Download Volume II Chapter 1 and more Lecture notes Accounting in PDF only on Docsity!

_________________________________________

Financial Policy

Volume II

Appropriations, Funds, and Related Information

Chapter 1

VA's Accounting Classification Structure

Approved:

Jon J. Rychalski

Assistant Secretary for Management

and Chief Financial Officer

- VA’s Accounting Classification Structure Volume II – Chapter

- 0101 Overview

- 0102 Revisions

- 0103 Definitions

- 0104 Roles and Responsibilities

- 0105 Policies

- 010501 General Policies

- 010502 Accounting Classification Structure (FMS)

- 010503 Accounting Classification Structure (iFAMS)........................................

- 010504 United States Standard General Ledger

- 010505 VA Standard General Ledger

- 010506 Agency Location Codes

- 0106 Authorities and References

- 0107 Rescissions.......................................................................................................

- 0108 Questions

- Appendix A: History of Revisions to this Chapter

- Appendix B: VA Station Numbers (FMS)...................................................................

- Appendix C: VA Organization Codes (iFAMS)

- Appendix D: Agency Location Codes

- Appendix E: VA’s Revenue Source Codes (FMS)....................................................

- Appendix F: VA’s Revenue Source Codes (iFAMS)

- Appendix G: Updating Elements in VA’s Accounting System (FMS)

- Appendix H: Updating Elements in VA’s Accounting System (iFAMS)

- Appendix I: General Ledger Request Process (FMS and MinX)

VA’s Accounting Classification Structure Volume II – Chapter 1

Section Revision Office Reason for Change Effective Date

Appendices E and F

Incorporated charts of VA Revenue Source Codes (RSCs) for FMS and iFAMS

OFP

(047G)

Implementation of iFAMS accounting system

November 2020

Appendices G, H, and I

Incorporated procedures for updating elements in VA’s ACS and VA SGL

OFP

(047G)

Implementation of iFAMS and Removal of Procedures from Volume I, Chapter 4

- Compliance with Federal Financial Management Improvement Act

November 2020

Various

Reformatted to new policy format and completed five-year update

OFP

(047G)

Reorganized chapter layout

February 2020

0102 Policy 0105 Procedures Appendix F, Journal Voucher Procedures

Removed journal voucher information from this policy and created Volume II, Chapter 1A – VA Journal Vouchers

OFP

(047G)

JV information is more appropriate in a separate policy

February 2020

VA SGL

Account Procedures (Formerly Appendix D)

Removed procedures for establishing and maintaining VA SGL Accounts

OFP

(047G)

Information is contained in Volume I, Chapter 4 – Financial Management Systems

February 2020

0103 Definitions

Accounting Classification Structure – The categorization of accounting data along several dimensions allowing the retrieval, summarization, and reporting of information in a meaningful way.

Agency Location Code (ALC) – A numeric symbol assigned by Treasury to identify an agency accounting and/or reporting office.

Budget Object Class (BOC) Code – Categories in a classification system that present obligations by the items or services purchased by the Federal Government.

VA’s Accounting Classification Structure Volume II – Chapter 1

Budgetary Account – An account that reflects budgetary operations and conditions, such as estimated revenues, appropriations, and obligations.

Cost Center – A four to six-digit code used to accumulate costs incurred by area of responsibility or geographic region (e.g., 301000, [Veterans Benefits Administration (VBA)] Executive Director). The cost center field only relates to Administrations and Staff Offices that utilize FMS. iFAMS contains a non-ACS field for the FMS cost center (does not impact the iFAMS ACS or iFAMS GL).

Direct Obligation – An obligation financed by appropriations, in contrast to reimbursable obligations.

Division Code – Classifies financial transactions by the entities responsible for managing resources and carrying out the programs and activities of the Federal Government. The Division Code represents the top level of the hierarchical structure in iFAMS, followed by the Organization Code.

Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) – A Treasury operated Government-wide web-based accounting system used by Federal agencies to submit both budgetary and proprietary financial data.

Integrated Financial and Acquisition Management System (iFAMS) – The system replacing VA’s legacy accounting system, FMS as the official financial and acquisition system of record. VA is implementing iFAMS in waves beginning in 2020.

Location Code – Represents the physical address of each organizational unit in VA’s Administrations and Staff Offices.

Object Class – Categorization of financial obligations and expenditures according to the nature of the services or items purchased as defined in OMB Circular A-11, Section

Organization Code – Classifies financial transactions by the entities responsible for managing resources and carrying out the programs and activities of the federal government. The organization code represents the lower levels of the hierarchical structure below the Division Code in iFAMS.

Proprietary Account – Accounts used to recognize and track assets, liabilities, net position accounts, revenues, and expenses.

Reimbursable Obligation – An obligation financed by offsetting collections credited to an expenditure account in payment for goods and services provided by that account.

Revenue – The inflow of resources brought into VA, earned through exchange transaction activity or received through non-exchange transactions. This may include

VA’s Accounting Classification Structure Volume II – Chapter 1

Congressional committees during the formulation process, defending and promoting VA’s program plans and budget estimates before examiners and committee staff. OB also obtains apportionments from OMB and issues Financial Management Allowances and Transfer of Disbursing Authority documents to establish funds controls in VA’s accounting system, and monitors execution for funds control and adherence to operating plans.

VA’s Station Identification Officer is responsible for assigning and maintaining the uniform station number system in FMS, as detailed in Appendix B, VA Station Numbers.

Financial Services Center (FSC) is responsible for maintaining the VA Standard General Ledger accounts, budget object classes, and revenue source codes. FSC is also responsible for the yearly update of the ALC Point of Contact listing.

Manpower Management Services within the Office of Human Resources and Administration (OHRA) is responsible for the maintenance of the Division, Organization, Location and Cost Organization Codes elements within iFAMS.

0105 Policies

010501 General Policies

A. An ACS is a comprehensive schema that supports the traceability and data interoperability of financial information to support budget, financial accounting, and performance reporting requirements.

B. The ACS will allow accounting systems to:

- Provide managers with accurate and complete financial data, including total operating expenses and total acquisition cost of real and personal property, to enable informed decision-making;

- Provide for uniform treatment of similar accounting transactions used by all VA organizations;

- Produce expense and cost information concerning programs, projects, and other activities, in accordance with internal management needs;

- Provide data to meet reporting requirements of OMB, Treasury, and the Chief Financial Officers Act of 1990; and

- Provide other financial data, as needed, for both internal and external reporting requirements.

010502 Accounting Classification Structure (FMS)

VA’s Accounting Classification Structure Volume II – Chapter 1

The following minimum elements are required by the Accounting Classification Structure. VA will comply with this structure, to the extent possible given limitations within FMS.

A. The Treasury Account Symbol is an identification code assigned by Treasury, in collaboration with OMB and VA, to an individual appropriation, receipt, or other fund account. Refer to Volume II, Chapter 2, VA’s Budget Cycle and Fund Symbols, for additional information.

B. Budget Fiscal Year refers to the fiscal year in which the obligation is made and captured on the obligating document; it is used to distinguish whether subsequent adjustments affect a prior year or the current year. The budget fiscal year differs from the TAS period of availability. VA’s accounting system uses Budget Fiscal Year to denote the period of availability, establish a base year, or denote year of funding for a no year. It is not the equivalent of the obligation year.

C. The Accounting Period is the period in which a transaction is established in the general ledger. In most instances, the accounting period pertains to a fiscal month within a fiscal year. However, in some instances, it represents a period that falls before or after the fiscal month and is used for recording opening balances to the period or period-end adjustments applicable to a month, quarter, or fiscal year. Accounting periods are used to group transactions by the period in which they are reported. The accounting system periods are from 00 (beginning) to 15 (closing).

- Period 00 - Beginning balances for the new fiscal year;

- Periods 01 to 12 - Monthly activity;

- Period 13 and 14 – Adjusting entries; and

- Period 15 – Closing entries

D. The Internal Fund Code is an agency-assigned code for a fund. It is a shorthand code entered on transactions and enables the derivation of the account identification codes (appropriation, receipt, or other TAS) required for reporting externally to Treasury (for reporting the TAS) and OMB (for reporting the budget account). VA will maintain appropriation fund codes in accordance with Treasury guidance. VA will establish separate fund accounts for direct and reimbursable obligations; these funds shall not be co-mingled. Refer to Volume II, Chapter 2, VA’s Budget Cycle and Fund Symbols.

E. Organization Code, often referred to as Station Number, is the official identification number for funding and budgetary purposes and for describing the sphere of authority of an organizational entity designated by the Secretary. A uniform station number methodology provides a unique identifier for each station and allows for easier association and integration of data among systems.

- The FSC Executive Director and FSC Deputy Executive Director, or other designee (as assigned by the Deputy Chief Financial Officer), are assigned VA’s Station Identification Officers. The Station Identification Officer is responsible for

VA’s Accounting Classification Structure Volume II – Chapter 1

H. Object Class Code, referred to as Budget Object Code (BOC), classifies obligations by the items or services purchased by the Federal government (e.g., personnel compensation, supplies, rent, or equipment). While OMB Circular A-11 establishes the standard codes, titles, and definitions of the object class, an agency may further define extensions for capturing additional detail to support internal information needs. Refer to Volume XIII Chapter 2, Budget Object Codes, for detailed information.

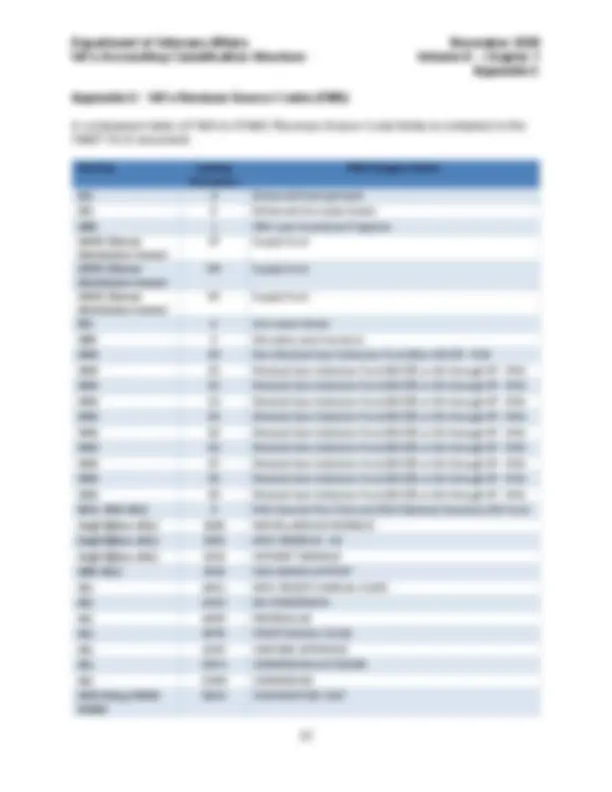

I. Revenue Source Code is used to track the revenue lifecycle from the initial order, processing, and finally to output, providing a history of financial activity related to the receipts. The code is agency-assigned and classifies revenue and receipt transactions by the type or source of revenue. The Revenue Source Codes is a unique four-digit code used to define revenue sources within different VA programs. The code in FMS also represents the mechanism to identify the applicable accounts receivable to move into the next fiscal year as part of the annual close process for Tricare and Shared Medical Resource bills under PL 104-262.

- Existing revenue source codes fall into two categories: (1) asset management revenue source codes, and (2) non-asset management revenue source codes.

