ABC ANALYSIS

ABC ANALYSIS

(INSIDE OUT)

(INSIDE OUT)

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

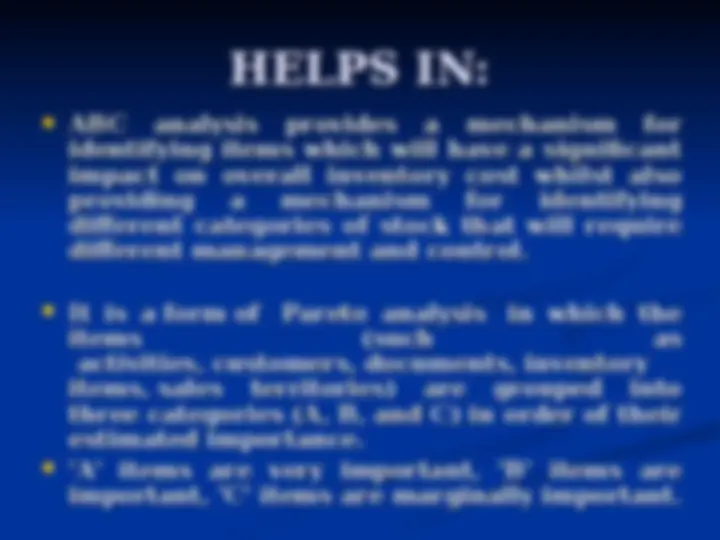

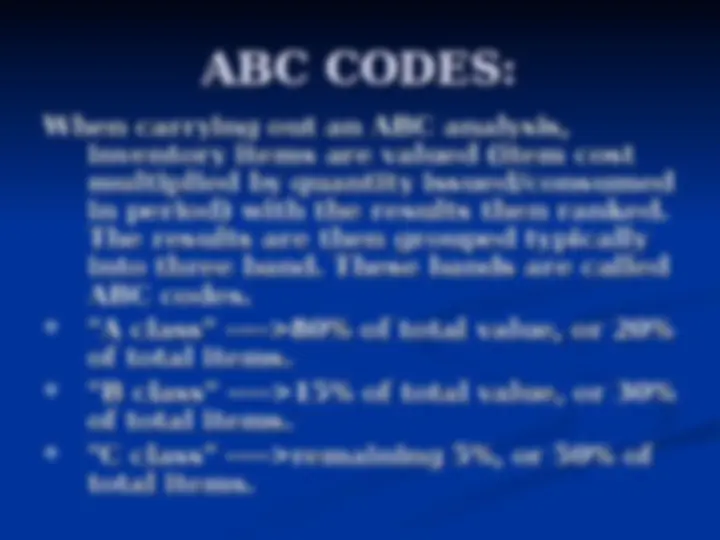

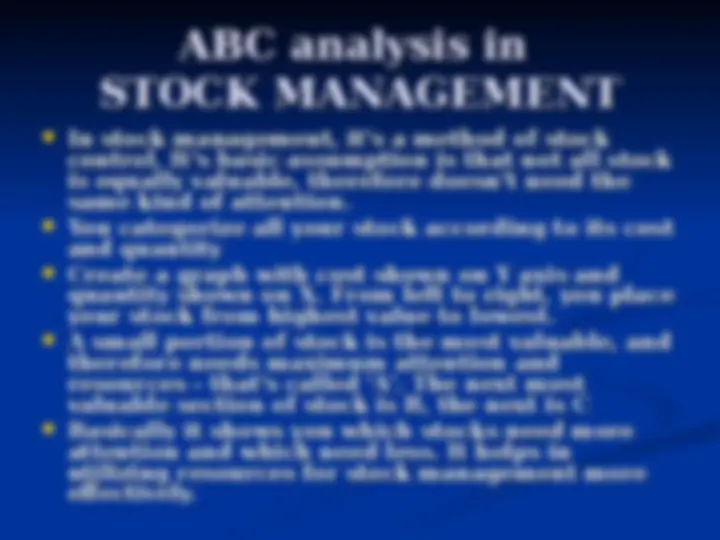

Abc analysis is a business technique used in inventory management and materials management for categorizing inventory based on their importance and value. It helps identify items with significant impact on overall inventory cost and provides a mechanism for differentiating management and control of different categories of stock. The concept, steps, and benefits of abc analysis.

Typology: Study notes

1 / 27

This page cannot be seen from the preview

Don't miss anything!

