Download Accounting test 1 notes and more Cheat Sheet Accounting in PDF only on Docsity!

What is the conceptual Framework:

Financial statements are prepared & presented by many entities around the world to a variety of external users.

They appear similar, but there are variations caused by different legal, social & economic circumstances of the

countries concerned. This has led to a variety of definitions, recognition criteria, measurement principles &

disclosure in the preparation of financial statements.

In 2nd Year we focus on Chapter 4: The elements of Financial Statements

→ The elements of the financial statements are:

- assets, liabilities & equity relating to an entity’s financial position; AND

- income and expenses relating to an entity’s financial performance.

Financial statements portray the financial effects of transactions by grouping them into categories according to

their economic characteristics. These categories are termed the elements of financial statements.

Financial position

The elements directly related to financial position are assets, liabilities & equity.

Assets: A present economic resource controlled by the entity as a result of past events.

An economic resource is a right that has the potential to produce economic benefits.

Three components to the definition:

- right;

- potential to produce economic benefits;

- control.

Liabilities A present obligation of the entity to transfer an economic resource as a result of past events.

Three criteria must be met for a liability to exist:

- entity has an obligation;

- obligation is to transfer an economic resource;

- obligation is a present obligation that exists as a result of past events.

Assets & liabilities: Unit of account

The unit of account is the right or group of rights, the obligation or group of obligations or the group of rights &

obligations, to which the recognition criteria & measurement concepts are applied.

A unit of account is selected to provide useful information.

Example: A group of assets & liabilities may be identified as a single unit if they will be disposed of in a single transaction.

Equity: Residual interest in the assets of an enterprise after deducting all the liabilities.

Financial performance

The elements directly related to performance are income and expenses.

Income: Increase in assets or decreases in liabilities that result in increases in equity, other than those relating to

contributions from holders of equity claims.

Expenses: Decrease in assets or increases in liabilities that result in decreases in equity, other than those relating

to distributions to holders of equity claims.

Steps when answering:

- Definitions- from above

- Application- Link the definition to the question

Conclusion- Link to definition eg: Based on the definition of an asset, the machinery can be considered an asset and

recognised in the financial statements under…

NB: LOOK AT PRACTICE SOLUTIONS GIVEN AND SEE HOW QUESTIONS WERE ANSWERED,

The elements of financial statements:

Recognise an element if it:

- Meets the definition

- Satisfies recognition criteria.

This is NOT A STANDARD

therefore does NOT

override other IFRS

statements

IN CASE OF CONFLICT –

IFRS PREVAILS

The Conceptual Framework-class

notes

Tuesday, 14 March 2023 16:

LU1- Conceptual Framework Page 1

- LU1- Conceptual Framework Page

- LU1- Conceptual Framework Page

The Conceptual Framework and IAS 1: Presentation of

Financial Statements

Overview of the framework

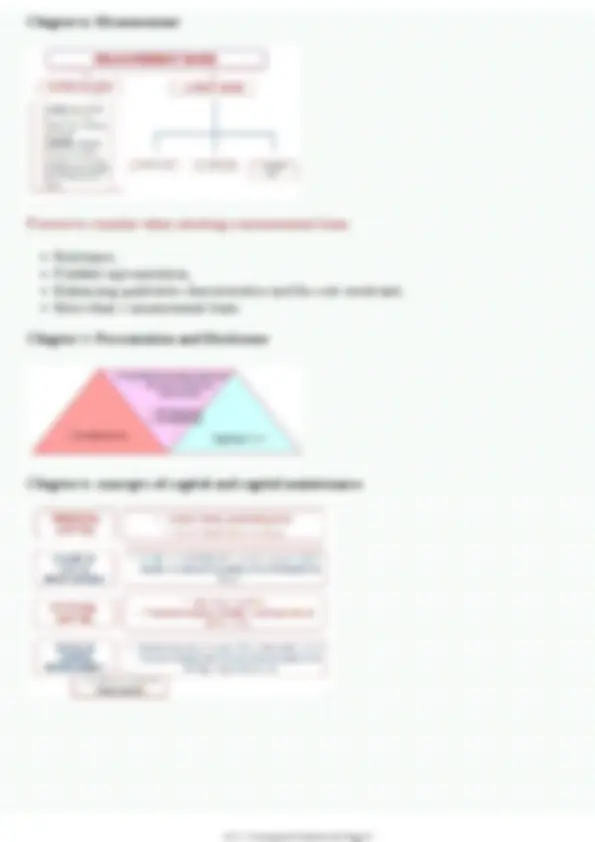

Chapter 1: Objective of general purpose financial reporting

- PURPOSE OF CONCEPTUAL FRAMEWORK:

Assists IASB to develop new IFRS and review existing IFRS;

- Assists preparers of AFS where there is no IFRS;

- Assists in selecting accounting policies;

- Assists all parties in understanding and interpreting the AFS.

The purpose of the conceptual framework is therefore to outline the concepts that underlie the preparation and

presentation of financial statements for external users

Objective of general purpose financial reporting is:

- To provide financial information about the reporting entity;

- that is useful to existing and potential investors, lenders and other creditors;

- in making decisions about providing resources to the entity.

Buying, selling or holding equity and debt instruments

Providing or settling loans/ other forms of credit

Voting rights

The following information is needed in order to make decisions:

- Economic resources of the entity, claims against the entity and changes to these resources;

- how efficiently and effectively the entity’s managing/governing board have discharged their responsibilities.

Economic Resources and Claims help to identify :

- Financial strengths and weaknesses

- Liquidity and Solvency

- Success in obtaining finance

- Priorities of payments

Changes in economic resources and claims:

- Financial performance

- Issuing of debt/equity instruments

Use of Entity’s Resources:

- Assess the stewardship of the resources

Accrual Accounting: Depicts the effect of

transactions and occurrences in period in

which they occur and not on a cash basis

Past Cash Flows:

A ssess entity’s ability to generate future

cash flows and managements

stewardship of economic resources.

What is the Status of the Conceptual

Framework:

This is NOT A STANDARD

therefore does NOT override other IFRS

statements

IN CASE OF CONFLICT – IFRS

PREVAILS

NOTES FROM SLIDES

Tuesday, 21 March 2023 18:

LU1- Conceptual Framework Page 5

Chapter 4: The elements of financial statements

Recognition, measurement, presentation and disclosure

Recognise an element when it:

(NB – Exam technique)

Satisfies the

DEFINITION:

ASSET

A present economic resource controlled by the entity as a result of past events.

PRESENT ECONOMIC RESOURCE :

An economic resource is a right that has the potential to produce economic benefits

Right

Correspond to the obligation of another party:

Rights to receive cash, goods or services etc.

Rights that do not correspond: rights over

physical objects, rights to use intellectual

property

Potential to produce economic benefit:

Receiving contractual cash flows

- Exchanging ER under favourable terms

Produces cash inflows/avoid cash outflows

- Receiving cash

- Extinguishing liabilities

CONTROLLED BY THE ENTITY :

Present ability to direct the use and obtain the FEB and present

ability to prevent others from directing use and the FEB

To control – the FEB from the resource must flow to the entity,

directly or indirectly, rather then to another party

- Arises form an ability to enforce legal rights

AS A RESULT OF PAST EVENTS :

Before year end

LIABILITY

A present obligation of the entity to transfer an economic resource , as a result of past events.

OBLIGATION

Duty/responsibility that an entity

has no practical ability to avoid.

Established by contract,

legislation and legally

enforceable.

Customary practices , published

policies – constructive obligations.

TRANSFER ECONOMIC RESOURCE

Obligation must have POTENTIAL to require the entity

to transfer ER.

Potential to exist – does not need to be certain or even likely

Obligations to transfer include:

Obligation to pay cash; ○

○ To deliver goods/services;

Exchange resources under UNFAVOURABLE

terms.

PAST EVENTS

- Entity has already obtained economic benefits

As a consequence, will have to transfer the economic

resources (things happening in the past that result in present

obligation)

Assets and Liabilities: Unit of Account:

- Rights / groups of rights to which recognition and measurement criteria are applied.

- Selected to provide more useful information

LU1- Conceptual Framework Page 7

EQUITY

Residual interest in the assets of an enterprise after deducting all the liabilities.

INCOME

Increase in assets or decreases in liabilities that result in increases in equity, other than those relating to

contributions from holders of equity claims.

EXPENSES

Decrease in assets or increases in liabilities that result in decreases in equity, other than those relating to

distributions to holders of equity claims.

Chapter 5: Recognition and Derecognition

Recognition criteria

- An item can only be recognised if it meets the DEFINTION and RECOGNITION CRITERIA

An item which meets the definition of an element should be recognised ONLY if the recognition provides

users with information that is:

○ RELEVANT ; and

○ FAITHFULLY REPRESENTED

APPLY JUDGMENT and CONCLUDE.

RELEVANCE as recognition criteria

a. Existence Uncertainty

○ May result in asset/liability not being recognized.

○ Uncertainty should still be disclosed.

