Download Economic Resources, Factors of Production, and Cross Elasticity of Demand and more Assignments Business Administration in PDF only on Docsity!

ASSIGNMENT No. 1

Course: Micro Economics (8406) Semester: Autumn, 2020

Level: BBA (4 years)

Q. 1 What are economic resources? What categories do economists use to classify

them? Why resources are also called factors of production? Why are they called

inputs?

Economic resources are the land, labor, capital and business potential used in the production of goods and services. There are four main types of economic resources : land, labor, capital, entrepreneurship Economic Resources 1: Land Earth is an economic resource that includes all natural physical resources such as gold, iron, silver, oil, etc. Some countries have very good natural resources and use these resources to boost their economies. Such as the development of North Sea oil and gas in Norway and the United Kingdom, or the overproduction of vast fields in the United States and Canada. Some other developed countries, such as Japan, have limited economic resources. Japan is the world's second largest economy but relies on imported oil. Economic Resources 2: Labor Human input in the production or manufacturing process is known as labor. Workers' ability to work varies. Each worker's work ability is based on their training, education and work experience. This ability to work is a matter of size and quality of the workforce. Increasing the quality and size of the workforce is essential to achieve economic growth. Economic Resources 3: Capital In economics, capital is a term that means investing in capital goods. Therefore, it can be used to manufacture other goods and services in the future. The capital factors are as follows.

Fixed capital This includes new technologies, factories, buildings, machinery and other equipment. Working capital It is a storehouse of finished goods or components or semi-finished goods or components. These equipment or components will be used in the near future Capital productivity New features of capital, machinery or technology are commonly used to improve the productivity of labor. For example, new farming methods help increase the productivity of the agricultural sector and create more valuable jobs in the sector that encourage people to come out for work. Infrastructure It is a reserve of capital that is used to sustain the entire economic system. Such as roads, railways, airports, etc. Economic Resources 4: Entrepreneurship A business person or individual who wants to supply products to the market in order to make a profit. Entrepreneurs usually invest in their business. This financial capital is usually based on their savings and they take risks associated with their investment. This risk can be offset by the profitability of the business. Entrepreneurship, thus, is an important economic resource. The factors of entrepreneurship are as follows. Income Wealth Wages and wages Capital and interest Profit and enterprise

Why resources are also called factors of production:

Factors of production because they produce products or services.

Why are they called inputs:

Inputs are just another word for factors of production.

Advantages of specialization in the use of human and material resources:

The benefits of specialization for workers are that they can choose a job according to their natural abilities, have the opportunity to complete these skills, and save time in not constantly moving from one job to another. Material resources will be developed and tailored to a specific use. On a regional basis, each region will produce the product for which it is best suited. By mastering its comparative advantage, maximum efficiency can be utilized using each region or set of human and material resources.

Exchange is the necessary consequence of specialization:

When there is expertise, it means that we can say that there can be human specialization and regional geographical specialization. So of these two forms of skills this means that one group or entity is doing one kind of good, and another group or another organization is doing another kind of good. So if we say that you are made of only growing corn and another group is only cultivating wheat, um, it is difficult to live on just corners, only wheat. But it is very easy to sustain life on a mixture of corn and weak, so skill. Although it is more, it allows people to get better at the work they master and also requires people to trade so that everyone has access to the goods that other people now make have been.

Q. 4 What is cross elasticity of demand? Explain with examples?

Flexibility in the demand range is the percentage change in the quantity of demand for a product which increases the price of the product by a percentage. One of the reasons for the demand for good is the price of related goods. For example, if two items A and B are eaten together, i.e. these are complements, an increase in the price of B will increase the price of the bundle (A + B) which in turn will reduce the demand for A and vice versa. Similarly, if A and B are alternatives, an increase in the price of A will increase the demand for B as B becomes relatively cheaper and the user switches from A to B which increases its demand. Cross-elasticity of demand is a quantitative tool that specializes in the sensitivity to demand of one product, called A to change the prices of other products.

Formula:

Cross elasticity of demand can be calculated using the following formula:

Cross Elasticity of Demand EA, B

% increase in quantity demanded of A % increase in price of product B Percentage changes in the above formula are calculated using the mid-point formula which divides actual change by average of initial and final values. The formula to calculate cross elasticity thus becomes: EA, B = Qf − Qi ÷ Pf − Pi (Qf + Qi) ÷ 2 (Pf + Pi) ÷ 2 Where, Qf and Qi are the final and initial quantities demanded of product A, respectively; and Pf and Pi are the final and initial prices of product B.

Explain the cross elasticity of demand

Substitute Goods: Cross-flexibility in the demand for alternative goods is always positive because when the price of good increases, the demand for good increases. For example, if the price of coffee goes up, the demand for tea (alternative beverages) increases as consumers turn to less expensive but alternative alternatives. This reflects the cross-flexibility of the demand formula, as it shows a positive increase in both numbers (percentage change in demand for tea) and denominator (price of coffee). Items with a coefficient of 0 are irrelevant items and are independent of each other. Items can be a weak alternative, with positive but low cross-flexibility in demand for both products. This is often the case for different product alternatives, such as coffee High flexibility in demand for items that are strong alternatives. Consider different brands of tea; An increase in the price of green tea from one company has a greater effect on the demand for green tea from another company. Complementary goods: Alternatively, cross-elasticity in the demand for complementary goods is negative. As the price of an item increases, an item becomes more closely associated with that item and is necessary for its use because the demand for essential good has also decreased. For example, if the price of coffee goes up consumers drinks less coffee as the required quantity of coffee sticks drops and they need to buy fewer sticks. In the formula, the numerator (demand quantity of stir sticks) is negative and the letter (value of coffee) is positive. The result is a negative cross-elasticity.

= (600 − 200) ÷ [(600+200) ÷ 2]

Percentage increase in quantity demanded of marijuana = (800 − 2,000) ÷ [(800+2000) ÷ 2] = -85.71% Cross elasticity of demand = % change in quantity demanded ÷ % change in price = -85.71% ÷ 100% = -0. Cigarettes and marijuana have negative cross elasticity of demand which tells that they are complimentary goods.

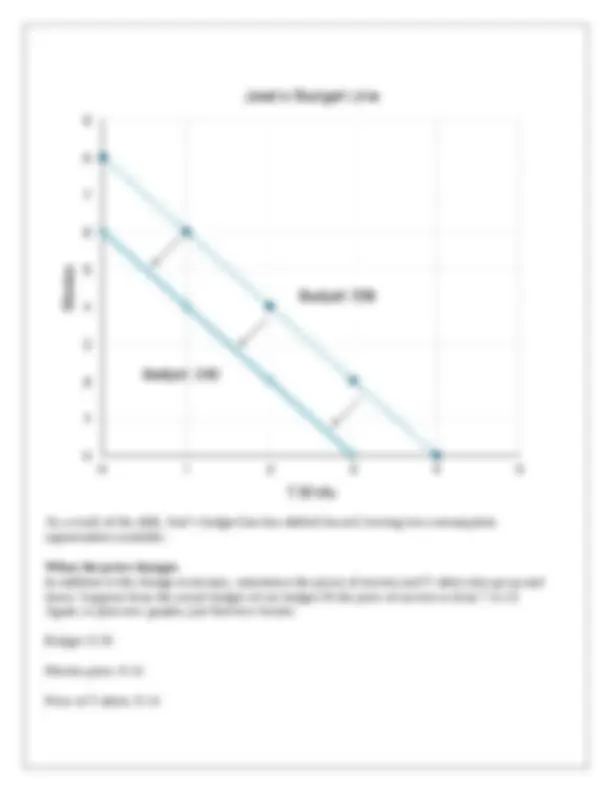

Q. 5 What information is embodied in a budget line? What shifts occur in the budget

line when money income ( a ) increases and ( b ) decreases? What shifts occur in the

budget line when the price of the product shown on the vertical axis ( a ) increases

and ( b ) decreases?

The budget line represents the maximum consumer consumption at a given revenue level. When there is a change in revenue, it shifts parallel, but when the price relationship changes, it rotates. The budget line is also called a budget constraint because it limits the total number of user usage. Total consumption in dollars at each point of the budget line is equal to total revenue. If Product A is planned on the Y axis and Product B on the X axis, the budget line touches the Y axis at the point where all budget is spent on Product A and it touches the X axis at the point where I only have product B. Is consumed at any point between these two extreme cases, a combination of products A and B is eaten. Budget constraints: We now know that Jos will have to make purchases at some point along the budget line according to his preferences. Note that any point in the budget line is possible. Juice can cost less than $ 56, but it's not very affordable as it can still buy more. Since T-shirts and movies are just two items, there is no saving in this model for juice. This means that not spending its entire budget is

necessarily a waste of revenue. On the other hand, there is no point beyond the budget line. If Joss has only $ 56, he can't afford more. Note that green zone areas should not be more appropriate than the points along the budget line. The maximum point depends on the preferences of the juice, which we will discuss when the curves of the indifference of the juice.

Slope

Although we can easily combine only the X and Y intercepts to find the budget line so that it represents all the combinations spent in the whole budget of JOSE, it is important to discuss what the slope of this line represents. does. Remember, the slope is the rate of change. In economics, the slope of the graph is often very important. In this case, the shield is QY / QX. If we want to represent the shield in terms of prices, it is equal to Px / PY. This may seem unreasonable at first, because we are used to seeing the shield as Y / X. but the reason this is not true for prices is because the y-axis represents quantity, not price. As we saw above, as price doubles, the quantity the consumer could previously purchase is halved. If José is making $56: When the price of movies is $7, he can buy 8 of them

As a result of the shift, José’s budget line has shifted inward, leaving less consumption opportunities available. When the price changes In addition to the change in income, sometimes the prices of movies and T-shirts also go up and down. Suppose from the actual budget of our budget 56 the price of movies is from 7 to 14. Again, to plan new graphs, just find new breaks: Budget: $ 56 Movies price: $ 14 Price of T-shirts: $ 14

Maximum number of movies (y-intercept): $ 56 / $ 14 = 4 Maximum number of T-shirts (X intercept): $ 56 / $ 14 = 4 As a result of the pivot, José has fewer consumption opportunities available and the slope of the line changes. This has two effects: The Size Effect: There are fewer opportunities for consumption (as a result of the price change, the purchasing power of José’s dollar has fallen). The Slope Effect: The relative price of movies is now higher, while the relative price of T-shirts is now lower. When Price and Income Change The last type of change is when both price and income change. Suppose the price of movies increases from $7 to $12 and José’s budget increases to $63. To plot the new budget line, follow the same steps as before: Budget: $ Price of movies: $ Price of T-shirts: $ Maximum number of movies (y-intercept): $63/$12 = 5. Maximum number of T-shirts (x-intercept): $63/$14 = 4. Those changes have interesting effects. José now has access to some new consumption opportunities, but many others are now unavailable. While the slope effect has clearly made the relative price of T-shirts lower, the size effect is uncertain. These effects are implicit in the income and substitution effects we will explore shortly.

reduces the supply of leather goods, shifts to the left side of the supply curve and increases the price of leather goods.