- VA will comply with the revenue recognition as required by FASAB, Statement of Federal Financial Accounting Standards (SFFAS) 7: Accounting for Revenue and Other Financing Sources and Concepts for Reconciling Budgetary and Financial Accounting, and OMB A-11, Budget Preparation, Submission, and Execution of the Budget.

- VA will maintain a revenue system, inclusive of revenue source codes, that will provide the capability to trace transactions from their initial source through all stages of related system processing. VA activities that generate income and are identified with associated revenue source codes include, but are not limited to, donations, rental income, enhanced-use leasing, and recycling and waste reduction programs.

- VA administration CFOs, or their designees, or the heads of applicable staff offices or their designees, will approve revenue source codes prior to implementation. A list of personnel approved to submit a request for revenue source codes will be furnished to the Director of VA’s Financial Management System (FMS) Service at the beginning of each fiscal year.

- Requests for new revenue source codes or changes/deletions to current revenue source codes will be forwarded to the Office of Financial Reporting via Microsoft Outlook mailbox, “ACC\FCP Requests.”

VA’s Accounting Classification Structure Volume II – Chapter 1

- FMS has moderate flexibility to accommodate new and emerging reporting requirements, both internally and externally, to enable individual operating components to carry out program responsibilities effectively and efficiently.

a. VA’s revenue source codes are assigned by using a standardized and unique numbering scheme as follows:

i. Enhanced sharing assets must begin with an alpha character of “A” followed by three sequential numbers;

ii. Enhanced-use lease assets must begin with an alpha character of “E” followed by three sequential numbers; and

iii. Out-lease assets must begin with an alpha character of “U” followed by three sequential numbers.

b. The numbering scheme supports the following activities:

- Transactions that record revenues based on sales of products or services, where the products or services are delivered prior to or concurrent with the payment.

- Transactions that allocate receipts to unearned revenue/advances (e.g., allow for entry of receipts to an advance USSGL account, either on an individual transaction basis or for a class of transactions, based on a predefined attribute or combination of attributes).

- Transactions that reclassify prior receipts to earned revenue based on some predetermined factor, such as an application process that allows for the earning of 25 percent of the fee as earned revenue as each step of the process is completed.

- VA uses revenue source codes in the following activities:

a. Supply Fund activities use a numbering scheme that begins with “SF,” “SM,” or “SR,” followed by two numeric characters for its revenue activities.

b. VHA uses revenue source codes for the Medical Care Collection Fund (MCCF) revenue activities and other reimbursable activities. The numbering scheme will begin with either code "81" through "89" with a combination of alpha-numeric for the third and fourth positions – or – with code "8A" through "8P" with a combination of alpha-numeric for the third and fourth positions. VHA will use a numbering scheme that begins with an “80” for all non-MCCF revenues and reimbursable activities.

c. VHA General Post Fund and NCA National Cemetery Gift Fund activities use a numbering scheme that begins with a “9” for revenue activities.

VA’s Accounting Classification Structure Volume II – Chapter 1

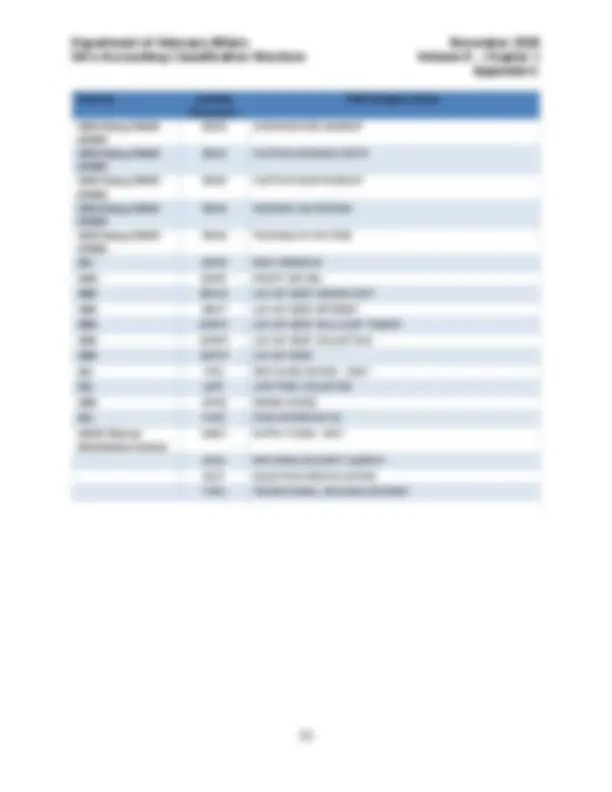

- Periods 01 to 12 - Monthly activity;

- Period 13 – Adjusting entries; and

- Period 14 – Closing entries.

E. The Internal Fund Code is an agency-assigned code value for a fund. The Fund Code and its attributes are used by agencies to classify financial transactions for reporting purposes. An agency’s Treasury Account Symbol (TAS) and Budget Accounts are also part of this category but are typically used for external reporting to Treasury and OMB, respectively. VA will maintain appropriation fund codes in accordance with Treasury guidance. VA will establish separate fund accounts for direct and reimbursable obligations; these funds shall not be co-mingled. Refer to Volume II, Chapter 2, VA’s Budget Cycle and Fund Symbols.

F. The Division Code in iFAMS represents the top level of hierarchical structure for organizational elements in the ACS. The next level of organizational element in the ACS is the Organization Code (referred to as station identification numbers in FMS). These are the official identification numbers for funding and budgetary purposes and for describing the sphere of authority of an organizational entity designated by the Secretary. A uniform organization system provides a unique identifier for each organization and allows for easier association and integration of data among systems which require unique identification in automated information systems.

- VA administrations and staff offices will designate an individual who will serve as an organization code liaison on all organization code matters affecting proposed changes to their field facilities. The liaison will be responsible for ensuring that the official request is accurate, complete and forwarded to the VAFSC Financial Accounting Service Program Office in the timeframe as specified in Appendix B, VA Station Numbers.

- The FSC Executive Director and FSC Deputy Executive Director, or other designee, are assigned as VA’s Organization Code Officer. The Organization Code Officer is responsible for approving, assigning, and maintaining the VA organization number system. A listing of VA facilities and organization / FMS station numbers is found at the VA Facility Listing website.

- In iFAMS, the FSC Director and FSC Deputy Director will initially approve the Organization / Station Identification codes and upload documentation into iFAMS as an attachment to be routed to Manpower Management Service for final approval as they are the data owner for Division, Organization, Location, and Cost Organization Codes.

G. Program, Project, and Activity (PPA) Codes provide VA the means to categorize financial information to support budget execution and reporting functions. The PPA Codes generally represent the lowest level of budget distribution. Refer to VA Volume II, Chapter 2, VA’s Budget Cycle and Fund Symbols, for additional information on the budget process. Detailed reference information for Accounting

VA’s Accounting Classification Structure Volume II – Chapter 1

Classification Codes, Budget Object Codes, Cost Centers, End of Month Reports, Funds, and other accounting transaction reports is available on the FMS Home website.

- Budget Program Code (BPC) – Defines distinct lines of work performed by organizations responsible for carrying out that function. The BPC reflects the application of authorized budgetary resources used for that function (unobligated balances, appropriations, borrowing authority, prior year recoveries, transfers, and collections). The BPC is also used to capture the application of budgetary resources to obligations by program activity, subject to reporting requirements in OMB’s MAX A-11 database and the Digital Accountability and Transparency Act (DATA Act).

- VA Program Code – Identifies an organized set of programs directed toward a common purpose or goal that an agency undertakes or proposes to carry out its responsibilities. VA Administrations and Staff Offices determine the VA Program Codes to meet their tracking and reporting requirements.

