Breakeven Analysis Or

Cost-Volume- Profit(CVP) Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

notes for breakeven analysis

Typology: Slides

1 / 30

This page cannot be seen from the preview

Don't miss anything!

Cost-Volume-Profit Analysis

4

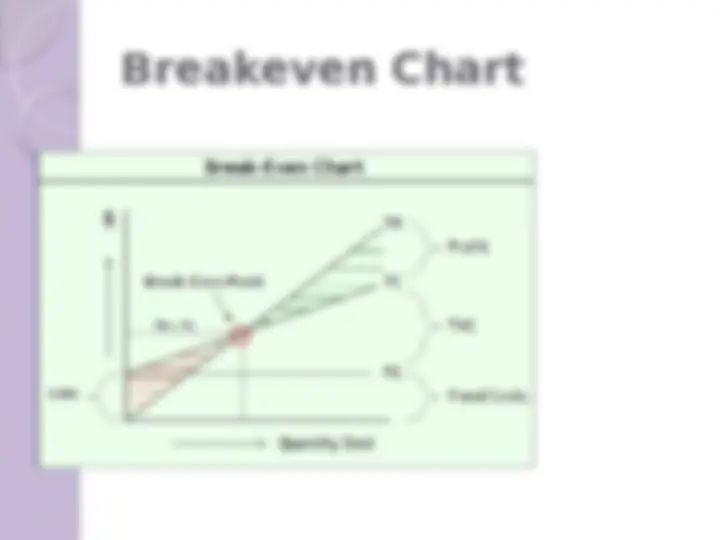

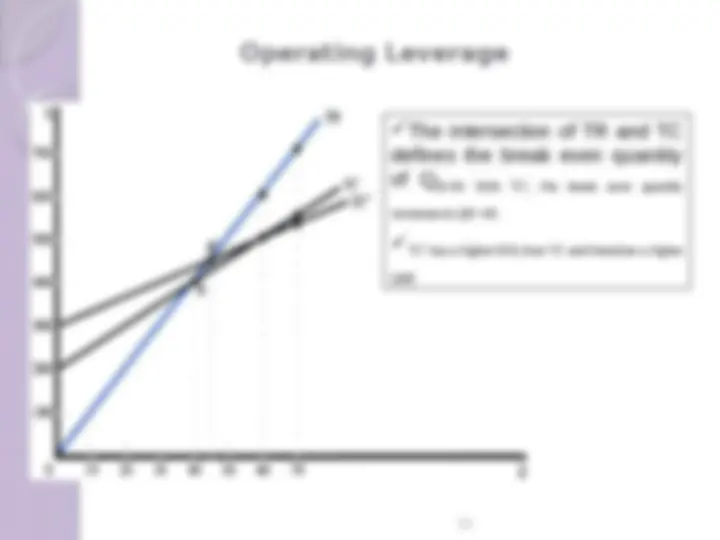

Cost-volume-profit or breakeven analysis examines

the relationship among the TR, TC, and total profits

of the firm at various levels of o/p. This technique is

often used by business executives to determine the

sales volume required for the firm to break even

and the total profits and losses at other sales levels.

The analysis uses a cost-volume-profit chart in

which the TR and TC curves are represented by

straight lines and the break-even o/p (Q

B) is determined at

their intersection.

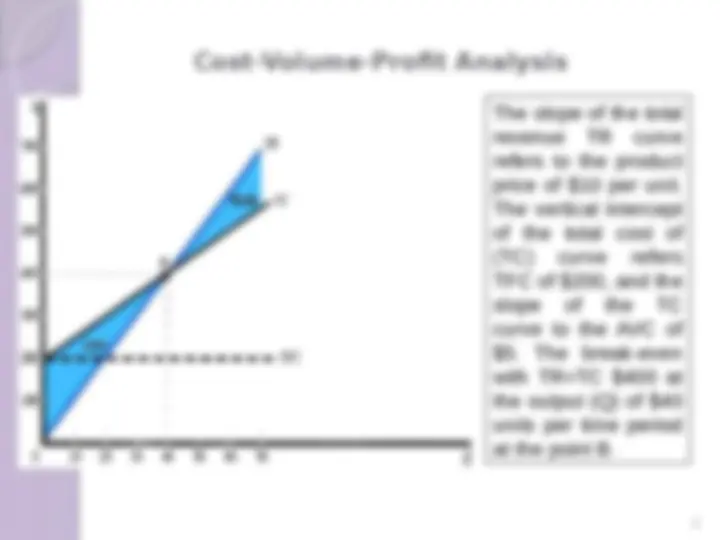

Cost-Volume-Profit Analysis

5

The slope of the total

revenue TR curve

refers to the product

price of $10 per unit.

The vertical intercept

of the total cost of

(TC) curve refers

TFC of $200, and the

slope of the TC

curve to the AVC of

$5. The break-even

with TR=TC $400 at

the output (Q) of $

units per time period

at the point B.

