Download CVP or Breakeven Analysis and more Study notes Management Accounting in PDF only on Docsity!

CVP or Breakeven Analysis

» CVP analysis: definition, advantages and disadvantages Page: 2 - 3

» Contribution, Contribution ratio and Variable cost ratio Page: 3 - 6

» Expected sales quantity and Expected sales amount Page: 7 - 12

» Breakeven Point Page: 1 2 - 16

» Margin of Safety Page: 1 6 - 18

» Limiting factor analysis Page: 1 9 - 39

» Make or buy decision Page: 40 - 43

In this chapter we shall discuss about Breakeven or Cost-Volume-Profit (CVP) Analysis. This chapter is important not only for Management Accounting exam, but also for practical workplace.

CVP analysis (cost-volume-profit) or breakeven analysis refers to determining interrelationships between cost, quantity and profit at different activity levels. CVP analysis includes a number of tools; such as: contribution margin analysis, breakeven point, margin of safety, limiting factor analysis, make or buy decision etc.

Advantages / benefits / importance of CVP or breakeven analysis:

- CVP analysis helps to know how much money is left for paying fixed costs (i.e. contribution).

- CVP analysis helps to know how much profit may be earned from a certain sales volume at a certain selling price.

- CVP analysis helps to know the expected selling price and the expected sales quantity for making a certain profit figure.

- CVP analysis helps to know the impact of changes in selling price and in sales quantity on profit.

- CVP analysis is used for fixing sales incentive, sales target, production priority etc.

- CVP analysis helps to know the required production volume for recovering all costs and thus for avoiding any loss (i.e. breakeven point).

- CVP analysis can demonstrate its results in several forms; such as: monetary amount basis, per unit basis, graphical basis and percentage basis.

- CVP analysis shows how much of the sales volume is left for profit, after recovering all expenses (i.e. margin of safety). This enables the company to decide price cuts, sales promotion etc.

- CVP analysis is used to assess if costs are too high for the business to be successful.

- CVP analysis is used to decide if certain product is worth launching in the market or not.

Criticisms / assumptions / limitations / disadvantages / weaknesses of CVP or breakeven analysis:

- CVP analysis requires to classify all costs between fixed cost and variable cost. But all mixed costs may not be accurately classifiable in this manner.

- Selling price per unit is assumed here to remain the same at any level of output. But selling price may decrease in case of a large sales volume (i.e. trade discount).

Contribution per unit = Selling price per unit – Variable cost per unit = (^) NumberContribution of units^ in sold^ $

Contribution ratio = ContributionSelling price^ perper^ unitunit × 100 = Contribution Total sales^ in $× 100 = 100% – Variable cost ratio

Variable cost ratio = VariableSelling price^ cost perper unitunit × 100 = TotalTotal^ variable sales^ cost × 100 = 100% – Contribution ratio

Variable cost ratio + Variable profit ratio = 100%

All the formulas are the different forms of the same thing and are corollary to each other, so perhaps not difficult to remember.

As you understand, 100 is multiplied at the end for expressing in percentage.

Contribution ratio is also known as profit-volume (P/V) ratio, variable profit ratio, marginal income ratio etc. On the other hand, contribution in $ is also known as contribution margin.

Illustration # 1: Sales is 10,000 units @ $10. Variable cost is $3 per unit. Find out: (i) Contribution margin; (ii) Contribution per unit; (iii) Variable profit ratio; and (iv) Variable cost ratio.

Solution: Contribution margin = Total sales – Total variable cost = (10,000 units sold × $10 selling price per unit) – (10,000 units sold × $3 variable cost per unit) = $70,

Alternatively: Contribution margin = (Selling price per unit – Variable cost per unit) × Number of units sold = ($10 – $3) × 10,000 units = $70,

Contribution per unit = Selling price per unit – Variable cost per unit = $10 – $3 = $

Alternatively: Contribution per unit = (^) NumberContribution of units^ in sold^ $ = 10 $70, 000 ,^000 units = $

Variable profit or Contribution ratio = ContributionSelling price^ perper^ unitunit × 100 = $7 ÷ $10 × 100 = 70%

Alternatively: Variable profit ratio = ContributionTotal sales^ in $× 100

= (^10) , 000 units sold ×$70 $10,^000 selling price per unit × 100 = 70%

Variable cost ratio = VariableSelling price^ cost perper unitunit × 100 = $3 ÷ $10 × 100 = 30%

Alternatively: Variable cost ratio = TotalTotal^ variable sales^ cost × 100

= (^1010) ,, 000000 units^ units sold^ sold ×^ × $10$3^ selling selling^ price price^ per per^ unit unit × 100 = 30%

Alternatively: Variable cost ratio = 100% – Variable profit ratio = 100% – 70% = 30%

Illustration # 2: Sales is $100,000. Fixed cost is $50,000. Profit is 20% of sales volume. Find out marginal income ratio.

