Download Understanding Production Order Variance.docx and more Study Guides, Projects, Research Law in PDF only on Docsity!

Understanding Production Order Variance - Part 2 The SAP Perspective Author: Ranjit Simon John Every PP, FI and CO user in any Manufacturing Industry will be facing a tough time during period-end processing every month. Production Order Variance posted against each process orders will have to be examined, explained & investigated thoroughly. Major questions arising will be; From Where the Variance has come How to Categorize the variance How to cut down the variance. Impact of variance on COGM, COGS & Closing Stock, has to be answered to the management. We have faced all these scenarios and after months of deep research in this field I came across few conclusions. For better understanding I will divide this blog into two categories; Category A: Basic understanding of Production Order Category B: Co-relating Category A scenarios with real life scenarios. Now let us examine the main points under Category A: The ultimate end point of any industry is sales. For selling the product several process has to be carried out. The success of any management depends on how well they forecast the sales, plan and schedules the activities.

Figure 1. Let us divide the process as given below;

- Initial Planning

- Cost Estimates

- Actual Posting

- Period – End Processing

- Initial Planning: Forecasting the sales for future. Sales and Operation Planning, Long term planning, Cost center planning should be well executed by the management.

- Cost Estimates: The major points to be considered here are; a) a) Master Data: a.1) Material Master: All the required information to manage a material. Transaction Codes: MM01, MM02, MM a.2) Bill of Material (BOM): Structured hierarchy of raw materials necessary to create a Finished / Semi Finished Good. Transaction Codes: CS01, CS02, CS a.3) Routing: List of tasks containing standard activity times required to perform operations to create a Finished / Semi Finished Good. Transaction Codes: CA01, CA02, CA a.4) Product Cost Collector: Collects actual costs during the production of a material. Transaction Codes: KKF6N a.5) Recipe: Recipes comprise information about the products and components of a process, the process steps to be executed, and the resources required for the production.

Postings to CO from external business transactions results in Primary Costs. Business transactions within CO results in Secondary Costs. 3.1 Primary Cost: Primary cost will be posted to CO mainly in the following scenarios: 3.1.1 Goods Issue to Production Order: When goods are issued from inventory, a general ledger balance sheet account is credited, and profit and loss consumption (expense) account is debited. A primary cost element with the same number and identifier as the inventory consumption is usually created in CO during initial system implementation. When the system detects a corresponding primary cost element in CO during a posting to General ledger expense account, a posting to CO cost object is also required. Primary Cost are posted to CO from FI. GL entry during Goods Issue

Debit Credit Raw Material Consumption XXX Stock of Raw Material XXX Table 1. 3.2 Secondary Cost: The costs in CO are allocated from overhead cost centers to production cost centers during assessment and then onto production order during activity confirmation. 3.2.1 Assessment Period-end assessments move costs from overhead cost centers to production cost centers. 3.2.2 Activity Confirmation: When production order activities are confirmed, the production or product cost collector is debited, and the production cost center is credited. There are no FI postings during activity confirmation. 3.3 Primary Credits Primary Credits occur when production orders deliver Finished / Semi finished good into inventory. As finished goods are delivered from manufacturing order into inventory, an inventory balance sheet account is debited, and profit and loss production output account is credited. Because there is a primary cost element corresponding to the production output account, a CO object is also credited. The finished goods are delivered from a production order, so the system automatically chooses the production order or product cost collector to receive the primary credit.

The credit value is calculated by multiplying the finished goods standard price by the quantity delivered to inventory.

Debit Credit Stock of Finished Good XXX COGM of Finished Good XXX Raw Material Consumption XXX Stock of Raw Material XXX Table 2. 3.4 Secondary Credit At period end the production order receives a secondary credit that is equal to the variance during settlement, resulting in zero balance. During the settlement process, product cost collectors and process order variance are posted to Profitability Analysis (CO-PA) and FI.