Low probability of inflow

○ Can exist even if probability of inflow is low.

○ Disclose relevant information (notes).

b.

FAITHFUL REPRESENTATION as recognition criteria

Measurement uncertainty

- Estimations are a normal part of accounting.

If uncertainty is so high, recognition of element might question the faithful representation of the item.

○ Include explanatory information or just disclose

- Faithful representation involves recognition, measurement, presentation and disclosure.

Derecognition

Derecognition is the removal or part removal of a recognised asset or liability from the statement of

financial position.

Asset:

- Normally when the entity loses control.

Liability:

- Normally when the entity no longer has a present obligation.

LU1- Conceptual Framework Page 8

Objective and Components of Financial Statements

IAS 1 covers the presentation of financial statements, which includes the layout of the financial statements,

as well as the considerations that have to be taken into account when preparing the financial statements.

The objective of financial statements is to provide financial information regarding the position (statement

of financial position) , the results for the financial year (statement of profit or loss and other

comprehensive income) and cash flows of the business in order to provide the end users with sufficient

information to make financial and business decisions.

Responsibility for Preparation and Presentation of Financial Statements

- Board of directors is responsible for the preparation and presentation of financial statements

Components of Financial Statements Includes:

- **A statement of financial position; (SFP)

- A statement of profit or loss and other comprehensive income;(P+L)

- A statement of changes in equity;(SOCIE)

- A statement of cash flows;**

- Accounting policies and explanatory notes;

- A statement of financial position at the beginning of the earliest comparative period.

Going concern

When preparing financial statements, management

should make an assessment of an enterprise’s ability

to continue as a going concern. Financial statements

should be prepared on a going concern basis unless

management:

Accrual basis

An enterprise should prepare its financial statements,

except for cash flow information, under the accrual

basis of accounting.

Other comprehensive income for the year(OCI)

This includes:

▫ revaluation surpluses and deficits ( also has column in SOCIE

▫ Gains on financial assets at fair value through OCI - not help for trading investments

NOTES:

Mark to Market reserve:

(QN will ask to calculate amount of shares that were bought to determine if it is a sub or not)

Income from investments:

1. Investment in Subsidiary: cost value @all times. Measured in SFP @ year end.

2. Investment in listed Company:

Currant asset- held for trading investment (usually Ltd )

Account name: Financial assets at fair value through P+L

Remeasurement of investment goes in other income / other expenses in I/S

Reflected in PBTN

3. Investments in Unlisted Company:

Non- currant asset- not held for trading(usually Pty Ltd)

Goes in Mark to market place in I/S- Gains through financial assets at FV through OCI

Mark to market reserve has its own column in SOCIE

International Accounting Standards

Tuesday, 14 March 2023 16:

LU2- IAS Page 10

Mark to market reserve has its own column in SOCIE

LU2- IAS Page 11

Expenses

Significant (material) items

Fair value adjustment – financial asset at fair value through profit or loss

Loss on the sale of non-current assets

Depreciation on non-current assets ( all for current year)

Staff cost

Auditors’ remuneration

- Auditing fees

- Fees for other services, e.g. accounting services

- Expenses

Income tax expense

R

SA Normal tax

Remuneration of directors’ and prescribed officers:

Name Directors

Fees

Salary Other

benefits

Pension

Fund

Loss of

Office

Less: Paid

by

subsidiaries

Total

Executive directors

Managing director

Marketing director etc

Non- executive directors

Chairman

Directors without specific

functions

Prescribed officers

Secretary

etc

Other benefits

Name Travel/ Entertainment Total

Note: if an employee works at the parent company and at the subsidiary their payments will be added

and it together on the remuneration note, other employees of the subsidiary who do not work for the

parent company will not be shown

LU2- IAS Page 13

Statement of Changes in Equity for year ended…(SOCIE)

OSC 10% cumulative

pref shares

125 non-

cumulative pref

shares

Retained

earnings

Mark to

Market

reserve

Revaluation

surplus

Total

Balance @beg of year

Ordinary shares issued

10% cumul. pref shares issued

12% non- cumul. pref shares

issued

Capitalisation issue (if have)

Total Comp. Income(I/S)

Dividends:

Balance @ end of the year

Note :

A Capitalisation issue occurs when a business does not have sufficient funds to pay dividends to shareholders and

therefore could give shareholders free shares in the company. This comes out of retained earnings and goes to the

type of shares they are being offered.

Ordinary dividend:

Preference dividend:

- Cumulative vs Non- cumulative pref shares

Cumulative pref: when no money is available to pay a div in one year, when money is available, div is paid for

current and previous years that were missed

Non- cumulative pref: only pay for current year

Redeemable: company has to pay back value of shares to shareholders at specific date( usually 5 years)

Non- redeemable: don’t have to pay back

LU2- IAS Page 14

Goods or services may include, but are not limited to:

- Sale of goods;

- Resale of goods;

- Resale of rights to goods or services;

- Performing a contractually agreed task;

- Providing goods or services when necessary or when requested (e.g. software updates or delivery on demand);

- Providing a service (directly or through an agent);

- Granting rights to goods or services in the future;

- Constructing, manufacturing or developing an asset for a customer;

- Granting licenses;

- Granting options to acquire additional goods or services.

Revenue is recognised when an entity has satisfied a performance obligation by transferring a promised good or

service to a customer. An asset is transferred when the customer has control of the asset. Performance obligations

may be transferred over a period of time if:

- The customer simultaneously receives and consumes the benefits; OR

- The entity’s performance creates or enhances an asset that the customer controls; OR

- The entity’s performance does not create an asset with an alternative use (to the entity) and the entity has the

enforceable right to receive payment for performance to date.

Step 3: Determine the transaction price.- selling price

Variable consideration

Time value of money

Non-cash consideration

Consideration payable to

customers

The transaction price is the amount of consideration an entity expects to be entitled to in exchange for

transferring the promised goods or services (excluding amounts collected on behalf of third parties, e.g. sales

taxes or value added taxes).

The transaction price may be affected by the nature, timing, and amount of consideration, including:

- **Variable consideration

- Significant financing components;

- Non-cash consideration;

- Amounts payable to the customer (e.g. refunds and rebates).**

Variable consideration

The entity must estimate the amount of consideration it expects to receive in exchange for transferring the goods

or services. Consideration may vary due to discounts, rebates, refunds, credits, concessions, incentives,

performance bonuses, penalties, and contingent payments.

At each reporting date the entity must estimate (and update) the amount of variable

consideration using either:

- Expected value method: based on probability weighted amounts within a range

(i.e. for large number of similar contracts);

- Single most likely amount: the amount within a range that is most likely to eventuate (i.e. where there are few

amounts to consider);

- Variable consideration is only recognised if it is highly probable that a subsequent change in its estimate would

not result in a significant revenue reversal (i.e. a significant reduction in cumulative revenue recognised).

An entity must recognise a refund liability if it expects to refund some or all of the consideration to a customer.

Significant financing components

Consideration is adjusted for the effects of the time value of money, if the timing of payments in the contract

provides either the customer or the entity with a significant benefit of financing the transfer of goods or services

to the customer. The transaction price is adjusted to reflect the cash selling price at the point in time control of

the goods or services is transferred.

LU3- IFRS 15 Page 16

A significant financing component can either be explicit or implicit. Factors to consider

include:

- Difference between the promised consideration and the cash selling price; and

- Combined effect of interest rates and length of time between transfer of control of the goods or services and

payment.

A significant financing component does not exist when:

- The timing of the transfer of control of the goods or services is at the customer’s discretion; OR

- The consideration is variable with the amount or timing based on factors outside of the control of the parties;

OR

- The difference between the consideration and cash selling price arises for other non-financing reasons (i.e.

performance protection).

The discount rate used must reflect credit characteristics of the party receiving the financing and any

collateral/security provided. A significant financing component is not identified if the entity expects that the

period between transfer of goods or services and payment is one year or less.

Non-cash consideration

Consideration may include non-cash amounts. These are measured at fair value. If the amount cannot be

estimated the non-cash consideration is the stand-alone selling price of the goods or services promised less cash

consideration.

Amounts payable to the customer

Includes cash paid (or expected to be paid) to the customer (or the customer’s customers) as well as

credits or other items such as coupons and vouchers.

These amounts are accounted for as a reduction in the transaction price, unless payment is in exchange for a

good or service received from the customer. Such payments are treated as a normal purchase from a supplier.

If consideration payable to a customer is accounted for as a reduction in the transaction price, the reduction in

revenue is recognised when either of the following occurs:

- The entity recognises revenue for the transfer of the goods or services; OR

- The entity promises to pay the consideration.

NOTE: USE TEXTBOOK FR STEP 2&

Chapter 10

Step 4: Allocate the transaction price to the performance obligations.

Allocation based on

stand-alone selling price

Allocate discounts

Allocate variable

consideration

Step 5:Recognise revenue when performance obligation is satisfied

Control

Over a period of time

At a point in time

LU3- IFRS 15 Page 17

Step 1: Identify the contract

A contract with a customer only exists if ALL of the following criteria are met:

- All parties have approved the contract (in writing, orally, or implied);

- Each party can identify their rights in terms of goods or services to be transferred;

Payment terms can be identified;

- Contract has commercial substance;

- It is probable that the consideration receivable will be collected.

The criteria are assessed at inception of the contract & only reassessed if there is a significant change in facts &

circumstances.

Step 2: Identify the performance obligations

A performance obligation is a promise in a contract to transfer to the customer either:

A good or service that is distinct; OR

A series of distinct goods or services that are substantially the same & have the same pattern of transfer to

the customer.

To be distinct both of the following criteria must be met:

The customer can benefit from the good or service on its own or together with other readily available

resources;

The promise to transfer a good or service is separable from other promises in the contract.

Step 3: Determine the transaction price

The transaction price is the amount of consideration an entity expects to be entitled to in exchange for the goods

or services.

The nature, timing, & amount of consideration may affect the transaction price including:

- Variable consideration;

- Significant financing components (time value of money adjustment if > 1year);

- Consideration payable to a customer (e.g. refunds & rebates);

- Non-cash consideration (measured at FV);

Variable consideration:

Variable consideration encompasses any amount that is variable under a contract. The amount of

consideration received under a contract can vary due to discounts, rebates, refunds, credits, incentives,

performance bonuses, penalties, contingencies, price concessions (including concessions due to doubts about the

collectability based on the customer’s credit risk) and other similar items. If the consideration of a contract is

variable, then the entity has to estimate the amount to which it will be entitled to after delivering the promised

goods or services. An entity estimates an amount of variable consideration by using either the expected value

(probability weighted method) or the most likely amoun t (single most likely amount in a range), depending on

whichever has the better predictive value. This estimate is however limited to the extent that it is highly

probable that its inclusion of this estimate in revenue will not result in a significant revenue reversal in the future

as result of a re-estimation.

To be distinct both of the following criteria

must be met:

The customer can benefit from the good

or service on its own or together with

other readily available resources;

The promise to transfer a good or service

is separable from other promises in the

contract.

LU3- IFRS 15 Page 19

Variable consideration continued:

Variable considerations include that an entity shall recognise a refund liability if the entity receives consideration

from a customer and expects to refund a portion of, or all of, the consideration to the customer.

The time value of money :

In determining the transaction price, the entity has to adjust the amount of consideration for the effects of the

time value of money if the contract includes a significant financing component. Revenue is therefore recognised

at an amount that reflects the price that a customer would have paid for the goods and services if the customer

had paid cash when the goods and services transfer to the customer.

Determining if the financing component is significant :

Even though the contract has a significant financing component, it is not necessary to separate the financing

component if the period between transfer of the goods or services and receipt of payment is expected to be less

than one year.

Measuring and recognising the financing component :

The discount rate to be used is the rate that would be reflected in a separate financing transaction between the

entity and the customer at contract inception. The discount rate should reflect the customer’s credit risk. After

the contract inception, the discount rate is not adjusted for changes in interest rates or other circumstances. The

effects of financing (interest) are presented separately from revenue in the statement of profit or loss and other

comprehensive income. Interest is accrued from the date that the entity recognised a contract asset (i.e. when the

right to receive consideration is recognised).

look at 10.7 in TB

Non-cash consideration

If the consideration received by the entity is not in cash, then the entity measures the non cash consideration at

fair value (IFRS 13, Fair Value Measurement). If the entity cannot reasonably estimate the fair value of the non-

cash consideration, it measures the considerations indirectly by reference to the stand-alone selling price of the

goods or services promised to the customer.

Step 4: Allocate the transaction price to each performance obligation

The transaction price (step 3) is allocated to each performance obligation (step 2) based on the stand-alone selling

price of each performance obligation.

If the stand-alone selling price(s) are not observable, they are estimated.

A stand-alone selling price is the price at which an entity would sell a promised good or service separately to a

customer.

Step 5: Recognise revenue as each performance obligation is satisfied

Transaction price allocated to each performance obligation (step 4) is recognised as & when the performance

obligation is satisfied, either:

Over time OR at a point in time.

This occurs when control of the goods or service is transferred to the customer through:

Ability to obtain substantially all the remaining benefits from the asset.

Factors to consider when assessing transfer of control:

- Entity has present right to payment for the asset

- Entity has physically transferred the asset

- Legal title of the asset

- Risks and rewards of ownership

- Acceptance of the asset by the customer.

LU3- IFRS 15 Page 20