REGRESSION DIAGNOSTIC III:

AUTOCORRELATION

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Autocorrelation in the context of linear regression, its causes, consequences, and methods for detection. Autocorrelation occurs when there is a correlation between an error term and a lagged error term. Consequences of autocorrelation include inefficiency of ols estimators, underestimation of standard errors, and suspect hypothesis-testing procedures. Two common methods for detecting autocorrelation are visual inspection of autocorrelation function (acf) and partial autocorrelation function (pacf) plots, and formal tests such as the durbin-watson test and the breusch-godfrey test.

Typology: Summaries

1 / 14

This page cannot be seen from the preview

Don't miss anything!

(^) One of the assumptions of the classical linear regression (CLRM) is that the covariance between u i , the error term for observation i, and u j , the error term for observation j, is zero. (^) Reasons for autocorrelation include: (^) The possible strong correlation between the shock in time t with the shock in time t+ (^) More common in time series data

There are two ways in general. The first is the informal way which is done through graphs and therefore we call it the graphical method or Visual Inspection. ACF/PACF PLOTS The second is through formal tests for autocorrelation, like the following ones:

(^) The Durbin-Watson d statistic is defined as:

The simplest and most commonly observed is the first-order autocorrelation. Consider the multiple regression model: Y t =β 1 +β 2

2t +β 3

3t +β 4

4t +…+β k

kt +u t in which the current observation of the error term u t is a function of the previous (lagged) observation of the error term: u t =ρu t- +e t

The coefficient ρ is called the first-order autocorrelation coefficient and takes values from -1 to +1. It is obvious that the size of ρ will determine the strength of serial correlation. We can have three different cases. (a)If ρ is zero, then we have no autocorrelation. (b) If ρ approaches unity, the value of the previous observation of the error becomes more important in determining the value of the current error and therefore high degree of autocorrelation exists. In this case we have positive autocorrelation. (c) If ρ approaches -1, we have high degree of negative autocorrelation.

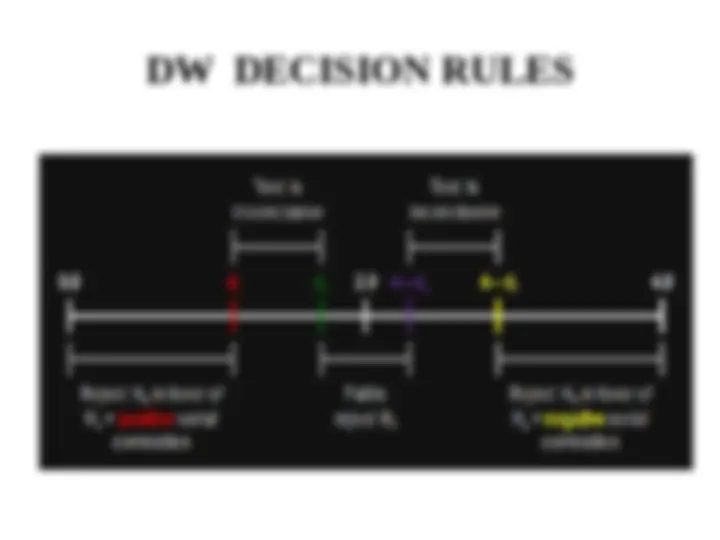

(^) If the statistic lies near the value 2, there is no serial correlation. (^) But if the statistic lies in the vicinity of 0, there is positive serial correlation. (^) The closer the d is to zero, the greater the evidence of positive serial correlation. (^) If it lies in the vicinity of 4, there is evidence of negative serial correlation

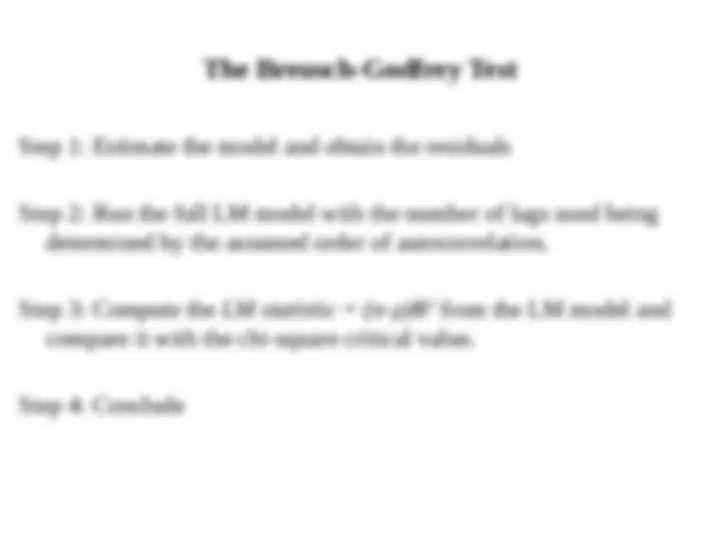

It is a Lagrange Multiplier Test that resolves the drawbacks of the DW test. Consider the model: Y t =β 1 +β 2

2t +β 3

3t +β 4

4t +…+β k

kt +u t where: u t =ρ 1 u t-

t

1

2

2t

3

3t

4

4t

k

kt

1

t-

2

t-

3

t-

p

t-p

t

0

1

2

p

a

Step 1: Estimate the model and obtain the residuals Step 2: Run the full LM model with the number of lags used being determined by the assumed order of autocorrelation. Step 3: Compute the LM statistic = (n-ρ)R 2 from the LM model and compare it with the chi-square critical value. Step 4: Conclude