS COMPANY

Weighted-Average Method Direct Material Conversion Total Work in process, June 1......................... $ 37,000 $ 36,750 $ 73, Costs incurred during June................... 150,000 230,000 380, Total costs to account for...................... $187,000 $266,750 $453, Equivalent units...................................... 17,000 48, Costs per equivalent unit....................... $11.00* $5.50†^ $16. *$11.00 = $187,000 ÷ 17, †$5.50 = $266,750 ÷ 48, Managerial Accounting, 11/e 4- 11 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

*Equivalent units in September 30 work in process: Direct Material Conversion Total equivalent units (weighted average)........................ 60,000 52, Units completed and transferred out................................. (50,000) (50,000) Equivalent units in ending work in process...................... 10,000 2,

- In the electronic version of the solutions manual, press the CTRL key and click on the following link: Build a Spreadsheet 04-22.xls Managerial Accounting, 11/e 4- 13 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

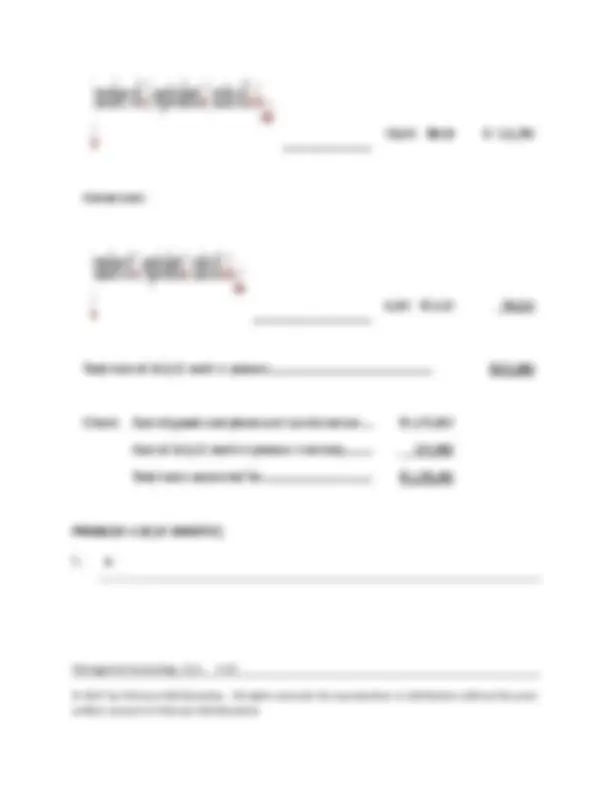

Exercise 4-23 (25 minutes) TULSA PAPERBOARD COMPANY Weighted-Average Method Direct Material Conversion Total Work in process, February 1................... $ 5,500 $ 17,000 $ 22, Costs incurred during February.............. 110,000 171,600 281, Total costs to account for........................ $115,500 $188,600 $304, Equivalent units........................................ 110,000 92, Costs per equivalent unit......................... $ 1.05 $ 2.05 $ 3.

- Cost of goods completed and transferred out during February: .......................

- Cost remaining in February 28 work in process: Direct material (20,000$1.05)... $ 21, Conversion (2,000$2.05).......... 4, Total............................................... 25, Total costs accounted for................. $304, 4 - 14 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

EXERCISE 4-24 (45 MINUTES)

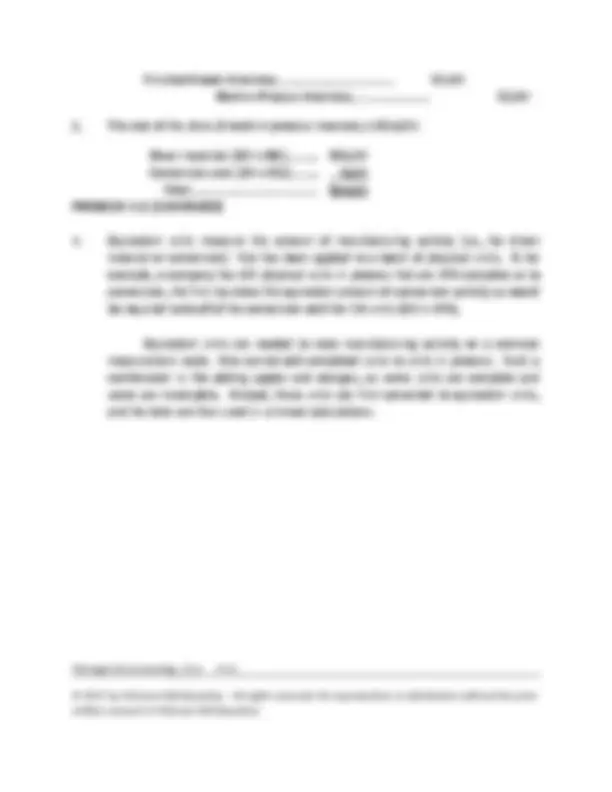

- Diagram of production process: Work-in-Process Inventory: Preparation Department Batch P25 Batch S Accumulated by department Conversion costs: Direct-labor Manufacturing overhead Work-in-Process Inventory: Finishing Department Batch P25 Batch S Accumulated by batch Direct- material costs 4 - 16 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

Work-in-Process Inventory: Packaging Department Batch P Finished-Goods Inventory Managerial Accounting, 11/e 4- 17 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

Work-in-Process Inventory: Preparation Department.......... 45,000* Raw-Material Inventory.................................................. 45, Direct-material cost for batch S33. Work-in-Process Inventory: Preparation Department.......... 45,000 Applied Conversion Costs............................................ 45, $45,000 = 6,000 units$7.50 per unit Work-in-Process Inventory: Finishing Department.............. 129,500 Work-in-Process Inventory: Preparation Department 129, *$129,500 = $39,500 + $45,000 + $45, Managerial Accounting, 11/e 4- 19 © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior

EXERCISE 4-24 (CONTINUED)

Work-in-Process Inventory: Finishing Department.............. 36,000* Applied Conversion Costs............................................ 36, $36,000 = 6,000 units$6.00 per unit Work-in-Process Inventory: Packaging Department............ 66,500 Finished-Goods Inventory...................................................... 99,000† Work-in-Process Inventory: Finishing Department..... 165, $66,500 = $39,500 + (2,000$7.50) + (2,000$6.00). These are the costs accumulated for batch P25 only. † $99,000 = $45,000 + (4,000$7.50) + (4,000$6.00). These are the costs accumulated for batch S33 only. Work-in-Process Inventory: Packaging Department............ 3, Raw-Material Inventory.................................................. 2,500 Applied Conversion Costs............................................ 1,000† *Cost of packaging material for batch P25. †$1,000 = 2,000 units$.50 per unit 4 - 20 Solutions Manual © 2017 by McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior