Download Understanding Assurance Engagements and Pro forma Adjustments in Financial Reporting and more Lecture notes Auditing in PDF only on Docsity!

Attachment to AUASB Board Meeting Summary Paper

AGENDA ITEM NO. 6.1.

Meeting Date: 12 September 2018

Subject: Attachment A – Glossary Supporting Tables

Date Prepared: 28 August 2018

Overview of document

The purpose of this attachment is to show the AUASB Technical Group’s (ATG) rationale for the presentation of terms with multiple definitions in Agenda Paper 6.1.3 Proposed AUASB Glossary 2018 – Clean. As outlined in paragraphs 3-7 of the BMSP to this Agenda Item, differing definitions were encountered within, and across, the suites of issued standards. Three tables have been provided to show how the ATG has dealt with each of the situations.

(a) Table 1 – Duplication within the suite of ASAs (Australian Auditing Standards);

(b) Table 2 – Duplication within the suite ASAEs (Standards on Assurance Engagements); and

(c) Table 3 – Complete list of all terms with multiple definitions including between ASAs and ASAEs.

Table 1 – Duplication within the suite of ASAs

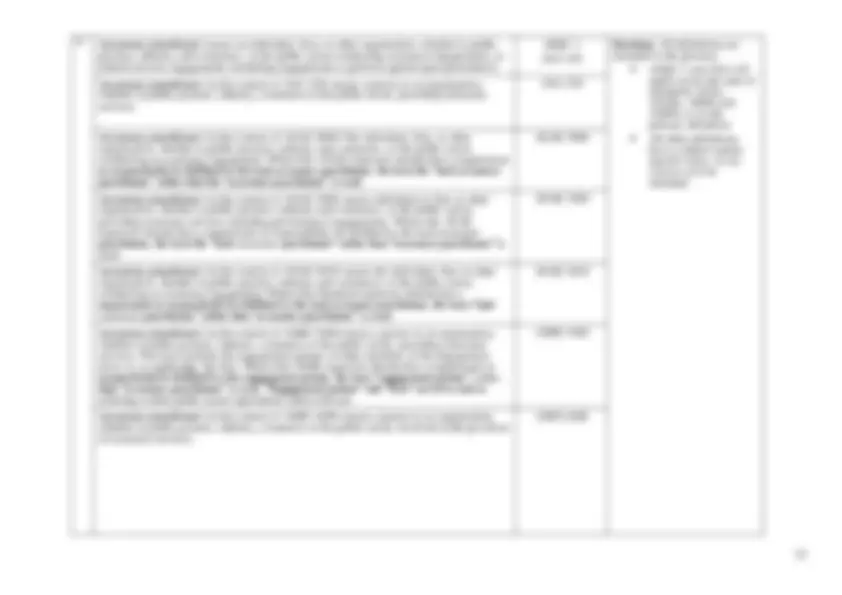

# Term and Definition Source ATG Comment 1 Applicable financial reporting framework means the financial reporting framework adopted by management and, where appropriate, those charged with governance in the preparation of the financial report that is acceptable in view of the nature of the entity and the objective of the financial report, or that is required by law or regulation.

The term fair presentation framework means a financial reporting framework that requires compliance with the requirements of the framework and:

(a) Acknowledges explicitly or implicitly that, to achieve fair presentation of the financial report, it may be necessary for management to provide disclosures beyond those specifically required by the framework; or

(b) Acknowledges explicitly that it may be necessary for management to depart from a requirement of the framework to achieve fair presentation of the financial report. Such departures are expected to be necessary only in extremely rare circumstances.

The term compliance framework means a financial reporting framework that requires compliance with the requirements of the framework, but does not contain the acknowledgements in (a) or (b) above. (see Fair presentation framework )

ASA 200 Decision: Both definitions are included in the glossary. ASA 200 is a general definition. ASA 600 has a focus on group audit. In the context of to be included. The same variance exists between ISA 200 and ISA 600.

Applicable financial reporting framework (in the context of ASA 600) means the financial reporting framework that applies to the group financial report.

ASA 600

(^2) Assurance practitioner means an individual, firm, or other organisation, whether in public practice, industry and commerce, or the public sector conducting assurance engagements, or related services engagements (including engagements to perform agreed-upon procedures).

ASQC 1

ASA 102

Decision: Both definitions are included in the glossary. ASQC 1 and ASA 102 apply across the suite of standards (ASAs, ASAEs, ASRE and ASRSs) so is the general definition. ASA 220 has focus on audit engagements. In the context of to be included.

Assurance practitioner (in the context of ASA 220) means a person or an organisation, whether in public practice, industry, commerce or the public sector, providing assurance services.

ASA 220

Engagement quality control reviewer means a partner, other person in the firm, suitably qualified external person, or a team made up of such individuals, none of whom is part of the engagement team, with sufficient and appropriate experience and authority to objectively evaluate the significant judgements the engagement team made and the conclusions it reached in formulating the auditor’s report.

ASA 220 report”^ in ASA 220 and “report” in the others. Insignificant difference so combined.

(^6) Financial statements means a structured representation of historical financial information,

including disclosures, intended to communicate an entity’s economic resources or obligations at a point in time, or the changes therein for a period of time, in accordance with a financial reporting framework. The term “financial statements” ordinarily refers to a complete set of financial statements as determined by the requirements of the applicable financial reporting framework, but can also refer to a single financial statement. Disclosures comprise explanatory or descriptive information, set out as required, expressly permitted or otherwise allowed by the applicable financial reporting framework, on the face of a financial statement, or in the notes, or incorporated therein by cross-reference.

ASA 200 (^) Decision: Both definitions are included in the glossary. ASA 200 is a general definition.

ASA 800 has focus on special purpose financial statements. In the context of to be included. The same variance exists between ISA 200 and ISA 800.

Financial statements (in the context ASA 800) means a complete set of special purpose financial statements. The requirements of the applicable financial reporting framework determine the presentation, structure, and content of the financial statements, and what constitutes a complete set of financial statements. Reference to “special purpose financial statements” includes the related disclosures.

ASA 800

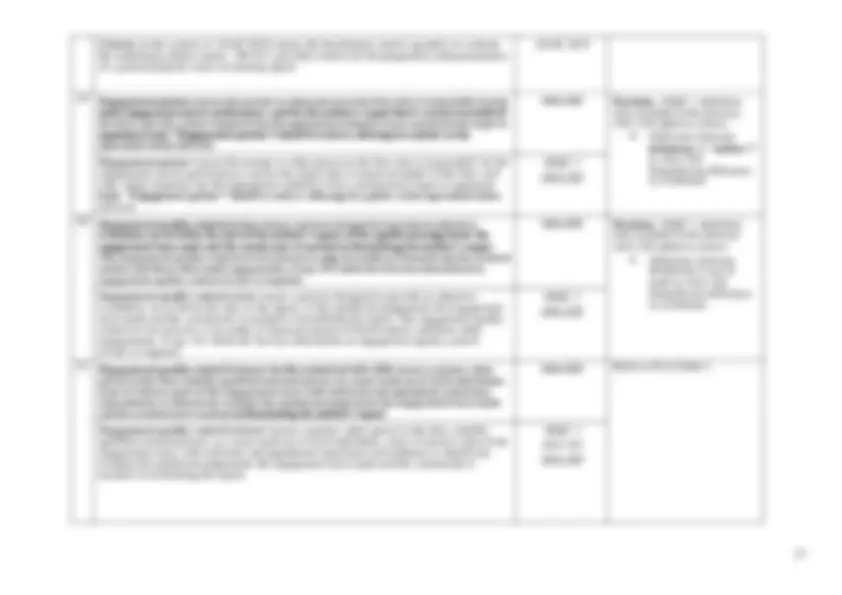

(^7) Inspection means in relation to completed engagements, procedures designed to provide

evidence of compliance by engagement teams with the firm’s quality control policies and procedures.

ASQC 1

ASA 220

Decision: Both definitions are included in the glossary. ASA 500 has a focus on inspection as an audit procedure. As an audit procedure included.

ASQC 1 and ASA 220 have a focus on inspection in the context of quality control.

Inspection (as an audit procedure) means examining records or documents, whether internal or external, in paper form, electronic form, or other media, or a physical examination of an asset.

ASA 500

(^8) Management means the person(s) with executive responsibility for the conduct of the entity’s

operations. For some entities in some jurisdictions, management includes some or all of those charged with governance, for example, executive members of a governance board, or an owner- manager.

ASA 200

ASA 260

Decision: Both definitions are included in the glossary. ASA 580 has a specific focus on management and those charged with governance in the context of written representations. In the context of to be included.

ASA 200 and ASA 260 have a general definition of management which does not

Management (in the context of ASA 580) should be read as “management and, where appropriate, those charged with governance.” Furthermore, in the case of a fair presentation framework, management is responsible for the preparation and fair presentation of the financial report in accordance with the applicable financial reporting framework; or the preparation of a financial report that gives a true and fair view in accordance with the applicable financial reporting framework.

ASA 580

include those charged with governance.

(^9) Misstatement means a difference between the amount, classification, presentation, or disclosure

of a reported financial report item and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. Where the auditor expresses an opinion on whether the financial report is presented fairly, in all material respects, or gives a true and fair view, misstatements also include those adjustments of amounts, classifications, presentation, or disclosures that, in the auditor’s judgement, are necessary for the financial report to be presented fairly, in all material respects, or to give a true and fair view.

ASA 200 (^) Decision: ASA 450 definition included in the glossary. ASA 200 added as a source. Difference between definitions is “Where the auditor expresses” in ASA 220 and “When the auditor expresses” in ASA 450. Insignificant difference so combined. Misstatement means a difference between the amount, classification, presentation, or disclosure of a reported financial report item and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. When the auditor expresses an opinion on whether the financial report is presented fairly, in all material respects, or gives a true and fair view, misstatements also include those adjustments of amounts, classifications, presentation, or disclosures that, in the auditor’s judgement, are necessary for the financial report to be presented fairly, in all material respects, or to give a true and fair view.

ASA 200

ASA 450

(^4) Carve-out method (in the context of ASAE 3150) means a method of dealing with controls

operating at a third party, which are integral to the system or control component which is subject to the engagement, whereby that third party’s relevant control objectives and related controls are excluded from the scope of the assurance practitioner’s engagement. The scope of the assurance practitioner’s engagement includes controls at the entity to monitor the effectiveness of controls which form part of the entity’s system, operating at the third party.

ASAE 3150 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Carve-out method (in the context of ASAE 3402 ) means a method of dealing with the services provided by a subservice organisation, whereby the service organisation’s description of its system includes the nature of the services provided by a subservice organisation, but that subservice organisation’s relevant control objectives and related controls are excluded from the service organisation’s description of its system and from the scope of the service auditor’s engagement. The service organisation’s description of its system and the scope of the service auditor’s engagement include controls at the service organisation to monitor the effectiveness of controls at the subservice organisation, which may include the service organisation’s review of an assurance report on controls at the subservice organisation.

ASAE 3 402

(^5) Comparative information (in the context of ASAE 3410) means the amounts and disclosures

included in the GHG statement in respect of one or more prior periods.

ASAE 3410 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context Comparative information (in the context of ASAE 3610) means the volumes and disclosures of to be included for all. included in the general purpose water accounting report in respect of one or more prior periods.

ASAE 3610

(^6) Complementary user entity controls (in the context of ASAE 3150) means controls that an

entity, which is a service organisation, assumes, in the design of its service, will be implemented by user entities or clients, and which, if necessary to achieve control objectives stated in the entity’s description of its system, are identified in that description.

ASAE 3150 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Complementary user entity controls (in the context of ASAE 3402) means controls that the service organisation assumes, in the design of its service, will be implemented by user entities, and which, if necessary to achieve control objectives stated in the service organisation’s description of its system, are identified in that description.

ASAE 3402

(^7) Control objective means the aim or purpose of a particular aspect of controls. Control

objectives relate to risks that controls seek to mitigate and may be categorised by the framework applied, such as operational (economy, effectiveness and efficiency), reporting (statutory or management, financial or non-financial) or compliance (adherence to laws and regulations or contractual obligations).

ASAE 3150 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Control objective (in the context of ASAE 3402) means the aim or purpose of a particular aspect of controls. Control objectives relate to risks that controls seek to mitigate.

ASAE 3402

(^8) Criteria means the benchmarks used to measure or evaluate the underlying subject matter. The

“applicable criteria” are the criteria used for the particular engagement.

ASAE 3000

ASAE 3150

ASAE 3402

Decision: All definitions included in the glossary. ASAE 3100 and ASAE 3500 are subject-matter specific. In the context of to be included The definition which applies to ASAE 3000, ASAE 3150 and ASAE 3402 will not have in the context included as it applies to multiple standards.

Criteria (in the context of ASAE 3100) means the benchmark, framework or legislation used to evaluate whether the compliance requirements have been met. The “applicable criteria” are the criteria used for the particular engagement.

ASAE 3100

Criteria (in the context of ASAE 3500) means the benchmarks used to measure or evaluate the underlying subject matter, which in a performance engagement is the activity. The “identified criteria” are the criteria used for the particular engagement.

ASAE 3500

Criteria (in the context of ASAE 3610) means the benchmarks used to quantify or evaluate the underlying subject matter. AWAS 1 provides criteria for the preparation and presentation of a general purpose water accounting report.

ASAE 3610

(^9) Engagement risk means the risk that the assurance practitioner expresses an inappropriate

conclusion when the subject matter information is materially misstated.

ASAE 3000

ASAE 3500

ASRE 2400

Decision: All definitions included in the glossary. ASAE 3610 is subject-matter specific. In the context of to be included. The definition which applies to ASAE 3000, ASAE 3500 and ASRE 2400 will not have in the context included as it applies to multiple standards.

Engagement risk (in the context of ASAE 3610) means the risk that the assurance practitioner expresses an inappropriate conclusion when the general purpose water accounting report is materially misstated.

ASAE 3610

(^10) Engagement team means all assurance practitioners and staff performing the engagement, and

any individuals engaged by the firm or a network firm who perform procedures on the engagement. This excludes an assurance practitioner’s external expert engaged by the firm or a network firm.

ASAE 3000 Decision:^ All definitions included in the glossary. ASAE 3610 is subject-matter specific and focuses on water accounting and assurance. In the context of to be included. The definition in ASAE 3000 applies to the suite of ASAEs.

Engagement team (in the context of ASAE 3610 ) means all assurance practitioners and staff performing the assurance engagement, and any individuals engaged by the firm or a network firm who perform procedures on the engagement. This excludes an assurance practitioner’s external expert engaged by the firm or a network firm.

ASAE 3610

(^14) Historical financial information means information expressed in financial terms in relation to

a particular entity, derived primarily from that entity’s accounting system, about economic events occurring in past time periods or about economic conditions or circumstances at points in time in the past.

ASAE 3000

ASAE 3450

Decision: ASAE 3000 definition only included in the glossary. ASAE 3450 added as source. Difference between definitions is “economic” in ASAE 3000. Insignificant difference so combined.

Historical financial information means information expressed in financial terms in relation to a particular entity, which is derived primarily from that entity’s accounting system and relates to events occurring in past time periods or about conditions or circumstances at points in time in the past.

ASAE 3450

(^15) Inclusive method (in the context of ASAE 3402) means method of dealing with the services

provided by a subservice organisation, whereby the service organisation’s description of its system includes the nature of the services provided by a subservice organisation, and that subservice organisation’s relevant control objectives and related controls are included in the service organisation’s description of its system and in the scope of the service auditor’s engagement.

ASAE 3402 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Inclusive method (in the context of ASAE 3150) means a method of dealing with the controls operating at a third party, which are integral to the system or control component which is subject to the assurance engagement, whereby the third party’s relevant control objectives and related controls are included in the scope of the assurance practitioner’s engagement.

ASAE 3150

(^16) Intended users means the individual(s) or organisation(s), or group(s) thereof that the

practitioner expects will use the assurance report. In some cases, there may be intended users other than those to whom the assurance report is addressed.

ASAE 3000

ASAE 3100

ASAE 3150

Decision: All definitions included in the glossary. ASAE 3500 definition is subject-matter specific. In the context of to be included. The definition which applies to ASAE 3000, ASAE 3100 and ASAE 3150 will not have in the context included as it applies to multiple standards.

Intended users (in the context of ASAE 3500) means parliament, responsible party, individual(s) or organisation(s), or group(s) thereof that the assurance practitioner expects will use the assurance report. In some cases, there may be intended users other than those to whom the assurance report is addressed, such as the general public if the assurance report is made publicly available.

ASAE 3500

(^17) Internal auditors means those individuals who perform the activities of the internal audit

function. Internal auditors may belong to an internal audit department or equivalent function.

ASAE 3402 Decision: All definitions included in the glossary. The ASAE 3150 definition expands internal auditors further, than ASAE 3402. In the context to be included for ASAE 3402 definition.

Internal auditors (in the context of ASAE 3150) means those individuals who perform the activities of the internal audit function. Internal auditors may belong to an internal audit department or equivalent function, out-sourcing entity or co-sourced from both internal and out-sourced resources.

ASAE 31 50

(^18) Lead assurance practitioner means the person in the firm who is responsible for the

engagement and its performance, and for the assurance report that is issued on behalf of the firm, and who, where required, has the appropriate authority from a professional, legal or regulatory body. The “lead assurance practitioner” should be read as referring to its public sector equivalents where relevant.

ASAE 3000

ASAE 3610

Decision: ASAE 3000 definition only included in the glossary. ASAE 3610 added as source. Difference between definitions is “the” in ASAE 3000. Insignificant difference so combined.

Lead assurance practitioner means the person in the firm who is responsible for the engagement and its performance, and for the assurance report that is issued on behalf of the firm, and who, where required, has the appropriate authority from a professional, legal or regulatory body. “lead assurance practitioner” should be read as referring to its public sector equivalents where relevant.

ASAE 3610

(^19) Limited assurance engagement means an assurance engagement in which the assurance

practitioner reduces engagement risk to a level that is acceptable in the circumstances of the engagement, but where that risk is greater than for a reasonable assurance engagement, as the basis for expressing a conclusion in a form that conveys whether, based on the procedures performed and evidence obtained, a matter(s) has come to the assurance practitioner’s attention to cause the assurance practitioner to believe the compliance requirements have not been met, in all material respects. The nature, timing and extent of procedures performed in a limited assurance engagement is limited compared with that necessary in a reasonable assurance engagement but is planned to obtain a level of assurance that is, in the assurance practitioner’s professional judgement, meaningful. To be meaningful, the level of assurance obtained by the assurance practitioner is likely to enhance the intended users’ confidence about the compliance outcome to a degree that is clearly more than inconsequential.

ASAE 3100

ASAE 3150

ASAE 3500

Decision: All definitions included in the glossary. ASAE 3450 definition is subject-matter specific. In the context of to be included. The definition which applies to ASAE 3100, ASAE 3150 and ASAE 35000 will not have in the context included as it applies to multiple standards.

Limited assurance engagement (in the context of ASAE 3450) means an assurance engagement in which the assurance practitioner reduces the assurance engagement risk to a level that is acceptable in the circumstances of the assurance engagement, but where the risk is greater than for a reasonable assurance engagement. The set of procedures performed in a limited assurance engagement is limited compared with that necessary in a reasonable assurance engagement, but is planned to obtain a level of assurance that is, in the assurance practitioner’s professional judgement acceptable in the circumstances of the assurance engagement. An example of a limited assurance engagement is a review.

ASAE 3450

(^20) Management means the person(s) with executive responsibility for the conduct of the

operations or individual business units of the entity. For some entities, in some circumstances, management includes some or all of those charged with governance, for example, executive members of a governance board, or an owner-manager.

ASAE 3450 Decision: Both definitions included in the glossary. ASAE 3610 definition is subject-matter specific. In the context of to be included.

ASAE 3450 will not have in the context included as it is broader.

Management (in the context of ASAE 3610) means for the purposes of this Standard, management refers to those with executive responsibility for the preparation and presentation of the general purpose water accounting report, including water accounting and reporting, unless otherwise specified. In some instances, management includes some or all of those charged with governance, for example, executive members of a governance board, or an owner- manager.

ASAE 36 10

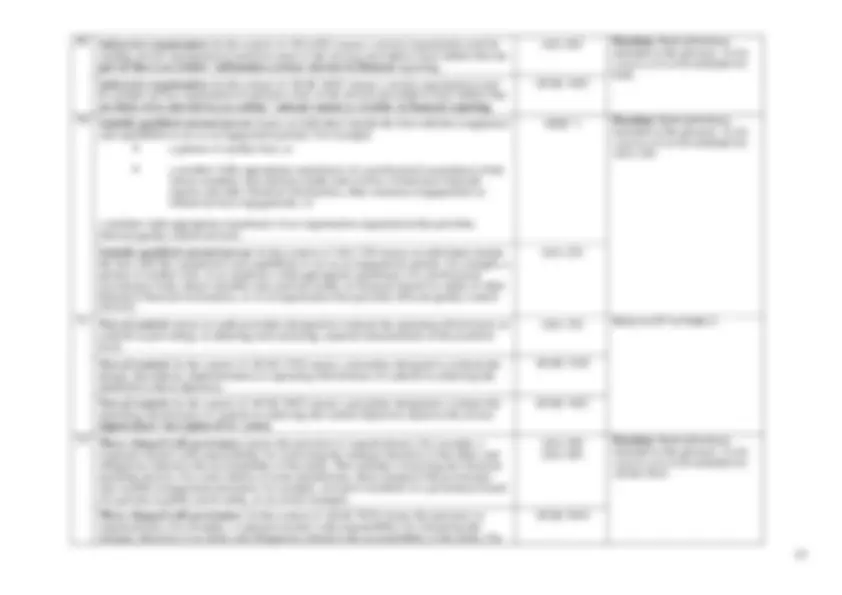

Misstatement of fact (with respect to other information) means other information that is unrelated to matters appearing in the subject matter information or the assurance report that is incorrectly stated or presented. A material misstatement of fact may undermine the credibility of the document containing the subject matter information.

ASAE 3000 Decision: Both definitions included in the glossary. ASAE 3000 has a focus on other information. With respect to other information to be included.

Misstatement of fact means information that is incorrectly stated or presented in the document. A material misstatement of fact may undermine the credibility of financial information that is the subject of the assurance report.

ASAE 3450

Performance materiality (in the context of ASAE 3410) means the amount or amounts set by the assurance practitioner at less than materiality for the GHG statement to reduce to an appropriately low level the probability that the aggregate of uncorrected and undetected misstatements exceeds materiality for the GHG statement. If applicable, performance materiality also refers to the amount or amounts set by the assurance practitioner at less than the materiality level or levels for particular types of emissions or disclosures.

ASAE 3410 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Performance materiality (in the context of ASAE 3610) means the amount or amounts set by the assurance practitioner at less than materiality for the general purpose water accounting report to reduce to an appropriately low level the probability that the aggregate of uncorrected and undetected misstatements exceeds materiality for the general purpose water accounting report.

ASAE 3610

Pro forma adjustments (in the context of ASAE 3420) means in relation to unadjusted financial information, these include: (a) Adjustments to unadjusted financial information that illustrate the impact of a significant event or transaction (“event” or “transaction”) as if the event had occurred or the transaction had been undertaken at an earlier date selected for purposes of the illustration; and (b) Adjustments to unadjusted financial information that are necessary for the pro forma financial information to be compiled on a basis consistent with the applicable financial reporting framework of the reporting entity (“entity”) and its accounting policies under that framework. Pro forma adjustments include the relevant financial information of a business that has been, or is to be, acquired (“acquiree”), or a business that has been, or is to be, divested (“divestee”), to the extent that such information is used in compiling the pro forma financial information (“acquiree or divestee financial information”).

ASAE 3420 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Pro forma adjustments (in the context of ASAE 3450) means adjustments selected by the responsible party in accordance with the stated basis of preparation to make to base financial information (historical or prospective) to: (i). illustrate the impact of a significant event or transaction (―event‖ or ―transaction‖) as if the event had occurred or the transaction had been undertaken at an earlier date than actually occurred, or as if it had not occurred at all; and/or

ASAE 3450

(ii). eliminate the effects of unusual or non-recurring event(s) or transaction(s) that are not part of the normal operations of the entity; and/or (iii). exclude certain event(s) or transaction(s), or present transactions or balances on a different recognition and measurement basis from that required or permitted by Australian Accounting Standards; and/or (iv). correct errors or uncertainties.

Pro forma financial information (in the context of ASAE 3420) means historical financial information shown together with adjustments to illustrate the impact of an event(s) or transaction(s) on unadjusted financial information as if the event had occurred or the transaction had been undertaken at an earlier date selected for purposes of the illustration. In this ASAE, it is assumed that pro forma financial information is presented in columnar format consisting of (a) the unadjusted historical financial information; (b) the pro forma adjustments; and (c) the resulting pro forma column.

ASAE 3420 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Pro forma financial information (in the context of ASAE 3450) means base financial information adjusted for pro forma adjustments in accordance with the stated basis of preparation, resulting in non-IFRS financial information that is not prepared in accordance with Australian Accounting Standards. It is subject to the assumptions inherent in the responsible party’s stated basis of preparation.

ASAE 3450

(^27) Professional judgement means the application of relevant training, knowledge and experience,

within the context provided by assurance and ethical standards, in making informed decisions about the courses of action that are appropriate in the circumstances of the engagement.

ASAE 3000

ASAE 3100

ASAE 3610

Decision: ASAE 3000 and ASAE 3100 definition only included in the glossary. ASAE 3610 added as source. Difference between definitions is “assurance” in ASAE 3610. Insignificant difference so combined.

Professional judgement means the application of relevant training, knowledge and experience, within the context provided by assurance and ethical standards, in making informed decisions about the courses of action that are appropriate in the circumstances of the assurance engagement.

ASAE 3610

(^28) Professional scepticism means an attitude that includes a questioning mind, being alert to

conditions which may indicate possible misstatement and a critical assessment of evidence.

ASAE 3000 Decision:^ All definitions included in the glossary. Each definition is subject-matter specific. In the context Professional scepticism (in the context of ASAE 3100) means an attitude that includes a of to be included for all. questioning mind, being alert to conditions which may indicate possible misstatement or non- compliance, and a critical assessment of evidence.

ASAE 3100

Professional scepticism (in the context of ASAE 3500) means an attitude that includes a questioning mind, being alert to the validity of evidence obtained and to critically assess evidence that contradicts or brings into question the reliability of documents and responses to enquiries and other information obtained.

ASAE 3500

Professional scepticism (in the context of ASAE 3610) means an attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement, and a critical assessment of evidence.

ASAE 3610

Reasonable assurance engagement (in the context of ASAE 3450) means an assurance engagement where the assurance practitioner reduces the assurance engagement risk to an acceptably low level in the circumstances of the assurance engagement as the basis for the assurance practitioner’s conclusion.

ASAE 3450

(^31) Representation means s tatement by the responsible party, either oral or written, provided to the

assurance practitioner to confirm certain matters or to support other evidence. A representation is additional to but may be provided in combination with the responsible party’s or evaluator’s Statement provided in an attestation engagement.

ASAE 3100

ASAE 3150

Decision: Both definitions included in the glossary. ASAE 3500 definition is subject-matter specific. In the context of to be included.

ASAE 3100 and ASAE 3150 will not have in the context included as it applies to multiple standards.

Representation (in the context of ASAE 3500) means statement by the responsible party, either oral or written, provided to the assurance practitioner to confirm certain matters or to support other evidence.

ASAE 3500

(^32) Responsible party means the party (ies) responsible for the underlying subject matter. ASAE 3000 Decision: All definitions included in the glossary. ASAE 3100, ASAE 3150, ASAE 3450, ASAE 3500 and ASAE 3610 definitions are subject-matter specific. In the context of to be included.

Responsible party (in the context of ASAE 3100) means the party (ies) responsible for the underlying subject matter, being the compliance activity (ies) in a compliance engagement.

ASAE 3100

Responsible party (in the context of ASAE 3150) means the party (ies) responsible for the underlying subject matter, being the design, description, implementation or operating effectiveness of controls in an assurance engagement on controls.

ASAE 3150

Responsible party (in the context of ASAE 3450) means those charged with governance of the entity (ordinarily the Board of Directors), who are also responsible for the preparation and issuance of the financial information included in the document. It may also mean the management of the entity in circumstances where the assurance practitioner has been requested to provide assurance to those charged with governance in relation to financial information prepared by management. Alternatively it may also mean the party responsible for the preparation of the financial information. The responsible party may be different from the party that is the engaging party.

ASAE 3450

Responsible party (in the context of ASAE 3500) means the party (ies) responsible for the performance of all or part of the activity, which is the subject matter of the performance engagement.

ASAE 3500

Responsible party (in the context of ASAE 3610) means those charged with governance or management, as appropriate, responsible for the preparation and presentation of the general purpose water accounting report.

ASAE 3610

(^33) Service organisation means a third party organisation (or segment of a third party organisation)

that provides services to user entities that are likely to be relevant to user entities’ internal control as it relates to relevant external reporting, whether financial, emissions and energy, carbon offsets, compliance or other reporting.

ASAE 3150 Decision: Both definitions included in the glossary. ASAE 3402 definition is subject-matter specific. In Service organisation (in the context of ASAE 3402) means a third-party organisation (or^ the context of^ to be included. segment of a third-party organisation) that provides services to user entities that are likely to be relevant to user entities’ internal control as it relates to financial reporting.

ASAE 3402

(^34) Statement (in the context of ASAE 3100) means the outcome in writing of the responsible

party or evaluator’s evaluation of compliance with the compliance requirements, provided to the assurance practitioner in an attestation engagement. A Statement is the subject matter information in an attestation engagement on compliance.

ASAE 3100 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Statement (in the context of ASAE 3150) means the outcome in writing of the responsible party or evaluator’s evaluation of the suitability of the design of controls to achieve the control objectives, and, if included in the scope of the engagement, the fair presentation of the description of the system, implementation of controls as designed or operating effectiveness of controls as designed, provided to the assurance practitioner in an attestation engagement. A Statement is the subject matter information in an attestation engagement on controls.

ASAE 3150

(^35) Subject matter information means the outcome of measurement or evaluation of the

underlying subject matter against the criteria, i.e., the information that results from applying the criteria to the underlying subject matter.

ASAE 3000 Decision: All definitions included in the glossary. ASAE 3150 and ASAE 3610 definitions are subject-matter specific. In the context of to be included.

Subject matter information (in the context of ASAE 3150) means the outcome of the measurement or evaluation of the underlying subject matter against the criteria. In an assurance engagement on controls the subject matter information is the Statement of the responsible party or evaluator in an attestation engagement or the assurance practitioner’s conclusion in a direct engagement, providing the outcome of their evaluation.

ASAE 3150

Subject matter information (in the context of ASAE 3610) means the information that results from applying the criteria to the underlying subject matter. The subject matter information in an engagement conducted under this Standard is the general purpose water accounting report.

ASAE 3610

(^36) Subject matter or underlying subject matter (in the context of ASAE 3150) means the controls

within the system designed to achieve the control objectives, and, if included in the scope of the engagement, the description of the system, the controls implemented or the controls in operation.

ASAE 3150 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all.

Subject matter or underlying subject matter (in the context of ASAE 3500) means the activity which is evaluated or measured against the identified criteria.

ASAE 3500

(^37) Test of controls (in the context of ASAE 3150 ) means a procedure designed to evaluate the

design, description, implementation or operating effectiveness of controls in achieving the identified control objectives.

ASAE 3150 Decision:^ Both definitions included in the glossary. Each definition is subject-matter specific. In the context of to be included for all. Test of controls (in the context of ASAE 3402) means a procedure designed to evaluate the operating effectiveness of controls in achieving the control objectives stated in the service organisation’s description of its system.

ASAE 3402

Table 3 – All differences between definitions including between suites of standards.

Pending Definition Pending source Comment

(^1) Anomaly means a misstatement or deviation that is demonstrably not representative of misstatements or deviations in a population.

ASA 530

ASAE 3150

Decision: ASA 530 definition only included in the glossary. ASAE 3150 added as a source. Difference between definitions is “misstatement or deviation” in ASA 530.

Anomaly means a deviation in a sample that is demonstrably not representative of deviations in a population.

ASAE 3150

(^2) Applicable criteria (in the context of ASAE 3420) means the criteria used by the responsible party when compiling the pro forma financial information. Criteria may be established by applicable law or regulation or in the absence of established criteria, be developed by the responsible party.

ASAE 3420 Refer to^ #1 in^ Table 2.

Applicable criteria (in the context of ASAE 3410) means that the criteria used by the entity to quantify and report its emissions in the GHG statement.

ASAE 3410

Applicable criteria (in the context of ASAE 3610) means the specific criteria used by the responsible party in preparing and presenting the general purpose water accounting report.

ASAE 3610

(^3) Applicable financial reporting framework means the financial reporting framework adopted by management and, where appropriate, those charged with governance in the preparation of the financial report that is acceptable in view of the nature of the entity and the objective of the financial report, or that is required by law or regulation. The term fair presentation framework means a financial reporting framework that requires compliance with the requirements of the framework and: (a) Acknowledges explicitly or implicitly that, to achieve fair presentation of the financial report, it may be necessary for management to provide disclosures beyond those specifically required by the framework; or

(b) Acknowledges explicitly that it may be necessary for management to depart from a requirement of the framework to achieve fair presentation of the financial report. Such departures are expected to be necessary only in extremely rare circumstances.

The term compliance framework means a financial reporting framework that requires compliance with the requirements of the framework, but does not contain the acknowledgements in (a) or (b) above. (see Fair Presentation framework)

ASA 200 Decision:^ All definitions included in the glossary. ASA 200 as it applies to more than one standard is the primary definition. All other definitions are subject-matter specific. In the context of to be included for all.

Applicable financial reporting framework (in the context of ASA 600) means the financial reporting framework that applies to the group financial report.

ASA 600

Applicable financial reporting framework (in the context of ASRE 2410) means a financial reporting framework that is designed to achieve fair presentation.

ASRE 2410

Applicable financial reporting framework (in the context of ASRS 4450) means the financial reporting framework adopted by the entity in the preparation of general or special purpose financial information of the entity that is acceptable based on the nature of the entity or as required by applicable law or regulation. In Australia, an applicable financial reporting framework that may be used in preparing such financial information is represented by the Australian Accounting Standards which are International Financial Reporting Standards (IFRS) compliant (as issued by the International Accounting Standards Board), or applicable law, such as the Corporations Act 2001. Other frameworks that may be used are the International Financial Reporting Standards, issued by the International Accounting Standards Board and the Generally Accepted Accounting Principles of the United States.

ASRS 4450

(^4) Assertions means representations by management and those charged with governance,

explicit or otherwise, that are embodied in the financial report, as used by the auditor to consider the different types of potential misstatements that may occur.

ASA 315 Decision:^ All definitions included in the glossary. ASA 315 as it applies to more than one standard is the primary definition. All other definitions are subject-matter specific. In the context of to be included for all.

Assertions (in the context of ASAE 3410) means representations by the entity, explicit or otherwise, that are embodied in the GHG statement, as used by the practitioner to consider the different types of potential misstatements that may occur.

ASAE 3410

Assertions (in the context of ASAE 3610) means representations by the responsible party, explicit or otherwise, that are embodied in the general purpose water accounting report, as used by the assurance practitioner to consider the different types of potential misstatements that may occur.

ASAE 3610

(^5) Assurance engagement means an engagement in which an assurance practitioner expresses a

conclusion designed to enhance the degree of confidence of the intended users, other than the responsible party, about the outcome of the evaluation or measurement of a subject matter against criteria. (see Reasonable assurance engagement and Limited assurance engagement ).

ASQC 1 Decision:^ All definitions included in the glossary. ASQC 1 it applies to more than one standard is the primary definition. All other definitions are subject-matter specific. In the context of to be included for all.

Assurance engagement (in the context of ASAE 3000 and ASAE 3610) means an engagement in which a practitioner aims to obtain sufficient appropriate evidence in order to express a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the subject matter information (that is, the outcome of the measurement or evaluation of an underlying subject matter against criteria). Each assurance engagement is classified on two dimensions: (i). Either a reasonable assurance engagement or a limited assurance engagement: a. Reasonable assurance engagement―An assurance engagement in which the assurance practitioner reduces engagement risk to an acceptably low level in the circumstances of the engagement as the basis for the assurance practitioner’s conclusion. The assurance practitioner’s conclusion is expressed in a form that

ASAE 3000

ASAE 3610