Download IS-LM Model vs. Keynesian Cross: Comparing Fiscal Policy and the Zero Lower Bound and more Slides Macroeconomics in PDF only on Docsity!

Aggregate Demand II: Applying

the IS - LM Model

Applying the IS-LM Model

• Section 12-1 shows how the IS-LM model that

we studied in Chapter 11 can be applied to

understand how an economy copes with

disturbances (or, shocks) in the short run

• Section 12-3 extends section 12-1 by looking

closely at

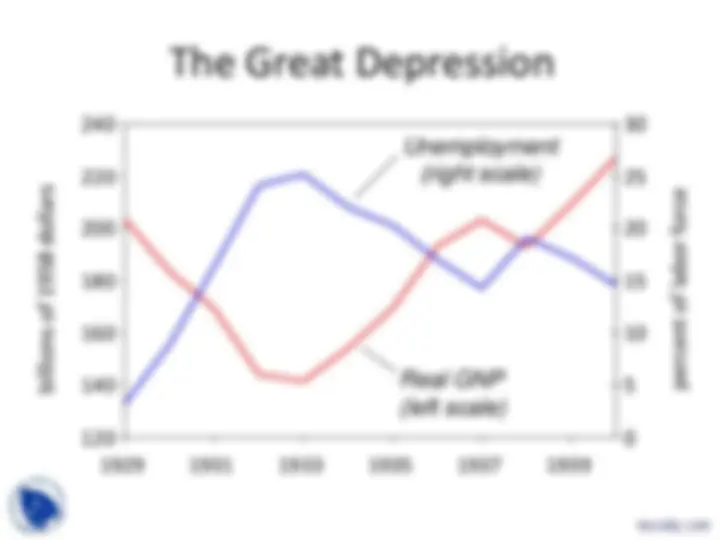

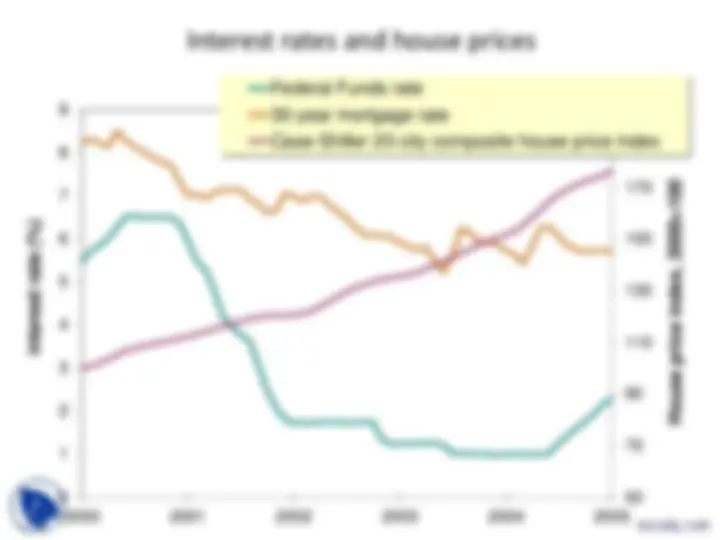

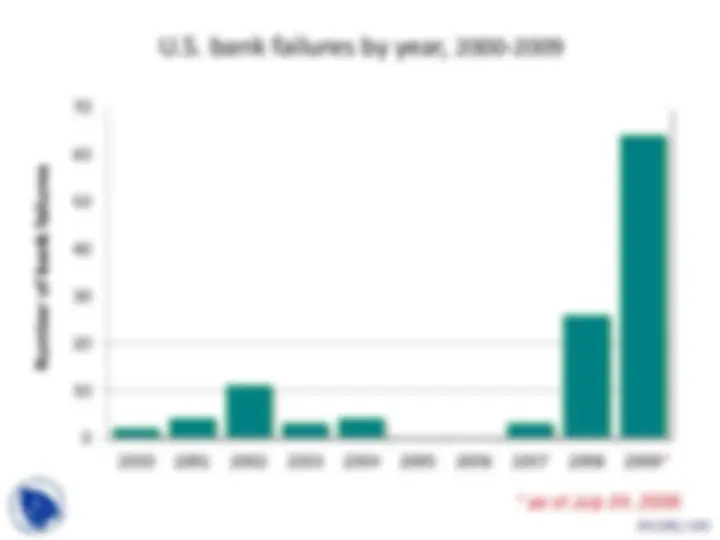

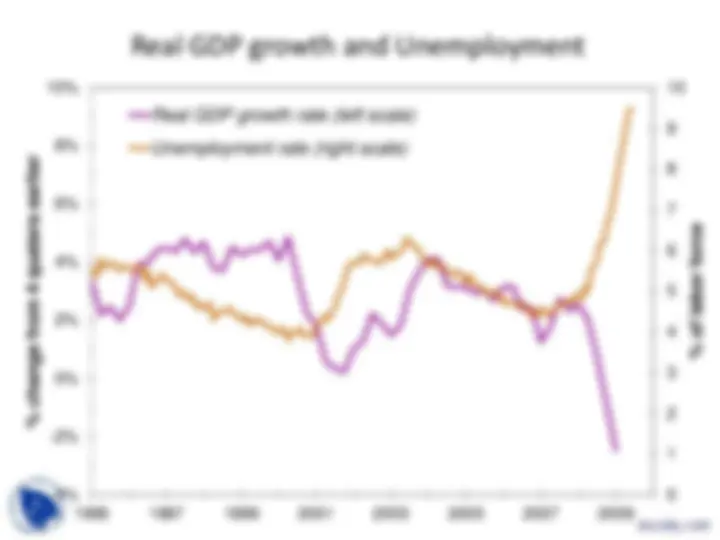

- The Great Depression of the 1930s, and

- The Great recession of 2008-

The IS-LM Model: Ch. 11 Summary

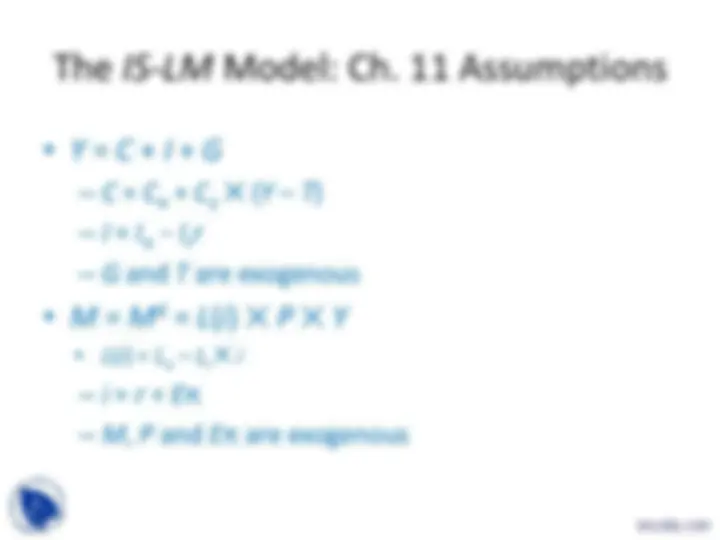

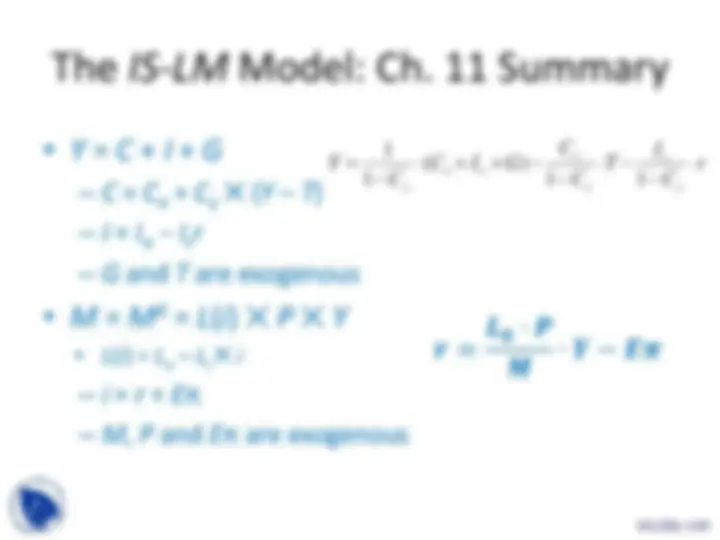

• Y = C + I + G

- C = C o + C y ✕ ( Y – T )

- I = I o − I r r

- G and T are exogenous

• M = M d^ = L ( i ) ✕ P ✕ Y

- L ( i ) = L o – L i ✕ i

- i = r + E π

- M , P and E π are exogenous

r C

T I C

C C I G C

Y y

r y

y o o y

1 1

( ) 1

1

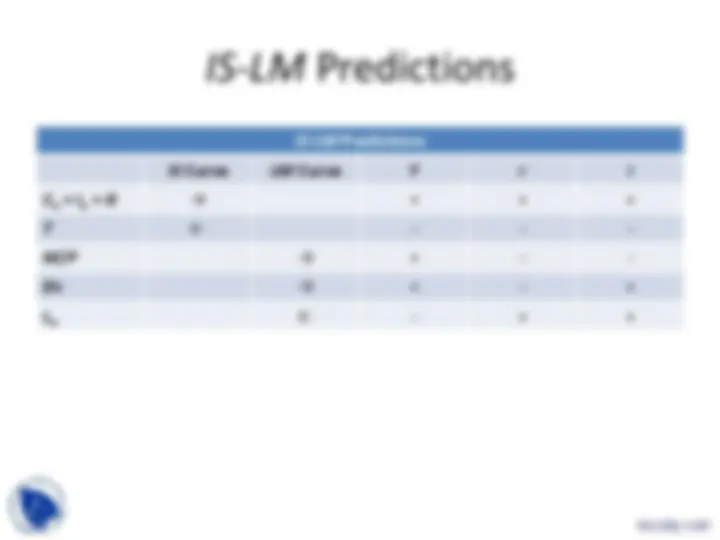

The IS-LM Model: Ch. 11 Summary

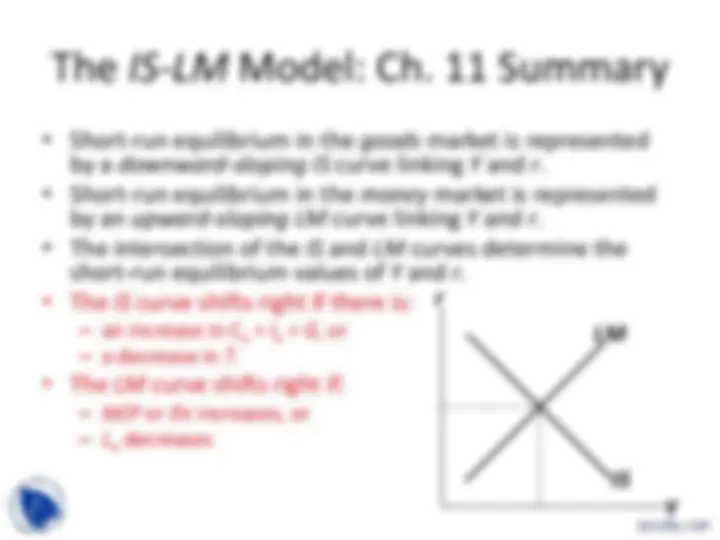

- Short-run equilibrium in the goods market is represented

by a downward-sloping IS curve linking Y and r.

- Short-run equilibrium in the money market is represented

by an upward-sloping LM curve linking Y and r.

- The intersection of the IS and LM curves determine the

short-run equilibrium values of Y and r.

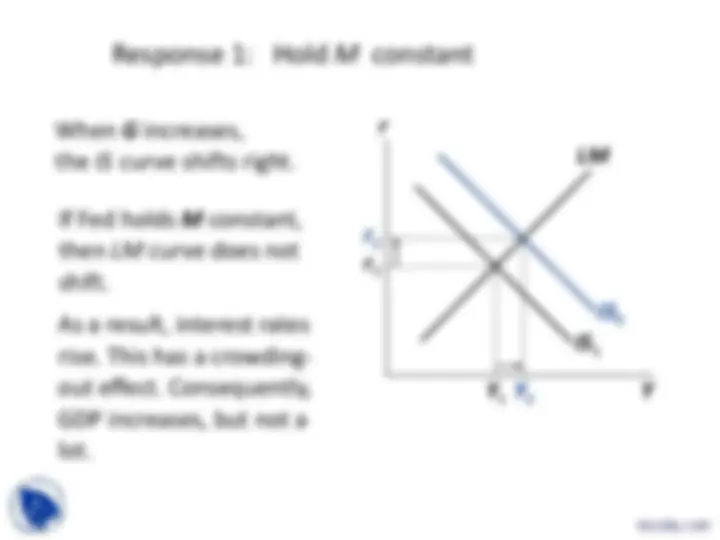

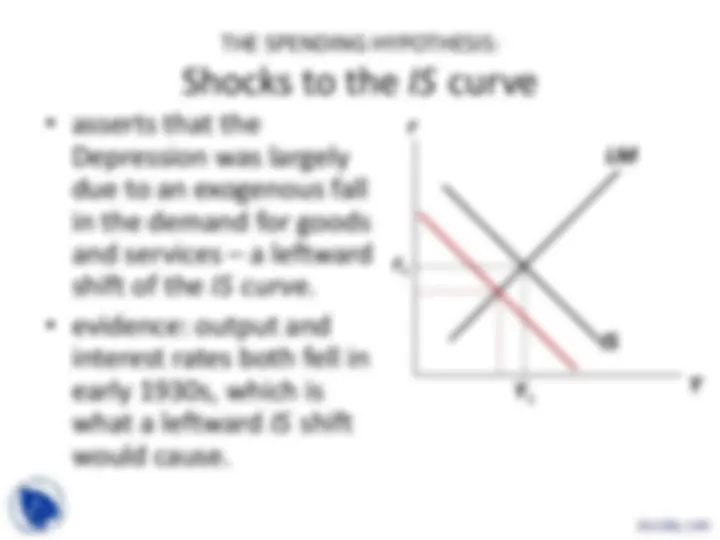

- The IS curve shifts right if there is:

- an increase in C o + I o + G , or

- a decrease in T.

- The LM curve shifts right if:

- M / P or E π increases, or

- L o decreases

Y

r

IS

LM

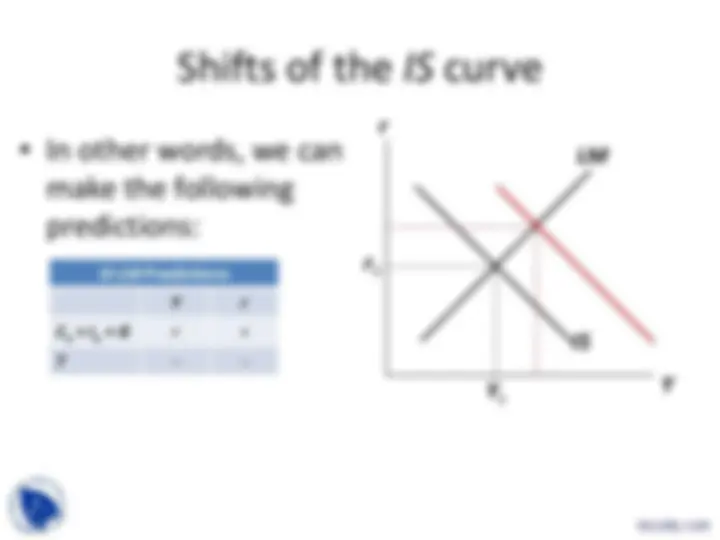

Shifts of the IS curve

- Recall from Chapter 11 that

- the consumption function is C ( Y – T ) = C o + C y ✕ ( Y – T ), and

- The investment function is I ( r ) = I o – I r ✕ r

- Recall also that the IS curve shifts right if there is: - an increase in C o + I o + G , or - a decrease in T.

- As a result, both Y and r increase

IS

Y

r LM

r 1

Y 1

Shifts of the IS curve

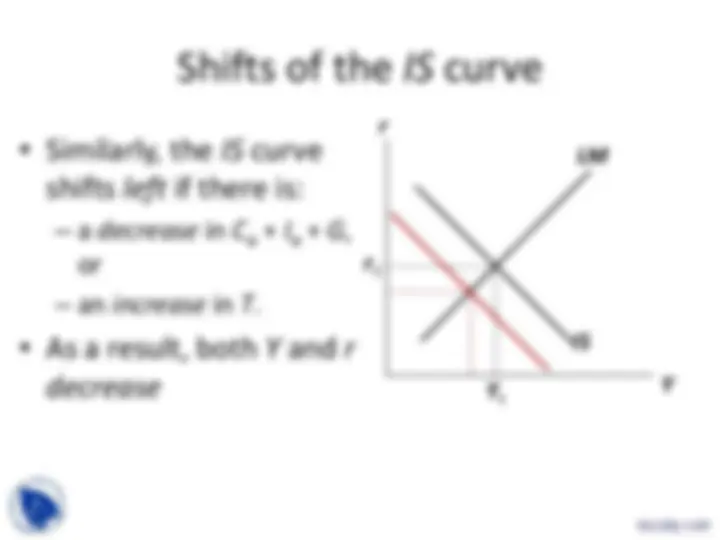

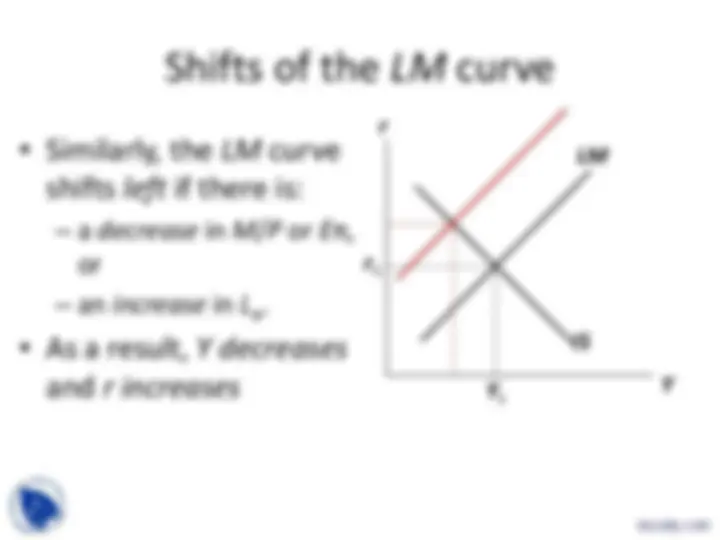

• Similarly, the IS curve

shifts left if there is:

- a decrease in C o + I o + G , or

- an increase in T.

