Interest rate models and derivatives

The LIBOR Market model

José Figueroa-López

Purdue University

Math 516 / Stat 541

Fall, 2008

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Material Type: Notes; Class: Elementary Algebra; Subject: Mathematics - IU; University: Purdue University - Main Campus; Term: Fall 2008;

Typology: Study notes

1 / 59

This page cannot be seen from the preview

Don't miss anything!

The LIBOR Market model

José Figueroa-López

Purdue University

Math 516 / Stat 541 Fall, 2008

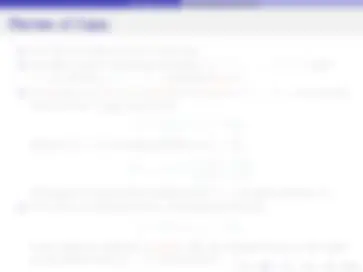

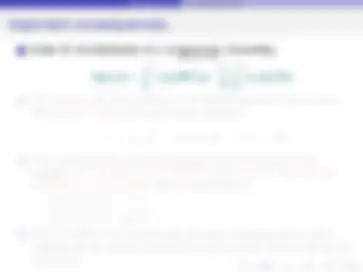

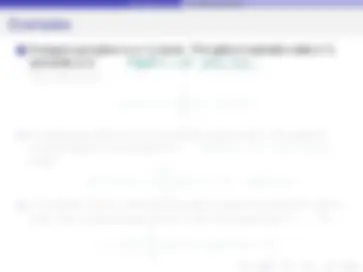

LIBOR Market model. Introduction.

1 The market quotes several important interest rate derivative, specifically cap/floors, as if the spot LIBOR forward rates L(t; S, T ) were lognormal. 2 Empirical evidence showed that parsimonious short-rate models does not account for the stylized features of the cap/floor and swaption market prices. 3 The inconsistencies inherent in short-rate models raise the problem of devising an arbitrage-free model that is consistent with the log-normality of LIBOR rates. 4 Moreover, we would like to determine an arbitrage-free model that can be easily calibrated to the market prices of traded cap/floors. 5 What will we gain?

LIBOR Market model. Introduction.

1 The market quotes several important interest rate derivative, specifically cap/floors, as if the spot LIBOR forward rates L(t; S, T ) were lognormal. 2 Empirical evidence showed that parsimonious short-rate models does not account for the stylized features of the cap/floor and swaption market prices. 3 The inconsistencies inherent in short-rate models raise the problem of devising an arbitrage-free model that is consistent with the log-normality of LIBOR rates. 4 Moreover, we would like to determine an arbitrage-free model that can be easily calibrated to the market prices of traded cap/floors. 5 What will we gain?

LIBOR Market model. Introduction.

1 The market quotes several important interest rate derivative, specifically cap/floors, as if the spot LIBOR forward rates L(t; S, T ) were lognormal. 2 Empirical evidence showed that parsimonious short-rate models does not account for the stylized features of the cap/floor and swaption market prices. 3 The inconsistencies inherent in short-rate models raise the problem of devising an arbitrage-free model that is consistent with the log-normality of LIBOR rates. 4 Moreover, we would like to determine an arbitrage-free model that can be easily calibrated to the market prices of traded cap/floors. 5 What will we gain?

LIBOR Market model. Introduction.

1 The market quotes several important interest rate derivative, specifically cap/floors, as if the spot LIBOR forward rates L(t; S, T ) were lognormal. 2 Empirical evidence showed that parsimonious short-rate models does not account for the stylized features of the cap/floor and swaption market prices. 3 The inconsistencies inherent in short-rate models raise the problem of devising an arbitrage-free model that is consistent with the log-normality of LIBOR rates. 4 Moreover, we would like to determine an arbitrage-free model that can be easily calibrated to the market prices of traded cap/floors. 5 What will we gain?

LIBOR Market model. Introduction.

1 The market quotes several important interest rate derivative, specifically cap/floors, as if the spot LIBOR forward rates L(t; S, T ) were lognormal. 2 Empirical evidence showed that parsimonious short-rate models does not account for the stylized features of the cap/floor and swaption market prices. 3 The inconsistencies inherent in short-rate models raise the problem of devising an arbitrage-free model that is consistent with the log-normality of LIBOR rates. 4 Moreover, we would like to determine an arbitrage-free model that can be easily calibrated to the market prices of traded cap/floors. 5 What will we gain?