Discussion: Since we have seen several forms of the same formula, it is very important to identify which particular form to use in light of the information provided in the question. For example: we have seen 3 formulas for marginal income or contribution ratio. But formulas # 1 and 3 cannot be used in this case due to lack of required information. We are left only with formula # 2.

For using formula # 2, total sales is given in the question. We need to calculate contribution in $.

For calculating contribution in $, we have 4 formulas in hand. We cannot use formulas # 1, 3 and 4 in this case due to lack of required information. We are left only with formula # 2.

For using formula # 2, fixed cost is given in question. We need to calculate profit by using the information provided in the question:

Profit = 20% of sales volume = $100,000 = 20% = $20,

Now we have all information in hand for using formula # 2 of marginal income ratio:

Contribution margin = Fixed cost + Profit = $50,000 + $20,000 = $70,

Marginal income or Contribution ratio = ContributionTotal sales^ in $× 100 = (^) $100$70,^000 , 000 × 100 = 70%

Hopefully you are clear about which particular form to use in light of information given in the question.

Let us see some more corollaries to contribution formula for making important managerial decisions.

Suppose the selling price and the target profit margin are given for a particular product, and you need to find out the sales volume required. Use following formula:

Expected sales quantity = FixedContribution^ cost^ +^ Expected per unit^ profit

Expected sales amount = FixedContribution^ cost^ +^ Expected ratio^ profit = Expected sales quantity × Selling price

Illustration # 5: A company sells a product at $10 per unit. Variable cost is $3 per unit and fixed cost is $30,000. In a certain period, management sets a profit target of $12,000. Find out the required sales in units and in $.

Solution: Expected sales quantity = FixedContribution^ cost^ +^ Expected per unit^ profit = $30,^000 $10^ + −^ $12 $3 ,^000 = 6,000 units

Expected sales amount = Expected sales quantity × Selling price = 6,000 units × $10 = $60,

Try yourself to find out expected sales amount using the other formula. A bit difficult, right?

Illustration # 6: W Limited sells one product for which data is given below: Selling price $10 per unit Variable cost $6 per unit Fixed cost $2 per unit The fixed costs are based on a budgeted level of activity of 5,000 units for the period.

How many units must be sold if W Limited wishes to earn a profit of $6,000 for one period?

You may remember that fixed cost per unit is multiplied with budgeted activity level (preferably budgeted production quantity ), not actual activity level, for arriving at total fixed cost.

Solution: Units to be sold = FixedContribution^ cost^ +^ Expected per unit^ profit = (^5 ,^000 units$10^ × −^ $2 $6) + $6,^000 = 4,000 units

Illustration # 7: AB Ltd. makes and sells a single product, for which variable costs are as follows:

Materials $10 per unit Labor $8 per unit Production overhead $6 per unit

Selling price is $30 per unit, and fixed costs per annum are $68,000. The company wishes to make a profit of $16,000 per annum. Determine the sales required to achieve this profit.

Solution: Expected sales in units = 14,000 units; Expected sales in $ = $420,000.

Illustration # 8: ABC Ltd. wishes to sell 14,000 units of a product. Variable cost per unit is $15, fixed cost $47,000 and expected profit $23,000. What is the required selling price per unit?

Discussion: This math can be solved in a number of ways, we are showing here only one way.

Using the information provided in the question, we can apply the formula of expected sales in units and find out contribution per unit. Next we can apply the formula of contribution per unit and find out selling price per unit.

Expected sales in units = FixedContribution^ cost^ +^ Expected per unit^ profit

Contribution per unit = FixedExpected^ cost^ + salesExpected in units^ profit = $47 14 ,^000 , 000 + units$23,^000 = $

Contribution per unit = Selling price per unit – Variable cost per unit

Selling price per unit = Contribution per unit + Variable cost per unit = $5 + $15 = $

Illustration # 9: The current sales of a manufacturing company is on average 40,000 units at $ each. Provided below cost structure, find out additional sales quantity required for maintaining current profit level if selling price is reduced by 10%: Prime costs $200, Variable overhead $40, Fixed overhead $100,

Illustration # 10: In Illustration # 6, assume that selling price and variable cost will increase by 20% and 12% respectively. By how much sales volume to change as compared with the original budgeted level, in order to achieve the original budgeted profit for the period?