• As a result, both Y and r

decrease

IS

Y

r LM

r 1

Y 1

Ch. 11: Comparing fiscal policy in the

Keynesian Cross and in the IS Curve

r C

I T C

C C I G C

Y y

r

y

y o o y

1 1

( ) 1

1

T C

C C I G C

Y y

y o o y

1

( ) 1

1

Keynesian Cross

IS Curve

In the Keynesian Cross model, expansionary fiscal policy boosts GDP by an amount dictated by the multipliers.

In the IS-LM model, expansionary fiscal policy also raises the real interest rate, thereby weakening the effect of fiscal policy on GDP. (Crowding-out effect)

K.C. Spending Multiplier K.C. Tax-Cut Multiplier

Fiscal Policy is Weakened by the

Crowding-Out Effect

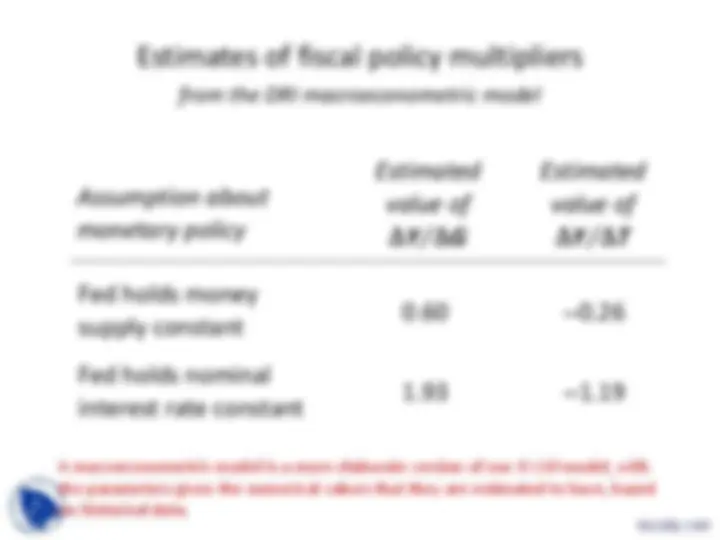

- We have just seen that, in the IS-LM model, expansionary fiscal policy ( G ↑ or T ↓) - leads to higher interest rates, which - exerts downward pressure on investment spending, which - exerts downward pressure on GDP and jobs.

- This negative aspect of expansionary fiscal policy is called the crowding-out effect

- This effect was absent in the Keynesian Cross model

- Thus, fiscal policy is less effective in the IS-LM model than in the Keynesian Cross model

IS 1

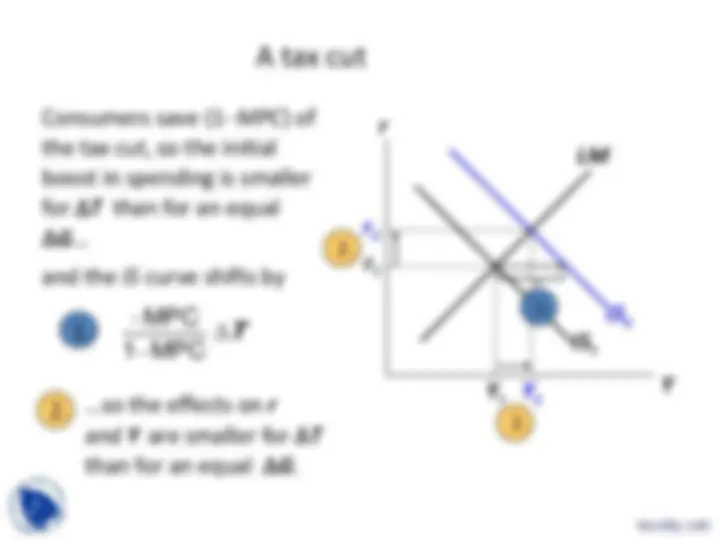

A tax cut

Y

r LM

r 1

Y 1

IS 2

Y 2

r 2

Consumers save (1 MPC ) of the tax cut, so the initial boost in spending is smaller for T than for an equal G …

and the IS curve shifts by

MPC 1 MPC

T

…so the effects on r and Y are smaller for T than for an equal G.