Debit 100 Raw Material 100 Labor 100 Over Heads Credit (250) Finished Good Balance 50 Variance Table 3. Total Variance is the difference between total production order debits and credits. Variance calculation at period end divides the variance into categories, based on the source of the variance. Production Variance settled to CO-PA are included at the gross profit margin level. Cost Center under/over absorption costs assessed to CO-PA are included at the operating profit level. 3.5) Post Actual Costs

- Period – End Processing 5.1 The three common types of variance calculation are as follows; 5.1.1) Total Variance Total variance is the difference between the actual cost debited to the order and credits from deliveries to inventory. Total Variance is variance relevant to settlement. The variance is settled in Financial Accounting (FI), Profit Center Accounting and Profitability Analysis 5.1.2) Production Variance

Input quantity variance occurs as a result of a difference between plan and actual quantities of materials and activities consumed. Input quantity variance = (actual input quantity – target input quantity) * plan price Category IV.4) Remaining Input Variance When input variance cannot be assigned to any other variance category. 5.2.2) Output Variance Variance can be from too little or too much of planned order quantity being delivered, or because the delivered quantity was valuated differently. 5.2.2) Output Variance is divided into; Category OV.1) Mixed – Price Variance Mixed-Price variance occurs when inventory is valuated using a mixed cost estimate for the material. Category OV.2) Output Price Variance Output price variance can occur in the following scenarios;

- If the standard price is changed after delivery to inventory, and before variance calculation.

- If the material is valuated at moving average price and it is not delivered to inventory at standard price during target value calculation. Output price variance = actual activity * (plan price – actual price) Category OV.3) Lot Size Variance Lot Size variance occurs if a manufacturing order lot size is different from the standard cost estimate costing lot size. Category OV.4) Remaining Variance Occurs if variance cannot be assigned to any other variance category. Category OV.5) Output Quantity Variance Represents the difference between manually entered actual costs and allocated actual quantities. Output Quantity variance = ( actual quantity –manual actual quantity) * plan price 5.3) Period End The most important period-end process relevant to production order variance analysis is; Overhead WIP

Variance Calculation Variance can be calculated using the formula; Variance = Actual Cost – Actual Cost Allocated (credits) – WIP – Scrap During variance calculation, target and control costs are compared, and variance categories are assigned. Variance categories are assigned in the following sequence: Input price variance Resource – usage variance Input quantity variance Remaining input variance Mixed –price variance Output price variance Lot Size Variance Remaining Variance Settlement : Settlement of Production Orders will be executed. KO88 - Individual Settlement CO88 - Collective Settlement Now let us examine the main points under Category B: Now you will be having a basic idea about production order variance , variance calculation types & various categories. Now let us try to co-relate this with real life scenarios. I will divide the topic into below mentioned sections;