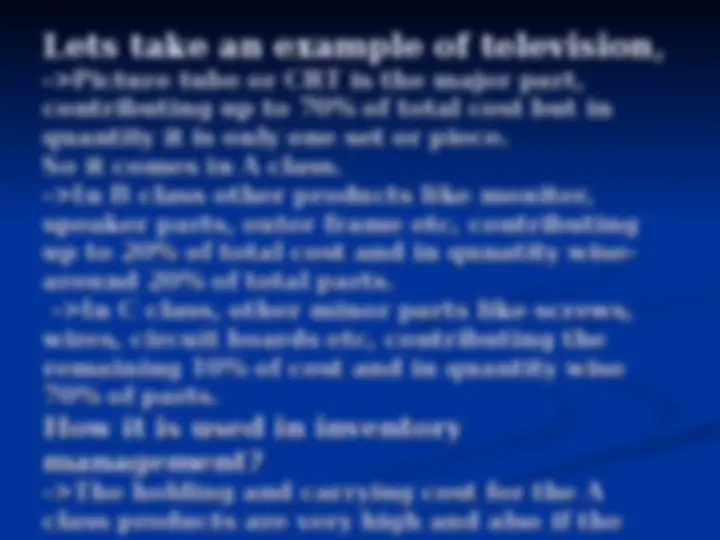

Lets take an example of television,Lets take an example of television,

How it is used in inventory How it is used in inventory management? management?

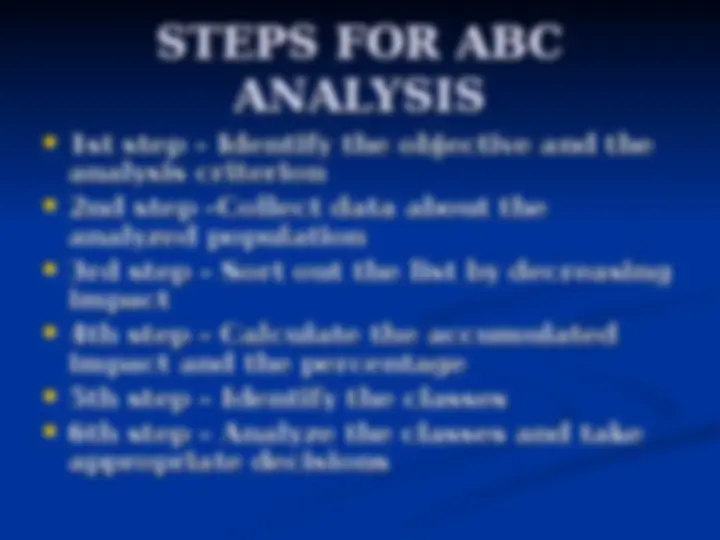

The ABC analysis can be be useful in several steps of The ABC analysis can be be useful in several steps of the the Sourcing Value Chan: Sourcing Value Chan: (^) Demand Identification, to gather the annual spendDemand Identification, to gather the annual spend of a site of a site (^) Demand Aggregation, to gather the annual spend ofDemand Aggregation, to gather the annual spend of several sites several sites (^) Opportunity Assessment, to identify leveragingOpportunity Assessment, to identify leveraging opportunities opportunities The ABC tool is used to identify the “vital few” from The ABC tool is used to identify the “vital few” from the “trivial many”, according to a defined set of the “trivial many”, according to a defined set of criteria. criteria. Different decisions may be taken from the result of Different decisions may be taken from the result of the ABC the ABC analysis analysis

