menu

3.X

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 1

Summary

5.1 The financial position of the company

5.2 The assets of the company

5.3 The financial statements

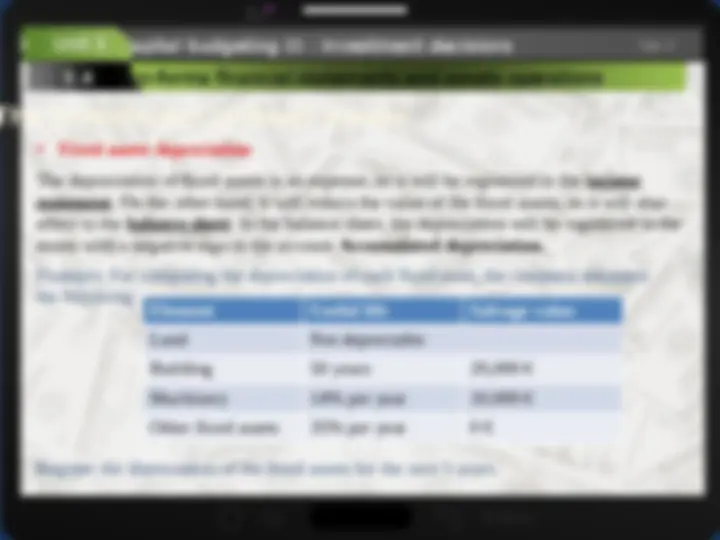

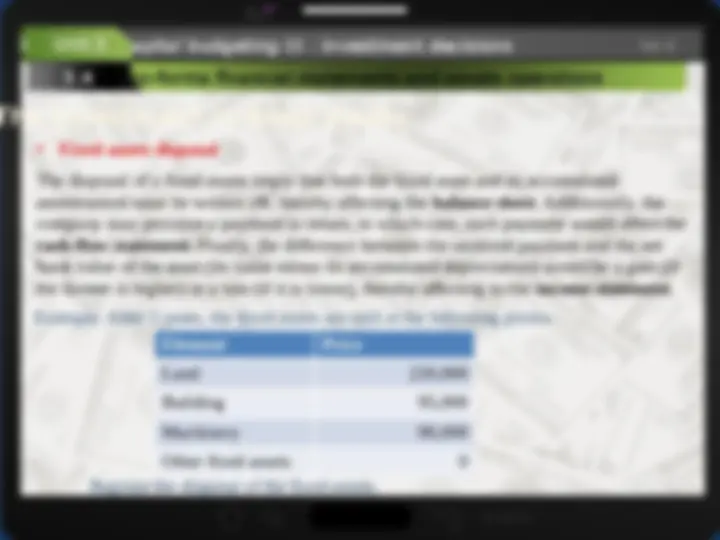

5.4 Pro-forma financial statements and assets operations

Studia grazie alle numerose risorse presenti su Docsity

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

Prepara i tuoi esami

Studia grazie alle numerose risorse presenti su Docsity

Prepara i tuoi esami con i documenti condivisi da studenti come te su Docsity

Trova i documenti specifici per gli esami della tua università

Preparati con lezioni e prove svolte basate sui programmi universitari!

Rispondi a reali domande d’esame e scopri la tua preparazione

Riassumi i tuoi documenti, fagli domande, convertili in quiz e mappe concettuali

Studia con prove svolte, tesine e consigli utili

Togliti ogni dubbio leggendo le risposte alle domande fatte da altri studenti come te

Esplora i documenti più scaricati per gli argomenti di studio più popolari

Ottieni i punti per scaricare

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

An in-depth analysis of the company's assets, focusing on current and fixed assets, and the concept of depreciation and amortization. It also covers the importance of pro-forma financial statements in investment decisions. Students will learn about the classification of assets, the difference between current and fixed assets, and the concept of depreciation and amortization. They will also gain an understanding of how to register the purchase, depreciation, and disposal of fixed assets, as well as the estimation of working capital.

Tipologia: Slide

1 / 32

Questa pagina non è visibile nell’anteprima

Non perderti parti importanti!

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 1

5.1 The financial position of the company

5.2 The assets of the company

5.3 The financial statements

5.4 Pro-forma financial statements and assets operations

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 2

5.1 The financial position of the company

A company can be considered as a succession of investing and financing projects. The

following steps describe how a company works from a financial point of view:

has to raise the needed money by issuing capital or liabilities (debt) , thereby defining the

financial structure of the company. The financial structure of the company , therefore, is the

specific mixture of capital and liabilities a company uses to finance its operations. The company

commits itself to remunerate the fund providers in return.

project. An asset can be defined as any resource with economic value which is expected to

generate future cash-flows.

consequence, other assets of (expected) higher value will arise. For example, if a company

buys a good by 10 € and sell it by 12 €, the company will loose that good (that asset

“disappears” or it is consumed) but, in exchange, it receives a new asset which value is

higher (money or a credit). Therefore, the operations of the company are expected to

increase the value of the assets that belong to the company. The increasing in the value of

the assets of a company in a given period of time is called the Operating Income of that

period.

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 4

5.1 The financial position of the company

Net

Earnings

Net

Earnings

Stockholders

Debtholders

Capital

Capital

As the company does its operations…

Operating

Income

Operating

Income

Interests

Interests

Dividends

Reserves

Reserves

Debt

Debt

Assets

Assets

Assets Assets

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 5

5.1 The financial position of the company

operating income. In this case, by substracting the interests to the operating income we

will get a negative net income, that is a net loss. In this case, the value of the

stockholders equity will decrease.

not receive assets of higher value, but assets of lower value. In this case, the

operations will produce an operating loss. In addition to that loss, the company will

still have to pay the interests to the debtholders, so those interests must be added to the

operating loss to produce an even larger net loss. Again, the value of the stockholders

equity will decrease.

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 7

5.2 The assets of the company

The assets of the company are the investments of that company. That is to say: an asset is

any economic resource controlled by the company which is expected to produce cash-

inflows in the future.

In the development of its operations, the assets of the company will disappear and they will

be replaced by other assets that are expected to be of the same or higher value. The

disappearance of an asset is called the consumption of that asset.

For example, let us consider the case of an industrial company. Its operations would be:

Buys raw materials

Convert raw materials

into finished products

Sell finished

products

Collect the

price

Money disappears

Raw materials appear

Raw materials disappear

Finished products appear

Finished products

disappear

Receivable

appears

Receivable

disappears

Money appears

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 8

5.2 The assets of the company

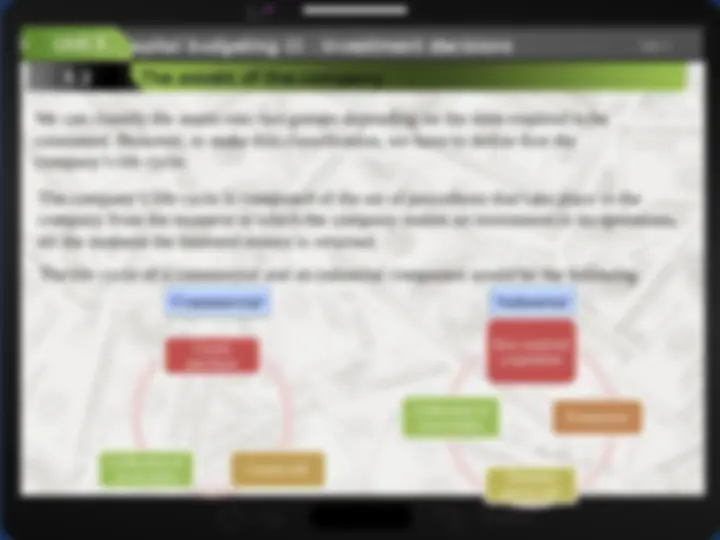

We can classify the assets into two groups depending on the time required to be

consumed. However, to make this classification, we have to define first the

company’s life cycle.

The company’s life cycle is composed of the set of procedures that take place in the

company from the moment in which the company makes an investment in its operations,

till the moment the invested money is returned.

The life cycle of a commercial and an industrial companies would be the following:

Goods

purchase

Goods sell

Collection of

receivables

Commercial

Commercial Industrial

Industrial

Raw material

acquisition

Production

Finished

goods sell

Collection of

receivables

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 10

5.2 The assets of the company

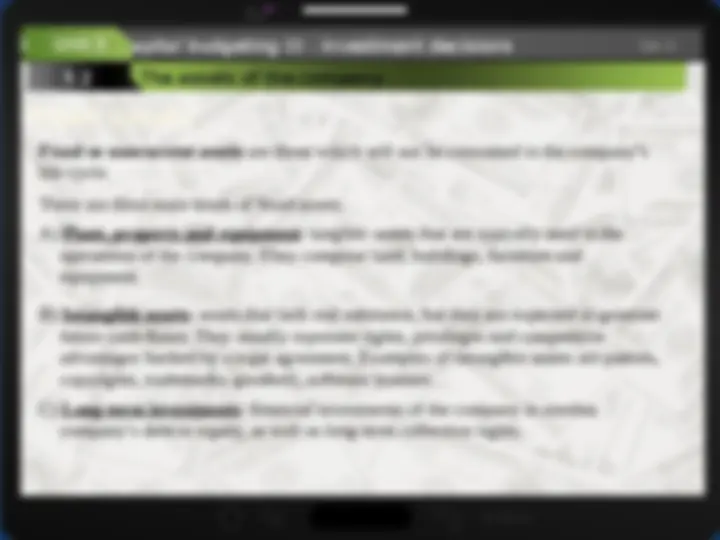

Fixed or noncurrent assets are those which will not be consumed in the company’s

life cycle.

There are three main kinds of fixed assets:

A) Plant, property and equipment : tangible assets that are typically used in the

operations of the company. They comprise land, buildings, furniture and

equipment.

B) Intangible assets : assets that lack real substance, but they are expected to generate

future cash-flows. They usually represent rights, privileges and competitive

advantages backed by a legal agreement. Examples of intangible assets are patents,

copyrights, trademarks, goodwill, software licenses…

C) Long-term investments : financial investments of the company in another

company’s debt or equity, as well as long-term collection rights.

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 11

5.2 The assets of the company

Long-term invested will be consumed as the collection rights are fulfilled. Real

fixed assets (that is, those which are tangible or untangible assets), however, will be

consumed in the operations of the company, although they will not be fully

consumed in one single life cycle, but in various life cycles.

The partial consumption of the value of the fixed asset occurred in a period of time

is called depreciation (in the case of tangible assets) or amortization (in the case of

intangible assets).

Not all the tangible assets, however, are depreciated: land assets are not depreciated

because it is assumed to have an unlimited useful life, that is to say, it would be

consumed in infinitum life cycles.

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 13

5.2 The assets of the company

Example: the cost value of a car is 30,000 €. The company estimates that this car wil be

used during 4 years, being sold after that time by 5,000 €. Estimate the annual

depreciation of this car.

Useful life: 4 years

Depreciation basis:

Annual depreciation:

Example: the cost value of a car is 30,000 €. The company estimates that this car wil be

used until it has run 300,000 Km, being then sold by 5,000 €. If the car has run 130,

Km this year, estimate the depreciation for this year.

Useful life: 300,000 Km

Depreciation basis:

Depreciation per Km:

Depreciation for this year:

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 14

5.3 The financial statements

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 16

5.3 The financial statements

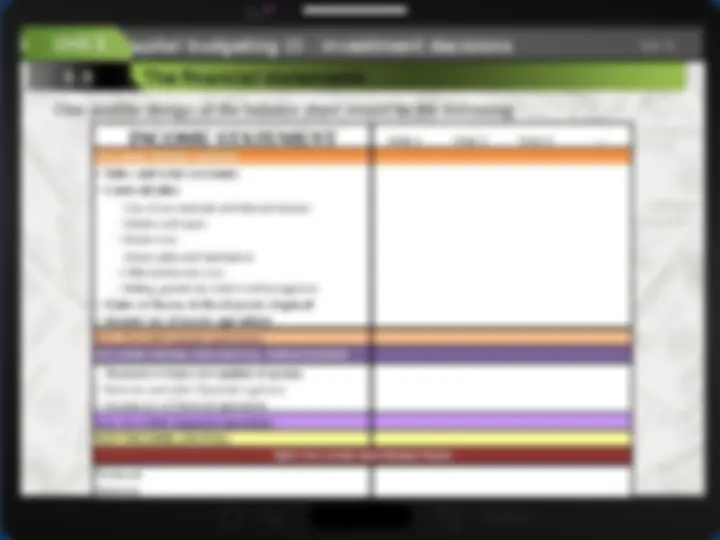

A possible design of the balance sheet from the point of view of accounting would be:

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 17

5.3 The financial statements

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 19

5.3 The financial statements

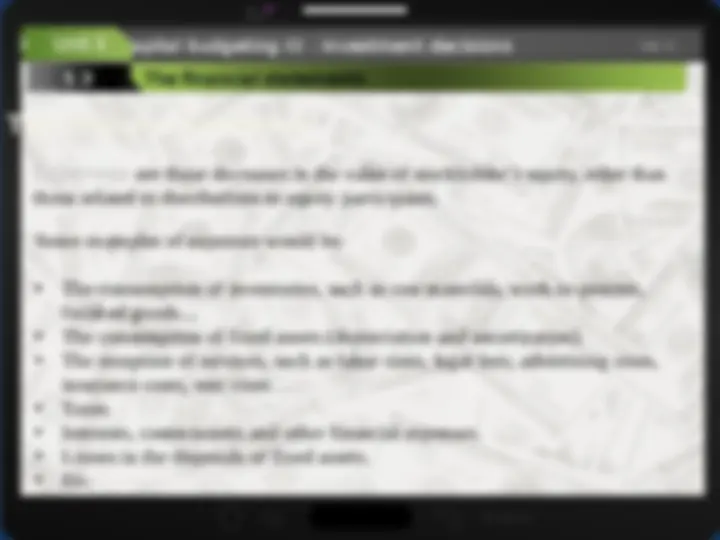

Most income is related to assets operations. The sales revenue, the gains in the

disposal of fixed assets, or the revenues and gains on their financial investments are

income related to the investments of the company.

Income from financial operations is much less usual. The only example we will

study is the periodic recognition of the income generated by a grant.

Expenses related to assets operations are all those expenses the company has to incur

to produce and sell its products. For instance, the consumption of inventories,

depreciation, wages and salaries, services, losses in assets disposals….

Financial-related expenses are the interests paid for the money the company

borrows, as well as the commissions, fees and other costs associated to the liabilities

operations.

zoom

Capital budgeting (I) : investment decisions

X Unit 5 Slide 20

5.3 The financial statements

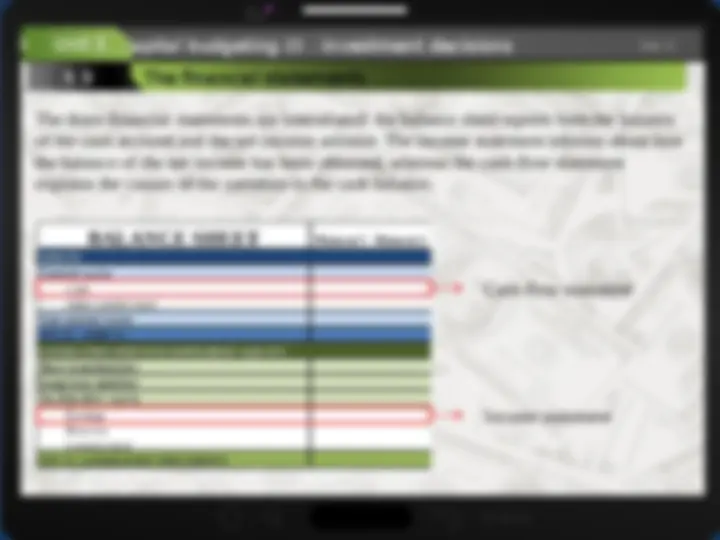

One posible design of the balance sheet would be the following: