Download Using a General Journal for Accounting Transactions: A Step-by-Step Guide and more Schemes and Mind Maps Business Administration in PDF only on Docsity!

Using a Journal

By Laurie L. Swanson

Principles of Accounting

HelpLesson

Use this presentation

to help you

learn about using the

General Journal.

Using A Journal

Recording a Transaction

In the previous tutorial, you learned to

analyze and record transactions on the

Transaction Analysis Sheet. This tool was

used to help you learn to analyze transactions

and is not actually used by accountants when

recording transactions.

Business transactions are recorded in a book

known as a journal.

Definitions

A General Journal is a book used to record a

company’s day-to-day business transactions.

The process of recording information in a

journal is called journalizing.

Using The General Journal

When recording transactions in a journal, first

analyze the transaction using the same steps you

have learned in the Analyzing Transactions and

Debits and Credits tutorials.

1. What accounts are involved in the transaction?

2. What is the classification of each account?

3. What is happening to each account—is it

increasing or decreasing?

4. How is this accomplished—with a debit or credit?

Using The General Journal

Next, record the transaction in the journal

as shown in the following slides. We will

use a transaction used in the previous

tutorial.

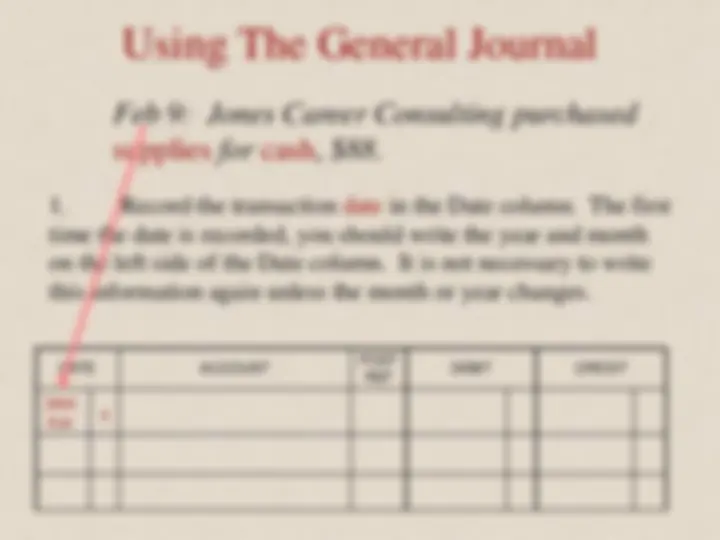

Using The General Journal

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

9

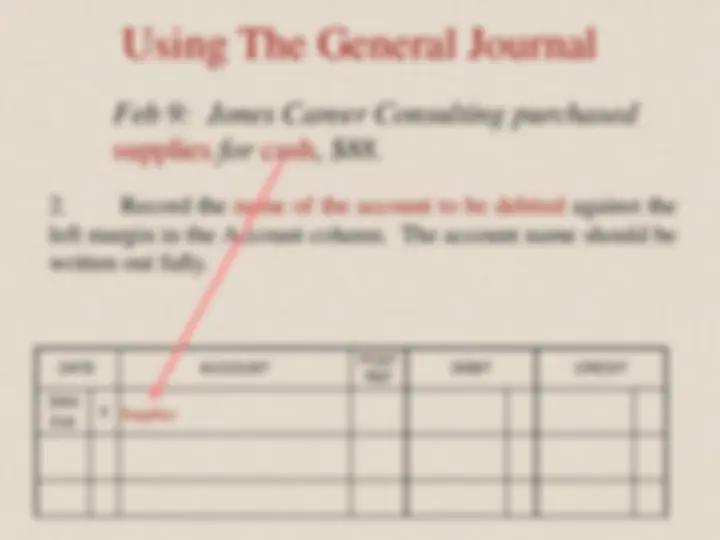

Feb 9: Jones Career Consulting purchased

supplies for cash, $.

2. Record the name of the account to be debited against the

left margin in the Account column. The account name should be

written out fully.

Supplies

Using The General Journal

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

9 Cash

Feb 9: Jones Career Consulting purchased

supplies for cash, $.

3. Record amount debited in the Debit column on the same

line as the account title for the debited account. Do not place a

dollar sign beside the amount.

