Download Targeting Monetary Aggregates - Banking - Lecture Slides and more Slides Banking and Finance in PDF only on Docsity!

THE HISTORICAL EXPERIENCE OF TARGETING MONETARY AGGREGATES Background – review. Monetarist theory and critique of Keynesian DMP; argument for rules.

Monetarism and party politics in the 1970s. ‘Demand-pull’, ‘cost-push’. Direct targeting: Y, P. Inflation in 1970s.

Monetarism in practice: Phase 1: Doctrinaire monetarism , 1979-82. ‘Cuts’. Recession. Phase 2: Pragmatic monetarism , 1982-5. Tacit return of DMP. Phase 3: Pragmatism. Goodhart’s law. Shift to ER focus

Assessment of Thatcher monetarist policies. Balance of pain and gain. Models assessed.

Problems of M aggregate targeting Controllability. Predictability. Direction of causation. Goodhart’s Law.Docsity.com

Monetarists: MS has stable relation to PY.

Policy swings on monetary aggregates principal cause of cycle.

“It is a matter of record that periods of relative stability in the rate of monetary growth have also been periods of relative stability in economic activity, both in the United States and other countries.” (Friedman and Schwartz). Shaded areas show recessions

Direct and indirect targets:

MP and direct targeting of Y and P.

Goals of MP = goals of macro policy as a whole:

- Low u and π , high and steady growth , BOP , etc.

- So why not target the goals directly?

- Particularly:

(1) Target Y?

(2) Target P?

Monetarist critique of Keynesian DMP in post-war decades.

→ Remain the basis of current arguments against this.

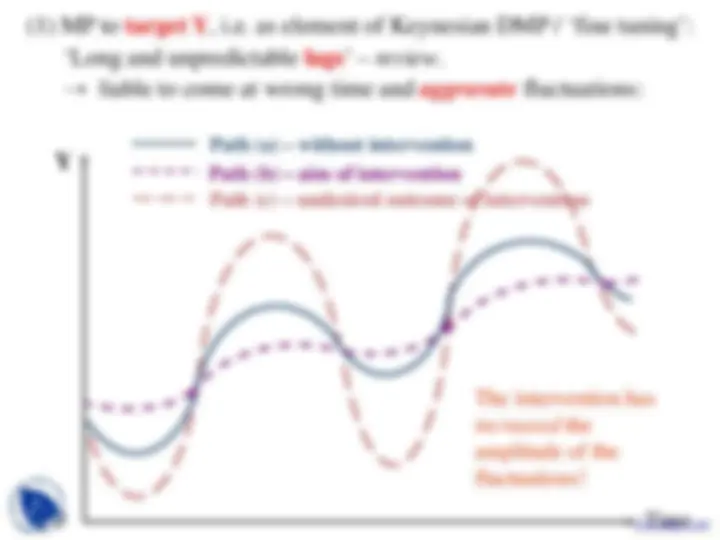

O (^) Time

Path (a) – without intervention

Path (c) – undesired outcome of intervention

Path (b) – aim of intervention

The intervention has increased the amplitude of the fluctuations!

Y

(1) MP to target Y , i.e. as element of Keynesian DMP / ‘fine tuning’:

‘Long and unpredictable lags ’ – review. → liable to come at wrong time and aggravate fluctuations:

(2) Targeting P :

1960s-70s: P&I policies of UK governments But monetary authorities today (usually CB) not in position to intervene in this way. Monetarists are against intervention anyway.

Monetarist alternative :

MP should focus instead on ‘ intermediate targets ’. i.e. Targets which affect Y and P , etc. Target which has affect over shorter and more predictable period > ‘long and unpredictable lags’. Usual intermediate target: a monetary aggregate.

