Associates

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

These are slideshow for Associate, which is taught in the subject Financial Reporting

Typology: Slides

1 / 12

This page cannot be seen from the preview

Don't miss anything!

Where the acquirer company does not gain control , the acquired company may be

(^) IAS 28 requirement – An Associate is accounted for in the consolidated financial statements using the equity method. With the equity method of accounting, the investor company reports the revenue earned by the other company on its income statement, in an amount proportional to the percentage of its equity investment in the other company. (^) Where significant influence is not demonstrated , and so an investment is not an associate, it is accounted for as a financial asset.

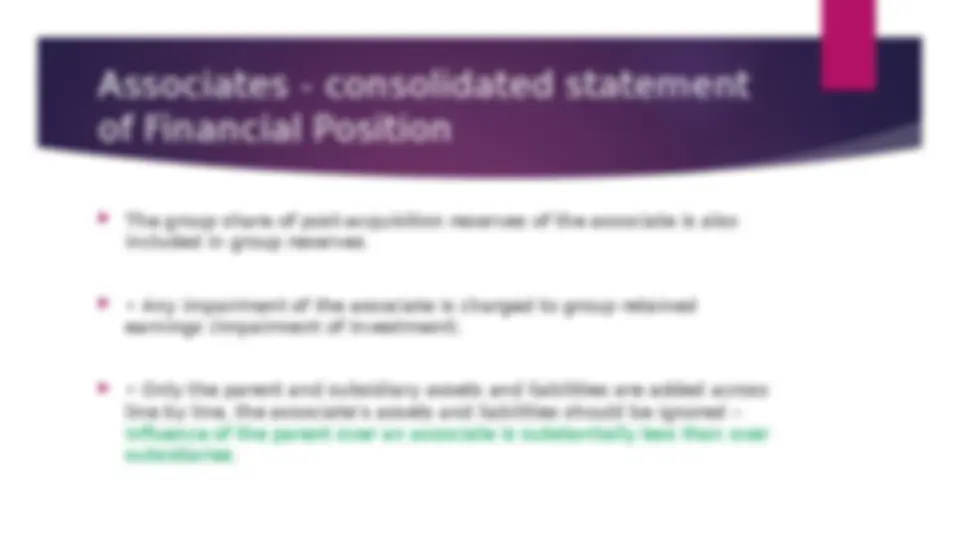

(^) The group share of post-acquisition reserves of the associate is also included in group reserves. (^) • Any impairment of the associate is charged to group retained earnings (Impairment of Investment). (^) • Only the parent and subsidiary assets and liabilities are added across line by line, the associate’s assets and liabilities should be ignored – influence of the parent over an associate is substantially less than over subsidiaries.

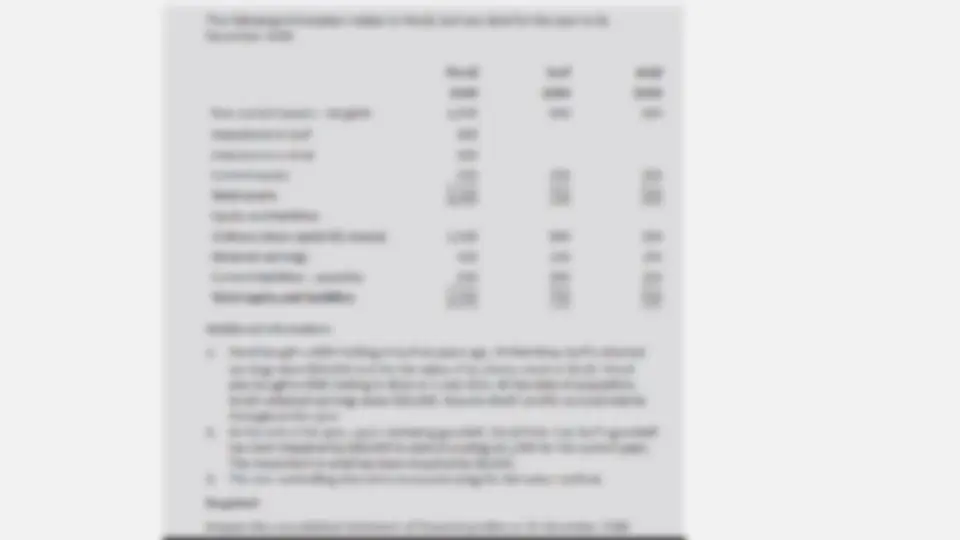

Assume that the investment in Albert has been impaired by $18,000.