CASH FLOW STATEMENT

DR.NARESH KUMAR

HOD COMMERCE

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An explanation of the cash flow statement and the calculation of cash from operating activities using both the direct and indirect methods. It includes examples and working notes for better understanding.

Typology: Lecture notes

1 / 55

This page cannot be seen from the preview

Don't miss anything!

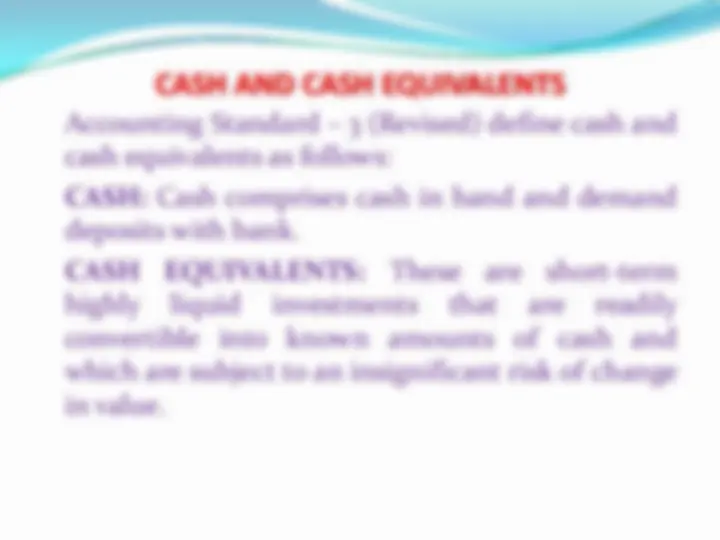

As per para 5 of Accounting Standard – 3 (Revised), cash flows are inflows and outflows of cash and cash equivalents.

Though cash flow statement, an attempt is being made to

focus on cash and cash equivalents.

Inflows (sources) may be due to issue of share capital, sale

of fixed assets, sale of investments, etc.

Outflow (usage) may be due to purchase of fixed assets,

redemption of preference shares or debentures, etc.

Difference between Inflows and outflows of cash and cash

equivalents is termed as net increase or decrease in cash and cash equivalents as the case may be.

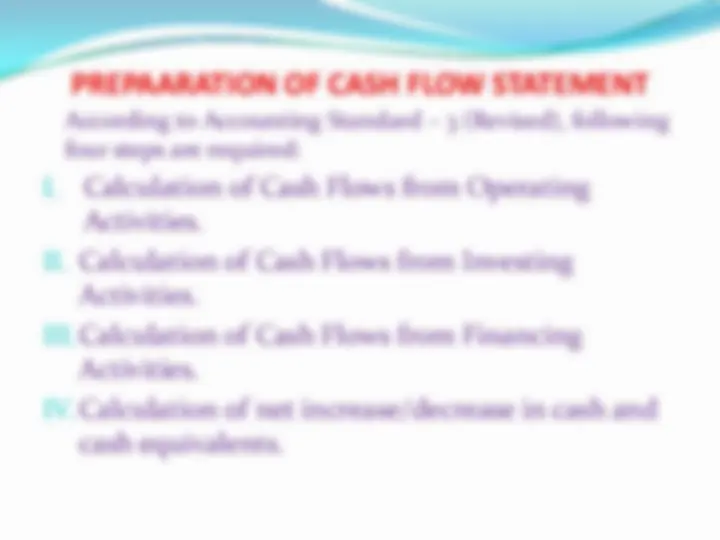

According to Accounting Standard – 3 (Revised), following four steps are required:

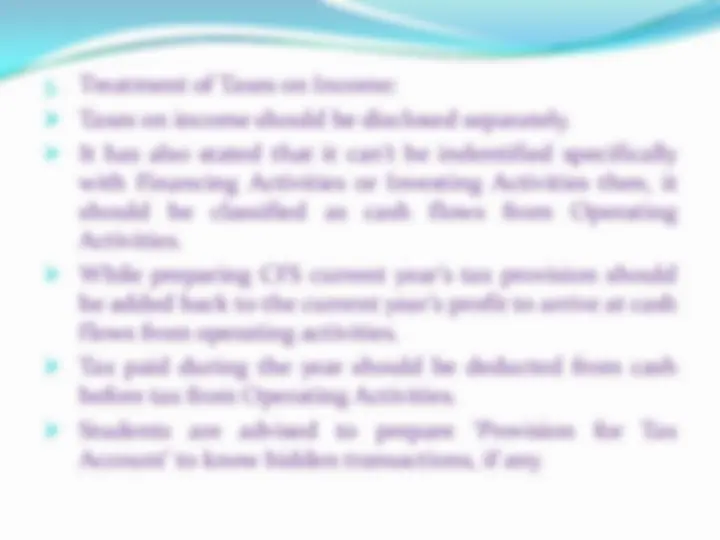

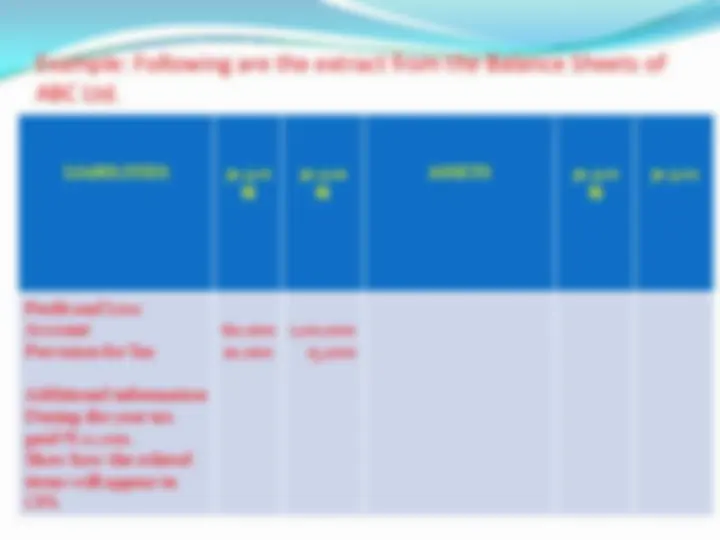

I. Calculation of Cash Flow from Operating Activites Cash flows from operating activities can be computed with the help of Income Statement of the current year, comparative Balance Sheets and the relevant additional information. As per AS – 3 (Revised), the following types activities can be regarded as cash flow from operating activities: Cash received from the sale of goods or rendering some services; Cash received from royalties, fees, commission and other revenue; Cash paid to suppliers for goods or services; Cash paid to employees or behalf of employees; Cash received or paid to insurance companies for premiums claims, annuities or other policy benefits; Cash paid as income tax or refund of income tax unless, they can be specifically identified with financing or investing activities; and Cash received or paid for future contracts, forward contracts, option contracts and swap contracts, when these are held for dealing or trading purpose.

Step (i) Calculation Cash Receipts from Sales N N Cash Sales xxx xxx Credit Sales xxx xxx Add: Opening Debtors and B/R xxx xxx Less: Closing Debtors and B/R xxx xxx Total Cash realized from sales xxx xxx Step (ii) Calculation of Cash Paid to Suppliers Cost of goods sold xxx xxx Add: Closing Stock xxx xxx Less: Opening Stock xxx xxx Total Purchases xxx xxx Add: Opening Creditors & B/P xxx xxx Less: Closing Creditors & B/P xxx xxx Cash paid to Suppliers xxx xxx

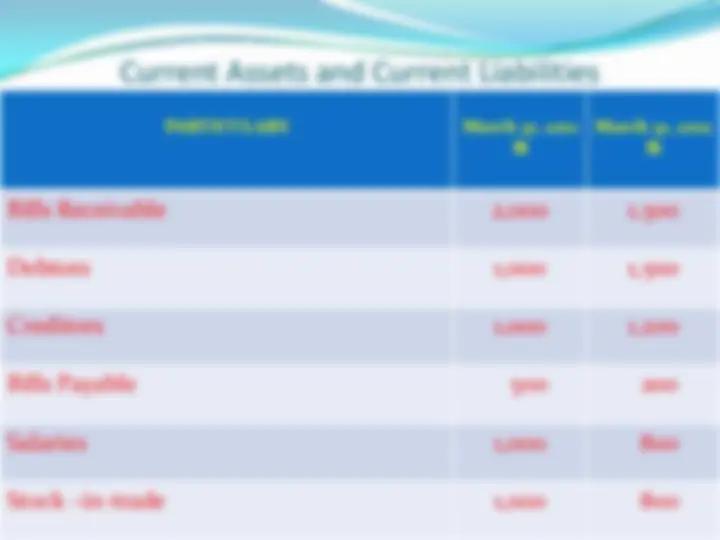

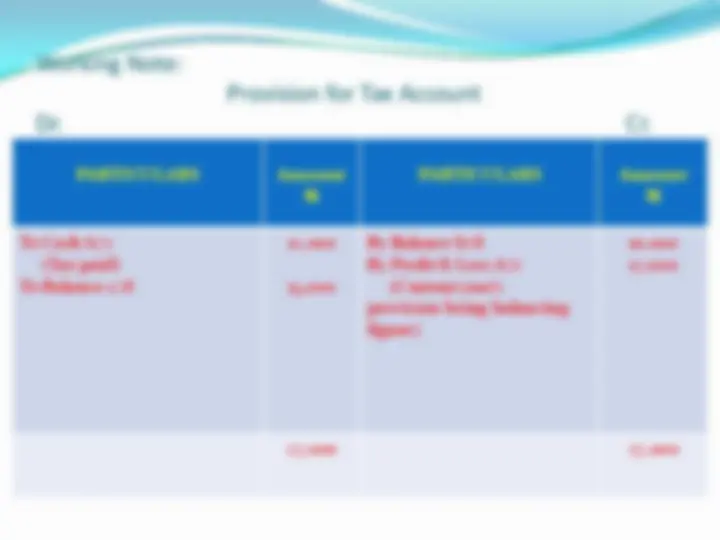

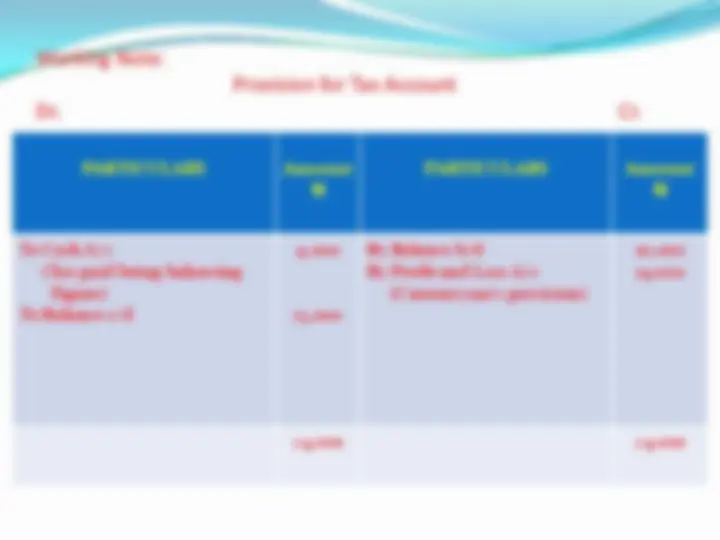

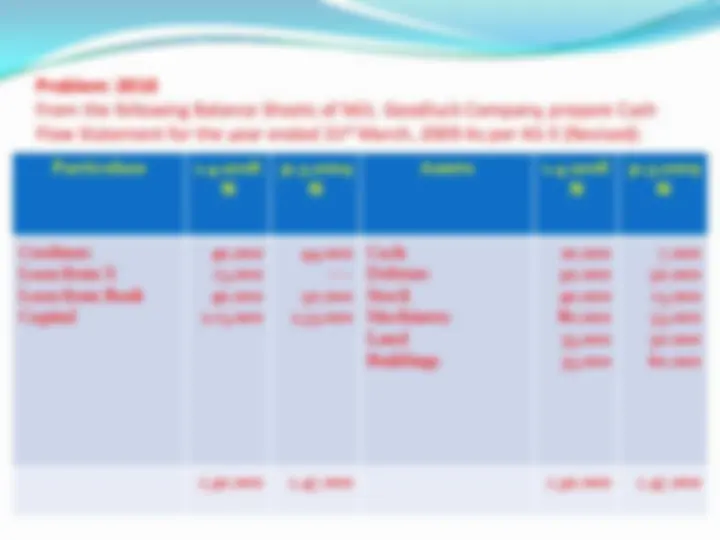

Step (iii) Calculation of Cash paid for any Expenses N N Expenses xxx xxx Add: O/S Expenses in the beginning xxx xxx Less: O/S Expenses at the end xxx xxx Cash paid for Expenses xxx xxx Problem: From the following information available from the books of X ltd. Compute cash from operating activities. Income Statement For the year ending 31st^ March, 2012 Sales N 18, Less: Cost of goods sold N 12, Gross margin N 5, Less: S & D Expenses N 2, Salaries N 1, Depreciation of Plant N 500 N 3, Net margin N 2,