88 00

Using The General Journal

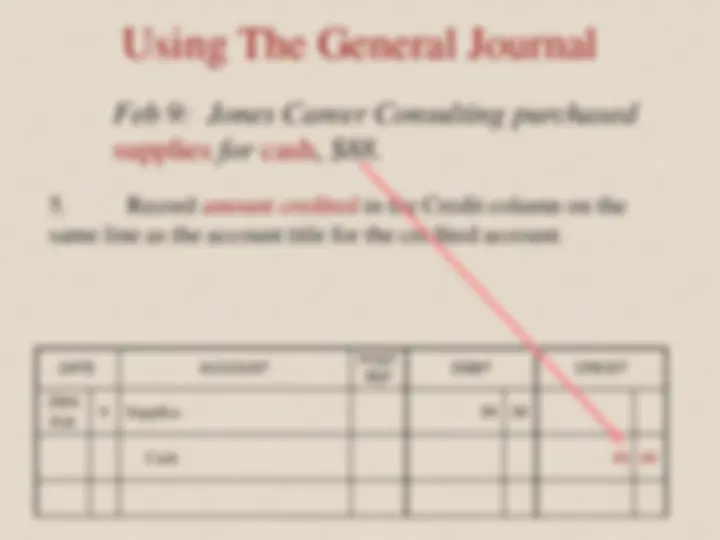

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

9 Supplies 88 00

Cash

Feb 9: Jones Career Consulting purchased

supplies for cash, $.

5. Record amount credited in the Credit column on the

same line as the account title for the credited account.

88 00

Using The General Journal

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

9 Supplies 88 00

Cash 88 00

Feb 9: Jones Career Consulting purchased

supplies for cash, $.

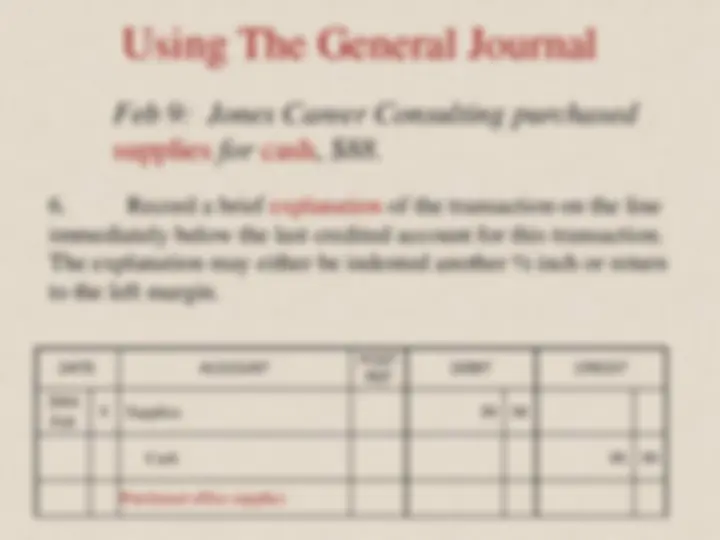

6. Record a brief explanation of the transaction on the line

immediately below the last credited account for this transaction.

The explanation may either be indented another ½ inch or return

to the left margin.

Purchased office supplies

Journal Formatting Rules

1. Do not include dollar signs, commas or decimal points for amounts in the journal.

2. Write the year, month, and date for the first transaction at the top of the journal in the

Date column. For all following transactions write only the date unless it is a new month

or year.

3. Spell out account names fully —do not use Sal Exp; write out Salaries Expense.

4. Refer to the Chart of Accounts so that you are using accurate account titles for each

company.

5. For each transaction, enter the debit ed account first with the title flush against the left

margin of the explanation (or account) column.

6. Enter the credit ed account title on the following line indented about ½ inch.

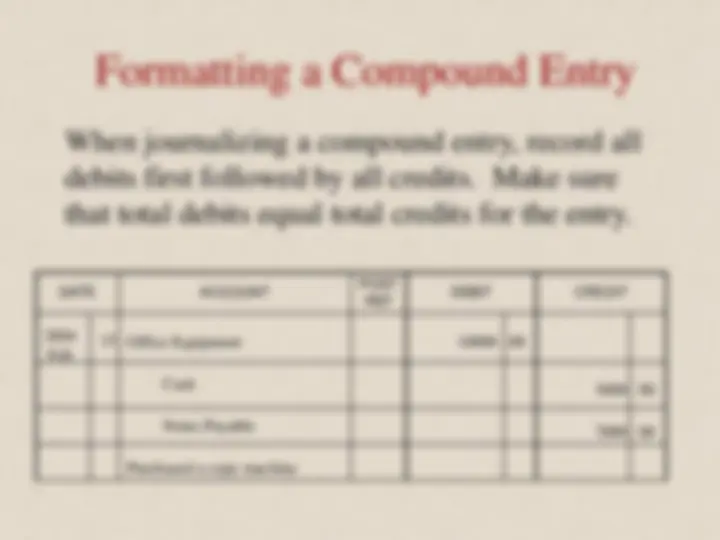

7. For compound entries, keep all debited accounts together followed by all credited

accounts.

8. Keep all credited accounts throughout the journal in line with the imaginary ½ inch

margin.

9. Follow the credited account with an explanation of the transactions. It is acceptable to

return this description to the left margin or indent it another ½ inch from the credited

account title.

10. Skip a line between transactions.

11. Keep entire transactions on the same page together. Start a new page if necessary.

12. Never total a journal.

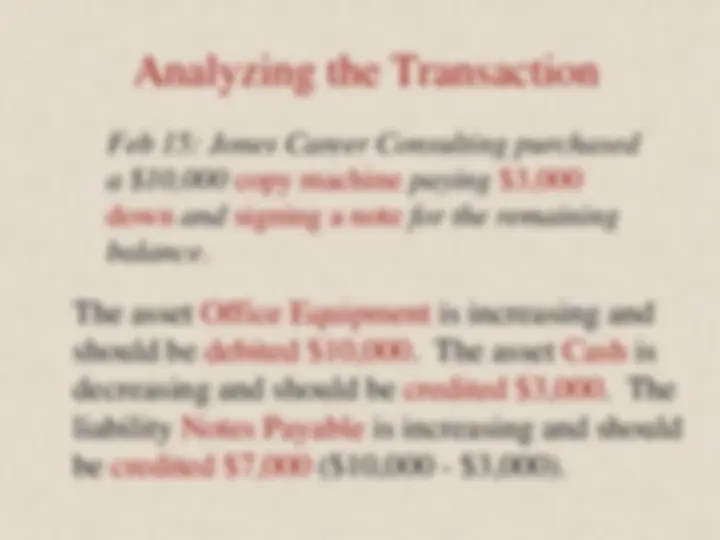

Journalize Another Transaction

Feb 12: Jones Career Consulting paid a creditor

on account, $.

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

9 Supplies 88 00

Cash 88 00

Skip a line between transactions.Enter the credited account title.Enter the debited account title.Enter the a brief explanation.Enter the credited amount.Enter the transaction date.Enter the debited amount.

12 Accounts Payable 350 00

Cash 350 00

Paid ABC Company

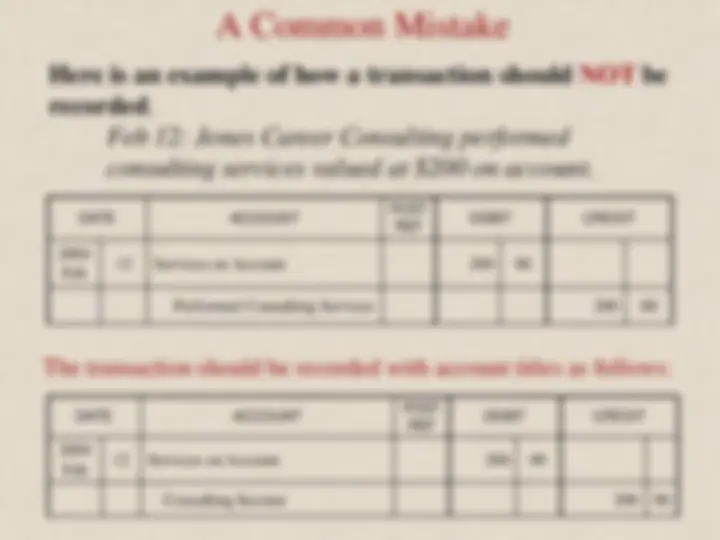

A Common Mistake

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb

12 Services on Account 200 00

Consulting Income 200 00

Here is an example of how a transaction should NOT be

recorded.

Feb 12: Jones Career Consulting performed

consulting services valued at $200 on account.

DATE ACCOUNT POST REF DEBIT CREDIT

2004 Feb 12 Services on Account^200

Performed Consulting Services 200 00

The transaction should be recorded with account titles as follows:

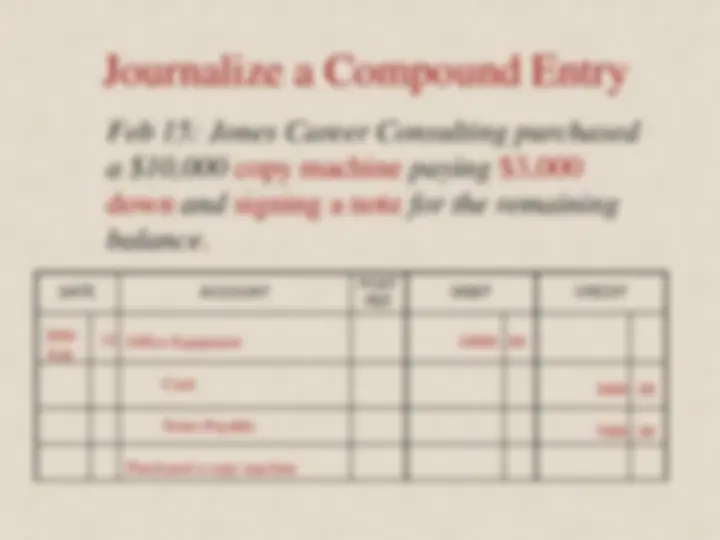

Compound Entry

A compound entry is a journal entry

with more than one debit or more than

one credit.