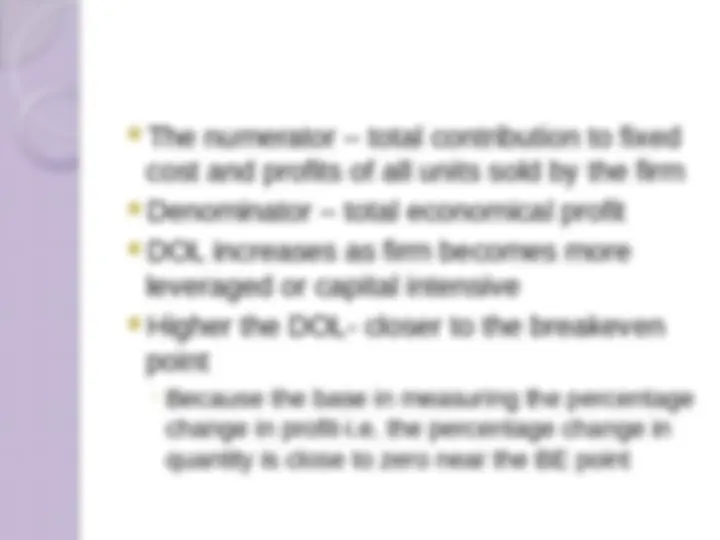

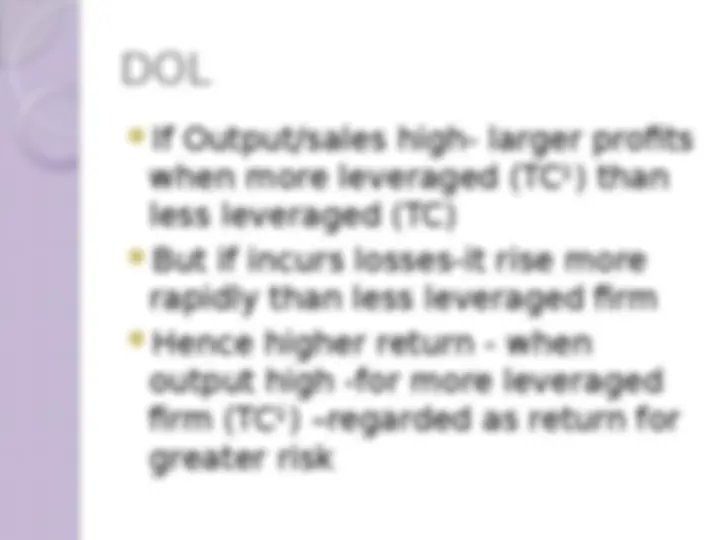

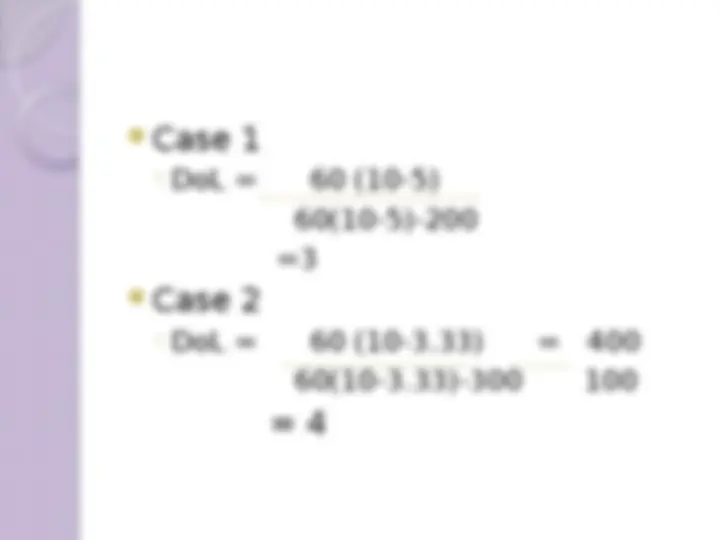

*Contribution margin per unit = Selling Price per

unit – Variable Cost per unit

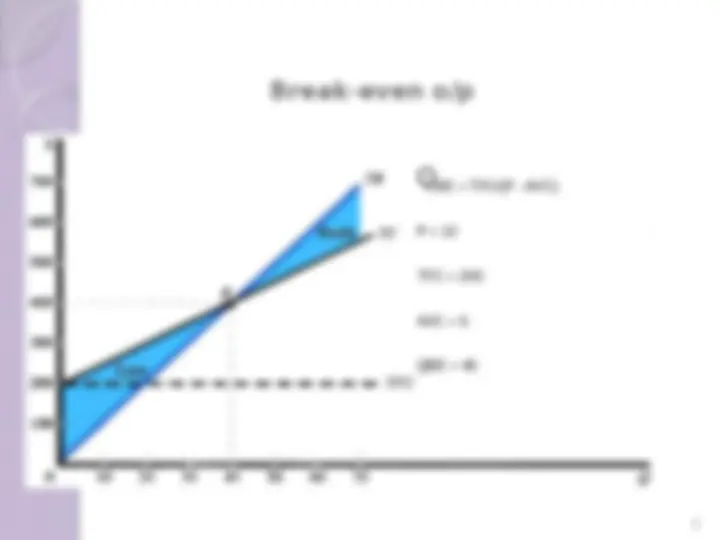

Break-even o/p

8

Q

BE = TFC/(P - AVC)

P = 10

TFC = 200

AVC = 5

QBE = 40

shown by increasing slope of TR

by an increase in vertical intercept

of TC curve

by an increase in the slope of TC

curve

Costs are either fixed or variable

Fixed and variable costs are clearly

discernable over the whole range of

output

Production = Sales

One product/constant sales mix

Selling price remains constant

Efficiency remains unchanged

Volume is the only factor affecting

costs

Margin of safety - a measure in which

the budgeted volume of sales is

compared with the volume of sales

required to break even

Marginal Cost – cost of producing

one extra unit of output