- How to analyze production order variance posted against production orders

- Major Reasons for the variance

- How to minimize the variance

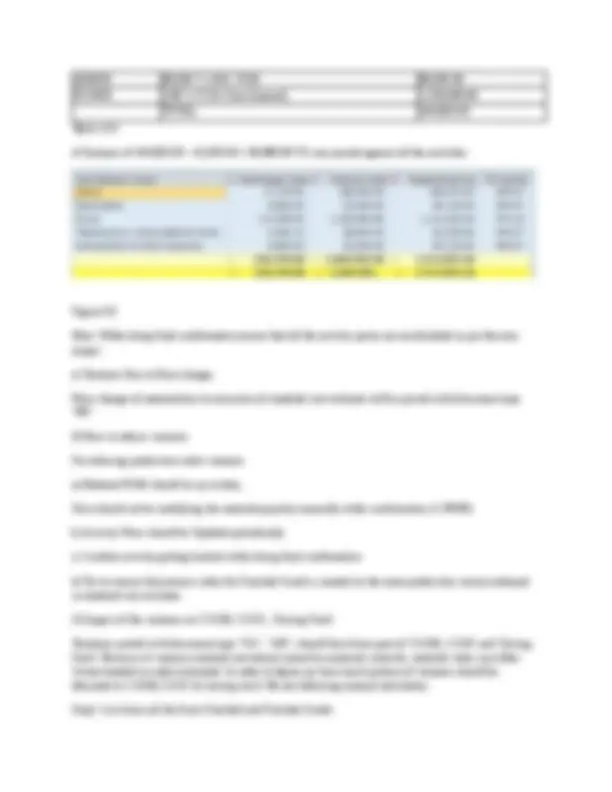

- Impact of production order variance on COGM, COGS & Closing Stock Category B.1) How to analyze variance posted against production order For explaining the scenarios I am taking one Semi Finished Good (SFG1– Semi Finished Good 1) which is used as a raw material for production of Finished Good.

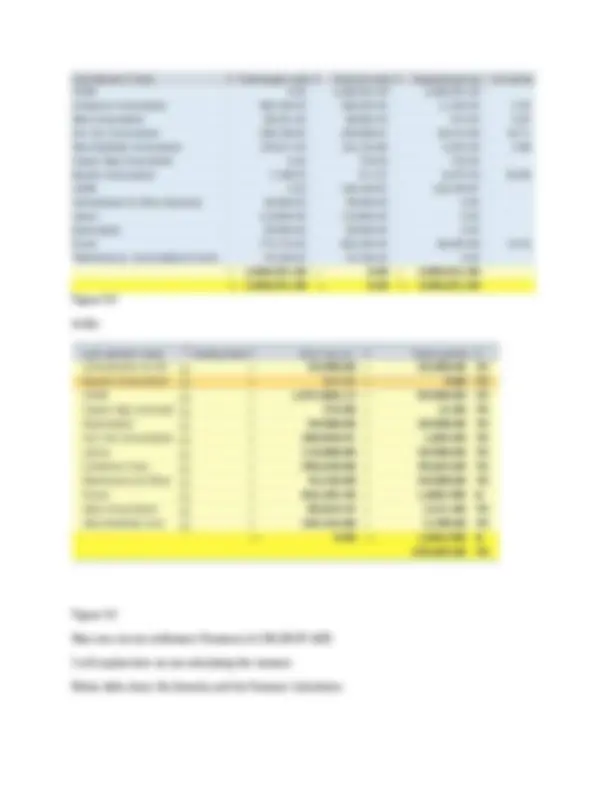

Figure 3. KOB

Figure 4. Here you can see settlement (Variance) of 128,190.87 AED. I will explain how we are calculating the variance. Below table shows the formula used for Variance Calculation.

All the Std. Rate, Std. Qty, Std. Cost value fields in Table 4.0 are calculated based on the master details (Material Recipe Figure 2.0). All the Actual Rate, Actual Qty. Actual Cost vale fields in table 4.0 are extracted from KOB1.

Cost Elements Std. Rate (Figure 2.0)

Std. Qty. (Figure 2.0)

Std. Cost Actual Rate

Actual Qty. (Figure 4.0)

Actual Cost (Figure 4.0)

Variance

RAWMATERI

AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

49,663.00 496,630.00 Std Cost - Act Cost RAWMATERI AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

3,411.00 89,824.45 Std Cost - Act Cost RAWMATERI AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

5,798.00 104,162.8 Std Cost - Act Cost RAWMATERI AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

1,003.00 209,858.91 Std Cost - Act Cost RAWMATERI AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

9.00 517.57 Std Cost - Act Cost RAWMATERI AL

Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

21.00 735.00 Std Cost - Act Cost Labor Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

59,900.00 119,800.00 Std Cost - Act Cost Depriciation Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

59,900.00 59,900.00 Std Cost - Act Cost Administration Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

59,900.00 59,900.00 Std Cost - Act Cost MACOOH Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