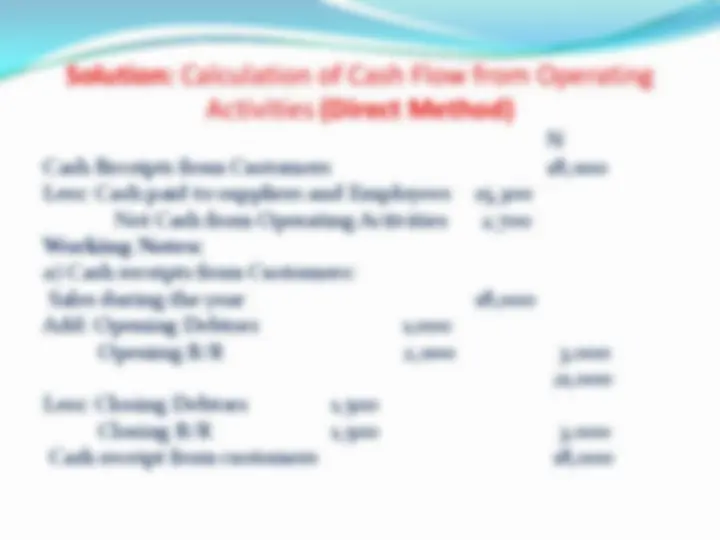

Solution: Calculation of Cash Flow from Operating Activities (Direct Method) N Cash Receipts from Customers 18, Less: Cash paid to suppliers and Employees 15, Net Cash from Operating Activities 2, Working Notes: a) Cash receipts from Customers: Sales during the year 18, Add: Opening Debtors 1, Opening B/R 2,000 3, 21, Less: Closing Debtors 1, Closing B/R 1,500 3, Cash receipt from customers 18,

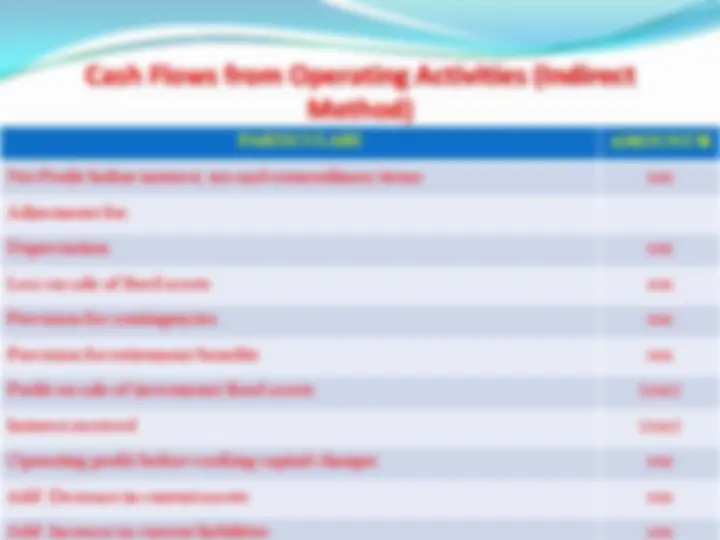

Cash Flows from Operating Activities (Indirect Method) PARTICULARS (^) AMOUNT N

Net Profit before interest, tax and extraordinary items xxx

Adjustment for:

Depreciation xxx

Loss on sale of fixed assets xxx

Provision for contingencies xxx

Provision for retirement benefits xxx

Profit on sale of investment/fixed assets (xxx)

Interest received (xxx)

Operating profit before working capital changes xxx

Add: Decrease in current assets xxx

Add: Increase in current liabilities xxx

Less: Increase in current assets Less: Decrease in current liabilities

(xxx) (xxx)

Cash generated from operations xxx

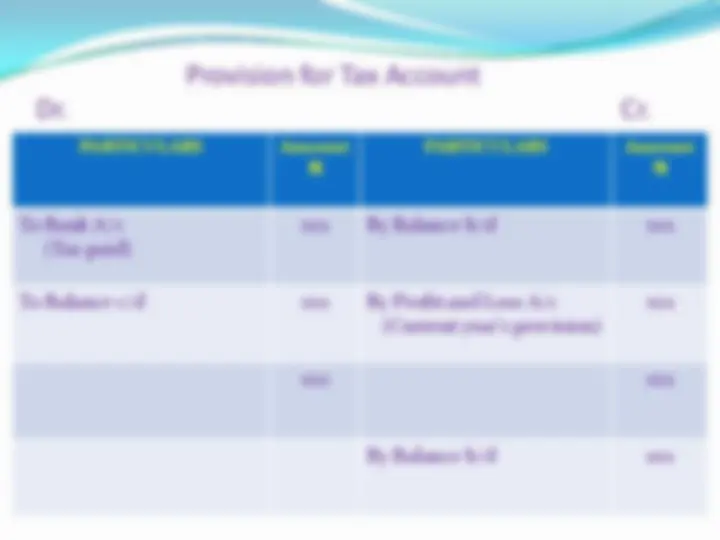

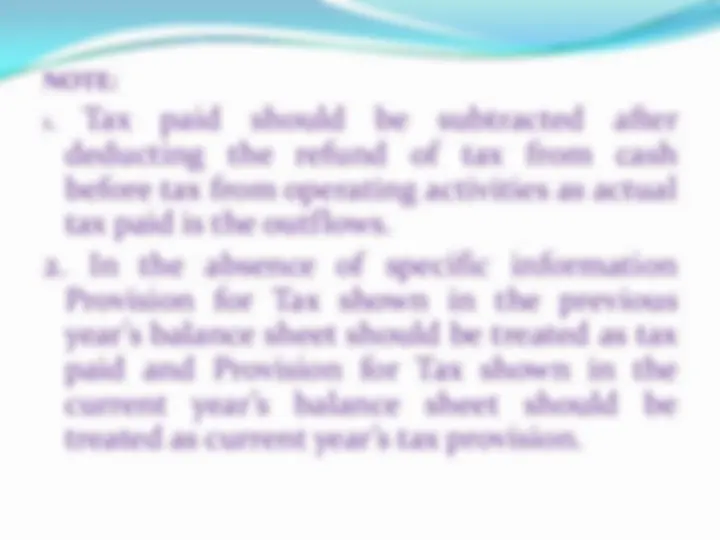

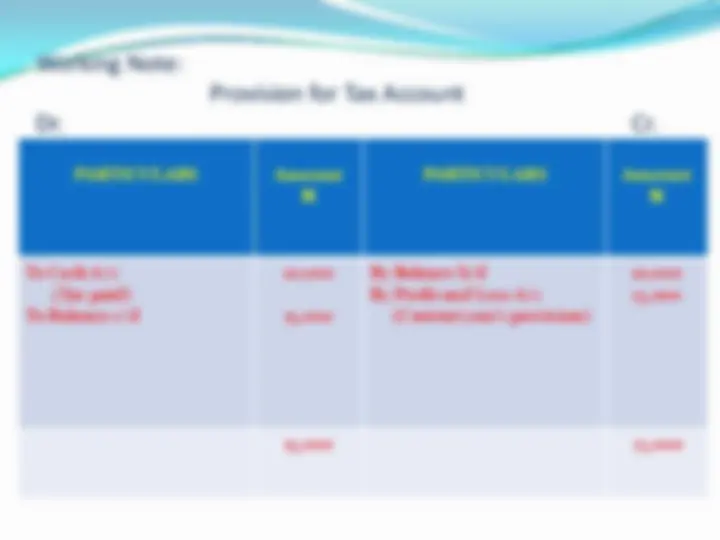

Tax paid (xxx)

