Demand and Supply

Chapter 3

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

chapter 3 supply and demand economics 2026

Typology: Lecture notes

1 / 52

This page cannot be seen from the preview

Don't miss anything!

After studying this chapter, you will be able to:

➢ If you effectively demand something, then you:

The law of demand states:

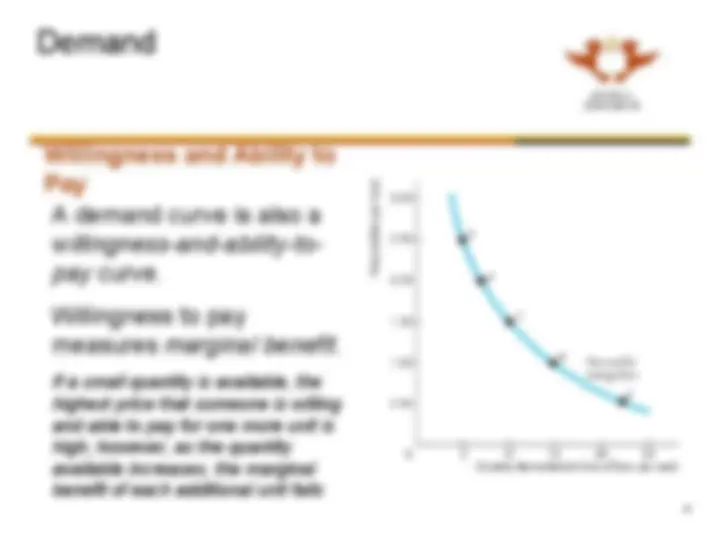

Demand Curve and Demand Schedule ➢ The term demand refers to the entire relationship between the price of the good and quantity demanded of the good. ➢ A demand curve shows the relationship between the quantity demanded of a good and its price when all other influences on consumers’ planned purchases remain the same. ➢ A demand schedule lists the quantities demanded at each price when all the other influences on consumers’ planned purchases remain the same (^7)

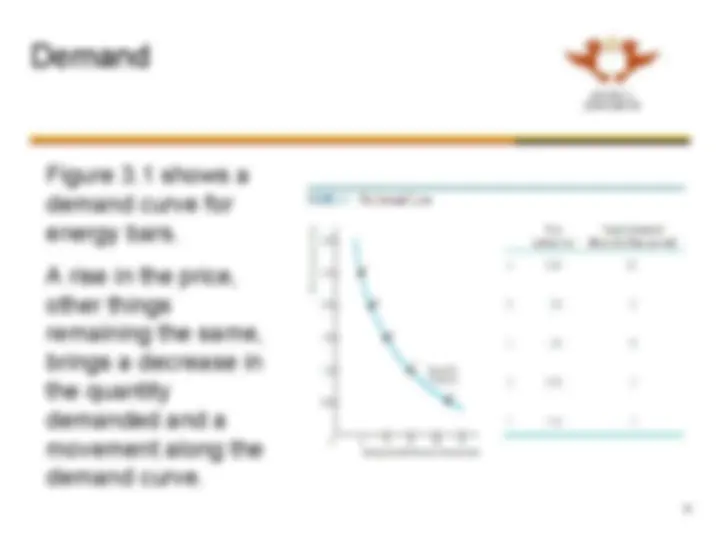

Figure 3.1 shows a demand curve for energy bars. A rise in the price, other things remaining the same, brings a decrease in the quantity demanded and a movement along the demand curve.

A Change in Demand ➢ When some influence on buying plans other than the price of the good changes, there is a change in demand for that good. ➢ The quantity of the good that people plan to buy changes at each and every price, so there is a new demand curve.

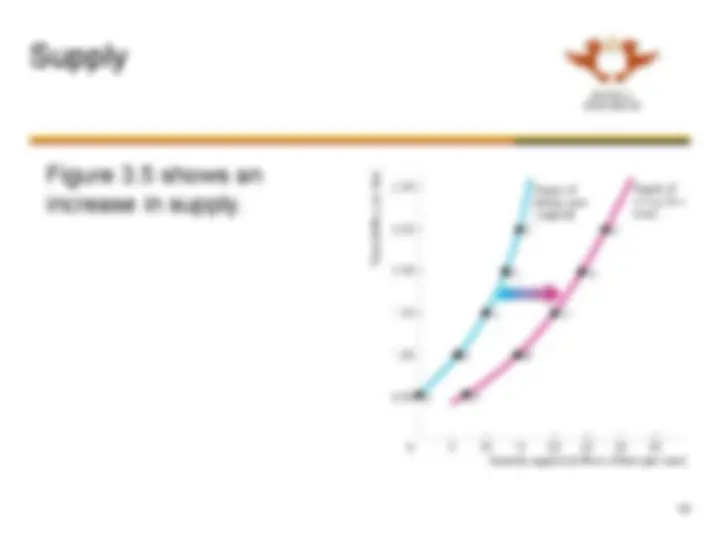

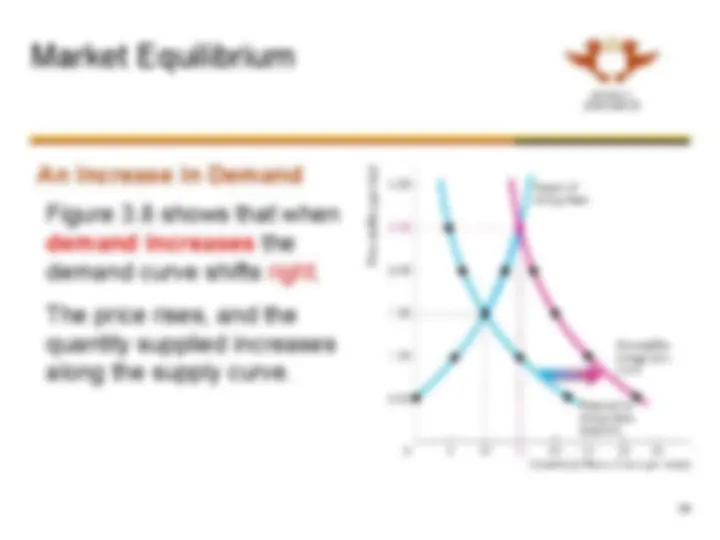

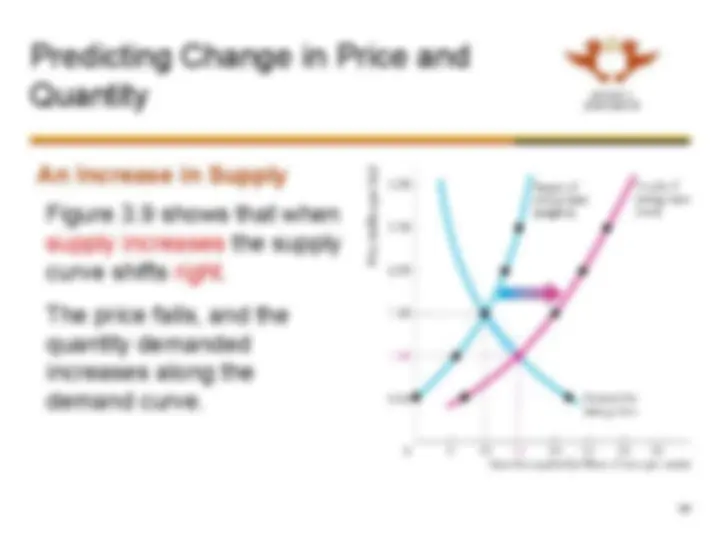

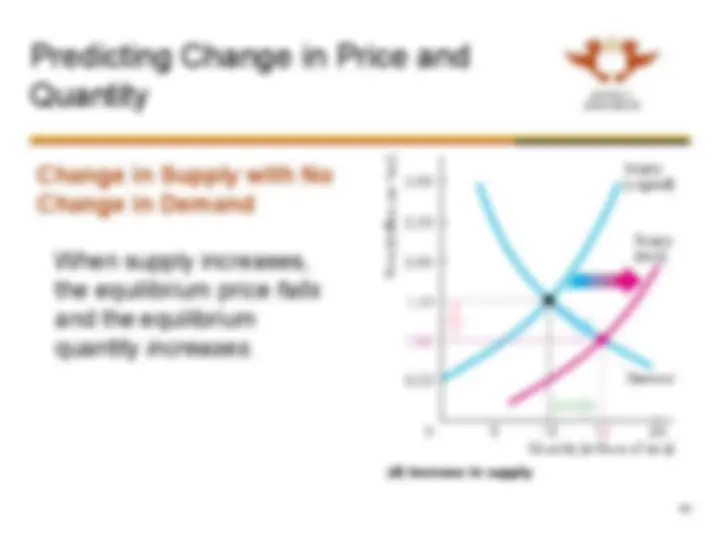

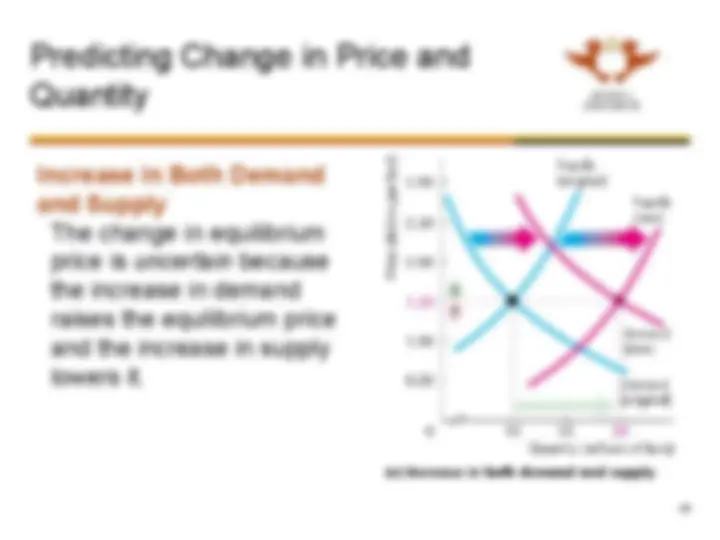

A Change in Demand ➢ When demand increases , the demand curve shifts rightward. ➢ When demand decreases , the demand curve shifts leftward.

Six main factors that change demand are The prices of related goods Expected future prices Income Expected future income and credit Population Preferences Can you think of any more?

Prices of Related Goods A substitute is a good that can be used in place of another good. A complement is a good that is used in conjunction with another good.

Income When income increases, consumers buy more of most goods and the demand curve shifts rightward. A normal good is one for which demand increases as income increases. An inferior good is a good for which demand decreases as income increases.

Expected Future Income and Credit When income is expected to increase in the future or when credit is easy to obtain, the demand might increase now. Population The larger the population, the greater is the demand for all goods. Preferences People with the same income have different demands if they have different preferences.

Supply If a firm supplies a good or service, then the firm

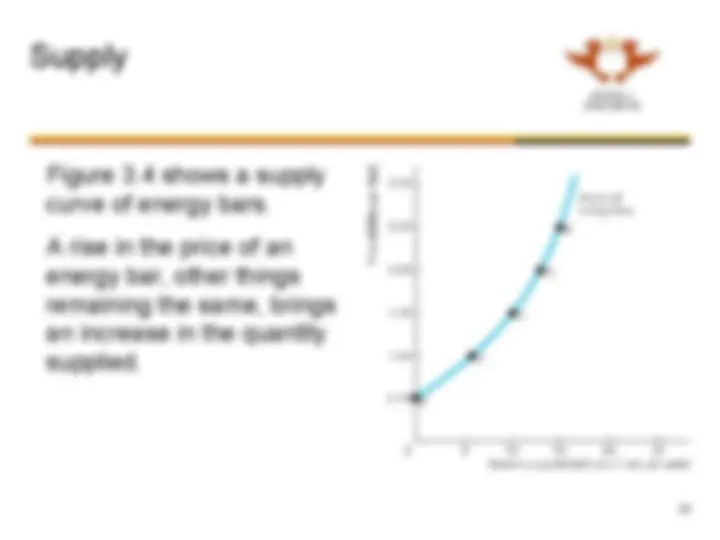

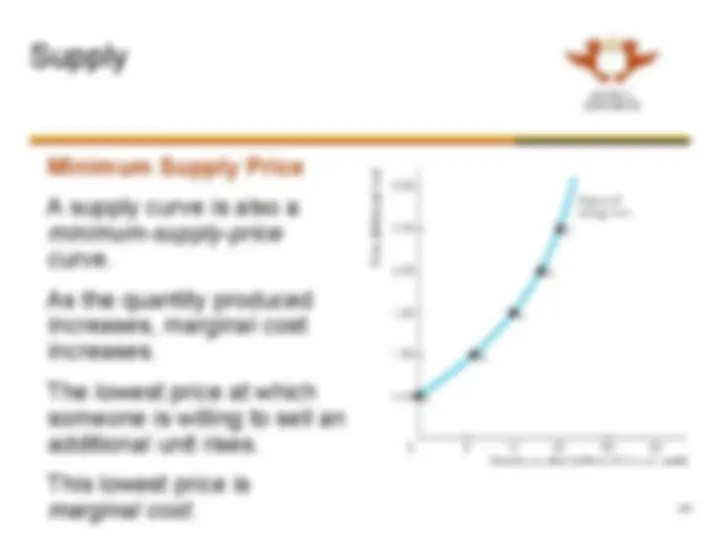

Supply ➢ Resources and technology determine what it is possible to produce. Supply reflects a decision about which technologically feasible items to produce. ➢ The quantity supplied of a good or service is the amount that producers plan to sell during a given time period at a particular price.