Download 53794 chapter 1 and more Thesis Accounting in PDF only on Docsity!

chapter 1 Fundamentals of Strategic Management (^1) 1

c h a p t e r 1

Fundamentals of

Strategic Management

W

hat do Circuit City, Washington Mutual, Saab, Blockbuster, and Borders have in common? All of these recognized companies filed for bankruptcy during the past several years. While the situation surrounding each firm is different, all of them failed to meet various strategic challenges. Put another way, organizations typically do not succeed or fail randomly. Some plan, prepare, and execute more effectively than others. Today’s business world is global, Internet-driven, and obsessed with speed. The challenges it creates for strategic managers are often complex, ambiguous, and unstructured. Add to this the incessant allegations of top management wrongdoings, economic stagnation, and increas- ing executive compensation, and it is easy to see why firm leaders are under great pressure to respond to strategic problems quickly, decisively, and responsibly. Indeed, the need for effec- tive strategic management has never been more pronounced. This text presents a framework for addressing today’s strategic challenges. This chapter introduces the notion of strategic management, highlights its importance, and presents a five-step process for strategically analyzing an organization. The remaining chapters expand on the various steps in the process with special emphasis on their application to ongo- ing enterprises.

What Is Strategic Management? ________________

Organizations exist for a purpose. The mission is articulated in a broadly defined but enduring statement of purpose that identifies the scope of an organization’s operations and its offerings to affected groups and entities. Most organizations of a significant size or stature have developed a formal mission statement, a concept discussed further in Chapter 5. Strategy refers to top management’s plans to develop and sustain competitive advantage —a state whereby a firm’s successful strategies cannot be easily duplicated by its 1

2 STRATEGIC MANAGEMENT

competitors^1 —so that the organization’s mission is fulfilled.^2 Following this definition, it is assumed that an organization has a plan, its competitive advantage is understood, and its members understand the reason for its existence. These assumptions may appear self-evident, but many strategic problems can be traced to fundamental misunderstandings associated with defining the strategy. Debates over the nature of the organization’s competitive advantage, its mission, and whether or not a strategic plan is really needed can be widespread.^3 As such, com- ments such as “We’re too busy to focus on developing a strategy” or “I’m not exactly sure what my company is really trying to accomplish” can be overheard in many organizations. Strategic management is a broader term than strategy and is a process that includes top management’s analysis of the environment in which the organization operates prior to formulat- ing a strategy, as well as the plan for implementation and control of the strategy. The difference between a strategy and the strategic management process is that the latter includes considering what must be done before a strategy is formulated through assessing whether or not the success of an implemented strategy was successful. The strategic management process can be sum- marized in five steps, each of which is discussed in greater detail in subsequent chapters of the book (see Figure 1.1):^4

- External Analysis: Analyze the opportunities and threats, or constraints, that exist in the organization’s external environment, including industry and forces in the external environment.

- Internal Analysis: Analyze the organization’s strengths and weaknesses in its internal environment. Consider the context of managerial ethics and corporate social responsibility.

- Strategy Formulation: Formulate strategies that build and sustain competitive advantage by matching the organization’s strengths and weaknesses with the environment’s opportunities and threats.

- Strategy Execution: Implement the strategies that have been developed.

- Strategic Control: Measure success and make corrections when the strategies are not producing the desired outcomes. The sequential order of the steps is logical. A thorough understanding of the organization and its environment is essential if the appropriate strategy is to be developed, put into action, and controlled. One could transpose the first two steps and analyze the internal environment before the external environment—the logic being that comprehending the organization informs the strategic assessment of factors outside of the firm. The external environment is analyzed before the internal environment in Figure 1.1, however, because internal goals, resources, and competencies are viewed in a relative fashion to some extent and are understood within the context of the industry and the factors that drive it. This dilemma resembles the chicken and egg argument; in a practical sense, external and internal analysis often occurs simultaneously. A distinction between outside and inside perspectives on strategy is also relevant. Outsiders analyzing a firm should apply a systematic approach that progresses through these steps in order. Doing so develops a holistic understanding of the firm, its industry, and its strategic challenges. Inside organizations, strategies are being formulated, implemented, and controlled simulta- neously while external and internal factors are continually reassessed. In addition, changes in one stage of the strategic management process will inevitably affect other stages as well. After a planned strategy is implemented, it often requires modification as conditions change. Hence, because these steps are so tightly intertwined, insiders tend to treat all of the steps as a single integrated, ongoing process.^5

4 STRATEGIC MANAGEMENT

Consider the razor and blades business model invented by Gillette. A company gives away or deeply discounts a product—the razor—while planning to profit from future sales of required replacement or complementary products—the blades. Cell phones are often given to customers willing to sign a 2-year service contract. Computer printers are typically sold below production cost, but customers must periodically replace the ink cartridges, which are high-margin items. This model is not foolproof, however. In a competitive marketplace, customers may be able to purchase the required complementary products at lower prices from rivals not under pressure to recoup initial losses. Successful business models can change over time. Since the early 2000s, a number of authors have strayed from the traditional business model whereby book publishers offer con- tracts and pay royalties of 10% to 15%. Leveraging advances in publishing software, social media, and a strong online retail book market, they have opted for a self-publishing model. Enterprising authors who publish their own work also shoulder the initial risk but can net as much as a 70% return on e-book sales from companies such as Amazon.com. The total print book and e-book output of self-publishers in the United States rose from about 50,000 titles in 2006 to over 125,000 in 2010.^6 While a successful strategy is built on the firm’s business model, crafting one can be a chal- lenge. Realistically, a number of factors are typically associated with successful strategies. Some of these factors including the following:

- The organization’s competitive environment is well understood, in detail.

- Strengths and weaknesses are assessed in a thorough and realistic manner.

- The strategy is consistent with the mission and goals of the organization.

- Plans for putting the strategy into action are designed with specificity before it is implemented.

- Possible future changes in the proposed strategy—a process called strategic control—are evaluated before the strategy is adopted. Careful consideration of these factors reinforces the interrelatedness of the steps in the strategic management process. Each factor is most closely associated with one of the five steps, yet they fit together like pieces of a puzzle. The details associated with the success factors—and others—will be discussed in greater detail in subsequent chapters. While some of these success factors are associated with the competitive environment in profit-seeking firms, strategic management is not limited to for-profit organizations. Top manag- ers of any organization, regardless of profit or nonprofit status, must understand the organiza- tion’s environment and its capabilities and develop strategies to assist the enterprise in attaining its goals. Former Drexel University president Constantine Papadakis, for example, was widely considered to be a leading strategic thinker among university top executives. The innovative Greek immigrant promoted Drexel through aggressive marketing, while campaigning for an all- digital library without books. In many respects, he managed the university in the same way that other executives manage profit-seeking enterprises. His annual salary was close to $1,000,000 in the years preceding his death in 2009, making him one of the highest paid university presidents in the country.^7

Intended and Realized Strategies

One of the most critical challenges facing organizations is the reality that strategies are not always implemented as originally planned. Sometimes strategic decisions seem to evolve. In this respect, strategy formulation can be seen as an iterative process where decision

chapter 1 Fundamentals of Strategic Management (^5) makers take actions, make sense of those actions afterward, and then decide how to proceed. Henry Mintzberg introduced two terms to help clarify the shift that often occurs between the time a strategy is formulated and the time it is implemented. An intended strategy (i.e., what management originally planned) may be realized just as it was planned, in a modified form, or even in an entirely different form. Occasionally, the strategy that management intends is actually realized, but the intended strategy and the realized strategy —what management actually implements—usually differ.^8 Hence, the original strategy may be realized with desirable or undesirable results, or it may be modified as changes in the firm or the environment become known. The gap between the intended and realized strategies usually results from unforeseen envi- ronmental or organizational events, better information that was not available when the strat- egy was formulated, or an improvement in top management’s ability to assess its environment. Although it is important for managers to formulate responsible strategies based on a realistic and thorough assessment of the firm and its environment, things invariably change along the way. Hence, it is common for such a gap to exist, creating the need for constant strategic action if a firm is to stay on course. Instead of resisting modest strategic changes when new information is discovered, managers should search for new information and be willing to make such changes when necessary. This activity is part of strategic control—the final step in the strategic manage- ment process.

Scientific and Artistic Perspectives on

Strategic Management

There are two different perspectives on the approach that top executives should take to strate- gic management. Most strategy scholars have endorsed a scientific perspective , whereby strategic managers are encouraged to systematically assess the firm’s external environment and evaluate the pros and cons of myriad alternatives before formulating strategy. The business environ- ment is seen as largely objective, analyzable, and largely predictable. As such, strategic manag- ers should follow a systematic process of environmental, competitive, and internal analysis and build the organization’s strategy on this foundation. According to this perspective, strategic managers should be trained, highly skilled analytical thinkers capable of digesting a myriad of objective data and translating it into a desired direction for the firm. Strategy scientists tend to minimize or reject altogether the role of imagination and creativity in the strategy process and are not generally receptive to alternatives that emerge from any process other than a comprehensive, analytical approach. Others have a different view. According to the artistic perspective on strategy, the lack of environmental predictability and the fast pace of change render elaborate strategy planning as suspect at best. Instead, strategists should incorporate large doses of creativity and intuition in order to design a comprehensive strategy for the firm.^9 Henry Mintzberg’s notion of a crafts- man—encompassing individual skill, dedication, and perfection through mastery of detail— embodies the artistic model. The strategy artist senses the state of the organization, interprets its subtleties, and seeks to mold its strategy like a potter molds clay. The artist visualizes the outcomes associated with various alternatives and ultimately charts a course based on holistic thinking, intuition, and imagination.^10 Strategy artists may even view strategic planning exercises as time poorly spent and may not be as likely as those in the science school to make the effort necessary to maximize the value of a formal planning process.^11 This text acknowledges the artistic perspective but emphasizes the science view. Creativity and innovation are important and encouraged but are most likely to translate into organizational success when they occur as part of a comprehensive, systematic approach to strategic manage- ment. Nonetheless, the type of formal strategic planning proposed in this text is not without its

chapter 1 Fundamentals of Strategic Management (^7) firm deviates from the industry norm and implements a new, successful strategy, other firms will rapidly mimic the higher-performing firm by purchasing the resources, competencies, or management talent that have made the leading firm so profitable. Hence, although the IO per- spective emphasizes the industry’s influence on individual firms, it is also possible for firms to influence the strategy of rivals and in some cases even modify the structure of the industry.^17 Perhaps the opposite of the IO perspective, resource-based theory views performance primarily as a function of a firm’s ability to utilize its resources.^18 Although environmental oppor- tunities and threats are important, a firm’s unique resources comprise the key variables that allow it to develop a distinctive competence , enabling the firm to distinguish itself from its rivals and create competitive advantage. Resources include all of a firm’s tangible and intangible assets, such as capital, equipment, employees, knowledge, and information.^19 An organization’s resources are directly linked to its capabilities, which can create value and ultimately lead to profitability for the firm.^20 Resource-based theory focuses primarily on individual firms rather than on the competitive environment. If resources are to be used for sustained competitive advantage —a firm’s ability to enjoy strategic benefits over an extended period of time—those resources must be valuable, rare, not subject to perfect imitation, and without strategically relevant substitutes.^21 Valuable resources are those that contribute significantly to the firm’s effectiveness and efficiency. Rare resources are possessed by only a few competitors, and imperfectly imitable resources cannot be fully duplicated by rivals. Resources that have no strategically relevant substitutes enable the firm to operate in a manner that cannot be effectively imitated by others and thereby sustain high performance. According to the third perspective, contingency theory , the most profitable firms develop beneficial fits with their environments. In other words, a strategy is most likely to be success- ful when it is consistent with the organization’s mission, its competitive environment, and its resources. Contingency theory represents a middle ground perspective that views organiza- tional performance as the joint outcome of environmental forces and the firm’s strategic actions. Firms can become proactive by choosing to operate in environments where opportunities and threats match the firms’ strengths and weaknesses.^22 Should the industry environment change in a way that is unfavorable to the firm, its top managers should consider leaving that industry and reallocating its resources to other, more favorable industries. Differences aside, each perspective has merit and has been incorporated into the strategic management process laid out in this text. The IO view is seen in the industry analysis phase, most directly in Michael Porter’s five forces model. Resource-based theory is applied directly to the internal analysis phase and the effort to identify an organization’s resources that could lead to sustained competitive advantage. Contingency theory is seen in the strategic alternative generation phase, where alternatives are developed to improve the organization’s fit with its environment. Hence, multiple perspectives are critical to a holistic understanding of strategic management.^23

Corporate Governance and Boards of Directors ____

A small business is often governed by one or several individuals well known to everyone in the organization. Ownership is often privately held and may rest with a single person, a family, or a few business partners. Because more resources are needed, many midsize and large organizations are publicly held , with shares of stock available for purchase on exchanges such as the New York Stock Exchange. In public corporations, shareholders—the owners of the firm—are represented by an elected board of directors legally authorized to monitor firm activities as well as the selection, evaluation, and compensation of top managers. Strategic

8 STRATEGIC MANAGEMENT

decision making in these firms is more complex because the ownership is widely dispersed and often changes frequently. Corporate governance refers to the board of directors, institutional investors (e.g., pen- sion and retirement funds, mutual funds, banks, insurance companies, among other money managers), and large shareholders known as blockholders who monitor firm strategies to ensure effective management. Boards of directors and institutional investors—representatives of pension and retirement funds, mutual funds, and financial institutions—are generally the most influential in the governance systems. Because institutional investors own more than half of all shares of publicly traded firms, they tend to wield substantial influence. Blockholders tend to hold less than 20% of the shares, so their influence is proportionally less than that of institutional investors.^24 Boards of directors often include both inside (i.e., firm executives) and outside direc- tors. Insiders bring company-specific knowledge to the board whereas outsiders bring independence and an external perspective. Over the past several decades, the compo- sition of the typical board has shifted from one controlled by insiders to one controlled by outsiders. This increase in outside influence often allows board members to oversee managerial decisions more effectively.^25 Moreover, when additional outsiders are added to insider-dominated boards, dismissal of the chief executive officer (CEO) is more likely when corporate performance declines^26 and outsiders are more likely to pressure for corpo- rate restructuring.^27 A number of companies became concerned about both potential conflicts of interest and the amount of time a board member who sits on multiple boards can spend with the affairs of each company. As a result, many companies have begun to limit the number of board memberships their own board members may hold. Approximately two-thirds of corporate board members at the largest 1,500 U.S. companies do not hold seats on other boards. The average director’s direct compensation ranged from $90,775 at firms with revenues between $50 million and $500 mil- lion to $228,058 at the 200 largest firms in the Standard & Poor’s 500 based on revenue.^28 The Sarbanes-Oxley Act , which was passed in 2002, requires firms to include more inde- pendent directors on their boards and make disclosures on internal controls, ethics codes, and the composition of their audit committees on annual reports. The act requires that both the CEO and the chief financial officer (CFO) certify every report that contains company financial state- ments. It restricts membership of the firm’s audit committee—the formal group charged with reporting oversight—to outsiders (i.e., board members who are not managers). Sarbanes-Oxley also prohibits firms from extending personal loans to board members or executives. Even with new disclosure regulations, however, it can be difficult to determine precisely what top executives earn at public companies. A number of analysts have noted positive changes among boards as a result of this legislation in terms of both independence and expertise, while others contend that government regulations like Sarbanes-Oxley have merely added more costly paperwork.^29 A record number of public firms went private in the mid- 2000s primarily due to investor and management frustration with the legislation. Evidence also suggests that many CEOs have become more reluctant to sit on boards of publicly held companies. Increased liability on the part of board members and recent policy changes that often restrict the number of outside boards on which a CEO may serve have also contributed to this change.^30 Boards of directors are responsible for monitoring activities in the organization, evaluat- ing top management’s strategic proposals, and establishing the broad strategic direction for the firm. As such, boards select and terminate the CEO, establish his or her compensation package, advise top management on strategic issues, and monitor managerial and company performance as representatives of the shareholders. Critics charge that board members do not always fulfill their legal roles.^31 One reason is that they are nominated by the CEO, who expects them to

10 STRATEGIC MANAGEMENT

Criticism notwithstanding, some board members have played effective stewardship roles. Many directors promote strongly the best interests of the firm’s shareholders and various other stakeholder groups as well. Research indicates, for instance, that board members are often invaluable sources of environmental and competitive information.^36 By conscientiously carrying out their duties, directors can ensure that management remains focused on company performance.^37 A number of recommendations have been made on how to promote an effective gover- nance system. For example, it has been suggested that outside directors be the only ones to evaluate the performance of top managers against the established mission and goals, that all outside board members should meet alone at least once annually, and that boards of directors should establish appropriate qualifications for board membership and communicate these qual- ifications to shareholders. For institutional shareholders, it is recommended that institutions and other shareholders act as owners and not just investors,^38 that they not interfere with day-to-day managerial decisions, that they evaluate the performance of the board of directors regularly,^39 and that they should recognize that the prosperity of the firm benefits all shareholders.

Strategic Decisions ___________________________

How does one think and act strategically, and who makes the strategic decisions? The answers to these questions vary across firms and may also be influenced by ownership and other issues related to corporate governance. It is also important to distinguish between strategic decisions and common management decisions. In general, strategic decisions are marked by four key distinctions:

- They are based on a systematic, comprehensive analysis of internal attributes and factors external to the organization. Decisions that address only part of the organization—perhaps a single functional area—are usually not considered to be strategic decisions.

- They are long-term and future-oriented but are built on knowledge about the past and present. Scholars and managers do not always agree on what consti- tutes the long term, but most agree that it can range anywhere from several years in duration to more than a decade.

- They seek to capitalize on favorable situations outside the organization. In gen- eral, this means taking advantage of opportunities that exist for the firm, but it also includes taking measures to minimize the effects of external threats as well.

- They involve choices. Although making win-win strategic decisions may be pos- sible, most involve some degree of trade-off between alternatives—at least in the short run. For example, raising salaries to retain a skilled workforce can increase wages and adding product features or enhancing quality can increase the cost of production. However, such trade-offs may diminish in the long run, as a more skilled, higher paid workforce may be more productive than a typical workforce, and sales of a higher-quality product may increase, thereby raising sales and potentially profits. Decision makers must understand these complex relation- ships across the business spectrum. Because of these distinctions, strategic decision making is generally reserved for the top executive and members of his or her top management team. The CEO is the individual ultimately responsible (and generally held responsible ) for the organization’s strategic management, but he or she rarely acts alone. Except in the smallest companies, he or she relies on a team of top-level executives—including members of the board of directors, vice presidents, and even various line and staff managers in some instances—all of whom play

chapter 1 Fundamentals of Strategic Management (^11) instrumental roles in strategically managing the firm. Generally speaking, the quality of strategic decisions improves dramatically when more than one capable executive participates in the process.^40 The size of the team on which the top executive relies for strategic input and support can vary from firm to firm. Companies organized around functions such as marketing and production generally involve the heads of the functional departments in strategic decisions. Very large organizations often employ corporate- level–strategic-planning staffs and outside consultants to assist top executives in the process. The degree of involvement of top and middle managers in the strategic management process also depends on the personal philosophy of the CEO.^41 Some CEOs are known for making quick decisions whereas others have a reputation for involving a large number of top managers and others in the process. Input to strategic decisions, however, need not be limited to members of the top manage- ment team. To the contrary, obtaining input from others throughout the organization, either directly or indirectly, can be quite beneficial. In fact, most strategic decisions result from the streams of inputs, decisions, and actions of many people. The top management team might cre- ate the context for strategic decisions by establishing rules and procedures and by influencing the informal means through which things are accomplished in the organization. Strategic deci- sions do not necessarily start with top management action, however, but instead can bubble up from a series of lower level decisions throughout the firm. For example, an employee in a company’s research and development department may attend a trade show where a new prod- uct or production process idea that seems relevant to the company is discussed. The employee may relate the idea to his or her manager, who, in turn, may modify and pass it along to his or her manager. Eventually, a version of the idea may be discussed with the organization’s market- ing and production managers and later presented to top management. Ultimately, the CEO will decide whether or not to incorporate the idea into the ongoing strategic planning process. This example illustrates the indirect involvement of individuals throughout the organization in the prison strategic management process. Top management is ultimately responsible for the final decision, but its decision is based on a culmination of the ideas, creativity, information, and analyses of others^42 (see Strategy at Work 1.1). While participation can be healthy, most firms place significant limits of the say that their managers have in strategic decisions. There are a few exceptions, however. At Ternary Software, for example, all of its 13 employees must agree before a strategic decision can be implemented. Such democracy is easier to implement in larger organizations, but even large companies like Google have taken steps to create an egalitarian culture for decision making.^43 The corporate boardroom is often a place where decisions that have already been made in a less formal setting are confirmed. A formal, systematic decision-making process is often applied as a means of confirming what top executives already see as the appropriate course of action. A danger associated with this type of approach is that it tends to jump straight to a proposed solution without considering how a decision should be made. Although there are no guarantees, top man- agement teams that circumvent a logical decision-making approach are more susceptible to mis- takes. For example, when a systematic cost-benefit analysis is not employed, leaders may confuse actual costs of a decision with sunk costs—those already expended—which is a common error that distorts decision making and can lead to an escalation of commitment to a failed strategy.^44

chapter 1 Fundamentals of Strategic Management (^13)

