Scarica Operations Management, appunti completi e più Appunti in PDF di Gestione Delle Operations solo su Docsity!

Operations management

Lesson 1 04/10/

Since the industrial revolution, the world has seen remarkable growth in the size and

complexity of organizations. This has created:

- an increasing division of labor and management responsibilities;

- segmentation of the activities within the same organization;

- an ever-growing organization’s dimension.

There are new management problems of increasing complexity.

The goal of operations management, also known as Operations Research, is to apply the

scientific method to investigate and solve problems that concern how to conduct and

coordinate activities (i.e., operations) within an organization. It has been applied to diverse

areas, including:

- Manufacturing;

- Transportation;

- Logistics;

- Financial planning;

- Healthcare, …

It uses big data and the internet of things to improve certain processes and help you in

certain situations.

The process of Problem Solving consists of 6 steps:

- Observe the problem and collect data;

- Construct a mathematical model;

- Validate the mathematical model;

- Interpret the solution to support managerial decision-making;

- Implement the solution;

- Monitor the outcomes.

The Birth of Operations Management:

Despite its roots can be dated back to 1564, the beginning of OM is universally attributed to

the management of military services early in World War I; first by the British and then the US

army.

The problem was to allocate

effectively (management)

scarce resources to military

operations and since then,

OM has been applied to a

wide range of application

areas (e.g., business,

industry, and government).

→ Successful applications of

OM

The goals of this class:

To provide an overview of the main mathematical optimization techniques to support

decision-making, to provide an introduction to problem solving techniques applied to a digital

enterprise, and to provide the basic knowledge regarding some of the software developed

for the solution of optimization model.

The content of the class

- Introduction: operations management, the scientific method, problems and

methodologies.

- Mathematical programming.

- Linear Programming (LP).

- Simplex method.

- Duality.

- Integer linear programming (ILP).

- Problems on graphs: shortest spanning tree, shortest paths.

- Project management.

- Queueing theory.

The exam

No differences between attending and non-attending students.

The exam is written. Length: 1 hour and a half. It contains both exercises and theoretical

questions. It is marked on a scale of 30 (rounded to the nearest integer). To be prepared for

the exam: Follow all lectures, keep the pace. Look at teaching material uploaded on the e-

learning website, contact the teacher. Book: F.S. Hillier, G.J. Lieberman, Introduction to

operations research , Tenth Edition, McGraw Hill Education, 2015 Chapters: 1, 2, 4 [Only

Sect. 4.1, 4.2, 4.3, 4.4, 4.5, 4.6, 4.7], 6, 9 [Only Sect. 9.1, 9.3], 10 [Only Sect. 10.1, 10.2,

10.3, 10.4], 12, 17 [Sections 17.7, 17.8 NOT requested], 22. (The book is not needed if you

follow all classes).

Teacher: Dott. Gianfranco GUASTAROBA, mail: [email protected]

Office hours: Tuesday 3.00PM-4.00PM Office 6B – S. Chiara Building

Meetings can be in person or remotely. In both cases, the student willing to have a meeting

must send an email some days before.

Problem:

Machines: 1. steel; 2. wood; 3. stuffing and assembling.

Products: 1. steel chair; 2. wood chair.

Information is usually in databases.

The first two machines can only work with one type of product,

and we indicate the respective needed time.

1. We need to find decision variables :

1

= number of steel chairs to produce;

2

= number of wood chairs to produce;

2. The objective function is to maximize the expected

profit coming from selling the two products:

Max z = 30𝑥 1

2

Linear optimization models:

- objectives function is linear,

- all constraints are linear

- decision variable can take fractions as values (Kg, acres, Km).

Matrix notation :

min 𝐶 𝑡

𝑥 s.t. 𝐴𝑥 = 𝑏 and 𝑥 ≥ 0.

some software use matrix notations (es. Matlab, which we won’t see in class).

HP : n decision variables and m constraints.

c = [𝑐 1

2

3

, …] (n-dimensional vector; so it contains n elements)

c is the objective function coefficient vector

x = [𝑥 1

2

3

, …] (n-dimensional vector)

x is the obj. fun. decision variables vector

A =

11

12

1 𝑛

2

22

2 𝑛

31

32

𝑚𝑛

mxn matrix; it’s the constraint coefficients matrix

b = [𝑏 1

2

3

, …] RHS (right hand side)

Extended form (which we will use in class):

min z = 𝑐 1

1

2

2

3

3

𝑛

𝑛

s.t. 𝑎 11

1

12

2

1 𝑛

𝑛

1

21

1

22

2

2 𝑛

𝑛

2

𝑚 1

1

𝑚 2

2

𝑚𝑛

𝑛

𝑛

1

2

3

𝑛

Compact form (for software like Lingo, Ampl, Mpl, Gams):

i = 1, 2, …, n decision variables

j = 1, 2, …, m

min 𝑧 =

𝑖

𝑖

𝑛

𝑖= 1

s.t.

𝑖𝑗

𝑖

𝑛

𝑖= 1

𝑗

𝑖

CONVEX SET

✓ DEF. a set “S”∈ ℝ(𝑛) (S contained in R of n dimension, where n is related to the

number of decision variables) is said to be a convex set only if the following

condition is satisfied: 𝑍 = (𝜆𝑥 + ( 1 − 𝜆) ∗ 𝑦) ∈ 𝑆 and this is valid for ∀𝑥, 𝑦 ∈ 𝑆, ∀𝜆 ∈

✓ This condition must be true for every couple of points within the set (so for every

couple of x and y)

Graphical representation of ℝ of n dimension (in this case n = 2)

We can understand if a set in convex thanks to the graphical analysis

Assume that you have a set S1 and a set S2. We look at all the

points contained in s1 and s2 and we take any two points. The

condition must be valid for every couple of points that are inside

the set.

We collect two points, and we look at segments and in particular

at the points included in this segment and we look at x and y too.

If you assume that 𝜆 = 0 then 𝑧 = 𝑦, if you assume that 𝜆 = 1

then 𝑧 = 𝑥, if you assume that lambda is between 0 and 1 then

we are considering the points on the line segment)

✓A set is convex if the line segment between every two points

(or couple of points) is contained inside the set → this

condition is valid for every couple x, y.

On the other hand, you look at S2 the condition is not valid for every couple of points → it is

sufficient that a single couple of point doesn’t respect the condition, to make a set a non-

convex set.

CONVEX FUNCTION

DEF: given a convex set S ⊆ ℝ (n), and a function c: S → ℝ (1) (c from set S to ℝ of

dimension 1 ) → this means that c is a function which associates to one point in the domain S

a value in the range R, and so a real number) then function C is convex on set S if the

following condition is verified:

And that is valid ∀ of x, y ∈ S, ∀𝜆: 0 ≤ 𝜆 ≤ 1

Assume that we have a function c(x) which is a “parabola”. Let’s

take any two points x and y we look at the related value of the

function for those two points, so we obtain c(x) and c(y).

The LEFT-HAND SIDE of the inequality (= 𝑪(𝝀𝒙 + (𝟏 − 𝝀) ∗ 𝒚) is

the value of the function on any point that is on the segment

going from c(x) and c(y) and we indicate it with light blue color.

The RIGHT-HAND SIDE of the inequality is the value of any

point that is straight line segment going from x to y

✓ So, when we identify a function inside a set, the function

is convex if the values of the left-hand side are always

below the values of the right-hand side.

In this graph the inequality is violated because it is not valid for

every couple of points and it is sufficient that only a single

couple of point doesn’t respect the condition, to make the

function NON-CONVEX.

FUNDAMENTAL PROPERTY OF CONVEX PROGRAMMING

❖ Given a problem P , a convex set F (feasibility set), a convex function c(x) on set F

(which is the objective function), the fundamental property of convex programming

states that a local minimum is ALWAYS a global minimum.

Remember that this property is valid if both the set F and the function are

convex (so the assumptions must be valid ).

We assume that we have a convex set F and a convex function c(x). In this

case there is one local solution and by this fundamental property the local

solution is also the global minimum solution

ANOTHER EXAMPLE

Suppose that there are 3 farmland destinations, and we must decide how to use these 3

different lands in order to MAXIMIZE the profit. We have got 3 different production corn,

sugar cane or tomatoes.

We could divide each land in 3 portion or 2 or not divide it.

For land number 1 we have got maximum 400 acres (1 acres = 4.047 square meters) and

we have got a tank containing water with a capacity of 1500 hectoliters. For land number 2

we have got 600 acres and a water tank of 2000 hectoliters. For land number 3 we have 300

acres and water tank of 900 hectoliters.

acres hectoliters

We have got other constraints related to the products:

acres hectoliters Profit

Corn A 700 5 per acre 400x acre

Sugar B 800 4 per acre 300x acre

Tomatoes C 3000 3 per acres 100x acre

In this case we have two indexes:

Index i = 1, 2, 3 and it refers to the land

Index j = A, B, C and it refers to the products

DECISION VARIABLES → in this case they have got two indexes

𝑖𝑗

= number of acres of land i assigned to product j

So, for ex: 𝑥 1 𝐴

= number of acres of land 1 assigned to product A

OBJECTIVE FUNCTION → we calculate the estimated profit from each product and then we

do a summation

So, for corn 𝑧 𝐴

= 400 × (𝑥

1 𝐴

2 𝐴

3 𝐴

) + 300 × (𝑥

1 𝐵

2 𝐵

3 𝐵

) + 100 × (𝑥

1 𝐶

2 𝐶

3 𝐶

The constraints are related to each land:

First constraint related to land 1: 𝑥 1 𝐴

1 𝐵

1 𝐶

Second constraint related to land 2: 𝑥

2 𝐴

2 𝐵

2 𝐶

Third constraint related to land 3: 𝑥

3 𝐴

3 𝐵

3 𝐶

The constraints are also related to the water (we calculate the consumption of water of the

land for each product):

First constraint related to land 1: 5 𝑥 1 𝐴

1 𝐵

1 𝐶

Second constraint related to land 2: 5 𝑥 2 𝐴

2 𝐵

2 𝐶

Third constraint related to land 3: 5 𝑥 3 𝐴

3 𝐵

3 𝐶

Max land per product:

First constraint related to product A: 𝑥 1 𝐴

2 𝐴

3 𝐴

Second constraint related to product B: 𝑥 1 𝐵

2 𝐵

3 𝐵

Third constraint related to product C: 𝑥 1 𝐶

2 𝐶

3 𝐶

Lesson 3 11/10/

General strategy to formulate a mathematical model :

- Identify the indices.

- Identify the data.

- Identify the decision variables.

- Identify and formulate the objective function.

- Identify and formulate the constraints.

Ex 1 – Production optimization:

A pharmaceutical company produces 4 different products: A, B, C and D. The production

cycle consists of three flow lines, referred to as L1, L2, and L3. Each of the product types

must undergo a sequential processing from the 3 lines. The following table shows the

number of man-hours required for the processing of each Kg of product on each line, and

the unit selling price (in € per Kg.) of each product.

For the next month, at least 1000Kg of

product B must be produced, and no more

than 500Kg of product D.

For each product line, the company can choose the number of man-hours to employ.

However, there is a maximum limit of man-hours available each month for each line, and a

unit cost in € per man-hour associated with each line. These values are shown in the

following table.

Formulate a linear programming model that allows to determine the monthly production plan

that maximizes the profit (=revenues – production costs).

Man-hour : estimated unit of measure of the amount of work required to perform a task.

- Identify the indexes:

i = A, B, C, D products

j = L1, L2, L3 lines

- Identify the data:

- A = man-hours per line and product

- C = unit selling price

- b = availability

- d = unit cost

- identify decision variables:

𝐴

= # of kg of A to produce

𝐵

= # of kg of B to produce

𝐶

= # of kg of C to produce

𝐷

= # of kg of D to produce

- net return of bond C = 4.692%

- net return of bond D = 4.048%

- net return of bond E = 3.075%

max 𝑧 = 3 .375%𝑥

𝐴

𝐵

𝐶

𝐷

𝐸

𝐴

𝐵

𝐶

𝐷

𝐸

= total net return

- identify and formulate the constraints (s.t.):

there are two different starting hypotheses:

𝐴

𝐵

𝐶

𝐷

𝐸

= 100000 (Hp: all budget is invested)

𝐴

𝐵

𝐶

𝐷

𝐸

≤ 100000 (Hp: at max invest 100.000€)

𝐵

𝐶

𝐷

≥ 0 , 4 ∗ 100000 amount invested in public bonds

2 𝑥

𝐴

𝐵

+𝑥

𝐶

𝐷

𝐸

100000

≤ 1 , 4 average rating value of investment must

not exceed 1,

𝐴

𝐵

𝐶

𝐷

𝐸

𝐴

𝐵

𝐶

𝐷

𝐸

𝐴

𝐵

𝐶

𝐷

𝐸

(but we can’t put decision variables as a denominator because the mathematical model

wouldn’t be linear anymore).

𝐴

𝐵

𝐶

𝐷

𝐸

Ex 3 – Distribution planning:

A company has 4 distribution centers located in Bologna, Piacenza, Rome, and Verona. The

company must serve 3 customers with the goods currently in stock at these warehouses.

The following table shows the stocks available at each distribution center in tons (t), the

demand of each customer (in tons), and the unit transportation cost (in € per ton) from each

distribution center to each customer.

Formulate a linear programming model to

determine the optimal distribution plan that

minimizes the total transportation cost.

- Identify the indexes:

i = 1, 2, 3, 4 distribution centers

j = C1, C2, C3 customers

- Identify the data:

C (4x3) =

𝑖𝑗

customers demand; 𝑑

𝑗

= general element

stock available at distribution center; 𝑆

𝑖

= general element

1 𝐶 1

1 𝐶 2

1 𝐶 3

2 𝐶 1

2 𝐶 2

2 𝐶 3

3 𝐶 1

3 𝐶 2

3 𝐶 3

4 𝐶 1

4 𝐶 2

4 𝐶 3

- identify decision variables:

𝑖𝑗

= amount of tons sent from the distribution center i to customer j.

- Identify and formulate the objective function:

min 𝑧 = ( 10 𝑥

1 𝑐 1

1 𝑐 2

1 𝑐 3

2 𝑐 1

2 𝑐 2

2 𝑐 3

3 𝑐 1

3 𝑐 2

3 𝑐 3

4 𝑐 1

4 𝑐 2

4 𝑐 3

= total transportation cost from distribution center (dc) 1 + … 2 + …3 + …

- identify and formulate the constraints (s.t.):

demand constraints:

1 𝑐 1

2 𝑐 1

3 𝑐 1

4 𝑐 1

= 325 total tons sent to customer c

1 𝑐 2

2 𝑐 2

3 𝑐 2

4 𝑐 2

= 215 total tons sent to customer c

1 𝑐 3

2 𝑐 3

3 𝑐 3

4 𝑐 3

= 230 total tons sent to customer c 3

Stock availability in each dc:

1 𝑐 1

1 𝑐 2

1 𝑐 3

≤ 120 total amount delivered from dc

2 𝑐 1

2 𝑐 2

2 𝑐 3

≤ 210 total amount delivered from dc 2

3 𝑐 1

3 𝑐 2

3 𝑐 3

≤ 195 total amount delivered from dc 3

4 𝑐 1

4 𝑐 2

4 𝑐 3

≤ 350 total amount delivered from dc 4

𝑖𝑗

≥ 0 i = 1, 2, 3 , 4; j = c1, c2, c

Compact form:

objective function: min 𝑧 = ∑ ∑ 𝑐 𝑖𝑗

𝑖𝑗

𝐶 3

𝑗 = 𝐶 1

4

𝑖 = 1

s.t.:

𝑖𝑗

𝑗

4

𝑖 = 1

(j = c1, c2, c3)

𝑖𝑗

𝑖

𝑐 3

𝑗 =𝑐 1

(i = 1, 2, 3, 4)

𝑖𝑗

Lesson 4 13 /10/

Ex 4 : Portfolio optimization:

A private investor has a capital of € 25,000 available for an investment in the stock market

over the next year. The investor is evaluating the investment in the following 6 stocks. The

expected return for each stock over the next year is shown in brackets.

- Technology: Apple (8%), Intel (6%), Samsung (5%);

- Banks: Intesa (7%), Santander (4%);

- Oil: Eni (2%).

The investor wants that at least 25% of the budget invested in the technology sector is

invested in Apple. Furthermore, he wants that the capital invested in the bank sector must be

at least as much as the capital invested in the technology sector, and that no more than 20%

of the available capital is invested in stocks whose expected return is less than or equal to

5%. Formulate a linear programming model that allows to determine the portfolio of

investments in stocks that maximizes the expected return on the investment.

- Indices:

i = 1, 2, 3, 4, 5, 6 (stocks)

1

2

3

= 65 it’s also correct to say “≥”

1

2

3

≤ 7 NB!

1

2

3

City logistics is concerned with the study and implementation of strategies that aim at

improving the efficiency of freight distribution in urban areas, while mitigating externalities

produced such as congestion and pollution.

In Brescia, there are Hub or Satellites (Ortomercato) where the trucks unload their shipment

and then the products that have to be delivered in the city center (old and narrow streets) are

uploaded on smaller, eco-friendly trucks. The general idea is the same even in London or

Paris, there are more hubs there and it’s important to decide where the trucks should go.

Ex 6: distribution network ( flow model )

A logistics company must organize the transport of goods currently stored in 2 warehouses.

The goods to be transported are of a single type and must be delivered to 2 customers. The

available distribution network is shown in the following figure.

The figure above shows the quantities available

at warehouses 1 and 2, as well as the quantities

demanded by customers A and B. The figure also

shows the possible connections (called arcs),

which represent the possible shipping routes. The

unit cost in € per kilogram (kg) transported along

each arc, as well as the maximum transportable

quantity, are shown next to each arc. Formulate a

linear programming model to determine the

optimal distribution plan that minimizes the total

transportation cost.

Graph : abstract representation of the reality.

Node/vertex : represent a physical location.

Arc : link connecting a pair of nodes, only goes one way. (→ : One way streets)

Edge : link connecting a pair of nodes, but it can go both ways (two ways streets).

- Indices:

1 value for each node

w 1

: warehouse 1

w 2

: warehouse 2

H: hub

CA: customer A

CB: customer B

i = w 1

, w 2

, H, CA, CB

- Decision variables: (how much should be transported over each arc)

x w1, w

: # of kg transported from w 1

to w 2

x w1, H

: # of kg transported from w 1

to H

x w 2 , H

: # of kg transported from w 2

to H

x H, CA

: # of kg transported from H to CA

x H, CB

: # of kg transported from H to CB

x CA, CB

: # of kg transported from CA to CB

x CB, CA

: # of kg transported from CB to CA

- Objective function:

Min 𝑧 = 40 𝑥

𝑤 1

,𝑤 2

𝑤 1

,𝐻

𝑤 2

,𝐻

𝐻,𝐶𝐴

𝐻,𝐶𝐵

𝐶𝐴,𝐶𝐵

𝐶𝐵,𝐶𝐴

= total

transportation cost

- Constraints:

𝑤

1

,𝐻

≤ 500 (maximum capacity)

𝑤

2

,𝐻

𝐻,𝐶𝐴

𝐻,𝐶𝐵

𝐶𝐴,𝐶𝐵

𝐶𝐵,𝐶𝐴

Flow conservation constraint :

𝒊

; ∀𝒊 ∈ 𝑽 (for each node)

𝑤

1

,𝑤

2

𝑤

1

,𝐻

= 500 Total exit w 1

𝑤

2

,𝐻

𝑤

1

,𝑤

2

= 400 Total exit w 2

𝐻,𝐶𝐴

𝐻,𝐶𝐵

𝑤 1

,𝐻

𝑤 2

,𝐻

𝐶𝐴,𝐶𝐵

𝐻,𝐶𝐴

𝐶𝐵,𝐶𝐴

𝐶𝐵,𝐶𝐴

𝐻,𝐶𝐵

𝐶𝐴,𝐶𝐵

𝑤

1

,𝑤

2

𝑤

1

,𝐻

𝑤

2

,𝐻

𝐻,𝐶𝐴

𝐻,𝐶𝐵

𝐶𝐴,𝐶𝐵

𝐶𝐵,𝐶𝐴

≥ 0 (non-negativity constraint)

𝑖

= balance of node i

𝑖

0 (origin flow, strictly positive) w 1

, w 2

𝑖

= 0 (transit node) H

𝑖

< 0 (node consuming the flow, destination) CA, CB

Lesson 5 18 /10/

LP: linear programming problem. All decision variables can take integer fractional values.

Graphical method: LP with 2 decision variables.

Simplex method: LP with any number of decision variables.

Min 𝑧 = 2 𝑥 1

2

S.t.:

1

2

2

1

2

Definition :

Feasible solution = is a solution where all the constraints are satisfied.

Unfeasible solution = is a solution where at least one constraint is violated.

Definition :

Isoline: is a line composed of points, where every point has the same value of the objective

function.

1

2

= 𝑘 k is a parameter chosen by the user.

1

2

1

= 1 and 𝑥

2

1

2

1

= 0 and 𝑥

2

1

2

1

∗= 0 and 𝑥

2

If 𝑘 = 12 , then 𝑧 = 0 − 4 = − 4.

Fundamental theorem of linear programming :

Given a linear programming problem, then one of the following conditions holds:

- there exists at least one optimal vertex;

- problem is infeasible; (feasible region is empty)

- problem is unbounded; (we can improve the objective function value without any limit)

Main implication → the optimal lies at one vertex of the feasible region.

Alternatively:

A = (0,4) 𝑧

𝐴

O = (0, 0) 𝑧

𝐵

B = (6, 0) 𝑧

𝐶

Min 𝑧 = 2 𝑥 1

2

S.t.:

1

2

2

1

2

(Adding a constraint we modify the

feasible region, and in general more

vertices are to be considered)

Graphical method: LP with 2 decision variables

- draw each constraint.

- Identify the feasible region and its vertices.

a) draw the isolines corresponding to the objective function in the direction that

improves its value.

b) move the isolines as much as possible until you fall outside the feasible region.

- Identify the optimal solution (its coordinates) and the corresponding value of the

objective function.

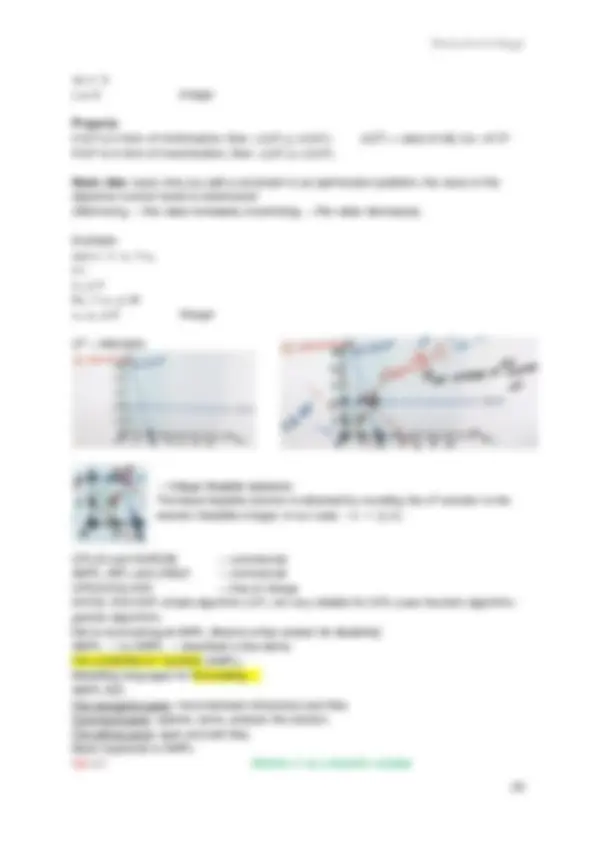

Ex. 1: Graphical method

Solve the following LP model by using the graphical method.

1

2

s.t.:

1

2

1

2

1

2

1

2

To find the isoline:

1

2

1

2

To identify the coordinates of the vertex “D” we have to solve an equation:

1

2

1

2

→ D = (25, 60) → 𝑥

1

∗= 25 and 𝑥

2

𝐷

Ex. 2 : Graphical method

Solve the following LP model by using the graphical method.

1

2

s.t.:

1

2

1

2

1

2

1

2

Let’s assume that now the objective function is different:

Different isoline, different direction of improvement.

In practice this model never happens. We either have a to check our mathematical model or

solution method.

Ex. 5 : Graphical method – infeasible problem

Solve the following LP model by using the graphical method.

1

2

s.t.:

1

2

1

2

1

2

There is no feasible solution that satisfies all the constraints.

In practice, this shouldn’t happen.

Simplex method : LP with any number of variables.

The method was developed in 1947 by George Dantzig, who at that time worked in the U.S.

Army.

Definition :

optimization problem is in standard form if it is:

𝑇

s.t.:

Hp .: m constraints, n decision variables.

c is an n-dimensional vector

x is n-dimensional vector of decision variables

A is an mxn matrix

b is an m-dimensional vector

Assumption: m < n (# of constraints is smaller than the # of decision variables).

If m > n → Ax = b (system of linear equations) has no feasible solution.

If m = n → Ax = b has only one solution x’ = A

b.

- If x’ is also non-negative (≥ 0 ), then the solution is optimal.

- If there is at least one variable that is ≤ 0 the problem is infeasible.

Hiller & Lieberman standard form: (book)

𝑇

𝑥 uses augmented form

s.t.:

Too complicated, we won’t use it.

In general

𝑇

s.t.:

𝐴𝑥 ≥ 𝑏 or 𝐴𝑥 ≤ 𝑏

𝑥 ≥≤ 0 (decision variables could be free, could assume any value)

𝑥 ≤ 0 → almost never happens, sometimes in engineering. We can replace the value with

𝑧 ≥ 0 ; so 𝑥 = −𝑧.

Tricks to get the standard form from a general form:

𝑇

𝑇

1

1

2

2

𝑛

𝑛

𝑛+ 1

≥ 0 (surplus variable)

1

1

2

2

𝑛

𝑛

𝑛+ 1

1

1

2

2

𝑛

𝑛

𝑛+ 1

≥ 0 (slack variable)

1

1

2

2

𝑛

𝑛

𝑛+ 1

𝑗

≥≤ 0 (free); 𝑥

𝑗

𝑗

−

𝑗

𝑗

𝑗

−

Ex.:

1

2

s.t.:

1

2

1

2

2

2

−

1

2

2

−

s.t.:

1

2

2

−

1

2

2

−