Cash flows before extraordinary items xxx

± Extra ordinary items xxx

NET CASH FROM OPERATING ACTIVITIES xxx

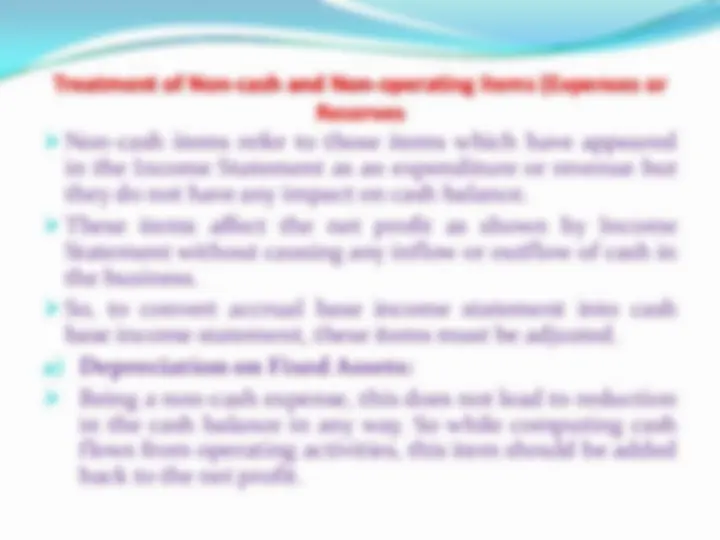

b) Amortization of Intangible assets, viz., Goodwill, Trade Marks, Patents, etc.:

This amortization of intangible assets reduces the net profit but do not affect the cash flow in any way. So to calculate cash flows from operating activities, the value of amortization of assets should be added back to net profit.

c) Fictitious Assets written off, e.g., preliminary expenses:

These also have nothing to do with the cash flows but reduce the net profit. So these expenses should be added back for the computation of cash flow from operating activities.

d) Profit or loss on sale of fixed assets:

Profit or loss on sale of fixed assets should be added back or deducted respectively, to the net profit figure, so that cash flow from operating activities can be computed.

