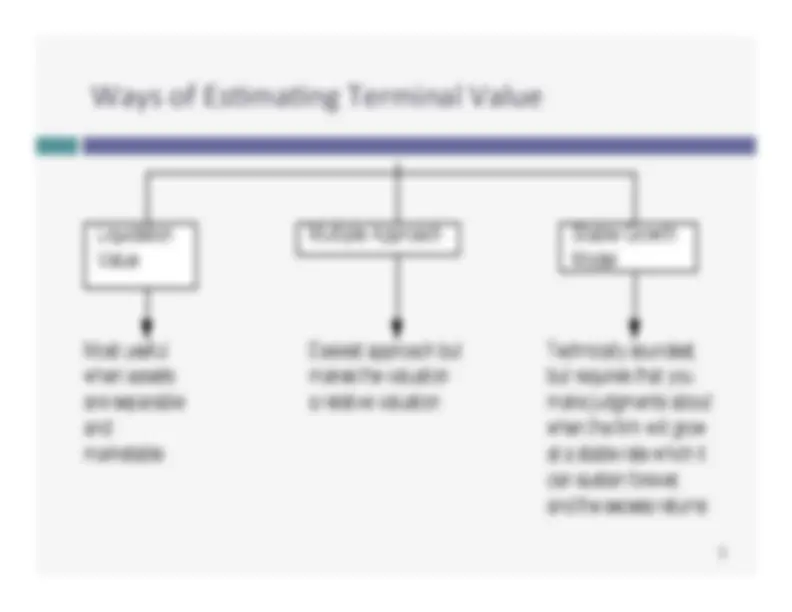

VALUATION:*TERMINAL*VALUE*

The*tail*that*wags*the*valua9on*dog..*

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

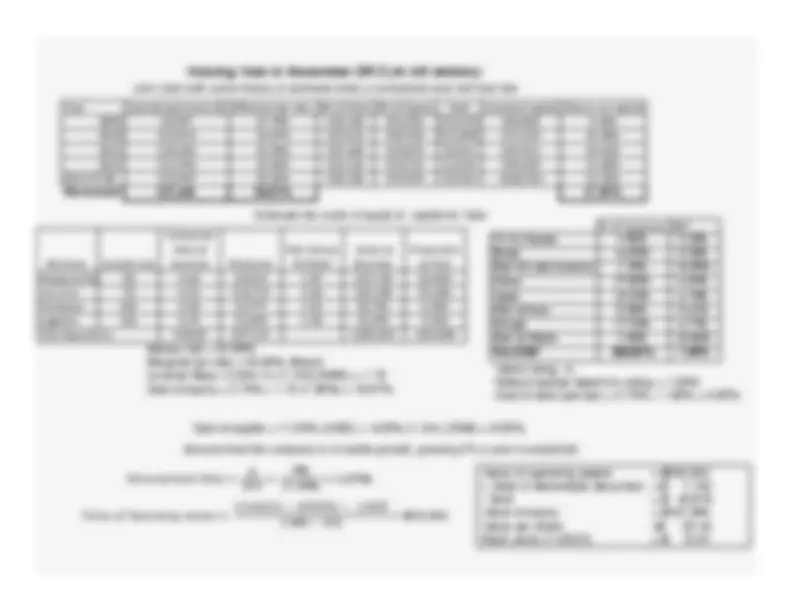

When a firm's cash flows grow at a “constant” rate forever, the present value of those cash flows can be wriWen as: Value = Expected Cash Flow Next Period ...

Typology: Schemes and Mind Maps

1 / 16

This page cannot be seen from the preview

Don't miss anything!