Solution: Original budgeted profit = Sales – Total cost = ($10 as selling price per unit - $6 as variable cost per unit - $2 as fixed cost per unit) × 5,000 units as budgeted activity level = $10,

Revised selling price per unit = $10 × (100% + 20%) = $

Revised variable cost per unit = $6 × (100% + 12%) = $6.

Revised contribution per unit = $12 – $6.72 = $5.

Units to be sold = FixedContribution^ cost^ +^ Expected per unit^ profit = (^5 ,^000 units$5^ ×^ .$2 28 ) + $10,^000 = 3,788 units

Change in budgeted sales quantity = 5,000 units – 3,788 units = 1,212 units decrease

% of decrease = 1,212 units ÷ 5,000 units × 100 = 24.24%

Earlier we told you that fixed cost per unit is multiplied with budgeted production quantity for arriving at total fixed cost. In some cases budgeted sales quantity, actual sales quantity, actual production quantity etc. are needed to use. Following math will clarify your concept in this regard.

Illustration # 11: Provided below budgeted and actual information, what should be actual sales quantity for achieving the original budgeted profit?

Particulars Budgeted Actual Production quantity 5,000 units 5,200 units Sales quantity 4,500 units? Selling price per unit $10 $ Variable cost per unit $4 $4. Fixed cost per unit $3 $3.

Solution: Original budgeted profit = (Budgeted sales quantity × Budgeted selling price per unit) – (Budgeted sales quantity × Budgeted variable cost per unit) – (Budgeted production quantity × Budgeted fixed cost per unit) = (4,500 units × $10) – (4,500 units × $4) – (5,000 units × $3) = $12,

Units to be sold = ActualActual^ fixed contribution^ cost^ +^ Expected per unit^ profit = (^5 ,^000 units$10^ × – $3 $4.^2 .) + 4 $12,^000 = 5,000 units

Illustration # 12: MN Ltd. bakes and sells a single type of cake. The variable cost of production is $0.15 per cake and the current sales price is $0.25 per cake. Fixed costs are $2,600 per month, and annual profit for the company at current sales volume is $36,000. The volume of sales demand is constant through the year. The sales manager wants to raise the sales price by $0.04 per cake, but considers that a price rise will result in some loss of sales. Ascertain the fall in monthly sales volume allowable before affecting current profitability, if the sales manager sticks to his decision.

Solution: Existing sales quantity = FixedContribution^ cost^ +^ Existing per unit^ profit

= $2,^600 +($36,^000 $0^ as. 25 annual – $0.^ profit 15 ÷^12 months)= 56,000 units

Expected sales quantity = FixedContribution^ cost^ +^ Expected per unit^ profit

= $2,^600 +($36($0,^000. 25 as +^ annual $0. 04 ) –^ profit $0. 15 ÷ 12 months)= 40,000 units

Fall in monthly sales volume allowable = 56,000 units – 40,000 units = 16,000 units

Illustration # 13: AB Ltd. makes a product which has a variable production cost of $8 and a variable selling cost of $2 per unit. Fixed costs are $40,000 per annum, the sales price is $18 per unit, and the current volume of output and sales is 6,000 units. The company is considering whether to hire an improved machine for production. Annual hire costs would be $10,000 and it is expected that the variable cost of production would fall to $6 per unit.

(i) Determine the number of units that must be produced and sold to achieve the same profit as is currently earned, if the machine is hired.

(ii) Calculate the annual profit with the machine if output and sales remain at 6,000 units per annum.

Solution: Current profit volume = Sales – Total cost = (6,000 units as current sales volume × $ as selling price per unit) – (6,000 units as current sales volume × $10 as variable cost per unit) – $40,000 as fixed cost = $8,

You understand that the annual hire cost of the machine is a fixed cost.

If in your exam you are asked to write the definition, you must put the formula also, without saying.

The lower the breakeven point, the better it is, because you can recover your expenses with a lower volume of production and sales.

Illustration # 15: Expected sales is 10,000 units @ $8. Variable cost is $5 per unit. Fixed cost is $21,000. Compute the breakeven point. Solution: Breakeven sales in units = 7,000 units; Breakeven sales in $ = $56,000. You understand that expected sales quantity i.e. 10,000 units is unnecessary for computing BEP.

Illustration # 16: Variable cost ratio is 30%. Fixed cost is $35,000. Find out breakeven point.

Solution: Contribution ratio = 100% – Variable cost ratio = 100% – 30% = 70% Breakeven sales in $ = Fixed cost ÷ Contribution ratio = $35,000 ÷ 70% = $50, Illustration # 17: Contribution ratio is 20% and selling price is $10 per unit. How many units must be sold for making a contribution of $50,000 towards fixed costs?

Discussion: You have to make a contribution of $50,000 towards fixed costs i.e. contribution = fixed costs = $50,000. And you remember that contribution = fixed cost at BEP. So you understand that the number of units must be sold for contribution = fixed cost means breakeven sales in units.

For calculating breakeven sales in units, fixed cost is given in the question. We need contribution per unit, which we can calculate easily from the formula of contribution ratio.

Contribution ratio = Contribution per unit ÷ Selling price per unit Contribution per unit = Selling price per unit × Contribution ratio = $10 × 20% = $ Number of units must be sold = Fixed cost ÷ Contribution per unit = $50,000 ÷ $2 = 25,000 units Illustration # 18: ABC Company makes a product which has a variable cost of $7 per unit. If fixed cost is $63,000 per annum, calculate the selling price per unit if the company wishes to breakeven with a sales volume of 12,000 units.

Solution: We are given breakeven sales in units. Let us use its formula and see what happens.

Breakeven sales in units = Fixed cost ÷ Contribution per unit

Contribution per unit = Fixed cost ÷ Breakeven sales in units = $63,000 ÷ 12,000 units = $5. Contribution per unit = Selling price per unit – Variable cost per unit

Selling price per unit = Contribution per unit + Variable cost per unit = $5.25 + $7 = $12.

Illustration # 19: Selling price is $10 per unit and variable cost is $3 per unit. Fixed cost is $35,000. Find out the minimum production volume required for avoiding any loss and explain its implication.

Answer: Minimum production volume is 5,000 units. This means the company makes no profit no loss (i.e. merely recovers its expenses) when it produces and sells 5,000 units during a period.

Illustration # 20: Annual demand is 5,000 units, variable cost $3 per unit and fixed cost $35,000. What is the minimum selling price for avoiding / before incurring any loss?

Answer: Contribution per unit is $7. Selling price per unit is $10.

Illustration # 21: A company is considering launching a new product. Selling price is targeted at $10 per unit, variable cost at $3 per unit and fixed cost at $35,000 per annum. Annual demand may be constrained to 4,000 units. Decide the appropriate course of action.

Answer: Sales = Total cost + Profit Profit = Sales – Total cost

Profit = (4,000 units × $10) – (4,000 units × $3) – $35,000 = $7,000 loss

So the company should not introduce the product.

Alternatively: Breakeven sales is 5,000 units. Since annual demand is lower than the periodic breakeven sales quantity, so the company should not introduce the product.

Illustration # 22: King Sport sells both bats and gloves. Historically, the firm has averaged three bats sold for each glove sold. Each bat has a $6 of variable cost and each glove $10. Fixed costs are $170,000 per year. Each bat sells for $10 on average and each glove for $15. Tax rate is 20%.

(i) How much sales is needed to break even?

(ii) How much revenue as well as quantity is needed to earn a pre-tax profit of $85,000?

(iii) How much revenue as well as quantity is needed to earn an after-tax profit of $85,000?

Discussion: The question mentions about two products. Some information are given for the two products separately. But fixed cost is given on gross basis i.e. not separately for each product. So you understand that it is not possible to calculate breakeven sales for each product separately. Instead, we have to consider the two products together as a single set and accordingly we can calculate the number of sets to be sold for reaching breakeven.

Now let us see some variation in above illustration.

Illustration # 23: In Illustration # 22, calculate the sales required for breakeven if the fixed cost is apportioned between bat and gloves at 60 : 40.

Solution: Fixed cost apportioned to bat = $170,000 × 60% = $102,

Fixed cost apportioned to gloves = $170,000 × 40% = $68,

Contribution per bat = $10 as selling price per bat – $6 as variable cost per bat = $

Contribution per glove = $15 as selling price per glove – $10 as variable cost per glove = $

Number of bats to be sold for breakeven = $102,000 as fixed cost apportioned to bat ÷ $4 as contribution per bat = 25,500 bats

Number of gloves to be sold for breakeven = $68,000 as fixed cost apportioned to gloves ÷ $5 as contribution per glove = 13,600 gloves

Breakeven sales revenue = (25,500 bats × $10) + (13,600 gloves × $15) = $459,

Since fixed cost was separable for bats and gloves, so we did not bother about comprising any set.

֍ ֍ ֍ ֍ ֍ ֍ ֍ ֍ ֍

So breakeven means no profit no loss. Below breakeven means you are at loss. And above breakeven means you are at profit. The quantity or revenue above BEP is known as margin of safety.

Margin of safety refers to the excess of sales over the breakeven point and thus the amount of sales directly contributing to profit. Margin of safety in units = Sales in units – Breakeven sales in units Margin of safety in $ = Sales revenue – Breakeven sales revenue Margin of safety in $ = Margin of safety in units × Selling price per unit

Margin of safety in % = MarginSales^ of^ safety quantity^ quantity × 100 = MarginSales^ of^ safety revenue^ revenue × 100

If in your exam you are asked to write the definition, you must put the formula also, without saying.

Margin of safety the higher the better, because it means more profit is earned.

Illustration # 24: In Illustration # 15, determine margin of safety and explain its implication.

Answer: Margin of safety in units = 3,000 units; Margin of safety in $ = $24,000.

The implication is that actual sales can fall short of expected sales by maximum 3,000 units or $30,000 in order to reach breakeven point and thus before incurring any loss.

Illustration # 25: ABC Co. sells a product which has a variable cost of $30 and selling price of $ per unit. Fixed cost is $70,000 and sales volume is 8,000 units. Calculate BEP and margin of safety.

Answer: Breakeven sales quantity = 7,000 units; Margin of safety quantity = 1,000 units.

Illustration # 26: In Illustration # 6, find out margin of safety if fixed cost is 20% higher than budgeted.

Solution: Breakeven quantity = Fixed cost ÷ Contribution per unit

= [(5,000 units × $2 per unit) × (100% + 20%)] ÷ ($10 – $6) = 3,000 units

Margin of safety quantity = Sales quantity (e.g. actual or budgeted) – Breakeven quantity

= 5,000 units – 3,000 units = 2,000 units

Margin of safety revenue = Margin of safety quantity × Selling price = 2,000 units × $10 = $20,

Margin of safety % = Margin of safety quantity ÷ Sales quantity (e.g. actual or budgeted) × 100

= 2,000 units ÷ 5,000 units × 100 = 40%

Illustration # 27: A company sells a product @ $10 per unit. Variable cost is $3 per unit. For earning a profit of $21,000, how many units should be sold above the breakeven point?

Discussion: At the first sight you definitely attempted for calculating expected sales quantity, breakeven sales quantity and finally quantity above breakeven point = expected sales quantity – breakeven sales quantity. Only due to the missing of fixed cost, this entire attempt is abandoned.

So we need to determine an alternative approach to solving this math. You understand that quantity to be sold above breakeven point means margin of safety quantity. Is there any formula of calculating margin of safety when profit is given in the question instead of fixed cost? The answer is: Yes.

Profit = Margin of safety in $ × Contribution ratio = Margin of safety in units × Contribution per unit

Margin of safety in units = Quantity to be sold above BEP = Profit ÷ Contribution per unit

= $21,000 as expected profit ÷ ($10 as selling price per unit – $3 as variable cost per unit) = 3,000 units

We have seen how important managerial decision can be made from breakeven point and margin of safety. Now let us move towards more critical level of managerial decision making.

A limiting factor or a constrained resource is a situation which restricts the highest level of activity and thus reduces the profitability of an organization. Such as: shortage of materials or labor supply, shortage of machine hours, shortage of demand etc. At the existence of any of these factors, products are ranked on the basis of either “contribution per unit of limiting factor” or “variable cost saved from in-house production per unit of limiting factor” instead of simple “contribution per unit”.

You understand that limiting factor analysis then refers to the determination of maximum profit potential under the existence of one or more limiting factors. This is in fact an advanced version of contribution analysis. Here several products are compared on the basis of their contribution per unit of limiting factor i.e. contribution margin is divided by the available quantity of the limiting factor or resource. Product with higher contribution per unit of limiting factor is given preference.

Before entering into mathematical illustrations, let us demonstrate the recommended steps for limiting factor analysis. Otherwise it will be very difficult to solve the math:

Step # 1: Determine the limiting factor.

Step # 2: Calculate contribution per unit and contribution per unit of limiting factor for each product.

Step # 3: Rank each product on the basis of contribution per unit of the limiting factor.

Step # 4: Determine the optimal product mix or profit maximizing production plan or maximum number of units of each product to be produced according to the ranking in step # 3, after allowing for any minimum production requirement.

Step # 5: Finally, Maximum amount of profit = Ʃ (Contribution per unit of each product × Quantity of each product).

Since the steps are sequential, you cannot overlap between them. For ranking products and for determining optimal product mix, contribution per unit of limiting factor is used. On the other hand, for calculating maximum profit, contribution per unit is used. When contribution per unit of limiting factor becomes same for two or more products, then the optimal product mix may contain any combination of those products.

When demand is unlimited for one or more products, step # 1 becomes undoable. Sometimes the question will mention a minimum production requirement for one or more products. Remember, this will get priority over optimal product mix. In other words, optimal production quantity cannot be lower than the minimum production requirement. If the question does not require you to calculate maximum amount of profit or to prepare any income statement, then step # 5 is to be skipped and fixed cost information is of no use. The question may require you to calculate the maximum amount of profit instead of determining the optimal product mix. You understand that still you have to conduct limiting factor analysis, because otherwise maximum profit cannot be calculated.

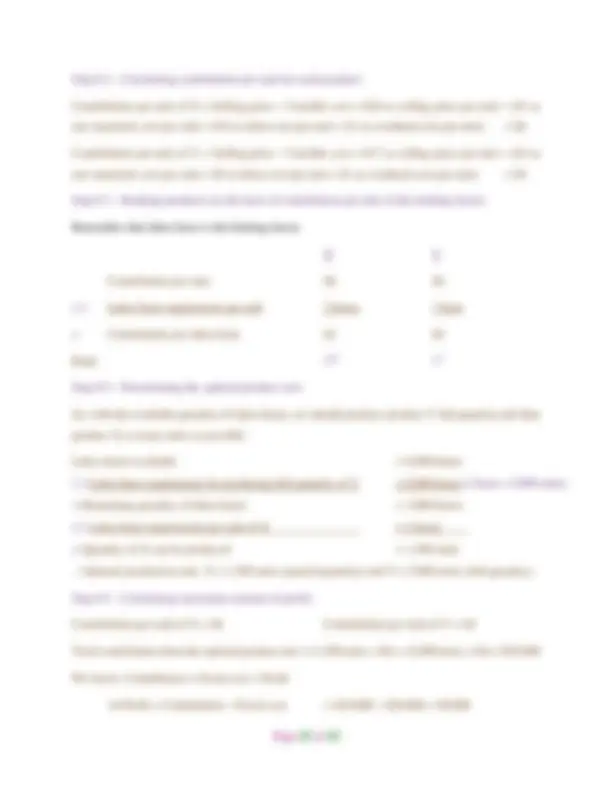

Illustration # 30: A company produces two products: X and Y. Relevant information is as follows:

X Y Raw materials required per unit 2 kg 3 kg Labor hour required per unit 7 hours 8 hours Selling price per unit $75 $ Periodic demand 10,000 pcs. 15,000 pcs. Raw materials price is $5 per kg. Hourly rate of production labor is $8. In a certain period, 50, kg of raw materials and 200,000 labor hours are available. Both products can be produced by the same machine, rent of which is $100,000 per period. Determine the appropriate product mix as well as the maximum amount of profit for the period.

In a certain period, 50,000 kg of raw materials and 200,000 labor hours are available. That means, either raw material or labor hour or both are the limiting factors. Let us check.

Solution: Step # 1 - Determining the limiting factor: Raw materials requirement during the period = (2 kg per pcs. of X × 10,000 pcs. as periodic demand of X) + (3 kg per pcs. of Y × 15,000 pcs. as periodic demand of Y) = 65,000 kg Raw materials availability during the period = 50,000 kg Labor hour requirement during the period = (7 hours per pcs. of X × 10,000 pcs. as periodic demand of X) + (8 hours per pcs. of Y × 15,000 pcs. as periodic demand of Y) = 190,000 hours Labor hour availability during the period = 200,000 hours So we find that raw materials is a limiting factor, but labor hour is not a limiting factor.