59,900.00 44,326.00 Std Cost - Act Cost POWER Total value / Qty

Per Ton Qty

Std Qty

Act Cost / Act Qty

1,609,780.00 692,205.4 Std Cost - Act Cost FINISHED GOOD

Let us try to calculate Variance by applying Formula for each category. Category IV.1: Input Price Variance = (Actual Price – Plan Price) * Actual Input Quantity Category IV.2: Resource Usage Variance – Actual Cost – Target Cost – Input Price Variance Category IV.3: Input Quantity Variance = (Actual Input Quantity – Target Input Quantity) * Plan Price

Cost Elements Plan Price

Target Input Qty

Target Cost

Actual Price

Actual Input Qty

Actual Cost

Varianc e Class

Variance RAWMATERI AL

C1 11,440.

RAWMATERI

AL

24.4262 3,653.90 89,251.00 26.3338 3,411.00 80,824.45 C2 573.

RAWMATERI

AL

C2 (5,454.25)

RAWMATERI

AL

C2 (48,310.09)

RAWMATERI

AL

60.00 119.80 7,188.00 57.5078 9.00 517.57 C2 (6,670.43)

RAWMATERI

AL

0.00 0.00 0.00 35.00 21.00 735.00 C3 735.

Power 0.43 1,797,000. 0

692,205.4 C1 (80,504.6)

TOTAL (128,190.27)

Table 7. Category B.2) Major Reasons for the variance From My experience I can point out that Production order variance occur mainly from; a) Material BOM not updated properly (Category IV.3) b) Material Price Change after release of Standard Cost Estimate (Category IV.1) c) Activity Price (Material Recipe) not updated properly (Category IV.2) d) Standard Cost estimate released for one production version and confirmation done against another production order. (Category OV.3) e) Total Planned Quantity and Actual Produced Quantity Difference (Category IV.4) f) Material used not included in BOM ((Category IV.2) Let us try to analyze all the scenarios. a) Material BOM not updated properly

Explained in Category B. b) Activity Price (Material Recipe) not updated properly Explained in Category B. Total POWER consumption as per KOB1 (Actual as per Material Recipe) and FBL3N should be approximately equal. KOB1 -> POWER consumption for the Materials Produced FBL3N -> Actual POWER receipt report (Receipt = Consumption) c) Standard Cost estimate released for one production version and confirmation done against another production order. Costing run executed for one Production Version and Process Order created against another production version. Let us take one example where two production versions are present Production Version 1 and Production Version 2 for Finished Good FG1. Production Version 1 will be using RM1 as raw material and production version 2 will be using RM2 as raw material. Standard cost estimate is released against Production version 1. Let me explain with an example; As per Released Standard Cost Estimate Material recipe / Ton of FG

Production Version Resource Total Value Quantity PO31 GCPRODCGM1 P031 POWER 15.05 0. PO31 GCPRODCGM1 P031 ADMINI 0.50 1. PO31 GCPRODCGM1 P031 DEPRN 1.00 1. PO31 GCPRODCGM1 P031 LABOUR 0.70 1. PO31 GCPRODCGM1 P031 MACOOH 1.19 1. GC01 RM1 149.54 0. GC01 RM3 4.47 0. TOTAL 172. Table 8. Process Order has been Created Under production version “PO32” The Activity Price recorded in system against “PO32” is as follows

Production Version Resource Total Value Quantity PO32 GCPRODCGM2 P032 POWER 17.00 0.