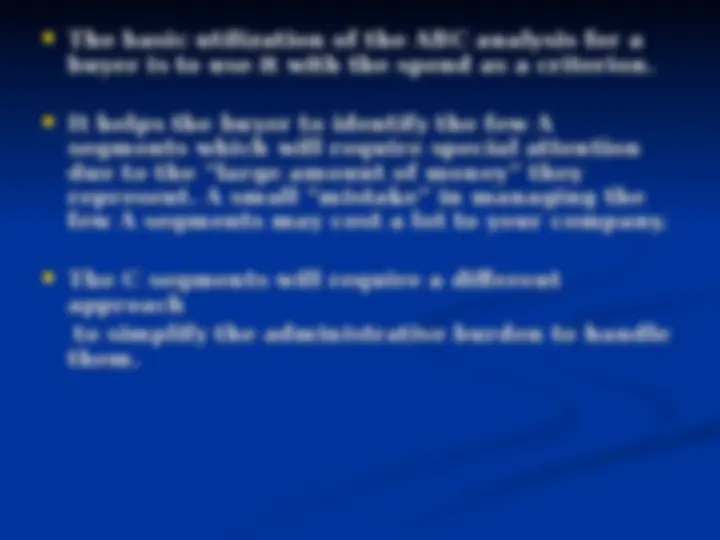

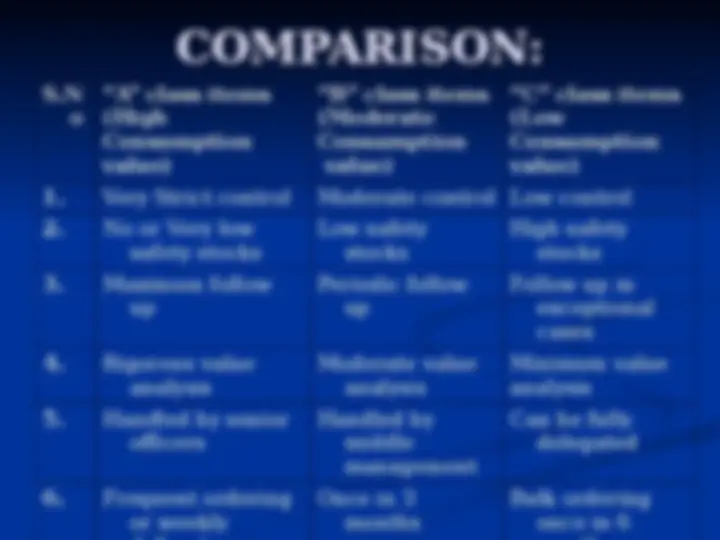

(^) The basic utilization of the ABC analysis for aThe basic utilization of the ABC analysis for a buyer is to use it with the spend as a criterion. buyer is to use it with the spend as a criterion. (^) It helps the buyer to identify the few AIt helps the buyer to identify the few A segments which will require special attention segments which will require special attention due to the “large amount of money” they due to the “large amount of money” they represent. A small “mistake” in managing the represent. A small “mistake” in managing the few A segments may cost a lot to your company. few A segments may cost a lot to your company. (^) The C segments will require a differentThe C segments will require a different approach approach to simplify the administrative burden to handle to simplify the administrative burden to handle them. them.

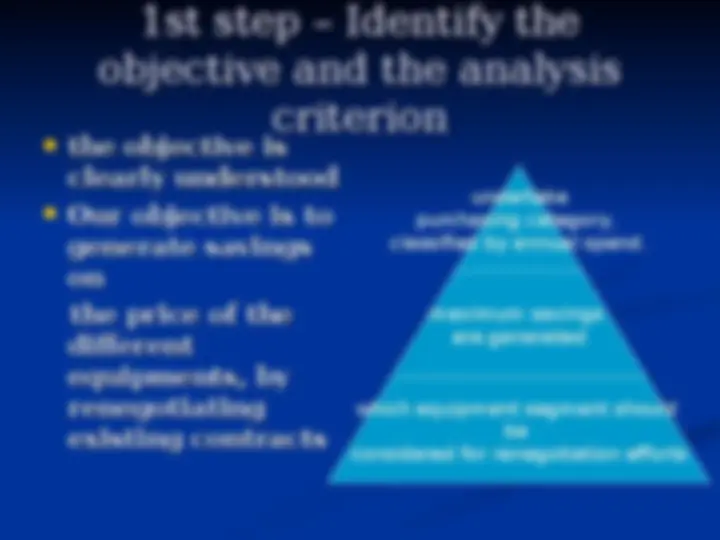

1st step – Identify the1st step – Identify the objective and the analysis objective and the analysis criterion criterion

undertake purchasing category, classified by annual spend. maximum savings are generated which equipment segment should be considered for renegotiation efforts

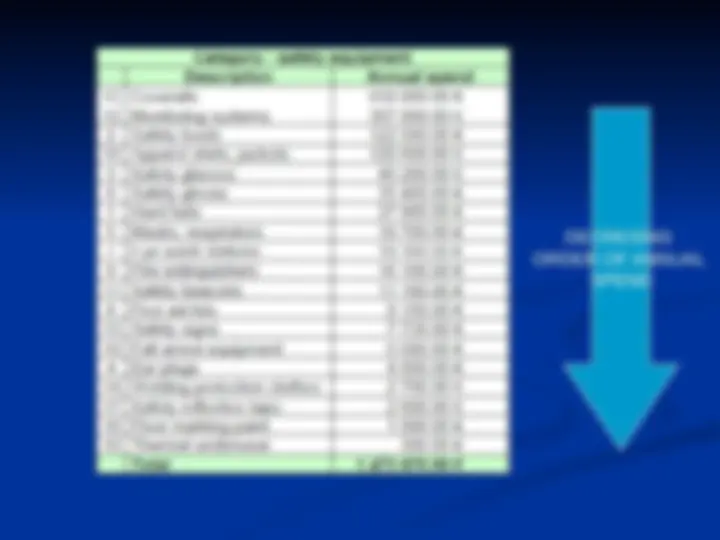

2nd step – Collect data about2nd step – Collect data about the analyzed population the analyzed population Collect the data necessary to carry Collect the data necessary to carry out the out the analysis analysis different safety equipments, anddifferent safety equipments, and corresponding annual spendcorresponding annual spend

3rd step – Sort out the list by3rd step – Sort out the list by decreasing impact decreasing impact Sort out the list of equipment, in Sort out the list of equipment, in decreasing decreasing order,according to our criterion of order,according to our criterion of analysis,i.e. analysis,i.e. annual spend. annual spend.

DECRESING ORDER OF ANNUAL SPEND

5th step – Identify by classes5th step – Identify by classes