Summary

Top managers face more complex strategic challenges today than ever before. Strategic management involves analysis of an organization’s external and internal environments, formulation and implementation of its strategic plan, and strategic control. These steps in the process are interrelated and typically done simultaneously in many firms. A firm’s intended strategy often requires modification before it has been fully implemented due to changes in environ- mental and/or organizational conditions. Because these changes are often difficult to predict, substantial changes in the envi- ronment may transform an organization’s realized strategy into one that is quite different from its intended strategy. The strategic management field has been influenced by such perspectives as IO theory, resource-based theory, and con- tingency theory. Although they are based on widely varied assumptions about what leads to high performance, each of these perspectives has merit and contributes to an overall understanding of the field. Strategy formulation is the direct responsibility of the CEO, but he or she relies on a team of other individuals as well, including the board of directors, vice presidents, and other various managers. In its final form, a strategic decision is crafted from the streams of input, decisions, and actions of the entire top management team.

Key Terms

Blockholders: Large shareholders who monitor firm strategies to ensure effective management. Business Model: The economic mechanism by which a business hopes to sell its goods or services and generate a profit. CEO Duality: A situation in which the CEO also serves as the chair of the board. Comparative Advantage: The idea that certain products may be produced more cheaply or at a higher quality in particular countries due to advantages in labor costs or technology. Competitive Advantage: A state whereby a business unit’s successful strategies cannot be easily duplicated by its competitors. Contingency Theory: A view that states the most profitable firms are likely to be the ones that develop the best fit with their environment. Corporate Governance: The board of directors, institutional investors, and blockholders who monitor firm strategies to ensure managerial responsiveness. Distinctive Competence: Unique resources, skills, and capabilities that enable a firm to distinguish itself from its competitors and create competitive advantage. Hedge Fund: An investment fund open to only a small number of investors but permitted by regulators to undertake riskier and more speculative investments. The first step in analyzing a firm is to develop familiarity with the organization. Analyzing an ongoing enterprise begins with a general introduction and understanding of the firm. When was the organization founded, why, and by whom? Is any unusual history associated with the organization? Is it privately or publicly held? What is the company’s mission? Has the mission changed since its inception? It is also important at this point to identify the business model on which the organization’s success is predicated. In other words, what is the profit-generating idea behind the company? Determining this information is simple for some companies (Ford, for example, hopes to sell cars and offer consumer financing at a profit) but may be complicated for others where revenue streams and competitive advantage are more difficult to identify.

Case Analysis 1.1 Step 1: Introduction of the Organization

14 STRATEGIC MANAGEMENT

Industrial Organization (IO): A view based in microeconomic theory that states firm profitability is most closely associated with industry structure. Intended Strategy: The original strategy top management plans and intends to implement. Mission: The reason for an organization’s existence. The mission statement is a broadly defined but enduring statement of purpose that identifies the scope of an organization’s operations and its offerings to affected groups (i.e., stakeholders, as defined later in the book). Realized Strategy: The strategy top management actually implements. Resource-Based Theory: The perspective that views performance primarily as a function of a firm’s ability to utilize its resources. Sarbanes-Oxley Act: Legislation passed in 2002 that created more detailed reporting requirements for boards and executives in public U.S. companies and accounting firms. Strategic Management: The continuous process of determining the mission and goals of an organization within the context of its external environment and its internal strengths and weaknesses, formulating and implementing strategies, and exerting strategic control to ensure that the organization’s strategies are successful in attaining its goals. Strategy: Top management’s plans to attain outcomes consistent with the organization’s mission and goals. Sustained Competitive Advantage: A firm’s ability to enjoy strategic benefits over an extended period of time. Top Management Team: A team of top-level executives—headed by the CEO—all of whom play instrumental roles in the strategic management process.

Review Questions and Exercises

- Identify a company with a published mission statement on its website. Evaluate its mission statement along each of the following criteria: a. Is the mission statement comprehensive? Is it concise? b. Does the mission statement delineate in broad terms what products or services the firm is to offer? c. Is the mission statement consistent with the company’s actual activities and competitive prospects?

- Is it necessary that the five steps in the strategic management process be performed sequentially? Why or why not?

- What is the difference between an intended strategy and a realized strategy? Why is this distinction important?

- How have outside perspectives influenced the development of the strategic management field?

- Does the CEO alone make the strategic decisions for an organization? Explain.

Practice Quiz

True or False?

- A strategy seeks to develop and sustain competitive advantage.

- Strategic management refers to formulating successful strategies for an organization.

- Each step in the strategic management process is independent so that changes in one step will not substantially affect other steps.

- The intended strategy and the realized strategy can never be the same.

16 STRATEGIC MANAGEMENT

Notes

- I. M. Cockburn, R. M. Henderson, and S. Stern, “Untangling the Origins of Competitive Advantage,” Strategic Management Journal 21 (2000): 1123–1145.

- P. Wright, M. Kroll, and J. A. Parnell, Strategic Management: Concepts (Upper Saddle River, NJ: Prentice Hall, 1998).