- Project – identifies a planned undertaking of something to be accomplished or produced, or an undertaking having a finite beginning and finite ending.

- Project Task Code – Identifies the actual work task or step performed in producing and delivering products and services within a project. It also captures the aggregation of actions performed within an organization that are useful for the purposes of activity-based costing. A Project Task Code must be used in conjunction with Project Code.

- Activity Code – represents business functions performed by VA. In many cases, business functions have subordinate sub-functions. The Activity Codes are intended to enable the aggregation of similar business functions across the VA (e.g., budget management, contract administration, talent development, podiatry, manage patient safety, occupational health management, etc.).

- VA will ensure that the PPA data elements and definitions are uniform and efficient for budget and accounting treatment, classification, and reporting.

- PPA are established for each budget fiscal year. IFAMS contains information on standard PPA used by more than one organization / station and non-standard codes that are used by a single organization / station. Users may identify the standard ACS by an asterisk in the Station field.

H. In iFAMS, the organization class value is representative of the FMS Cost Center, where the FMS cost centers are organizationally based. The FMS cost center is housed in iFAMS as a non-ACS user-defined field. iFAMS will maintain the integrity of the standardized data and provide the user with an understanding of how FMS cost centers relate to the new iFAMS ACS.

I. Object Class Extension, referred to as Budget Object Class (BOC) Code, classifies obligations by the items or services purchased by the Federal government (e.g., personnel compensation, supplies, rent, or equipment). While OMB Circular A- establishes the standard codes, titles, and definitions of the object class, an agency

VA’s Accounting Classification Structure Volume II – Chapter 1

- Transactions that record revenues based on sales of products or services, where the products or services are delivered prior to or concurrent with the payment.

- Transactions that allocate receipts to unearned revenue/advances (e.g., allow for entry of receipts to an advance USSGL account, either on an individual transaction basis or for a class of transactions, based on a predefined attribute or combination of attributes).

- Transactions that reclassify prior receipts to earned revenue based on some predetermined factor, such as an application process that allows for the earning of 25 percent of the fee as earned revenue as each step of the process is completed.

K. A Trading Partner is a federal entity that is party to intragovernmental transactions with another federal entity.

L. Procedures for updating elements of the ACS and VA SGL in iFAMS are found in Appendices H and I.

010504 United States Standard General Ledger

A. VA’s ACS will support Treasury’s reporting requirements via compliance with the Treasury Financial Manual and the United States Standard General Ledger (USSGL).

B. Proprietary asset and liability accounts cover the receipt of funds in the Treasury, the proper classification of assets (such as receivables, prepayment, inventory, and fixed assets), and the recognition and proper classification of liabilities. The transactions in these accounts provide information on how operations are functioning, as well as ensure that the basic accounting equation remains in proper balance. Revenue and expense accounts measure the realization of revenues from reimbursements and the recognition of costs through the use and consumption of assets. The financial control provided through accounting records for property provides managers with a tool that helps to effectively discharge their stewardship function for those resources.

C. Budgetary accounts reflect the recording of appropriation, apportionment, allocation, commitment, obligation, reimbursement and expenditure processed. The transactions involve anticipating resources, realizing resources, or changing the status of resources.

010505 VA Standard General Ledger

A. VA’s Chart of Accounts will be based upon the USSGL, thus providing a consistent basis for recording and reporting financial transactions and resource balances. The

VA’s Accounting Classification Structure Volume II – Chapter 1

Chart of Accounts will also provide the basic structure for VA’s proprietary and budgetary reporting functions. In iFAMS, the General Ledger Account Code dimension consists of the USSGL Account and Extension Code, which is at the lowest level. The four roll-ups associated with the General Ledger Account Code are Category, Class, Group and Type, which are characteristics of the GL Account.

