Download Maximizing Sharpe Ratio in Portfolio Optimization under Uncertainty and more Slides Statistics in PDF only on Docsity!

Two-Fund Separation under Model Mis-Specification

Seung-Jean Kim∗^ Stephen Boyd∗

Working paper, January 2008

Abstract The two-fund separation theorem tells us that an investor with quadratic utility can separate her asset allocation decision into two steps: First, find the tangency portfolio (TP), i.e., the portfolio of risky assets that maximizes the Sharpe ratio (SR); and then, decide on the mix of the TP and the risk-free asset, depending on the investor’s attitude toward risk. In this paper, we describe an extension of the two-fund separation theorem that takes into account uncertainty in the model parameters (i.e., the expected return vector and covariance of asset returns) and uncertainty aversion of investors. The extension tells us that when the uncertainty model is convex, an investor with quadratic utility and uncertainty aversion can separate her investment problem into two steps: First, find the portfolio of risky assets that maximizes the worst-case SR (over all possible asset return statistics); and then, decide on the mix of this risky portfolio and the risk-free asset, depending on the investor’s attitude toward risk. The risky portfolio is the TP corresponding to the least favorable asset return statistics, with portfolio weights chosen optimally. We will show that the least favorable statistics (and the associated TP) can be found efficiently by solving a convex optimization problem.

1 Introduction

The two-fund separation theorem [53] is a central result in modern portfolio theory pioneered by Markowitz [39, 40]. It tells us that the risk-return pair of any admissible or feasible portfolio cannot lie above the capital market line (CML) in the risk-return space, obtained by combining the risk-free asset and the portfolio that maximizes the Sharpe ration (SR). An important implication is that an investor can separate her asset allocation decision into two steps: First, find the portfolio of risky assets that maximizes the SR; then, decide on the mix of the optimal risky portfolio and the risk-free asset, depending on her attitude toward risk. Sharpe [50] and Lintner [34] derive the implications of the two-fund separation property for equilibrium prices, which is known as the capital asset pricing model (CAPM).

∗Information Systems Laboratory, Department of Electrical Engineering, Stanford University, Stanford,

CA 94305-9510. ({sjkim,boyd}@stanford.edu)

The two-step asset allocation process is based on the assumption that there is no model uncertainty or model mis-specification, i.e., the input data or parameters (the mean vector and covariance matrix of asset returns) are perfectly known. These input parameters are typically empirically estimated from historical data of asset returns, or from extensive anal- ysis of various types of information about the assets and macro-economic conditions. Due to inevitable imperfections in the analysis and estimation procedure, the parameters are esti- mated with error. The standard two-step asset allocation process can be very sensitive to the estimation error: Portfolios constructed on the basis of estimated values of the parameters cam have very poor performance for another set of parameters that is similar and statisti- cally indistinguishable from the one used in the allocation decision [28]. The literature on the sensitivity problem of MV allocation to estimation error or model uncertainty is huge; see, [3, 4, 8, 7, 23, 27, 43] to name a few. A variety of approaches have been suggested for alleviating the sensitivity problem in MV asset allocation. The list includes imposing constraints such as no short-sales constraints [26], the resampling approach [43], Bayesian approaches [1, 9, 31, 44, 45, 56], the shrinkage approach [13, 55, 24], the empirical Bayes approach [19], the Black-Litterman approach [4] (which allows investors to incorporate economic views into the asset allocation process), and the worst-case approach [11, 16, 20, 25, 29, 28, 54, 47, 49]. The reader is referred to the expository article [6] for an overview of these approaches. This paper contributes to the literature on the worst-case approach. This approach is related to the view of Knight [32] that we should distinguish between “uncertainty” (am- biguous probabilities) and “risk” (precisely known probabilities), and model uncertainty, or more precisely, the investors’ assessment of model uncertainty, which cannot be represented by a probability prior. Its axiomatic foundation is laid out in [21, 15] which formally describe the max-min expected utility framework, in which an investor with ambiguity or uncertainty aversion would compute the expected utility by using the “worst” parameter set over the set of all possible parameters and chooses its strategy to maximize the worst-case expected utility. More generally, the worst-case approach explicitly incorporates a model of data un- certainty in the formulation of a portfolio selection problem, and optimizes for the worst-case scenario under this model; see, e.g., [11, 16, 14, 22, 20, 25, 29, 28, 35, 54, 47, 49]. The reader is referred to a recent survey [18] and monographs [17, 42, 48] on robust asset allocation. In this paper, we describe an extension of the asset allocation process, that takes into account model mis-specification and investor uncertainty aversion. We show that when the uncertainty model is convex, and the investor’s utility is quadratic, she separate her investment problem into two steps: Find the portfolio of risky assets that maximizes the worst-case SR (over all possible asset return statistics); then, decide on the mix of the risky portfolio and the risk-free asset, considering her risk aversion. The risky portfolio is the TP of the least favorable asset return statistics, with the portfolio weights chosen optimally. We will also show that the least favorable statistics (and the associated TP) can be found efficiently by solving a convex optimization problem. We give a review of the two-fund separation theorem in Section 2, to set up our notation and compare it to the extension we describe in Section 3. We illustrate the extension with