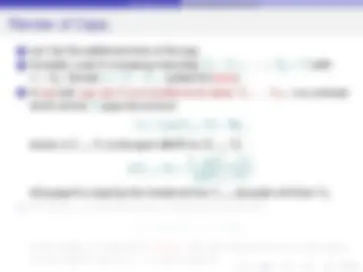

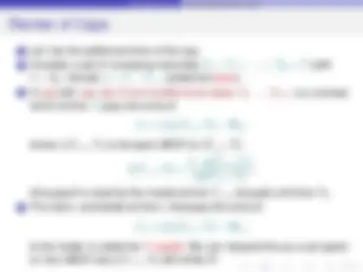

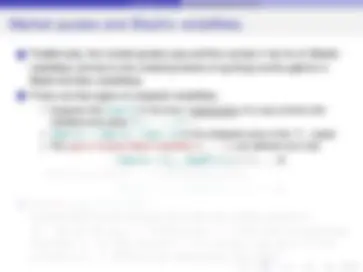

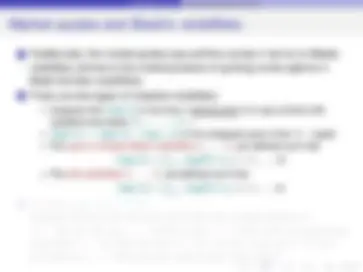

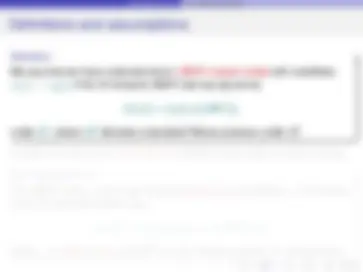

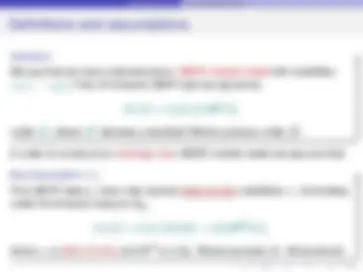

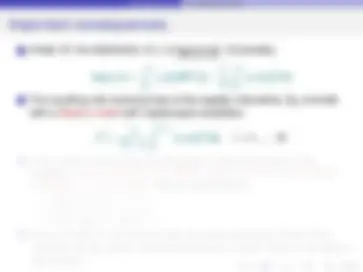

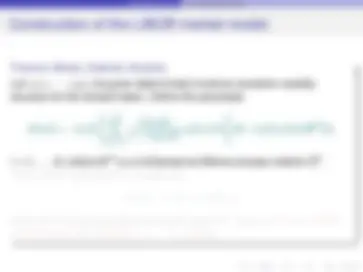

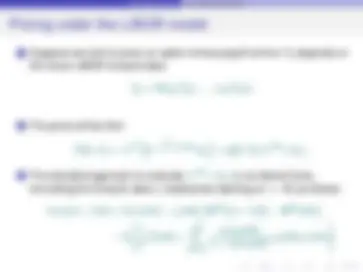

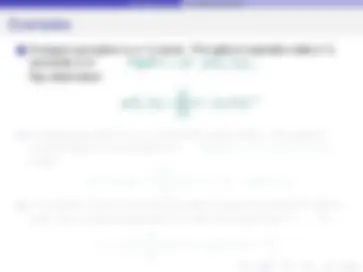

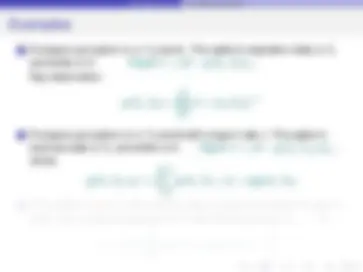

LIBOR Market model. Market pricing practices for caps.