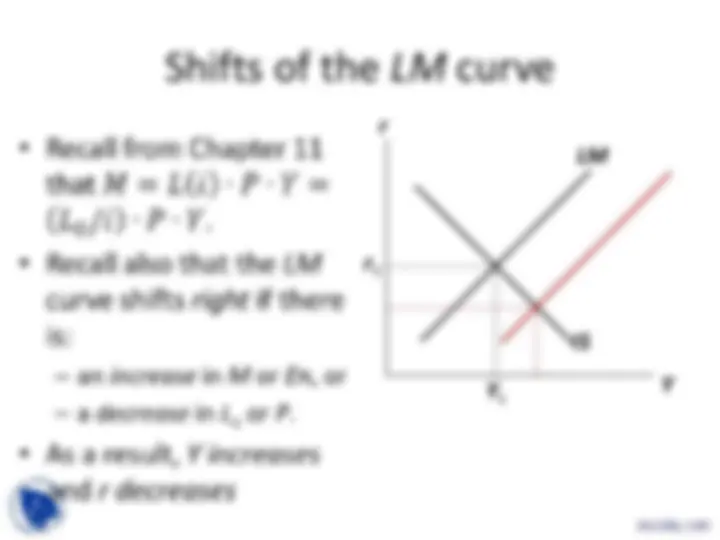

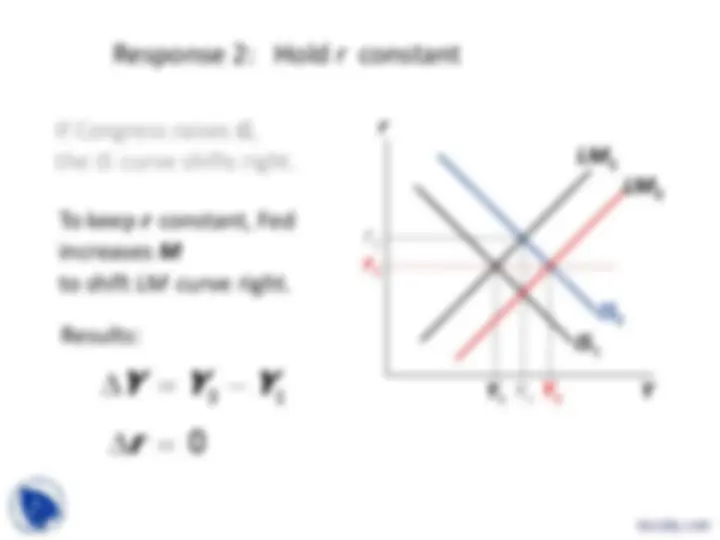

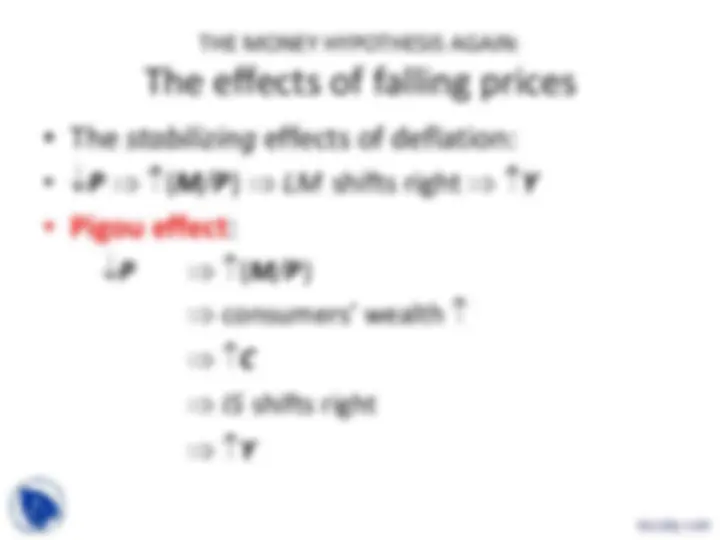

Shifts of the LM curve

IS

Y

r LM

r 1

Y 1

Shifts of the LM curve

Shifts of the LM curve

• Recall from Ch. 11 that, if

expected inflation ( E π)

increases (decreases),

the LM curve shifts down

(up) by the exact same

amount!