and the return volatility or risk, measured by the standard deviation, is

σ(x, Σ) = | 1 − θ|(wT^ Σw)^1 /^2 = (1 − θ)(wT^ Σw)^1 /^2

since we assume θ ≤ 1. For a portfolio of the form x = (w, 0), we use the shorthand notation

r(w, μ) = r(w, 0 , μ), σ(w, Σ) = σ(w, 0 , Σ).

As the leverage of the risky portfolio w is changed, the risk and return of the portfolio of x = ((1 − θ)x, θ) vary as

r((1 − θ)w, θ, μ) = (1 − θ)r(w, μ) + θμrf , σ((1 − θ)w, θ, Σ) = (1 − θ)σ(w, Σ),

which traces a line, parametrized by θ, in risk-return space. The choice of a portfolio involves a trade-off between risk and return [39]. The optimal trade-off achieved by admissible portfolios of risky assets a 1 ,... , an is described by the curve

fμ,Σ(σ) = sup w∈W, (wT^ Σw)^1 /^2 ≤σ

wT^ μ, (1)

which is called the (MV or Markowitz) efficient frontier (EF) for the risk assets. Each point on the EF corresponds to the risk and return of the portfolio that maximizes the mean return subject to achieving a maximum acceptable volatility level σ and satisfying the asset allocation and portfolio budget constraints. A basic property of the EF is that it is increasing and concave. When the risk-free asset is included, the optimal trade-off analysis becomes simpler. It suffices to find a single fund (portfolio) of risky assets; any MV efficient portfolio can then be constructed as a combination of the fund and the risk-free asset, as first observed by Tobin [53]. In this case, the EF is a straight line.

2.2 SR maximization and optimal capital allocation line

The reward-to-variability or Sharpe ratio [51, 52] of a portfolio x = ((1 − θ)w, θ), which is denoted as S(x, μ, Σ), is its excess return (relative to the risk free rate) divided by the standard deviation of its excess return:

S(x, μ, Σ) =

r(x, μ) − μrf σ(x, Σ)

For a portfolio (w, 0) of risky assets only, we use the shorthand notation

S(w, μ, Σ) = S(w, 0 , μ, Σ).

The SR of x is invariant to the leverage of the risky portfolio w: for θ < 1,

S((1 − θ)w, θ, μ, Σ) = S(w, μ, Σ) =

wT^ μ − μrf √ wT^ Σw

The problem of finding the portfolio of risky assets that maximizes the SR can be cast as maximize S(w, μ, Σ) subject to w ∈ W,

where the variable is w ∈ Rn^ and the problem data are μ and Σ. This problem is called the SR maximization problem (SRMP). With general convex asset allocation constraints, it can be reformulated as a convex optimization problem [22, 30, 54]. Its optimal value is called the market price of risk. We use Smp(μ, Σ) to denote the optimal value, as a function of the parameters μ and Σ: Smp(μ, Σ) = sup w∈W

S(w, μ, Σ).

As the fraction θ of the risk-free asset decreases from 1, the risk σ and the return r of x = ((1 − θ)w, θ) move along the line

r = μrf + S(w, μ, Σ)σ

in the (σ, r) space, which is called the capital allocation line (CAL) of w. The line

r = μrf + Smp(μ, Σ)σ (3)

is called the optimal CAL or capital market line (CML). When the SRMP has a solution w⋆, the optimal CAL is tangential to the efficient frontier at the point (σtan, rtan) where σtan and rtan are the risk and return of the portfolio w⋆. For this reason, the portfolio w⋆^ is called the tangency portfolio. Otherwise, the efficient frontier has an (upper) asymptote and the optimal CAL is parallel to the asymptote. Figure 1 illustrates this key result in modern portfolio theory.

2.3 Optimal allocation and two-fund separation

The following proposition follows from the observations made above.

Proposition 1 (Two-fund separation [53]). The CML is the optimal trade-off curve between risk and return for portfolios x ∈ X :

- The risk σ and the return r of any admissible portfolio x ∈ X cannot lie above the optimal CAL: r ≤ μrf + Smp(μ, Σ)σ. (4)

- If the SR is maximized by w⋆^ ∈ W, then for any θ ≤ 1 , the risk σ and the return r of x = ((1 − θ)w⋆, θ) lie on the optimal CAL:

r = μrf + Smp(μ, Σ)σ. (5)

The two-fund separation property allows us to find a closed-form solution for the EQUMP.

Proposition 2. The EQUMP (7) has a solution if and only if the SRMP (2) has a solution. If w⋆^ ∈ W solves the SRMP (2), then the portfolio x⋆^ = ((1 − θ⋆)w⋆, θ⋆) ∈ Rn+1, with

θ⋆^ = 1 −

γ

w⋆T^ μ − μrf w⋆T^ Σw⋆^

is the unique solution to (7).

Figure 1 illustrates the basic results in modern portfolio theory given above. The dotted curve is the optimal optimal indifference curve

r = U ⋆^ + (γ/2)σ^2 , U ⋆^ = sup x∈X

U (x, μ, Σ),

consisting of risk-return pairs which achieve the highest level of utility attainable subject to the asset allocation and budget constraints. The point at which the optimal indifference curve is tangential to the CML corresponds to the risk and return (σ(x⋆, Σ), r(x⋆, μ)) of the portfolio x⋆^ = ((1 − θ⋆)w⋆, θ⋆) that maximizes the expected quadratic utility.

3 Two-fund separation under model mis-specification

We now consider the case when the input parameters in the asset allocation model are not known, i.e., we take into account model mis-specification.

3.1 Risk and return under model mis-specification

We use U ⊆ Rn^ × Sn ++ to denote the set of possible input parameters. This set could represent, for example, the set of parameter values that are hard to distinguish from the baseline or nominal values, based on historical returns. Here Sn ++ denotes the set of all n × n symmetric positive definite matrices; Sn^ denotes the set of all n × n symmetric matrices. With model uncertainty, the risk and return profile of a portfolio x is described by a set in the risk-return plane. We use P(x) to denote the set of possible risk-return pairs of a portfolio x = ((1 − θ)w, θ), consistent with the uncertainty model U:

P(x) = {(r(x, μ), σ(x, Σ)) | (μ, Σ) ∈ U}.