B. VA SGLs must point to or roll into a valid USSGL.

C. VA may use SGL accounts in its accounting system that are more detailed than the USSGL chart of accounts to provide detailed information for decision making or reporting purposes.

D. VA will use, maintain, and record SGL accounts for all appropriations and fund activities, regardless of the source of funds.

E. In addition to the USSGL accounts published by Treasury, VA may use SGL accounts in the accounting systems that are different from the USSGL Chart of Accounts when it is deemed necessary and the internal SGLs are rolled into a valid USSGL.

VA’s six-digit SGL accounts are classified as follows:

- 100000 Assets;

- 200000 Liabilities;

- 300000 Net Position;

- 400000 Budgetary;

- 500000 Revenues and Financing Sources;

- 600000 Expense;

- 700000 Gains/Losses/Extraordinary Items, etc.;

- 800000 Memorandum; and

- 900000 Memorandum

USSGL 800000 is currently used by VBA for credit reform transactions and by all organizations to capture purchases of PP&E.

F. VA will record all transactions (e.g., resources acquired and used by VA and claims against those resources) to the appropriate SGL (transaction level) in VA’s accounting system.

G. Refer to Appendix I, General Ledger Request Process, for the procedures for establishing and maintaining VA SGL Accounts.

010506 Agency Location Codes

VA’s Accounting Classification Structure Volume II – Chapter 1

Treasury Financial Manual

TFM US Standard General Ledger

VA Facility Listing website

VA Financial Policy Volume I, Chapter 4 – Financial Management Systems

VA Financial Policy Volume II, Chapter 2 - Budget Cycle and Fund Symbols

VA Financial Policy Volume VII – Financial Reporting

VA Financial Policy Volume XIII, Chapter 1 – Cost Centers

VA Financial Policy Volume XIII, Chapter 2 – Budget Object Class Codes

VA FMBT ACS SharePoint Site

0107 Rescissions

Volume II Chapter 1, VA’s Accounting Classification Structure, February 2020.

0108 Questions

Questions concerning these financial policies should be directed to the following points of contact:

VHA VHA Financial Policy (Outlook) VBA VAVBAWAS/CO/OPERATIONS (Outlook) NCA NCA Financial Policy Group (Outlook) All Others OFP Accounting Policy (Outlook)

VA’s Accounting Classification Structure Volume II – Chapter 1 Appendix A

Appendix A: History of Revisions to this Chapter

A. The following table provides the history of revisions to this chapter.

Section Revision Office Reason for Change

Effective Date Appendix C, Agency Location Codes (Previously numbered Appendix E)

Updated VBA’s contact information on the ALC chart

OFP

(APS)

Contact information was updated

September 2018

Appendix F

Updated the FSC Accounting e-mail address, FMS JV Approval procedures, and MinX JV Data Field Requirements

OFP

(047G)

Financial Reporting Corrective Action Plan

September 2018

Definitions Added iFAMS definition

OFP

(047G)

Define iFAMS June 2018

Appendix E Updated ALC listing

OFP

(047G)

Added ALC listing for iFAMS processing

June 2018

Appendix D

Updated responsibilities for maintenance of USSGL accounts

OFP

(047F)

To reflect current responsibilities and procedures

February 2018

Appendix E Update Agency Location Code listing

OFP

(047G)

Update with current information

February 2018

0102 Policies

Added pre-approval requirement for non- routine FMS and MinX JVs equal to or greater than $100 million

OFP

(047G)

NFR 15-1,

Consolidated Financial Reporting

December 2017

Agency Location Code

Removed references to Treasury FMS 224, Statement of Transactions

OFP

(047G)

FMS 224 is no longer used

December 2017

0104 Roles and Responsibilities

Assigned roles and responsibilities for pre- approval of non-routine FMS and MinX JVs equal to or greater than $100 million

OFP

(047G)

NFR 15-1,

Consolidated Financial Reporting

December 2017