Stochastic Model Predictive Control

•stochastic finite horizon control

•stochastic dynamic programming

•certainty equivalent model predictive control

Prof. S. Boyd, EE364b, Stanford University

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Dr. Hanumant Chawd delivered this lecture at Alagappa University for Convex Optimization course. Its main points are: Stochastic, Model, Predictive, Control, Dynamic, Programming, Equivalent, Model, Causal, State, Feedback

Typology: Slides

1 / 15

This page cannot be seen from the preview

Don't miss anything!

stochastic finite horizon control

stochastic dynamic programming

certainty equivalent model predictive control

Prof. S. Boyd, EE364b, Stanford University

docsity.com

linear dynamical system, over finite time horizon:

x

t

Ax

t

Bu

t

w

t

t

x

t

n

is state,

u

t

m

is the input at time

t

w

t

is the process noise (or exogeneous input) at time

t

t

x

0

,... , x

t

is the state history up to time

t

causal state-feedback control:

u

t

φ

t

t

ψ

t

x

0

, w

0

,... , w

t

−

1

t

φ

t

(

t

+1)

n

m

called the control

policy

at time

t

1 docsity.com

an infinite dimensional problem: variables are

functions

φ

0

,... , φ

T

−

1

can restrict policies to finite dimensional subspace,

e.g.

φ

t

all affine

key idea: we have

recourse

(a.k.a. feedback, closed-loop control)

we can change

u

t

based on the observed state history

x

0

,... , x

t

cf standard (‘open loop’) optimal control problem, where we committo

u

0

,... , u

T

−

1

ahead of time

in general case, need to evaluate

(for given control policies) via

Monte Carlo simulation

3 docsity.com

let

t

t

be optimal value of objective, from

t

on, starting from initial

state history

t

T

T

T

x

T

⋆

0

x

0

t

can be found by backward recursion: for

t

t

t

) = inf

v

∈U

t

x

t

, v

t

t

, Ax

t

Bv

w

t

t

t

t

are convex functions

optimal policy is causal state feedback

φ

⋆t

t

) = argmin

v

∈U

t

x

t

, v

t

t

, Ax

t

Bv

w

t

t

4 docsity.com

special case of linear stochastic control

t

m

x

0

, w

0

,... , w

T

−

1

are independent, with

x

0

w

t

x

0

x

T 0

w

t

w

Tt

t

t

x

t

, u

t

x

Tt

t

x

t

u

Tt

t

u

t

, with

t

t

T

x

T

x

TT

T

x

T

, with

T

6 docsity.com

can show value functions are quadratic,

i.e.

t

x

t

x

Tt

t

x

t

q

t

t

Bellman recursion:

T

T

q

T

; for

t

t

z

inf

v

z

T

t

z

v

T

t

v

Az

Bv

w

t

T

t

Az

Bv

w

t

q

t

works out to

t

T

t

T

t

T

t

t

−

1

T

t

t

q

t

q

t

Tr

t

t

7 docsity.com

at every time

t

we solve the certainty equivalent problem

minimize

T

−

1

τ

=

t

t

x

τ

, u

τ

T

x

T

subject to

u

τ

τ

τ

t,... , T

x

τ

Ax

τ

Bu

τ

w

τ

|

t

τ

t,... , T

with variables

x

t

,... , x

T

u

t

,... , u

T

−

1

and data

x

t

w

t

|

t

w

T

−

1

|

t

w

t

|

t

w

T

−

1

|

t

are predicted values of

w

t

,... , w

T

−

1

based on

t

e.g.

, conditional expectations)

call solution

˜x

t

x

T

u

t

˜u

T

−

1

we take

φ

mpc

t

u

t

φ

mpc

is a function of

t

since

w

t

|

t

w

T

−

1

|

t

are functions of

t

9 docsity.com

widely used,

e.g.

, in ‘revenue management’

based on (bad) approximations: –

future values of disturbance are exactly as predicted; there is nofuture uncertainty

in future, no recourse is available

yet, often works very well

10 docsity.com

sample trace of

x

1

and

u

1

0

10

20

30

40

50

−1 −

2 1 0

0

10

20

30

40

50

−0.

0

x 1 )t( u

1 )t(

t

Prof. S. Boyd, EE364b, Stanford University

12 docsity.com

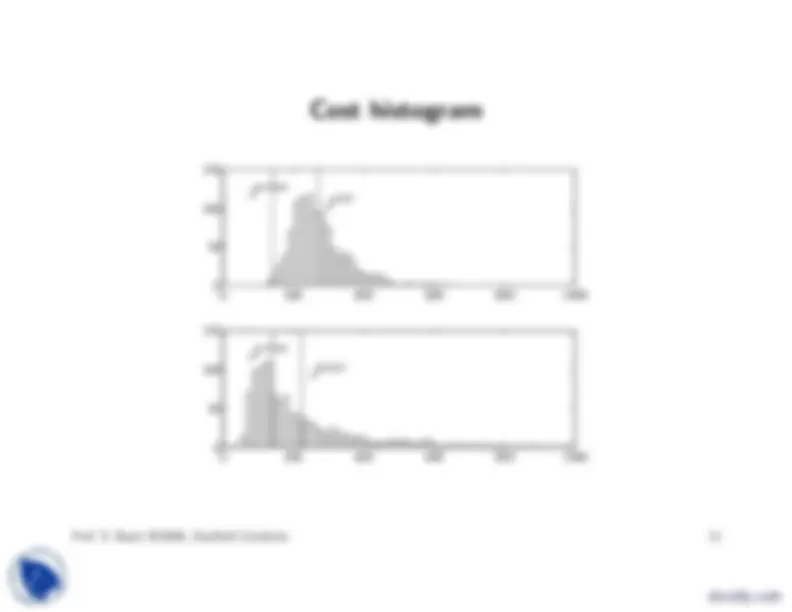

0

200

400

600

800

1000

0 50 150 100

0

200

400

600

800

1000

0 50 150 100

J

mpc

J

relax

J

relax

J

sat

13 docsity.com