Download Volume V, Chapter 9 and more Summaries Construction in PDF only on Docsity!

_________________________________________

Financial Policy

Volume V

Assets

Chapter 9

General Property, Plant, and Equipment

Approved:

Jon J. Rychalski

Assistant Secretary for Management

and Chief Financial Officer

General Property, Plant, and Equipment

General Property, Plant, and Equipment Volume V - Chapter 9 0901 OVERVIEW This chapter establishes the Department of Veterans Affairs’ (VA) financial policy and procedures for general property, plant, and equipment (PP&E) owned or leased by VA, to include depreciation or amortization, deferred maintenance and repairs, non-recurring maintenance, and major and minor construction projects. VA has a vast holding of diverse assets consisting of hospitals, clinics, cemeteries, office buildings, and medical and non-medical equipment, VA-owned and leased. For the purposes of this chapter, heritage assets, internal use software (IUS), stewardship property, and hazardous cleanup (e.g., asbestos or other hazardous waste removal) are not included. Refer to Office of Financial Policy (OFP) Volume III, Miscellaneous Accounting Topics , Chapter 7, Required Supplementary Stewardship Information, Volume V, Assets, Chapter 13, Accounting for Internal Use Software, Chapter 14, Heritage Assets & Stewardship Land, and Volume VI, Liabilities , Chapter 8, Environmental and Disposal Liabilities, for additional VA policy specific to these topics. VA’s overall governance, oversight and policies for current and future assets are guided by rules and requirements of various laws and regulations, such as the Statement of Federal Financial Accounting Standards (SFFAS), Government Performance and Results Act (GPRA), Federal Financial Management Improvement Act of 1996, and Office of Management and Budget (OMB) circulars. Each of these has distinct requirements, and VA has incorporated them into policies for acquiring and managing capital assets. Refer to Appendix A, Guidance on Managing VA Assets, for additional information. 0902 POLICIES 090201 PROPERTY, PLANT, AND EQUIPMENT 090201.01 PP&E DETERMINATION. VA will follow SFFAS 6: Accounting for Property, Plant, and Equipment , and other related standards for PP&E and related accounting transactions. A. To properly determine, record, and report PP&E, VA must first determine that the item is considered PP&E. PP&E is defined as tangible assets that:

- Have an estimated useful life of 2 years or more;^1

- Have been acquired or constructed with the intention of being used or being available for use by VA; and

- Are not intended for sale in the ordinary course of VA operations. (^1) Used as an accounting basis, the normal operating life of an asset in terms of usefulness to the owner. Refer to section 090206 Depreciation/Amortization Expense.

General Property, Plant, and Equipment Volume V - Chapter 9 PP&E does not include items held in anticipation of physical consumption, such as operating materials and supplies, and items in which VA has a reversionary interest.^2 B. PP&E Characteristics. PP&E typically is used:

- To produce goods or services or to support the mission of the agency, but could be used for alternative purposes (e.g., by other Federal programs, state or local governments or non-governmental entities);

- For business-type activities;^3 or

- For entity activities whose costs may be compared to other entities performing similar activities, e.g., VA medical hospitals compared with other hospitals. C. PP&E is further classified as either real or personal property.

- Real property consists of Federal facilities and installed equipment, to include real property acquired through capital leases and leasehold improvements,^4 and real property owned by VA, but held by others. Real property may include:

- Land, buildings, other structures,^5 and improvements to land, to include water and sewage systems, roads, sidewalks, and other improvements,

- Leased real property, whether owned commercially or by the General Services Administration (GSA), or

- Building service equipment, which is an integral part of the real property for the purpose of rendering the building or structure usable or habitable and permanently affixed. For example, heating/air-conditioning systems, lighting fixtures, elevators, vaults, fire alarm systems, and other items normally required for the functional use of buildings and structures. (^2) The Federal government sometimes retains an interest in PP&E acquired with grant money. In the event that the grant recipient no longer uses the PP&E in the activity for which the grant was originally provided, the PP&E reverts to the Federal Government. (^3) Business-type activity is defined as a significantly self-sustaining activity which finances its continuing cycle of operations through the collection of revenue as defined in SFFAS 7: Accounting for Revenue and Other Financing Sources. (^4) Leasehold improvements include improvements made to PP&E acquired through either a capital or operating lease. (^5) Other structure is an asset not classified as another real property category (e.g., parking garages, open- sided sheds, water towers, generators, solar panels, and windmills). The asset may be a structure or system serving more than one building or structure as one asset and is not building service equipment. The asset is carried as one asset in the subsidiary records. Other structures (or other real property) is generally classified as BOC 3240 or 3241 titled, Other Structures (or Facilities).

General Property, Plant, and Equipment Volume V - Chapter 9

- Normally has, but is not limited to, an acquisition cost of $300 or more. An item classified as non-expendable may cost less than $300, e.g., refrigerators, microwave, printers, digital cameras, and items of a sensitive nature that require accountability controls. b. For property not listed in ISMS, a request should be emailed to the Operations Analysis Division (OAD), located at VA’s National Acquisition Center (NAC)^10 , which is responsible for assigning a CSN to new non-expendable items. VA Form 0886, Request for Catalog Change, will be used by field activities when requesting to change an item from non-expendable to expendable. 090201.02 PP&E COSTS. After a determination has been made that an asset is considered PPE, as defined above, the cost of the asset must be determined to properly record the item. Recording PP&E costs accurately begins with identifying purchases that meet generally accepted accounting principles for included costs and those that do not. In accordance with SFFAS 6, cost shall include all costs incurred to bring the PP&E to a form and location suitable for its intended use. As applicable, PP&E costs may include, but are not limited to:

- Amounts paid to vendors.

- Transportation charges to the point of initial use.

- Handling and storage.

- Labor (including purchase and hire), materials, supplies and other direct or indirect production costs (for assets produced or constructed).

- Engineering and architectural services for designs, plans, specifications and surveys.

- Acquisition and preparation costs of land, buildings, and other structures or facilities. Preparation costs of land may include such items as initial clearing, grading, or other permanent land developments.^11

- Fixed equipment and related installation costs required for activities in a building or facility. (^10) The OAD contacts are available on the NAC Contacts web page under Business Resource Service, http://www.va.gov/oal/about/nacContacts.asp. (^11) Land developments may be included in the cost of land, buildings, or other structures as appropriate. Land developments are not recorded as a separate asset.

General Property, Plant, and Equipment Volume V - Chapter 9

- Site preparation costs directly related to equipment.^12

- Direct costs of inspection, supervision, and administration of construction contracts and construction work, such as Corps of Engineers surcharges.

- Administration of contracting costs for equipment purchases, such as Solutions for Enterprise-Wide Procurement (SEWP) fees, Corps of Engineers, etc.

- Legal and recording fees, and damage claims. PP&E costs should not include: NAC surcharge (or other surcharges or fees within VA) associated with the acquisition and/or construction of PP&E.

- Feasibility studies. Feasibility studies are not the same service described in engineering and architectural services described above.

- Training costs, such as materials or travel for class, which are not associated with IUS. 13 Post-implementation training costs or costs identified or reasonably estimated in the PP&E contract price will be expensed; training costs that cannot be easily extrapolated from a contract may be capitalized with the PP&E.

- Costs related to continuing operations will not be a cost of the asset, for example, the cost of renting a Computerized Tomography (CAT) Scan trailer during construction or the cost of operating supplies.

- Cost for asbestos and hazardous material clean-up (See 090202.05 Asbestos and Hazardous Material Clean-Up Costs). 090201.03 RECORDING PP&E. Each VA Administration and Staff Office will maintain records of both owned and leased assets and agreements to serve their organizational needs. Electronic or hardcopy documentation will be maintained for both capitalized assets and expensed non-capitalized assets. Basic documentation will be maintained for the life of the asset and for three years after disposal or transfer of the asset, as (^12) Where a site preparation project is only related to the installation of a specific equipment asset, the cost of the project should be included in the capitalized value of that equipment asset and the evaluation of the capitalization threshold will apply to the total cost (i.e. site prep plus equipment cost). Where a project contains site preparation costs, but is larger in scope than site preparation for a specific piece of equipment (e.g. total renovation of a wing or facility), the project will be treated as a betterment to the building asset and evaluated independently of the equipment asset. Asbestos and other hazardous material removal are not part of the site preparation cost. Refer to Volume VI, Liabilities , Chapter 8, Environmental and Disposal Liabilities, for additional information. (^13) Refer to OFP Volume V, Chapter 13, Accounting for IUS , for cost information related to IUS.

General Property, Plant, and Equipment Volume V - Chapter 9

- VA will record PP&E acquired by exchange or transfer from another Federal agency at the cost recorded by the transferring entity less any accumulated depreciation (net book value). If the receiving station within VA cannot reasonably ascertain the net book value, the cost will be the fair value at the time acquired.

- VA will record PP&E acquired through exchange at the fair value of the PP&E surrendered at the time of exchange. If the fair value of the PP&E acquired is more readily determinable than that of the PP&E surrendered, the cost shall be the fair value of PP&E acquired. If neither the surrendered or acquired fair value can be determined, the cost of the PP&E will be the cost recorded less any accumulated depreciation or amortization. a. In the event that cash consideration is included in the exchange, the cost of general PP&E acquired will be increased by the amount of cash consideration surrendered or decreased by the amount of cash consideration received.^17 b. Any difference between the net recorded amount of the PP&E surrendered and the cost of the PP&E acquired will be recognized as a gain or loss.

- VA will record PP&E acquired through forfeiture in accordance with SFFAS No. 3, Accounting for Inventory and Related Property. Refer to Volume V, Chapter 8, Inventories , for additional guidance. D. VA will record the cost of PP&E net of purchase discounts. VA will recognize purchase discounts lost and late payment penalties as an operating expense in the period incurred. E. VA will record expenditures incurred to maintain PP&E in a satisfactory operating condition as an operating expense, refer to 090202, Capitalization and 090202.03, Maintenance and Repairs. Some examples of expenditures may be preventive maintenance, repainting, normal maintenance and repair, and costs incurred under the terms of a service contract. F. VA will record non-expendable equipment in the Fixed Assets Package (FAP) Subsystem^18 through an interface with the Automated Engineering Management System/Medical Equipment Reporting System (AEMS/MERS). AEMS/MERS serves as the inventory record for accountable equipment, which may be either capitalized or non- capitalized assets. FAP documents the original and subsequent value of assets and interfaces with other VA Financial Management System (FMS) subsystems to support fiscal and risk management as well as standard reporting. Refer to Appendix C, Fixed Asset Package (FAP) Subsystem Procedures, for additional information. (^17) Example: Equipment purchased for $1,300,000 plus trade-in valued at $100,000, will be recorded with a cost of $1,400,000 (1,300,000 + $100,000) (^18) The FAP Subsystem is VA’s subsidiary ledger that supports many types of assets such as land, buildings and nonexpendable equipment.

General Property, Plant, and Equipment Volume V - Chapter 9

- All non-expendable equipment within AEMS/MERS is assigned a standardized Equipment Inventory List (EIL) number.

- An EIL number identifies the department within the facility to which the equipment belongs and is to be used when entering equipment in the AEMS/MERS system and conducting physical inventories. G. VA will use historical cost, when available, to record PP&E assets that are not recorded or not recorded correctly. However, when historical cost is not readily available, VA may reasonably estimate the historical cost.^19

- VA may use historical cost estimates based on any of the following: a. The cost of similar assets at the time of acquisition; b. The current cost of similar assets discounted for inflation since the time of acquisition (i.e., deflating current costs to costs at the time of acquisition by general price index); c. Information such as, but not limited to, budget, appropriations, engineering documents, contracts, or other reports reflecting amounts to be expensed; d. The current replacement costs of similar items and deflating those costs; or e. Other reasonable auditable methods.

- VA Administrations and Staff Offices’ financial activities are responsible for maintaining adequate documentation to support the historical cost data and the methodology. Refer to section 090501A, Reconstructing or Correcting PP&E Records. 090202 CAPITALIZATION. Purpose of Capitalization and Depreciation: Capitalization recognizes the cost of acquiring a tangible resource as an asset, on the balance sheet, for more than one operating cycle. The purpose of depreciation is to match the cost of a productive asset (that has a useful life of two years or more) to the revenues earned from using the asset. Since it is hard to see a direct link to revenues, the asset's cost is usually allocated to (assigned to, spread over) the years in which the asset is used. Depreciation systematically allocates or moves the asset's cost from the balance sheet to expense on the income statement over the asset's useful life. In other words, depreciation is an allocation process in order to achieve the matching principle; it (^19) Per SFFAS 35 as it amended SFFAS 6, Accounting for Property, Plant, and Equipment.

General Property, Plant, and Equipment Volume V - Chapter 9 the property is placed in service. The date the asset is placed in service is considered to be the date of acquisition.

- When construction WIP projects meet the capitalization threshold, but are installed in phases, VA will capitalize each phase when placed in service, regardless of the cost of the phase.

- The net amount of all phases encompassing the total project shall be considered when assessing whether the capitalization threshold will be met. Refer to the section 090203, Construction WIP F. For PP&E that is acquired or constructed by a central VA organization, VA will transfer the assets to the responsible organization when the asset is placed in service. Refer to section 090502C and Appendix E, Procedures for Transferring Assets within VA. The procedures provided in the appendix are general guidance and may be altered to accomplish a similar transfer as circumstances dictate. The purchasing or transfer- out finance activity and receiving finance activity will coordinate actions to ensure that PP&E is properly transferred and is not duplicated in FMS. G. VA will capitalize its share of PP&E acquired in joint ownership projects with another entity when VA’s portion of ownership meets the capitalization criteria. 090202.01 PERSONAL PROPERTY COMPONENTS. VA will capitalize personal property components that make up a system, e.g., a larger piece of equipment, or an asset, when the combined cost of the system meets VA’s capitalization criteria and when either title passes to VA or when it is delivered and accepted by VA. A. VA will record a (personal property) system serving more than one building or structure as one asset in the subsidiary records. The system cost will not be distributed to an associated asset, e.g., a building or structure. B. When the planned system purchased meets the capitalization threshold, but is installed in phases, VA will capitalize each component, regardless of the individual cost, when either the title passes to or when it is delivered and accepted by VA. Refer to 090202, Capitalization. The system is recorded as one asset. C. When the planned system purchased is expensed, VA will expense any subsequent components purchased.

General Property, Plant, and Equipment Volume V - Chapter 9 090202.02 SUBSEQUENT EXPENDITURES - ADDITIONS OR IMPROVEMENTS (a.k.a., BETTERMENTS^24 ). According to SFFAS No. 6, costs which either extend the useful life of existing general PP&E, or enlarge or improve its capacity shall be capitalized and depreciated/amortized over the remaining useful life of the associated general PP&E. VA will capitalize additions and improvements (subsequent to the acquisition or construction of a capitalized asset) if a project meets the VA capitalization acquisition cost or FMV threshold as applicable: o $100,000, prior to October 1, 2013; o $1,000,000, on or after October 1, 2013; and if it, meets one of the following criteria, otherwise will be expensed:

- Has extended the useful life of an associated asset (as opposed to maintaining its normal operating life); or

- Has enlarged or improved the capacity or function of the associated asset; or

- The quantity of services or units produced from the associated asset is increased. For additional information on projects that may be considered subsequent projects, refer to sections 090202.04, Severely Damaged or Destroyed Assets, as applicable to these items and to Appendix D: Examples of Capitalization versus Expense including Capitalization Worksheet. Refer to section 090206E, Subsequent Projects, for additional information on depreciation/amortization. 090202.03 MAINTENANCE AND REPAIRS. Under normal conditions, maintenance and repairs are expensed because they are used to keep assets in an acceptable working condition. They may include preventive maintenance, normal repairs, replacement of parts and structural components, and other activities needed to preserve the asset for it to continue to provide acceptable services and achieve the expected life. The intent behind the replacement of an asset or part of asset is crucial to the determination of whether a replacement is a repair or an improvement. When repairing a real property facility, the components of the facility may be repaired by replacement, and the replacement may involve upgrading to current building standards and codes and generally would be expensed. In certain conditions, a maintenance or repair project may become larger than anticipated and be deemed an improvement to the asset and may be capitalized. (^24) For accounting purposes, an improvement is also referred to as betterment.

General Property, Plant, and Equipment Volume V - Chapter 9 B. VA will fund construction project costs incurred during the design and development phases from applicable VA construction appropriations and record the costs in the appropriate WIP accounts. Following are examples of costs that may be included:

- All materials, supplies and services applicable to the project;

- All items of installed capital equipment;

- Transportation costs applicable to materials, supplies, any installed capital-type equipment and any Government-owned equipment;

- The additional overhead or support costs that would not have been incurred were it not for the project;

- Travel and per diem related to applicable labor; and,

- The costs applicable to the operation and maintenance of Government-owned equipment. (Refer to section 090201.02, PP&E Costs.) C. VA will maintain separate appropriated fund accounts, as authorized, for major and minor construction and non-recurring maintenance projects, and supporting documentation for the construction WIP on each project.

- VA will carry forward available fund balances from year to year in its construction multi-year and no-year funds as appropriate.

- VA will keep track of and manage carryover balances remaining after construction projects are completed to ensure unexpended fund balances are available for other construction project needs.

- VA will not acquire or improve a real property facility (major construction projects) through a series of minor construction projects in lieu of a single major construction project, since incremental-type construction violates the intent of Congressional appropriations. D. VA will notify and submit information on the status of construction projects to Congress as required. VA will submit its entire major construction project plans for medical facilities to Congress for approval, as required by 38 U.S.C. 8104(a) (2), prior to receiving appropriated funds. E. VA will record constructed real property as construction WIP until it is placed in service.^25 The asset will be transferred to either capitalized or non-capitalized PP&E, as (^25) For constructed real property, “placed in service” is the date the asset is ready and available for its intended use. Even if the property is not being used, it is in service when it is ready and available for its

General Property, Plant, and Equipment Volume V - Chapter 9 appropriate, within 90 days of being placed in service. The date the asset is placed in service is also the date of acquisition. Refer to section 090202, Capitalization, for additional information.

- VA will record a construction project completed in multiple phases as “construction WIP” until the project phase is placed in service.

- Each project may be comprised of multiple assets. Each asset, e.g., building, land improvement, other structure, will be recorded as a separate asset when it meets the capitalization criteria as identified in section 090202, Capitalization.

- Personal property and equipment not capitalized and installed as part of a construction project should be recorded in the appropriate personal property records. 090204 LEASES. Leases include capital leases, lease purchases, or operating leases. A. Capital Lease. VA may acquire PP&E under a capital lease arrangement; a capital lease may be for real or personal property. VA will ensure that a proposed capital lease meets the capitalization criteria (section 090202, Capitalization) and any one of the following criteria^26 :

- The lease transfers ownership of the property to VA at the end of the lease term;

- The lease contains an option for VA to purchase the leased property at a bargain price;

- The lease term is equal to or greater than 75 percent of the estimated economic life of the leased property; or

- The present value of rental and other minimum lease payments, excluding the portion of the payments representing executory cost, equals or exceeds 90 percent of the fair value of the leased property.

- VA will capitalize the asset (leased property or equipment) in an amount equal to the liability for the capital lease at its inception, i.e., the net present value of the capital lease asset’s minimum lease payments during the lease term (base and any amortized build-out) excluding executory costs (insurance, maintenance, and taxes for leased property whether paid by lessee or lessor). Refer to Volume VI, Chapter 18, Capital Lease Liability , for additional guidance on recording the liability and subsequent payments. intended use. Placed in service date may not coincide with the completion of financial actions (e.g., payments). (^26) The last two bullets are not applicable when the beginning of the lease term falls within the last 25 percent of the total estimated economic life of the leased property.

General Property, Plant, and Equipment Volume V - Chapter 9

- Ownership and risk of ownership of the asset remains with the lessor during the term of the lease and is not transferred to the Government at or shortly after the end of the lease period.

- The lease does not contain a bargain-price purchase option.

- The lease term does not exceed 75 percent of the estimated economic lifetime of the asset.

- The present value of the minimum lease payments over the life of the lease does not exceed 90 percent of the fair market value of the asset at the inception of the lease.

- The asset is a general purpose asset rather than being for a special purpose of the Government and is not built to unique specification for the Government as lessee.

- There is a private-sector market for the asset.

- VA will record an operating lease as an expense equal to the amount of the rental payments not to exceed 12 months unless the fund is available for a longer period. 090205 LEASEHOLD IMPROVEMENTS. VA will capitalize a leasehold improvement that meets VA’s capitalization criteria. Refer to section 090202, Capitalization, for the criteria, and 090206F for the amortization requirements. A. Leasehold improvements may include improvements made to either a capital or operating lease. B. Leasehold improvements to an operating lease are only capitalized if the operating lease renewals are determined to be “reasonably assured.”^28 090206 DEPRECIATION/AMORTIZATION EXPENSE. A. VA will record depreciation expense on PP&E, except land and land rights of unlimited duration, in a contra asset account - accumulated depreciation. The depreciation expense will be recorded monthly using the straight-line method of depreciation with salvage value set at zero and will be reflected on capital assets in the financial statements as prescribed by SFFAS No. 6 and OMB Circular A-136. Refer to sections 090201.01C1 (Real Property) and 090201.01C2 (Personal Property) for additional information.

- The finance activity will work in conjunction with the engineering staffs or program managers to assign the useful life for real property, and with the OAD for personal (^28) To assume a moderately sufficient extent or degree of certainty that an action will come to fruition or pass, to include as designated in the contract renewal periods.

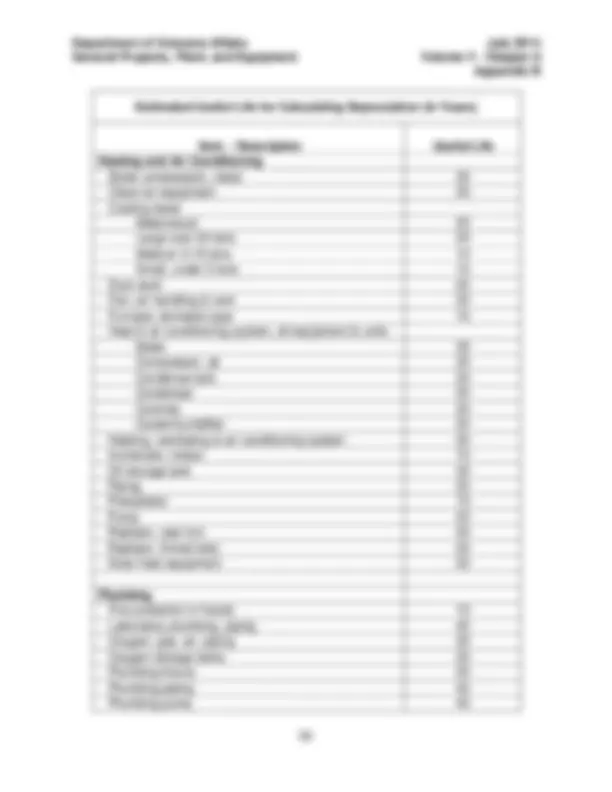

General Property, Plant, and Equipment Volume V - Chapter 9 property. The estimated useful life of certain real property is provided in Appendix B, VA Real Property Estimated Useful Life Guide, or it may be derived from a recognized source^29 used by an administration or staff office. Engineering staffs or program managers will use the tables in Appendix B only as a guide in determining the useful life of real property. Any deviation from the useful life in the Appendix B tables will be supported and provided to the finance activity for recording the transaction.

- The assigned useful life will reflect the primary element of the property for which costs may be determined.

- For projects containing component elements, the useful life assigned will reflect the component part which best represents the project as a whole.

- The finance activity will validate the calculation of depreciation generated from the FAP subsystem and ensure depreciation has been recorded monthly for all capital assets.

- In iFAMS, depreciation will be automatically calculated based on the in-service date of the asset. B. VA will consider factors such as physical wear and tear and technological change (e.g., obsolescence) when determining estimated useful life and depreciation. C. VA will record depreciation while the asset remains in service. The initial depreciation amount will represent all depreciation accrued from the date when the asset was accepted or placed into service. D. VA will reflect any changes in the estimated useful life or salvage/residual value prospectively, i.e., in the period of change and future periods. No adjustments will be made to previously recorded depreciation or amortization. E. Subsequent Projects. 30 VA will depreciate the cost of an addition or improvement that meets the capitalization criteria as identified in section 090202.02, Subsequent Expenditures - Additions and Improvements, and 090202.04, Severely Damaged or Destroyed Assets. The depreciation expense recorded is determined based upon the useful life of the associated asset as outlined below.

- If the addition or improvement useful life is comparable to the useful life of the associated asset, the addition or improvement is depreciated over the remaining useful life of the associated asset.^31 (^29) Examples may be IRS tables or developed from historical items. (^30) For accounting purposes, an improvement is also referred to as betterment. (^31) Associated Asset refers to the original capitalized building or personal property.