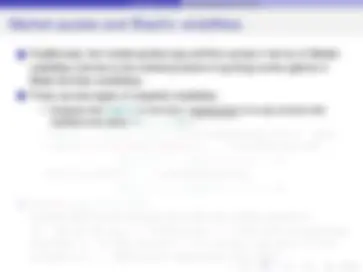

1 Let t be the settlement time of the cap. 2 Consider a set of increasing maturities T 0 < T 1 < · · · < TN = T (with t ≤ T 0 ). Denote δi = Ti − Ti− 1 (called the tenor). 3 A cap with cap rate R and resettlements dates T 0 ,... , TN− 1 is a contract which at time Ti pays the amount Xi = δi (L(Ti− 1 , Ti ) − R)+,

where L(Ti− 1 , Ti ) is the spot LIBOR on [Ti− 1 , Ti ]:

L(Ti− 1 , Ti ) =

1 − p(Ti− 1 , Ti ) δi p(Ti− 1 , Ti )

(this payoff is reset by the market at time Ti− 1 , but paid until time Ti ). 4 The claim, contracted at time t, that pays the amount

Xi = δi (L(Ti− 1 , Ti ) − R)+,

to the holder is called the Ti -caplet. We can interpret this as a call option on the LIBOR rate L(Ti− 1 , Ti ) with strike R.

LIBOR Market model. Market pricing practices for caps.

1 Let t be the settlement time of the cap. 2 Consider a set of increasing maturities T 0 < T 1 < · · · < TN = T (with t ≤ T 0 ). Denote δi = Ti − Ti− 1 (called the tenor). 3 A cap with cap rate R and resettlements dates T 0 ,... , TN− 1 is a contract which at time Ti pays the amount Xi = δi (L(Ti− 1 , Ti ) − R)+,

where L(Ti− 1 , Ti ) is the spot LIBOR on [Ti− 1 , Ti ]:

L(Ti− 1 , Ti ) =

1 − p(Ti− 1 , Ti ) δi p(Ti− 1 , Ti )

(this payoff is reset by the market at time Ti− 1 , but paid until time Ti ). 4 The claim, contracted at time t, that pays the amount

Xi = δi (L(Ti− 1 , Ti ) − R)+,

to the holder is called the Ti -caplet. We can interpret this as a call option on the LIBOR rate L(Ti− 1 , Ti ) with strike R.

LIBOR Market model. Market pricing practices for caps.

1 Let t be the settlement time of the cap. 2 Consider a set of increasing maturities T 0 < T 1 < · · · < TN = T (with t ≤ T 0 ). Denote δi = Ti − Ti− 1 (called the tenor). 3 A cap with cap rate R and resettlements dates T 0 ,... , TN− 1 is a contract which at time Ti pays the amount Xi = δi (L(Ti− 1 , Ti ) − R)+,

where L(Ti− 1 , Ti ) is the spot LIBOR on [Ti− 1 , Ti ]:

L(Ti− 1 , Ti ) =

1 − p(Ti− 1 , Ti ) δi p(Ti− 1 , Ti )

(this payoff is reset by the market at time Ti− 1 , but paid until time Ti ). 4 The claim, contracted at time t, that pays the amount

Xi = δi (L(Ti− 1 , Ti ) − R)+,

to the holder is called the Ti -caplet. We can interpret this as a call option on the LIBOR rate L(Ti− 1 , Ti ) with strike R.

LIBOR Market model. Market pricing practices for caps.

1 Let t be the settlement time of the cap. 2 Consider a set of increasing maturities T 0 < T 1 < · · · < TN = T (with t ≤ T 0 ). Denote δi = Ti − Ti− 1 (called the tenor). 3 A cap with cap rate R and resettlements dates T 0 ,... , TN− 1 is a contract which at time Ti pays the amount Xi = δi (L(Ti− 1 , Ti ) − R)+,

where L(Ti− 1 , Ti ) is the spot LIBOR on [Ti− 1 , Ti ]:

L(Ti− 1 , Ti ) =

1 − p(Ti− 1 , Ti ) δi p(Ti− 1 , Ti )

(this payoff is reset by the market at time Ti− 1 , but paid until time Ti ). 4 The claim, contracted at time t, that pays the amount

Xi = δi (L(Ti− 1 , Ti ) − R)+,

to the holder is called the Ti -caplet. We can interpret this as a call option on the LIBOR rate L(Ti− 1 , Ti ) with strike R.

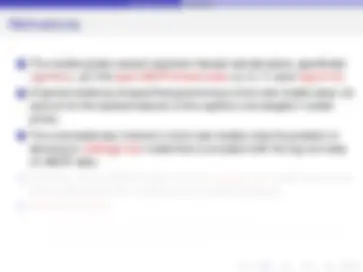

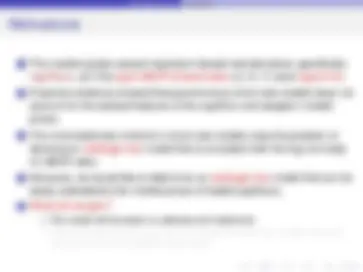

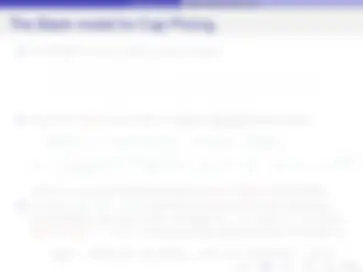

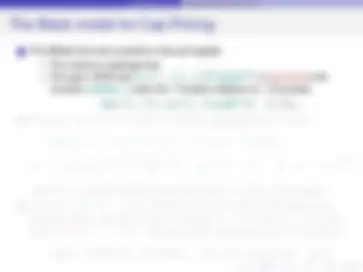

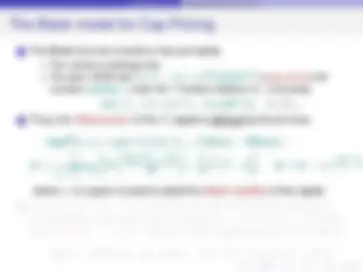

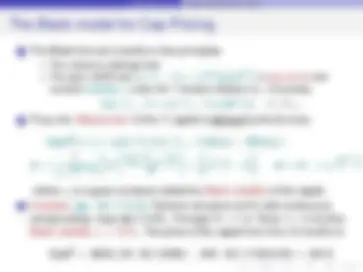

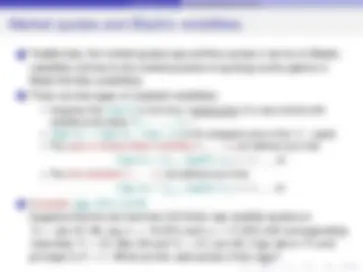

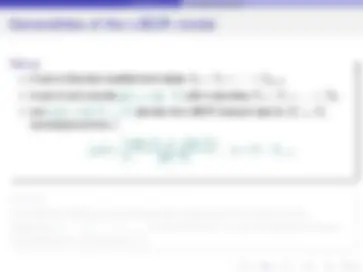

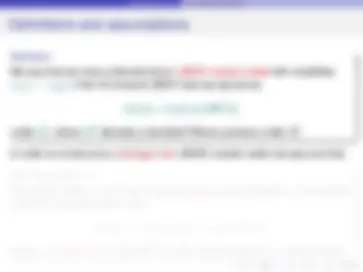

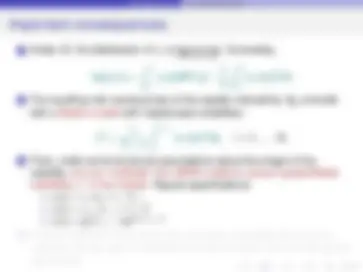

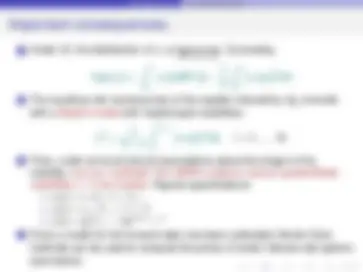

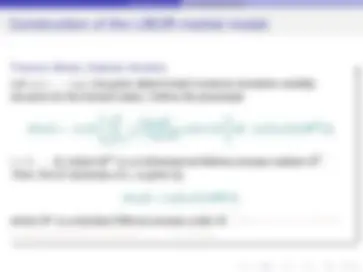

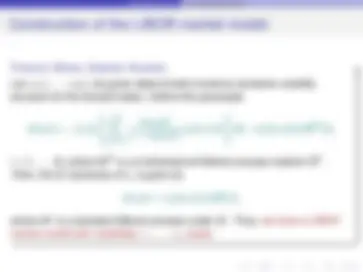

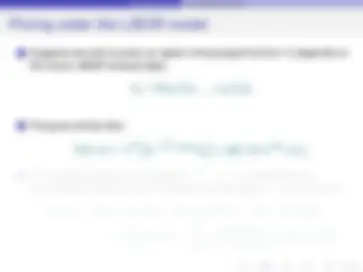

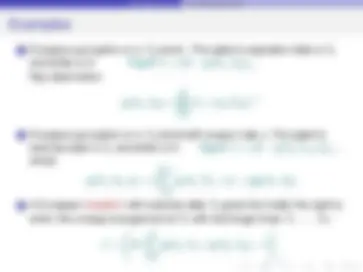

LIBOR Market model. Market pricing practices for caps.