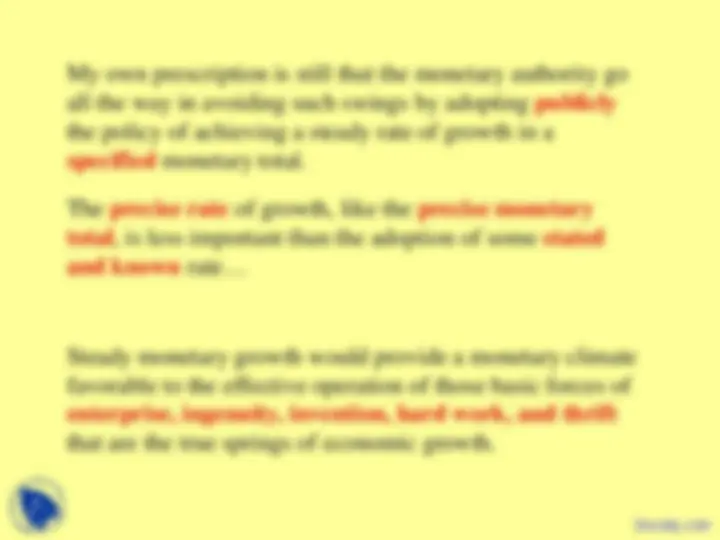

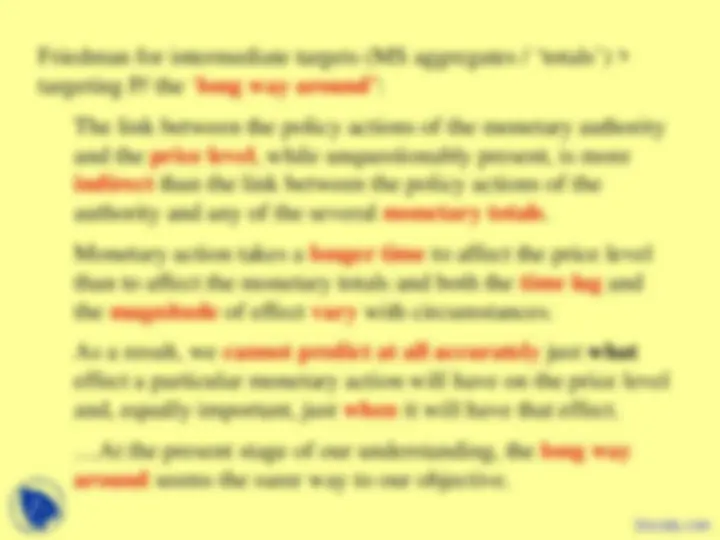

Friedman for intermediate targets (MS aggregates / ‘totals’) > targeting P/ the ‘ long way around’ :

The link between the policy actions of the monetary authority and the price level , while unquestionably present, is more indirect than the link between the policy actions of the authority and any of the several monetary totals. Monetary action takes a longer time to affect the price level than to affect the monetary totals and both the time lag and the magnitude of effect vary with circumstances. As a result, we cannot predict at all accurately just what effect a particular monetary action will have on the price level and, equally important, just when it will have that effect. …At the present stage of our understanding, the long way around seems the surer way to our objective.

Inflation – ‘Cost-Push’ from oil prices:

1973-4 – Arab-Israeli war October 1973; Arab oil boycott. 1979-80 – Iranian revolution.

Much comment on 1970s π emphasises these ‘oil shocks’:

i.e. emphasis on π from external ‘ Cost-Push’.

BUT:

UK π exceptionally severe > other industrialised countries

→ Domestic factors also need emphasis:

- Cost-Push from wage inflation as well as oil. Industrial disputes of 1970s: miners, etc.

- Demand-Pull from expansionary MP.

Inflation – demand-pull from DMP?

Monetarist view : π is a monetary phenomenon only.

π is “always and everywhere a monetary phenomenon” (Friedman), i.e. ultimately / LR, QTM holds. i.e. π a demand-pull effect of expansionary MP.

Might fit early 1970s :

- Recession → reflationary measures 1972 / ‘Barber boom’.

- Overtaken by global boom during 1973. → Already severe inflationary pressure summer 1973.

- Then ‘oil shock’ , October 1973 – i.e. just a catalyst for an underlying D-pull π problem.