As the leverage of the risky portfolio w is changed, the set P((1 − θ)w, θ) varies as

P((1 − θ)w, θ) = (1 − θ)P(w) + θ(0, μrf ), (9)

where we use the shorthand notation P(w) = P(w, 0), A + (u, v) means the translation of the set A by the vector (u, v), and αA means the scaling of A by α. As the risky portfolio is more leveraged, the risk and return set of x = ((1 − θ)w, θ) moves along a line, and grows proportionally. Figure 2 illustrates the dispersion effect due to the leverage.

risk σ

mean return

r

P(0, 1) = {(0, μrf )}

P(w, 0)

P(1. 5 w, − 0 .5)

P(0. 5 w, 0 .5) (^) worst-case CAL of w

Figure 2: Risk-return sets of portfolios with different leverages of a portfolio w of risky assets under model uncertainty.

3.2 Worst-case SR analysis and optimization

We introduce the counterparts of several definitions, such as the SR and CAL, in MV analysis under model mis-specification. We will then give a review of the minimax result for the SR proved in [30], along with a geometric interpretation. We make the following assumption:

inf (μ,Σ)∈U

w¯T^ μ > μrf. (10)

This assumption means that there exists an admissible portfolio ¯w ∈ W of risky assets whose worst-case mean excess return is positive.

Worst-case SR analysis

For a given portfolio x, the worst-case SR analysis problem can be formulated as

minimize S(x, μ, Σ) subject to (μ, Σ) ∈ U,

in which μ and Σ are the variables and x is fixed. Here, we compute the ‘worst’ (smallest) SR of the given portfolio when the mean return vector and covariance vary over the set U. The

These two problems lead us to define two robust counterparts of the optimal CAL (3). In the (σ, r) space, the line

r = μrf + sup w∈W

inf (μ,Σ)∈U

S(w, μ, Σ)σ (15)

is called the robust optimal CAL. The line

r = μrf + inf (μ,Σ)∈U

sup w∈W

S(w, μ, Σ)σ (16)

is the CML of the least favorable asset return statistics and called the least favorable CML. The minimax inequality or weak minimax property

sup (μ,Σ)∈U

inf w∈W

S(w, μ, Σ) ≤ inf (μ,Σ)∈U

sup w∈W

S(w, μ, Σ)

holds for any uncertainty set U. That is, the slope of the robust optimal CAL is no greater than that of the least favorable CML. As a consequence, when the inequality is strict, the portfolio that maximizes the worst-case SR is not the TP of any asset return statistics in U. The following proposition summarizes the minimax result for the zero-sum game men- tioned above.

Proposition 3 (Saddle-point property of the SR [30]). Suppose that the uncertainty set U is compact and convex, and the assumption (10) holds. Then, the SR satisfies the minimax equality sup w∈W

inf (μ,Σ)∈U

S(w, μ, Σ) = inf (μ,Σ)∈U

sup w∈W

S(w, μ, Σ). (17)

Moreover, if the least favorable pair (μ⋆, Σ⋆) has the tangency portfolio w⋆^ ∈ W, then the triple (w⋆, μ⋆, Σ⋆) satisfies the saddle-point property

S(w, μ⋆, Σ⋆) ≤ S(w⋆, μ⋆, Σ⋆) ≤ S(w⋆, μ, Σ), ∀ w ∈ W, ∀ (μ, Σ) ∈ U, (18)

and w⋆^ is the unique solution to the worst-case SRMP (13) although there may be multiple least favorable models.

This proposition tells us that when the uncertainty set U is convex, the two lines (15) and (16) coincide with each other. When the saddle-point property (18) holds, the slope of the robust optimal CAL can be written as

sup w∈W

inf (μ,Σ)∈U

S(w, μ, Σ) = inf (μ,Σ)∈U

sup w∈W

S(w, μ, Σ) = S(w⋆, μ⋆, Σ⋆) = Smp(μ⋆, Σ⋆).

With a convex uncertainty set U, the worst-case MPRAP (14) can be reformulated as the convex optimization problem

minimize (μ − μrf 1 + λ)T^ Σ−^1 (μ − μrf 1 + λ) subject to (μ, Σ) ∈ U, λ ∈ W⊕,

in which the optimization variables are μ ∈ Rn, Σ ∈ Sn, and λ ∈ Rn. Here W⊕^ is the positive conjugate cone of W,

W⊕^ = {λ ∈ Rn^ | λT^ w ≥ 0 , ∀w ∈ W}.

The details are given in [30]. Since convex problems are tractable, we conclude that there is a general tractable method for computing the saddle point (if it exists). The saddle-point property (18) for the SR has a geometric interpretation in the risk- return space. The risk-return set P(w⋆) of the portfolio w⋆^ lies on or above the robust optimal CAL, which in turn lies on or above the efficient frontier of the least favorable asset return statistics (μ⋆, Σ⋆):

r ≥ μrf + S(w⋆, μ⋆, Σ⋆)σ ≥ fμ⋆,Σ⋆^ (σ), ∀ (σ, r) ∈ P(w⋆).

The lower boundary of the set P(w⋆) and the efficient frontier of the least favorable asset return statistics (μ⋆, Σ⋆) meet at (σ⋆, r⋆) = (r(w⋆, μ⋆), σ(w⋆, Σ⋆)):

r⋆^ = μrf + S(w⋆, μ⋆, Σ⋆)σ⋆^ = fμ⋆,Σ⋆ (σ⋆).

We conclude that the robust optimal CAL (15) is the CML of the least favorable asset return statistics (μ⋆, Σ⋆) and is tangential to the efficient frontier fμ⋆,Σ⋆ at the point (σ⋆, r⋆). The robust optimal CAL is called the robust CML, and the portfolio that maximizes the worst-case SR is called the robust tangency portfolio. Figure 3 illustrates the geometric interpretation given above.

3.3 Robust optimal allocation and two-fund separation

We can observe from the definition of the robust optimal CAL that the set of possible risk- return pairs, consistent with the assumptions made on the model, of any admissible portfolio cannot lie entirely above the robust optimal CAL. The following proposition follows from the observation and (12).

Proposition 4 (Two-fund separation under model uncertainty). For any subset U of Rn^ × Sn ++, the line (15) is the worst-case efficient frontier in the following sense:

- The risk-return set P((1 − θ)w, θ) of any admissible portfolio ((1 − θ)w, θ) ∈ X cannot lie entirely above the robust optimal CAL, that is, there exists a point (σ, r) in P((1 − θ)w, θ) such that r ≤ μrf + sup w∈W

inf (μ,Σ)∈U

S(w, μ, Σ)σ.

- If the worst-case SRMP (13) has a solution w⋆, then for any θ < 1 , the risk-return set of the portfolio ((1 − θ)w⋆, θ) lies above or on the robust optimal CAL:

r ≥ μrf + sup w∈W

inf (μ,Σ)∈U

S(w, μ, Σ)σ, (σ, r) ∈ P((1 − θ)w⋆, θ).

The expected quadratic utility function is convex in (μ, Σ) over Rn^ × Sn ++ for fixed x, and concave in x for fixed (μ, Σ). It follows from the standard minimax theorem for convex/concave functions that when U is convex and compact, the minimax equality

sup x∈X

inf (μ,Σ)∈U

U (x, μ, Σ) = inf (μ,Σ)∈U

sup x∈X

U (x, μ, Σ)

holds. From a standard result in minimax theory, when the worst-case EQUMP (20) has a solution, say x⋆, it along with the solution (μ⋆, Σ⋆) to the worst-case MPRAP (14) satisfies the saddle-point property

U (x, μ⋆, Σ⋆) ≤ U (x⋆, μ⋆, Σ⋆) ≤ U (x⋆, μ, Σ), ∀ x ∈ X , ∀ (μ, Σ) ∈ U. (21)

The following proposition describes a closed-form solution to the worst-case EQUMP (20).

Proposition 5. Suppose that the uncertainty set U is convex and compact, and the as- sumption (10) holds. Then, the worst-case EQUMP (20) has a solution if and only if the worst-case SRMP (13) has a solution. If w⋆^ maximizes the worst-case SR, then the affine combination x⋆^ = ((1 − θ⋆)w⋆, θ⋆) of w⋆^ and the risk-free asset, with

θ⋆^ = 1 −

γ

w⋆T^ μ⋆^ − μrf w⋆T^ Σ⋆w⋆^

is the unique solution to (20).

The proof is deferred to Appendix A.3. This proposition tells us that due to her uncertainty aversion, the investor would hold a combination of the robust TP (when it exists) and the risk-free asset, regardless of her risk aversion. The fraction θ⋆^ is determined by her attitude toward risk (i.e., the constant γ) and the risk-variance ratio of the robust TP when the asset return statistics are least favorable. The saddle-point property (21) has a simple geometric interpretation in the risk-return space. The quadratic curve r − (γ/2)σ^2 = U ⋆, (23)

with U ⋆^ = U ((1 − θ⋆)w⋆, θ⋆, μ⋆, Σ⋆), is the optimal indifference curve when the asset return statistics are least favorable. We call this curve the robust optimal indifference curve. The saddle-point property means that the quadratic curve lies entirely above the robust CML except at the point (σ⋆, r⋆) = (σ(x⋆, Σ⋆), r(x⋆, μ⋆)):

μrf + Smp(μ⋆, Σ⋆)σ⋆^ =

γ 2

σ⋆^2 + U ⋆

and μrf + Smp(μ⋆, Σ⋆)σ <

γ 2

σ^2 + U ⋆, σ 6 = σ⋆.

It also follows that the risk-return set of the portfolio ((1 − θ⋆)w⋆, θ⋆) lies on or above the curve (23),

r −

γ 2

σ^2 ≥ U ⋆, ∀ (σ, r) ∈ P((1 − θ⋆)w⋆, θ⋆),

risk σ

return

r

(0, μrf )

robust optimal indifference curve

robust optimal CAL

least favorable EF

risk-return set of ((1 − θ⋆)w⋆, θ⋆)

Figure 4: Two-fund separation under under model mis-specification and worst-case expected quadratic utility maximization.

and the lower boundary of the risk-return set and the curve meet at (σ⋆, r⋆). Figure 4 illustrates the extension of the theorem given above. (With the singleton U = {(μ, Σ)}, it reduces to the illustration of the classical two-fund separation theorem in figure 1).) The shaded region is the risk-return set P((1 − θ⋆)w⋆, θ⋆) of the robust opti- mal portfolio ((1 − θ⋆)w⋆, θ⋆) that maximizes the worst-case expected quadratic utility. The dotted curve corresponds to the robust optimal indifference curve r = U ⋆^ + (γ/2)σ^2.

4 Numerical example

4.1 Setup and computation

We consider a synthetic example with 8 risky assets (n = 8) and

W = {w ∈ Rn^ | 1 T^ w = 1}.

The positive conjugate cone of W is

W⊕^ = {η 1 ∈ Rn^ | η ≥ 0 }.

The risk-free return is μrf = 4.

nominal SR worst-case SR nominal TP 0. 65 0. 11 robust TP 0. 58 0. 48

Table 1: The nominal and worst-case SR of the two portfolios: nominal and robust tangency portfolios.

4.2 Numerical results

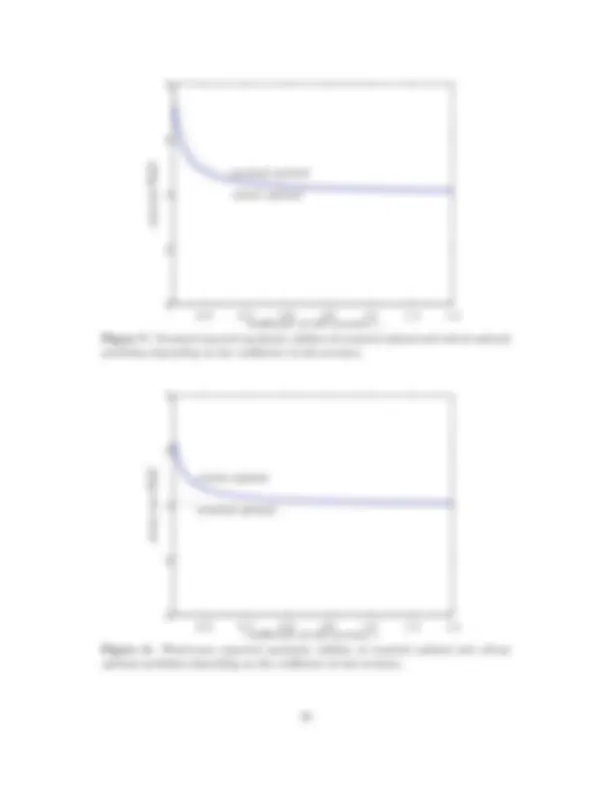

Table 1 shows the nominal and worst-case SR of the nominal optimal and robust optimal allocations. In comparison with the nominal optimal TP, the robust TP shows a relatively small decrease in the SR, in the presence of parameter variation. The SR of the robust TP decreases about 17% from 0.58 to 0.48, while the SR of the nominal TP decreases about 83% from 0.65 to 0.11. We see that the nominal performance of the robust TP is not too much worse to that of the nominal TP, but the robust TP is much more robust than the nominal TP to parameter variation. Figure 5 compares the weights of the nominal and robust TPs. The nominal TP has short positions in some assets, while the robust TP has long positions in all assets. This figure shows that the nominal TP has some relatively large weights, which is one reason it is sensitive to variations in the parameters. Figure 6 shows how the leverage of the risky portfolio varies as the constant γ varies. This proposition shows that uncertainty aversion reduces demand for the risky asset, which is in line with the result in [38]. Figure 7 compares the nominal expected quadratic utility, computed with the baseline model, achieved by the nominal optimal and robust optimal portfolios as γ varies. Since the nominal TP maximizes the SR for the baseline model, the combination of the robust TP and the risk-free asset cannot outperforms the combination of the nominal TP and the risk-free asset. Figure 8 compares the worst-case expected quadratic utility (EQU) achieved by the nominal optimal and robust optimal portfolios as γ varies. Since the robust TP maximizes the worst-case SR, the combination of the robust TP and the risk-free asset should outperforms the combination of the nominal TP and the risk-free asset, which is confirmed by this figure. The gap is especially large when the risk aversion constant γ is small. We can see a significant improvement brought about by the robust combination. Of course, the latter is less efficient than the nominal portfolio with the baseline model. Model uncertainty makes the nominal TP a poor choice over the robust TP.

asset

weight

wntp

wrtp

1 2 3 4 5 6 7 8

-0.

-0.

-0.

-0.

0

Figure 5: Weights of assets in nominal tangency portfolio and robust tangency port- folio.

coefficient of risk aversion γ

fraction of the risk-free asset

nominal TP

robust TP

0.2 0.4 0.6 0.8 1.0 1.2 1.

-0.

0

1

Figure 6: Fraction of the risk-free asset in the nominal optimal and robust optimal portfolios, depending on the coefficient of risk aversion.

5 Conclusions

In this paper, we have described an extension of the two-fund separation theorem to MV analysis under model mis-specification. The extension tells us that when the uncertainty model is convex, an investor with quadratic utility and uncertain aversion would hold a combination of the risk-free asset and the risky portfolio which is the tangency portfolio of the least favorable asset return statistics in terms of the market price of risk. The fraction is determined by her attitude toward risk, and the risky portfolio can be found efficiently using convex optimization. The two-fund separation property holds for other several standard utility maximization problems than quadratic utility functions, when the asset returns are jointly normal; the reader is referred to [10, 2] for more on utility maximization problems compatible with the two-fund separation property. The two-fund separation property can be extended to certain types of worst-case utility maximization problems including exponential utility functions, when the asset returns are jointly normal. An exponential utility function has the form

U (c) = −e−λc,

where λ is the coefficient of absolute risk aversion. When the asset returns are jointly normal, the expected exponential utility of a portfolio x is

EU (xT^ a) = − exp

−(E(xT^ a) − (λ^2 /2)V(xT^ a))

which is an increasing function of the expected quadratic utility. Therefore, worst-case ex- pected exponential utility maximization is the same as worst-case quadratic utility maximiza- tion with γ = λ^2 , so the two-fund separation property readily extends. It is an interesting topic to clarify the class of worst-case utility maximization problems which exhibit the robust two-fund separation property. The two-fund separation property has also been extended to dynamic and other settings; see, e.g., [41, 46] to name a few. It is also an interesting topic to extend the two-fund separation property to other settings while taking into account model mis-specification and uncertainty aversion. The two-fund separation property has an important implication for equilibrium prices of assets, which is known as the CAPM. The extension of the two-fund separation theorem tells us that as long as investors with uncertainty aversion and quadratic utility have the same uncertainty model, they would hold a combination of the same portfolio of risky assets and the risk-free asset, regardless of their risk tolerance. An implication for equilibrium prices of assets is that under the standing assumptions of the CAPM and the additional assumption that all investors share the same convex uncertainty model, the robust TP that maximizes the worst-case SR is the market portfolio. An immediate observation we can make is that the market portfolio is not necessarily MV efficient when the true model is not least favorable. An interesting topic is to examine the implications of this observation in terms of uncertainty premium and build an asset pricing model which takes into account not only risk premium but also uncertainty premium. Related work in this direction includes [12, 33], which argue that equity premium can be decomposed into two components, risk premium and uncertainty premium.

Acknowledgments

This material is based upon work supported by the Focus Center Research Program Center for Circuit & System Solutions award 2003-CT-888, by JPL award I291856, by the Precourt Institute on Energy Efficiency, by Army award W911NF-07-1-0029, by NSF award ECS- 0423905, by NSF award 0529426, by DARPA award N66001-06-C-2021, by NASA award NNX07AEIIA, by AFOSR award FA9550-06-1-0514, and by AFOSR award FA9550-06-1-

References

[1] V. Bawa, S. Brown, and R. Klein. Estimation Risk and Optimal Portfolio Choice, volume 3 of Studies in Bayesian Econometrics Bell Laboratories Series. Elsevier, New York: North Holland, 1979.

[2] J. Berk. Necessary conditions for the CAPM. Journal of Economic Theory, 73(1):245– 257, 1997.

[3] M. Best and P. Grauer. On the sensitivity of mean-variance-efficient portfolios to changes in asset means: Some analytical and computational results. Review of Fi- nancial Studies, 4(2):315–342, 1991.

[4] F. Black and R. Litterman. Global portfolio optimization. Financial Analysts Journal, 48(5):28–43, 1992.

[5] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

[6] M. Brandt. Portfolio choice problems. In Y. Ait-Sahalia and L. Hansen, editors, Hand- book of Financial Econometrics. North-Holland, 2005.

[7] M. Britten-Jones. The sampling error in estimates of mean-variance efficient portfolio weights. Journal of Finance, 54(2):655–671, 1999.

[8] M. Broadie. Computing efficient frontiers using estimated parameters. Annals of Op- erations Research, 45:21–58, 1993.

[9] S. Brown. The effect of estimation risk on capital market equilibrium. Journal of Financial and Quantitative Analysis, 14(2):215–220, 1979.

[10] D. Cass and J. Stiglitz. The structure of investor preferences and asset returns, and separability in portfolio allocation: A contribution to the pure theory of mutual funds. Journal of Economic Theory, 2(2):122–160, 1970.

[11] S. Ceria and R. Stubbs. Incorporating estimation errors into portfolio selection: Robust portfolio construction. Journal of Asset Management, 7(2):109–127, 2006.