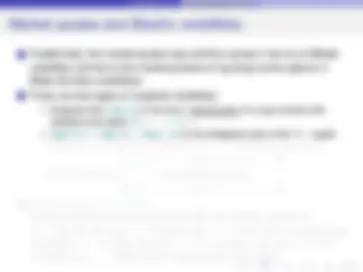

1 The Black formula is build on two principles:

CapliB (t; σi ) = δi p(t, Ti ) {L(t; Ti− 1 , Ti )N(d 1 ) − RN(d 2 )} ,

d 1 =

σi

Ti − t

ln

L(t; Ti− 1 , Ti ) R

2 σ

2 i (Ti^ −^ t)

, d 2 = d 1 − σi

Ti − t,

where σi is a given constant called the Black volatility of the caplet. 3 Example: [pp. 191, C & S]. Flat term structure at 5% with continuous compounding. Cap rate if 4. 5 %. Principal K = 1 m. Tenor δ = 3 months. Black volatility σi = 10 %. The price of the caplet from 9 to 10 months is

CapliB =. 9632 (. 05 · N( 1. 2599 ) −. 045 · N( 1. 1733 ) 0. 25 ) =. 0013.

LIBOR Market model. Market pricing practices for caps.

1 The Black formula is build on two principles:

CapliB (t; σi ) = δi p(t, Ti ) {L(t; Ti− 1 , Ti )N(d 1 ) − RN(d 2 )} ,

d 1 =

σi

Ti − t

ln

L(t; Ti− 1 , Ti ) R

2 σ

2 i (Ti^ −^ t)

, d 2 = d 1 − σi

Ti − t,

where σi is a given constant called the Black volatility of the caplet. 3 Example: [pp. 191, C & S]. Flat term structure at 5% with continuous compounding. Cap rate if 4. 5 %. Principal K = 1 m. Tenor δ = 3 months. Black volatility σi = 10 %. The price of the caplet from 9 to 10 months is

CapliB =. 9632 (. 05 · N( 1. 2599 ) −. 045 · N( 1. 1733 ) 0. 25 ) =. 0013.

LIBOR Market model. Market pricing practices for caps.

1 The Black formula is build on two principles:

CapliB (t; σi ) = δi p(t, Ti ) {L(t; Ti− 1 , Ti )N(d 1 ) − RN(d 2 )} ,

d 1 =

σi

Ti − t

ln

L(t; Ti− 1 , Ti ) R

2 σ

2 i (Ti^ −^ t)

, d 2 = d 1 − σi

Ti − t,

where σi is a given constant called the Black volatility of the caplet. 3 Example: [pp. 191, C & S]. Flat term structure at 5% with continuous compounding. Cap rate if 4. 5 %. Principal K = 1 m. Tenor δ = 3 months. Black volatility σi = 10 %. The price of the caplet from 9 to 10 months is

CapliB =. 9632 (. 05 · N( 1. 2599 ) −. 045 · N( 1. 1733 ) 0. 25 ) =. 0013.

LIBOR Market model. Market pricing practices for caps.

1 The Black formula is build on two principles:

CapliB (t; σi ) = δi p(t, Ti ) {L(t; Ti− 1 , Ti )N(d 1 ) − RN(d 2 )} ,

d 1 =

σi

Ti − t

ln

L(t; Ti− 1 , Ti ) R

2 σ

2 i (Ti^ −^ t)

, d 2 = d 1 − σi

Ti − t,

where σi is a given constant called the Black volatility of the caplet. 3 Example: [pp. 191, C & S]. Flat term structure at 5% with continuous compounding. Cap rate if 4. 5 %. Principal K = 1 m. Tenor δ = 3 months. Black volatility σi = 10 %. The price of the caplet from 9 to 10 months is

CapliB =. 9632 (. 05 · N( 1. 2599 ) −. 045 · N( 1. 1733 ) 0. 25 ) =. 0013.