Product : FG Standard Cost Estimate Released for Production Version "PO31" Table 11. Material Recipee for FG1 (CK13N)

Production Version Resource Total Value Fixed Value Quantity PO31 POWER 15.05 15.05 0. PO31 ADMINI 0.50 0.00 1. PO31 DEPRIN 1.00 0.00 1. PO31 LABOUR 0.70 0.00 1. PO31 MACOOH 1.19 0.00 1. RM1 149.54 32.69 0. RM3 4.47 0.00 0. TOTAL 172.45 47. Figur 5. Process Order is Created under production Version "PO32" When a Process order is created for Material FG1 system calculates Planned cost as follows; Quantity Produced -> 25,302.00 TO Use the same calculation logic used in Table 1.0;

Resource Quantity Amount RM1 23,910.39 3,783,661. RM3 13,916.10 1,130,999. ADMIN 25,302.00 12,651. LABOR 25,302.00 17,711. DEPRIN 25,302.00 25,302. MACOOH 25,302.00 30,109. POWER 885,570.00 380,795. Table 12. Planned Cost for Producing 25,302.00 TO of FG

Figure 6.

Process Order has been created in Production version "PO32". During Confirmation System calculates actual cost as follows;

Figure 7. d) Total Planned Quantity and Actual Produced Quantity Difference We came across this production order variance in few process orders only. While doing final confirmation of process orders user made mistake by not allowing system to re calculate the activity prices. Material: FG Total Process Order Quantity: 93,000 TO Quantity Produced: 8,865.00 TO The total quantity produced is 8,865.00 TO against which the activities booked are;

Activity Quantity Amount LABOR 8,865 * 2 DH / TON 17,730. DEPRIN 8,865 * 1 DH / TON 8,865. MACOOH 8,865 * 0.74 DH / TON 6,560. ADMIN 8,865 * 1 DH / TON 8,865. POWER 8,865 * 0.03 * 1000 265,950. TOTAL 42,020. Table 13. Since during final confirmation of the Order, re calculation of activities were bypassed (by user) system calculated the activities against the production order as below;

Activity Quantity Amount LABOR 93,000 * 2 DH / TON 186,000. DEPRIN 93,000 * 1 DH / TON 93,000. MACOOH 93,000 * 0.74 DH / TON 68,820.

Step 2: Record total variance posted against each material (FBL3N) (Document type "SA" & "AB") Step 3: Record total quantity produced (MB5B with movement types 101 & 102) Step4: Variance Per Ton = Step3 / Step 2 Step5: Record closing stock of Material (MB5B) Step6: Closing Stock Variance Allocation = Step5 * Step Step7: Record COGM Quantity (MB5B with movement type 201 + 202 & 261 + 262) Step8: COGM Variance Allocation = Step7 * Step Step9: Record COGS Quantity (MB5B with movement type 601 + 602) Step10: COGS Variance Allocation = Step9 * Step

Material Varianc e Step 2

Production Qty Step 3

Variance / Ton Step 4

Closing Stock Qty Step 5

Closing Stock Variance Step 6

COGM

Variance Step 8

COGS

Qty Step 9

COGS

Variance Step 10 MATERIA L

V1 P1 VT1 =

P1 / V

C1 C1 * VT1 COGM Qty

S1 S1 * VT

MATERIA

L

V2 P2 VT2 =

P2 / V

C2 C2 * VT2 COGM Qty

S2 S2 * VT

MATERIA

L

V3 P3 VT3 =

P3 / V

C3 C3 * VT3 COGM Qty

S3 S3 * VT

Table 15. Few Important Document Types Posted in Production Order Variance GL are; AB -> Reversal of Production Order Settlement SA -> Production Order Settlement PR -> Price Change WA -> Confirmation Reversal (If Price Changed after Confirmation) WL -> Sales Reversal (If Price Changed after Sales)

Figure 10. Few Important Transaction Codes KKBC_ORD KOB KOC FBL3N CK13N CK11N CK MB5B MB Reference: Production Variance Analysis in SAP Controlling By John Jordan, Published by SAP Galileo PresAlso refer s

Understanding Production Order Variance - Part 3 Price

Difference Variance

Author: Ranjit Simon John

In my blog "resaons for varinace in production order. In this blog let us see in detail the price difference variacne posted during Understanding Production Order Variance - Part 2 The SAP Perspective " I have mentioned the main order settlement. Input Price Variance: