Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth analysis of assurance engagements, including their nature, objective, elements, and types. Assurance engagements involve a practitioner expressing satisfaction with an assertion made by one party for the use of another, with the primary objective being to provide intended users with a level of confidence on the reliability and credibility of the subject matter. the three-party relationship, suitable subject matter and criteria, sufficient appropriate evidence, and assurance engagement risk. It also discusses the different types of assurance engagements, such as audits, reviews, and other assurance services.

Typology: Assignments

1 / 54

This page cannot be seen from the preview

Don't miss anything!

1.0 Fundamentals of Auditing And Assurance Services What is Assurance? Assurance is an affirmation and commitment PLAY i MORE INFO

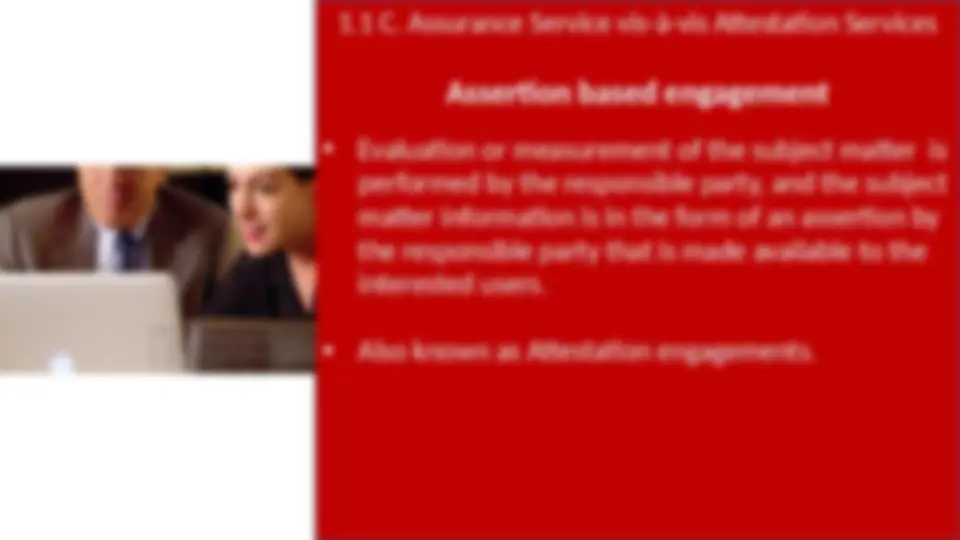

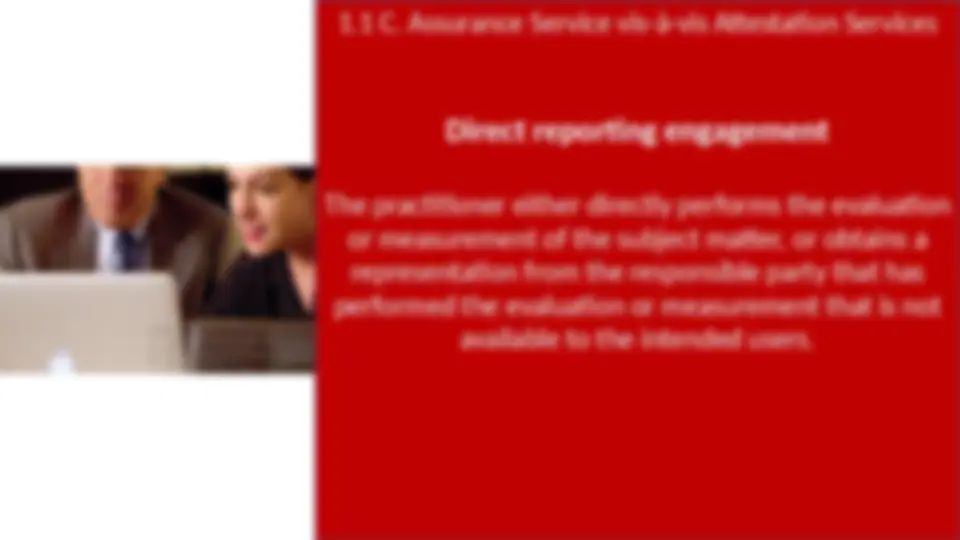

1.1 Introduction to Assurance Engagement What is Assurance Engagement? “Assurance engagement” means an engagement in which a practitioner expresses a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the outcome of the evaluation or measurement of a subject matter against criteria. PLAY i MORE INFO

1.1 A. Nature, objective and elements Objective of Assurance Engagements The primary objective of assurance engagements is the professional accountant’s expression of a conclusion that will provide intended users with a level of assurance on the degree of confidence to place on the reliability and credibility of the subject matter.

1.1 A. Nature, objective and elements The following elements of an assurance engagement are discussed in this section: a. A three party relationship b. An appropriate subject matter; c. Suitable criteria; d. Sufficient appropriate evidence; and e. A written assurance report in the form appropriate to a reasonable assurance engagement or a limited assurance engagement. PERCS

1.1 A. Nature, objective and elements An appropriate subject matter Subject matter

1.1 A. Nature, objective and elements Suitable criteria

1.1 A. Nature, objective and elements Sufficient appropriate evidence

1.1 A. Nature, objective and elements Sufficient appropriate evidence

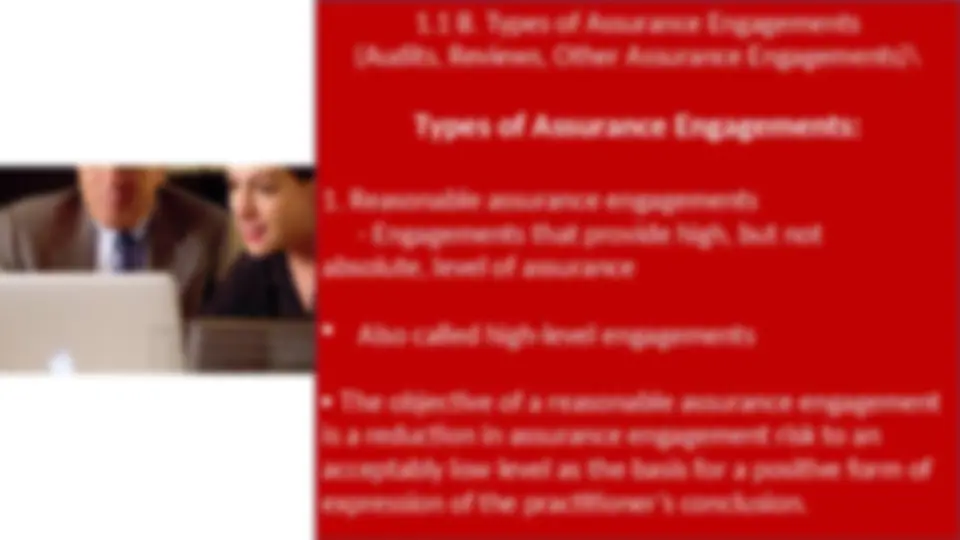

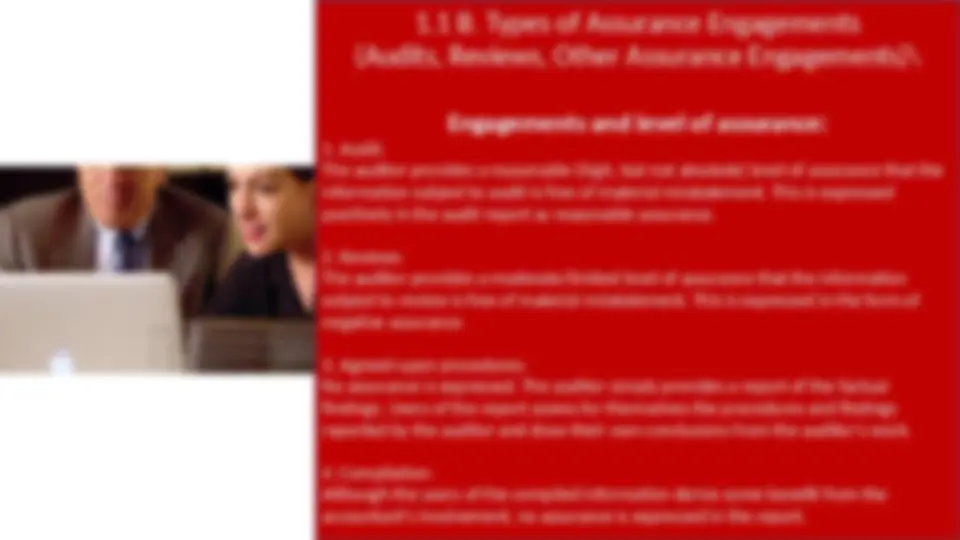

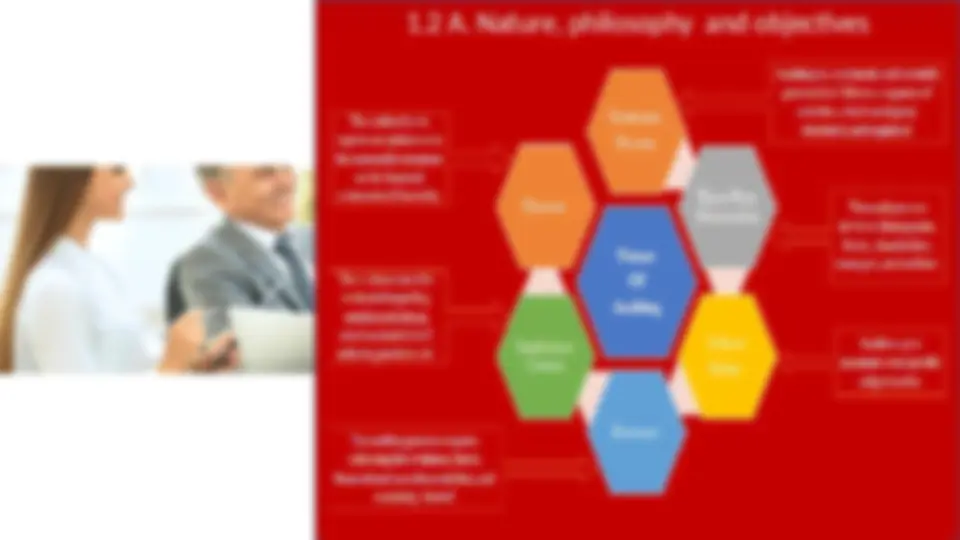

1.1 B. Types of Assurance Engagements (Audits, Reviews, Other Assurance Engagements)

Assurance Engagement Risk: Assurance engagement risk is the risk that the practitioner expresses an inappropriate conclusion when the subject matter information is materially misstated.

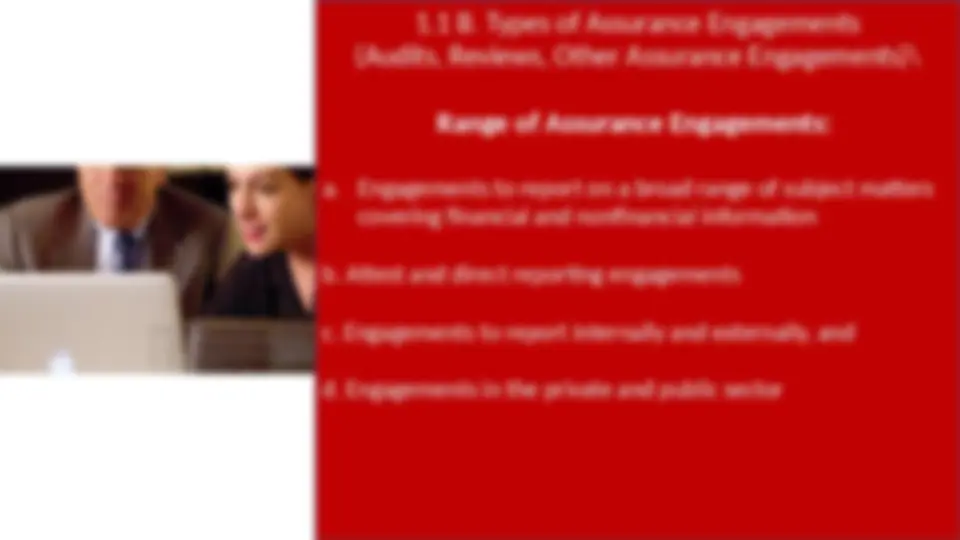

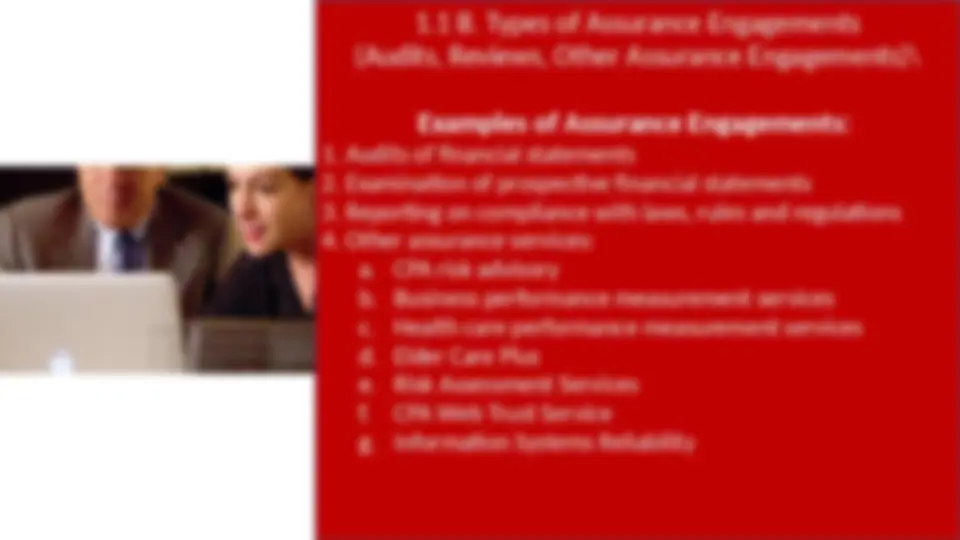

1.1 B. Types of Assurance Engagements (Audits, Reviews, Other Assurance Engagements)

Components of assurance engagement risk :

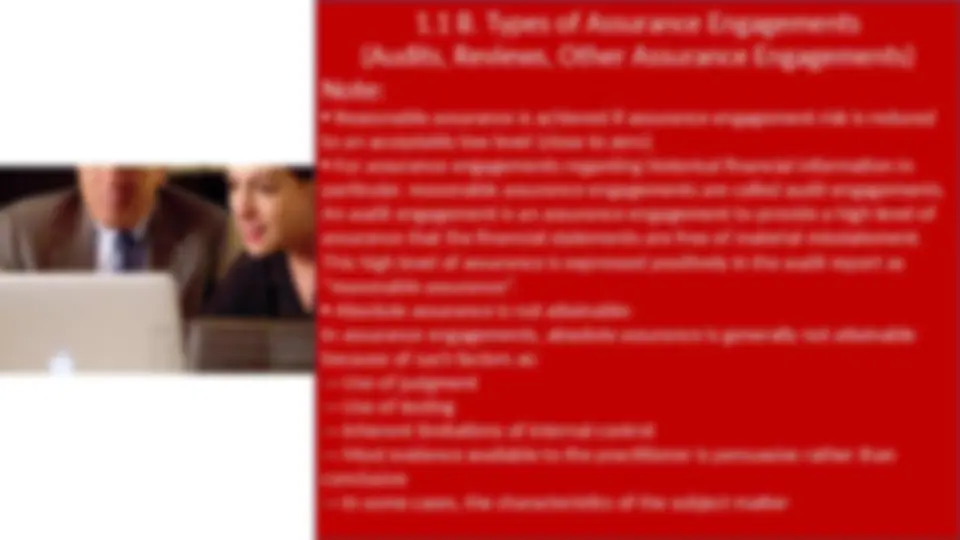

1.1 B. Types of Assurance Engagements (Audits, Reviews, Other Assurance Engagements) Note: · Reasonable assurance is achieved if assurance engagement risk is reduced to an acceptably low level (close to zero). · For assurance engagements regarding historical financial information in particular, reasonable assurance engagements are called audit engagements. An audit engagement is an assurance engagement to provide a high level of assurance that the financial statements are free of material misstatement. This high level of assurance is expressed positively in the audit report as “reasonable assurance”. · Absolute assurance is not attainable: In assurance engagements, absolute assurance is generally not attainable because of such factors as: Use of judgment Use of testing Inherent limitations of internal control Most evidence available to the practitioner is persuasive rather than conclusive In some cases, the characteristics of the subject matter

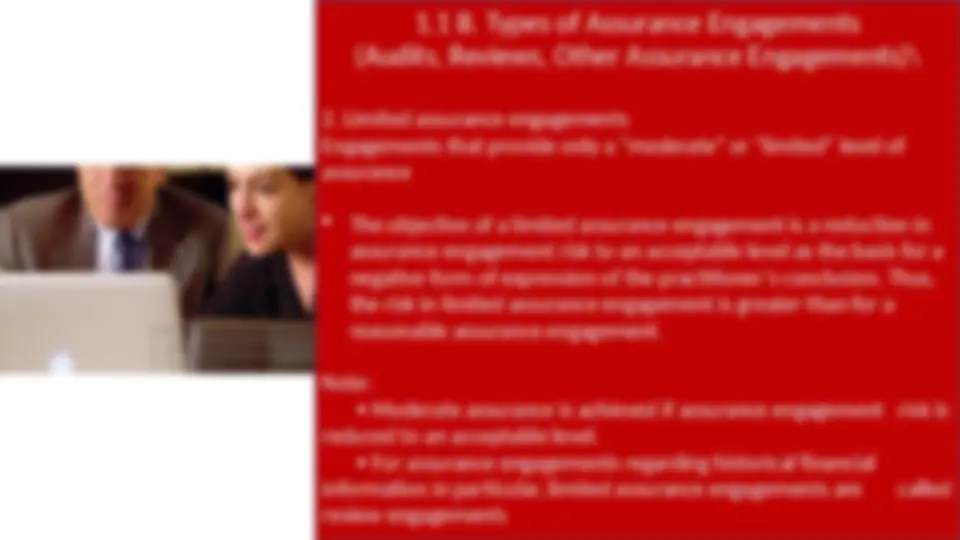

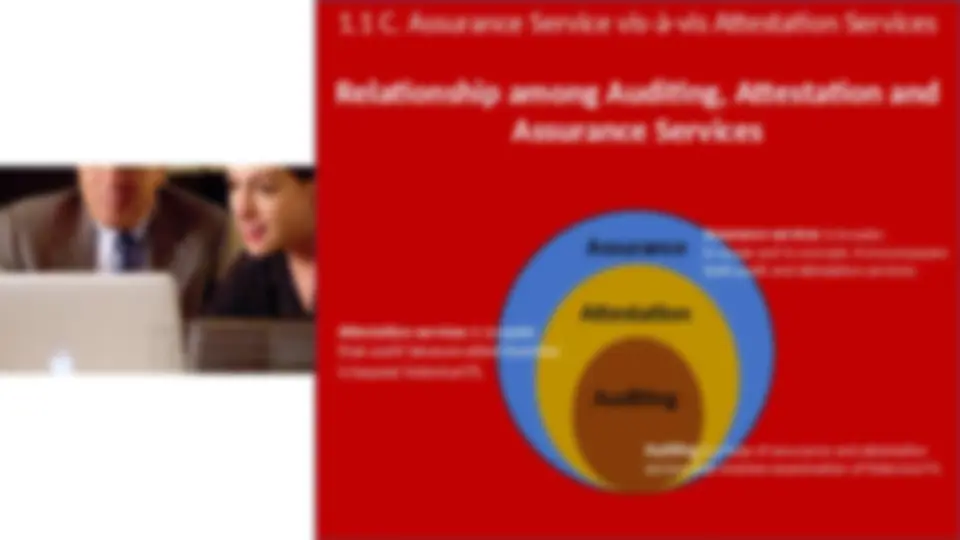

1.1 B. Types of Assurance Engagements (Audits, Reviews, Other Assurance Engagements)\