3

Ge?ng Terminal Value Right

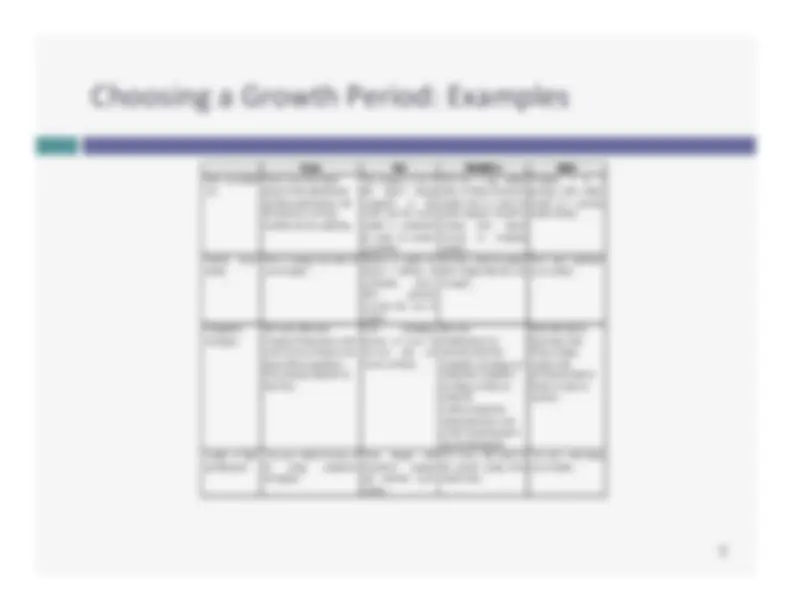

And the key determinant of growth periods is the company’s compe99ve advantage… ¨ Recapping a key lesson about growth, it is not growth per se that creates value but growth with excess returns. For growth firms to con9nue to generate value crea9ng growth, they have to be able to keep the compe99on at bay. ¨ Proposi9on 1: The stronger and more sustainable the compe99ve advantages, the longer a growth company can sustain “value crea9ng” growth. ¨ Proposi9on 2: Growth companies with strong and sustainable compe99ve advantages are rare.

Disney Vale Tata Motors Baidu Firm size/market size Firm is one of the largest players in the entertainment and theme park business, but the businesses are being redefined and are expanding. The company is one of the largest mining companies in the world, and the overall market is constrained by limits on resource availability. Firm has a large market share of Indian (domestic) market, but it is small by global standards. Growth is coming from Jaguar division in emerging markets. Company is in a growing sector (online search) in a growing market (China). Current excess returns Firm is earning more than its cost of capital. Returns on capital are largely a function of commodity prices. Have generally exceeded the cost of capital. Firm has a return on capital that is higher than the cost of capital. Firm earns significant excess returns. Competitive advantages Has some of the most recognized brand names in the world. Its movie business now houses Marvel superheros, Pixar animated characters & Star Wars. Cost advantages because of access to low-cost iron ore reserves in Brazil. Has wide distribution/service network in India but competitive advantages are fading there.Competitive advantages in India are fading but Landrover/Jaguar has strong brand name value, giving Tata pricing power and growth potential. Early entry into & knowledge of the Chinese market, coupled with government-imposed barriers to entry on outsiders. Length of high- growth period Ten years, entirely because of its strong competitive advantages/ None, though with normalized earnings and moderate excess returns. Five years, with much of the growth coming from outside India. Ten years, with strong excess returns.

Don’t forget that growth has to be earned..

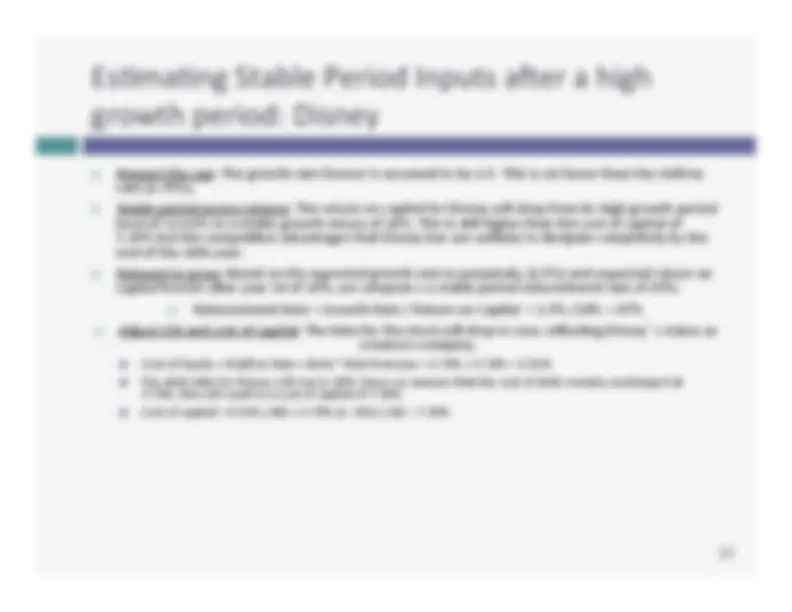

¨ Respect the cap: The growth rate forever is assumed to be 2.5. This is set lower than the riskfree rate (2.75%). ¨ Stable period excess returns: The return on capital for Disney will drop from its high growth period level of 12.61% to a stable growth return of 10%. This is s9ll higher than the cost of capital of 7.29% but the compe99ve advantages that Disney has are unlikely to dissipate completely by the end of the 10th year. ¨ Reinvest to grow: Based on the expected growth rate in perpetuity (2.5%) and expected return on capital forever a]er year 10 of 10%, we compute s a stable period reinvestment rate of 25%: ¨ Reinvestment Rate = Growth Rate / Return on Capital = 2.5% /10% = 25% ¨ Adjust risk and cost of capital: The beta for the stock will drop to one, reflec9ng Disney’s status as a mature company. ¤ Cost of Equity = Riskfree Rate + Beta * Risk Premium = 2.75% + 5.76% = 8.51% ¤ The debt ra9o for Disney will rise to 20%. Since we assume that the cost of debt remains unchanged at 3.75%, this will result in a cost of capital of 7.29% ¤ Cost of capital = 8.51% (.80) + 3.75% (1-‐.361) (.20) = 7.29%