• Therefore, if E π

decreases, r will increase,

but by a smaller amount.

• Therefore, i = r + E π will

decrease.

IS

Y

r LM

r 1

Y 1

Monetary Policy

• The practice of changing the quantity of

money ( M ) in order to affect the

macroeconomic outcome is called monetary

policy

- an increase in the quantity of money ( M ↑) is called expansionary monetary policy, and

- A decrease in the quantity of money ( M ↓) is called contractionary monetary policy

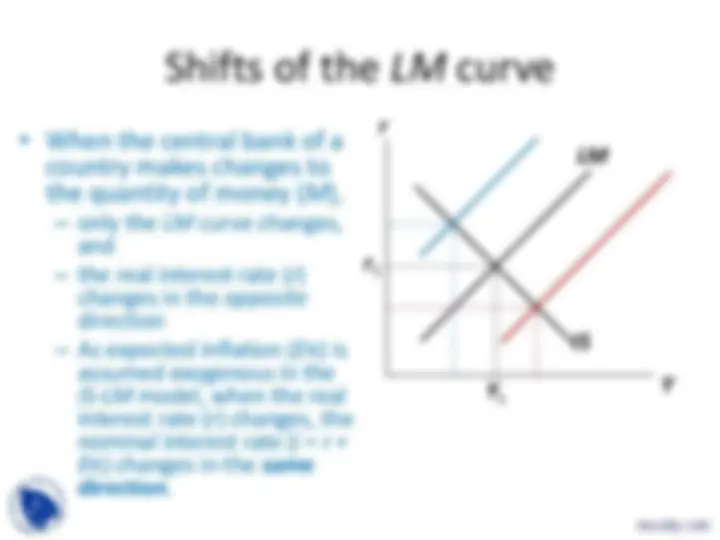

Shifts of the LM curve

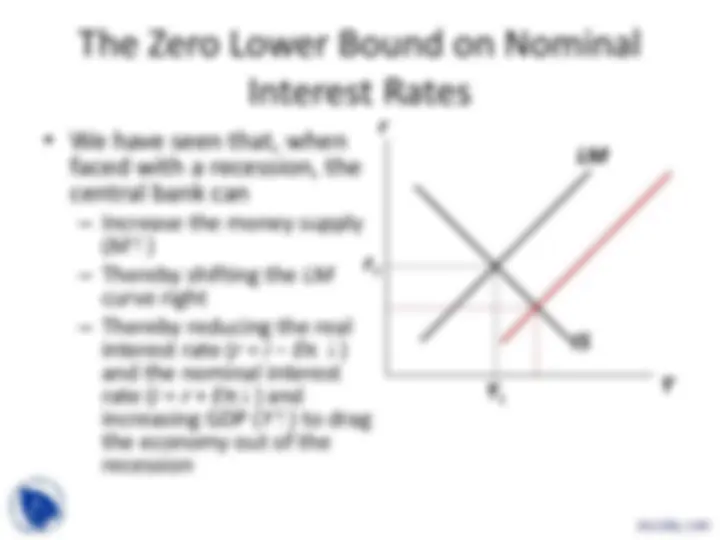

- When the central bank of a country makes changes to the quantity of money ( M ), - only the LM curve changes, and - the real interest rate ( r ) changes in the opposite direction - As expected inflation ( E π) is assumed exogenous in the IS-LM model, when the real interest rate ( r ) changes, the nominal interest rate ( i = r + E π) changes in the same direction.

IS

Y

r LM

r 1

Y 1