- D. C. Hambrick and J. W. Fredrickson, “Are You Sure You Have a Strategy?” Academy of Management Executive 15 (2001): 48–59.

- Based on Wright et al., Strategic Management.

- A. E. Singer, “Strategy as Moral Philosophy,” Strategic Management Journal 15 (1994): 191–213.

- J. A. Trachtenberg, “Secrets of Self-Publishing: Success,” Wall Street Journal , October 31, 2011, B1, B7.

- B. Wysocki Jr., “How Dr. Papadakis Runs a University Like a Company,” Wall Street Journal , February 23, 2005, A1; P. Fain, “High Pay Makes Headlines,” Chronicle of Higher Education Online Edition , November 24, 2006.

- H. Mintzberg, “Opening Up the Definition of Strategy,” in The Strategy Process, eds. J. B. Quinn, H. Mintzberg, and R. M. James (Englewood Cliffs, NJ: Prentice Hall, 1988), 14–15.

- C. M. Ford and D. M. Gioia, “Factors Influencing Creativity in the Domain of Managerial Decision Making,” Journal of Management 26 (2001): 705–732.

- H. Mintzberg, “Crafting Strategy,” Harvard Business Review 65, no. 4 (1987): 66–75.

- G. Hamel, “Strategy as Revolution,” Harvard Business Review 74, no. 4 (1996): 69–82; B. Huffman, “What Makes a Strategy Brilliant?” Business Horizons 44, no. 4 (2001): 13–20.

- H. Courtney, J. Kirkland, and P. Viguerie, “Strategy under Uncertainty,” Harvard Business Review 75, no. 6: 67–79.

- G. Hamel, “Strategy as Revolution”; B. Hoffman, “What Makes a Strategy Brilliant?” Business Horizons (July–August 2001): 13–20.

- M. E. Porter, “The Contributions of Industrial Organization to Strategic Management,” Academy of Management Review 6 (1981): 609–620.

- G. Hawawini, V. Subramanian, and P. Verdin, “Is Performance Driven by Industry- or Firm-Specific Factors? A New Look at the Evidence,” Strategic Management Journal 24 (2003): 1–16.

- J. S. Bain, Industrial Organization (New York: Wiley, 1968); F. M. Scherer and D. Ross, Industrial Market Structure and Economic Performance (Boston: Houghton-Mifflin, 1990).

- A. Seth and H. Thomas, “Theories of the Firm: Implications for Strategy Research,” Journal of Management Studies 31 (1994): 165–191; J. B. Barney, “Strategic Factor Markets: Expectations, Luck, and Business Strategy,” Management Science 42 (1986): 1231–1241.

- It has been argued that the resource-based perspective does not qualify as an academic theory. For details on this exchange, see R. L. Priem and J. E. Butler, “Is the Resource-Based ‘View’ a Useful Perspective for Strategic Management Research,” Academy of Management Review 26 (2001): 22–40; J. B. Barney, “Is the Resource-Based ‘View’ a Useful Perspective for Strategic Management Research? Yes,” Academy of Management Review 26 (2001): 41–56.

- J. B. Barney, “Looking Inside for Competitive Advantage,” Academy of Management Executive 19 (1995): 49–61.

- W. W. C. Chung, M. F. S. Chan, and T. S. Leung, “A Framework of Performance Modeling for Dynamic Strategy,” International Journal of Business Performance Management 8 (2006): 62–76; N. Foss and I. Ishikawa, “Towards a Dynamic Resource-Based View: Insights from Austrian Capital and Entrepreneurship Theory,” Organization Studies 28 (2007): 749–772.

- S. L. Berman, J. Down, and C. W. L. Hill, “Tacit Knowledge as a Source of Competitive Advantage in the National Basketball Association,” Academy of Management Journal 45 (2002): 13–32.

- E. J. Zajac, M. S. Kraatz, and R. K. F. Bresser, “Modeling the Dynamics of Strategic Fit: A Normative Approach to Strategic Change,” Strategic Management Journal 21 (2000): 429–453.

- C. A. Lengnick-Hall and J. A. Wolff, “Similarities and Contradictions in the Core Logic of Three Strategy Research Streams,” Strategic Management Journal 20 (1999): 1109–1132; O. E. Williamson, “Strategy Research: Governance and Competence Perspectives,” Strategic Management Journal 20 (1999): 1087–1108.

- S. Chen and K. W. Ho, “Blockholder Ownership and Market Liquidity,” Journal of Financial & Quantitative Analysis 35 (2000): 621–633; J. J. McConnell and H. Servaes, “Additional Evidence on Equity Ownership and Corporate Value,” Journal of Financial Economics 27 (1990): 595–612.

- W. J. Salmon, “Crisis Prevention: How to Gear Up Your Board,” Harvard Business Review 71 (1993): 68–75.

- B. Hermalin and M. S. Weisbach, “The Determinants of Board Composition,” Rand Journal of Economics 19 (1988): 589–605; E. F. Fama and M. C. Jensen, “Separation of Ownership and Control,” Journal of Law and Economics 26 (1983): 301–325; M. S. Weisbach, “Outside Directors and CEO Turnover,” Journal of Financial Economics 20 (1988): 431–460.

- P. A. Gibbs, “Determinants of Corporate Restructuring: The Relative Importance of Corporate Governance, Takeover Threat, and Free Cash Flow,” Strategic Management Journal 14 (1993): 51–68.

chapter 1 Fundamentals of Strategic Management (^17)

- National Association of Corporate Directors, “NACD Director Compensation Report 2010–2011,” April 15, 2011, http:// www.directorship.com/compensation-rises-with-the-market/ (accessed October 14, 2011).

- N. Dunne, “Adding a Little Muscle In the Boardroom,” Financial Times , October 10, 2003, I.

- A. Raghavan, “More CEOs Say ‘No Thanks’ to Board Seats,” Wall Street Journal , January 28, 2005, B1, B4.

- J. H. Morgan, “The Board of Directors Is No Longer Just a ‘Rubber Stamp,’” TMA Journal 19, no. 5 (1999): 14–18.

- B. R. Baliga and R. C. Moyer, “CEO Duality and Firm Performance,” Strategic Management Journal 17 (1996): 41–53; P. Stiles, “The Impact of Board on Strategy: An Empirical Examination,” Journal of Management Studies 38 (2001): 627–650.

- S. Finkelstein and R. D’Aveni, “CEO Duality as a Double-Edged Sword,” Academy of Management Journal 37 (1994): 1079–1108.

- A. Zimmerman, “Target Cooks Up Rebound Recipe in Grocery Aisles,” Wall Street Journal , May 12, 2009, B1, B2.

- N. Dunne, “Adding a Little Muscle In the Boardroom,” Financial Times , October 10, 2003, I; W. Royal, “Impeach the Board,” Industry Week, November 16, 1998, 47–50; C. Torres, “Firms’ Restructuring Often Hurt Foreign Buyers,” Wall Street Journal Interactive Edition , May 13, 1996; M. L. Weidenbaum, “The Evolving Corporate Board,” Society (March–April 1995): 9–16.

- J. Goldstein, K. Gautum, and W. Boeker, “The Effects of Board Size and Diversity on Strategic Change,” Strategic Management Journal 15 (1994): 241–250.

- M. S. Mizruchi, “Who Controls Whom? An Examination of the Relation Between Management and Board of Directors in Large American Corporations,” Academy of Management Review 8 (1983): 426–435.

- C. Wohlstetter, “Pension Fund Socialism: Can Bureaucrats Run the Blue Chips?” Harvard Business Review 71 (1993): 78.

- J. A. Conger, D. Finegold, and E. E. Lawler III, “Appraising Boardroom Performance,” Harvard Business Review 76, no. 1 (1998): 136–148.

- T. K. Das and B. Teng, “Cognitive Biases and Strategic Decision Processes: An Integrative Perspective,” Journal of Management Studies 36 (1999): 757–778; M. A. Carpenter, “The Implications of Strategy and Social Context for the Relationship Between Top Team Management Heterogeneity and Firm Performance,” Strategic Management Journal 23 (2002): 275–284.

- A. J. Hillman and M. A. Hitt, “Corporate Political Strategy Formulation: A Model of Approach, Participation, and Strategy Decisions,” Academy of Management Review 24 (1999): 825–842.

- P. Wright, M. Kroll, and J. A. Parnell, Strategic Management: Concepts (Upper Saddle River, NJ: Prentice Hall, 1998).

- J. Badal, “Can a Company Be Run as a Democracy?” Wall Street Journal , April 23, 2007, B1, B6.

- B. M. Staw, “Knee-Deep in the Big Muddy: A Study of Escalating Commitment to a Chosen Course of Action,” Organizational Behavior and Human Performance 16, no. 1 (1976): 27–44.

- C. Devonshire-Ellis, “China Now Has Third Highest Labor Costs in Emerging Asia,” China Briefing , January 19, 2011, www .china-briefing.com/news/2011/01/19/china-near-top-of-the-list-for-wage-overheads-in-emerging-asia.html (accessed October 13, 2011).

- T. Eiben, “U.S. Exporters on a Global Roll,” Fortune , June 29, 1992, 94.

chapter 1 Fundamentals of Strategic Management (^19) As Financial Times columnist Martin Wolf wrote on September 13, 2009, the West’s “reputation for financial and economic competence is in tatters, while that of China has soared.” Moreover, profitability is rising for global com- panies in China. A 2009 study by the American Chamber of Commerce in Beijing noted that in 1999, only 13 per- cent of companies reported margins in China that were higher than their worldwide averages; in mid-2008 (before the onset of the global financial crisis), this figure reached 50 percent. Moreover, a large number of multinational executives feel that they have gained enough experience in China to expect a relatively coherent, expanding future for their Chinese operations. But the challenge of doing business in China has increased during the past few years. Most businesses, even many that are currently successful, will find themselves inadequately prepared for the turmoil and dynamism to come. Not only could they miss out on the opportunities in this economy; they could be pushed aside by rivals, old and new, that use China to transform their competitive positions. In 2005, I wrote in this magazine that in the world’s fastest-growing economy, the experience of the last 10 years will not be the best guide to the next 10 years. This statement has even more truth, and even greater urgency, in 2010. Business leaders around the world who want to be successful will need to take on a chal- lenge with four components: the growing complexity of the Chinese market, the new sophistication of Chinese competitors, the evolving interests of the Chinese government, and their own entrenched assumptions about global business.

The Complexity of Open China _____________________________

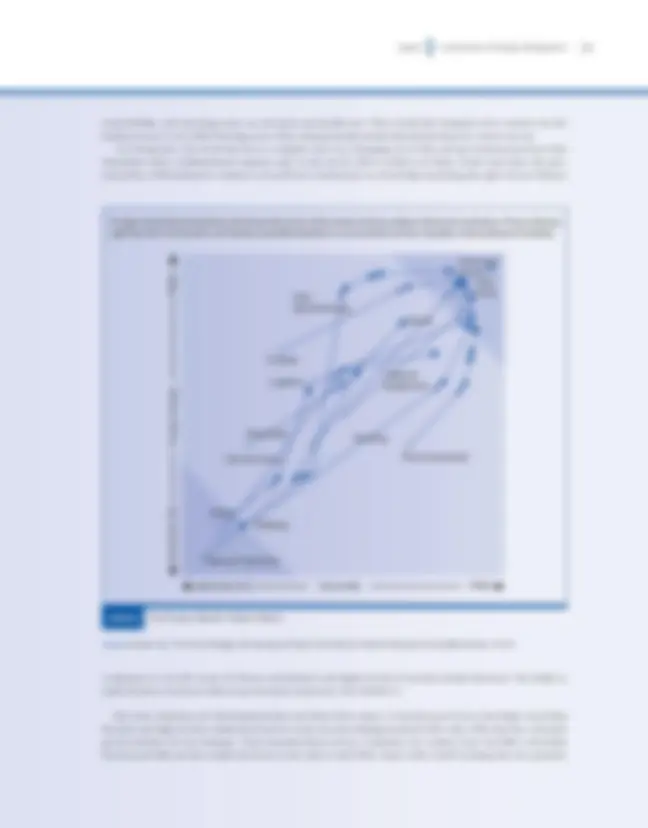

Only 30 years after it began to open and liberalize its economy, China offers its consumers an extraordinary range of brands and products that no other country, even the wealthy consumer markets of Japan, Europe, and the United States, can match. In any convenience store in Shanghai or Dalian, you can find Western beverages such as Coke, Pepsi, and Schweppes; Japanese soft drinks made by Suntory, Kirin, and Sapporo; Taiwanese flavors under the Uni-President label; Hong Kong brands such as Vitasoy; and local teas, coffees, soy milks, and fruit drinks. Chinese companies make their own versions of every international flavor, and many flavors that are not produced elsewhere. Outside, on the newsstands, are Chinese magazines and Chinese editions of such familiar global titles as Cosmopolitan , Vogue , and Elle. Driving on the streets are locally manufactured vehicles from almost every global carmaker—General Motors and Ford, Toyota and Honda, Volkswagen and its subsidiary Audi, BMW and Mercedes, Citroën and Hyundai—plus a host of local auto brands, including Chery, Geely, Brilliance, and Great Wall Motor. Step inside a department store and you will see a similar proliferation of labels and choices. For most of the local patrons in cities such as Shenyang, Wuhan, and Changsha, this is a remarkable change from the sparsely stocked, dour shops that they patronized just a decade ago. The shift in population from predominantly rural to predominantly urban is having an impact on almost every aspect of Chinese life. Millions of people are being lifted from poverty, probably far more in the next few years than in the past few decades. Since the start of the 1990s, annual retail sales in China have increased more than 15-fold, from around US$100 billion to more than $1.6 trillion by the end of 2008. (The 2008 figure is about one- third of the retail sales in the United States during the same year.) The Chinese middle class, although new, will not be a short-lived phenomenon; it is here to stay. At first glance, for global consumer-oriented companies, this situation would seem to be the realization of a dream. For years, they have looked forward to the rise of the mythical “land of 1 billion–plus consumers”—eager for new products, ready to be sold to. A company with a product or service well targeted for a market category or consumer segment—perhaps a packaged good aimed at newly urbanized, frugal, demanding consumers—can expect to find hundreds of thousands of potential customers in China. This consumer market represents the larg- est “niche play” opportunity in the history of world commerce.

20 STRATEGIC MANAGEMENT

Yet this market is far more complex than many outsiders realize. The expansion of Chinese markets is accom- panied by phenomenal competition, as well as abrupt rises and falls in market share for both new and established products. Most importantly, although China’s markets are open to global products, they are also extraordinarily local, rooted in traditional customs and tastes, with extreme variations from one region to the next. The methods that most global marketers have used in China so far will not be effective in the future. Most multinationals have concentrated their Chinese marketing in relatively small parts of the country, targeting only a fraction of the potential consumer population. Global companies are most familiar with the “big three” clus- ters: the Yangtze River Delta region around Shanghai, the Pearl River Delta region running from Hong Kong to Guangzhou, and the region around Beijing and its neighbor Tianjin. These three areas account for almost half of China’s GDP and have relatively high per capita GDP, about $5,000 to $6,500. But the rest of China represents a yet more promising market, with a higher urbanization rate, new transportation and communications links, and many cities with populations of more than 1 million. (See Exhibit 1.) The differences within regions are also enormous. Even in the wealthiest provinces, such as the coastal parts of Guangdong or Zhejiang, you need travel only a short distance inland and incomes fall abruptly. The gap between rural and urban residents splits the nation; the divide between permanent residents and migrant workers splits many cities. Exhibit 1 Emerging Cities in China, Present and Future Source: Edward Tse, The China Strategy: Hamessing the Power of the World’s Fastest-Growing Economy (Basic Books, 2010) A growing number of cities in China, including many outside the “big three” clusters, are rapidly becoming vibrant consumer markets, but are still relatively ignored by global multinationals.