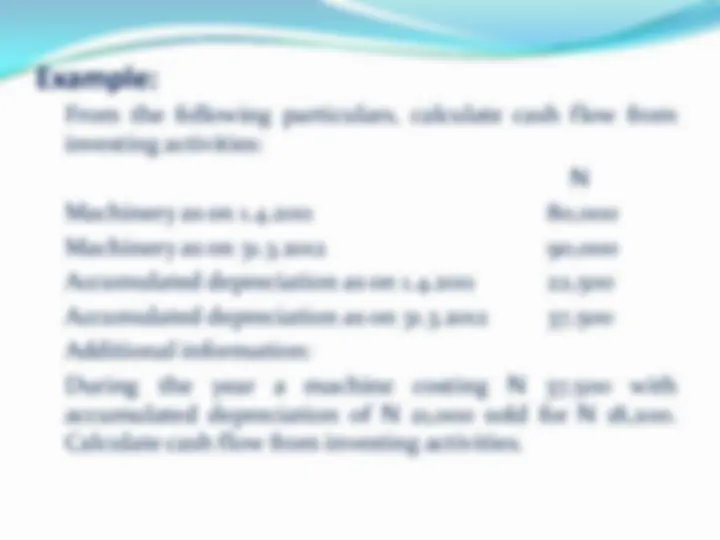

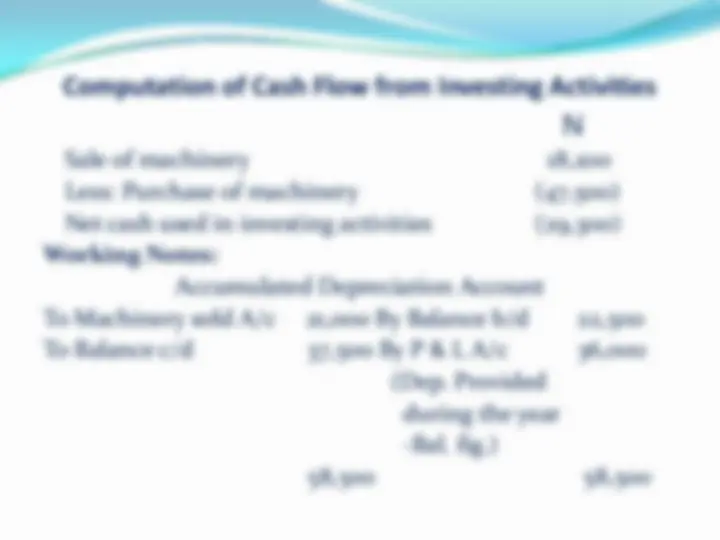

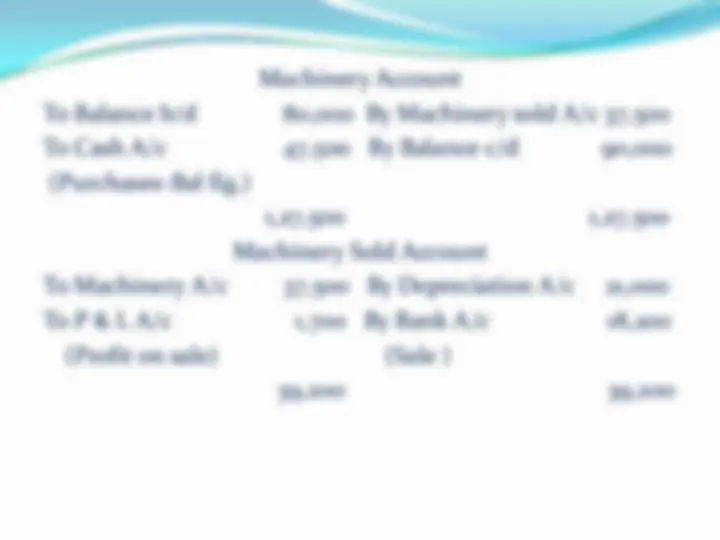

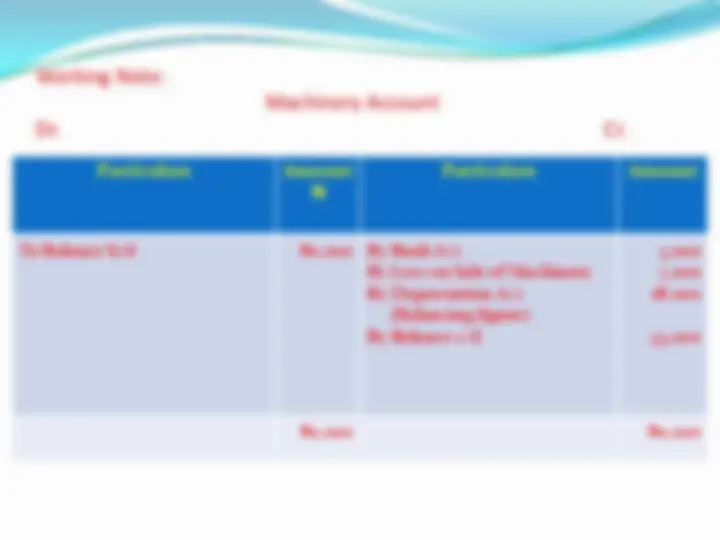

In case, a fixed assets is sold during the year following treatment should be accounted for:

(i) Calculate the depreciation charged on the assets during the year by preparing “Accumulated Depreciation Account” to be added to the net income for the year before adjustment.

(ii) Calculate amount of profit or loss on the sale of the part of that fixed assets which shall either of subtracted or add respectively to the net income for the year before adjustment.

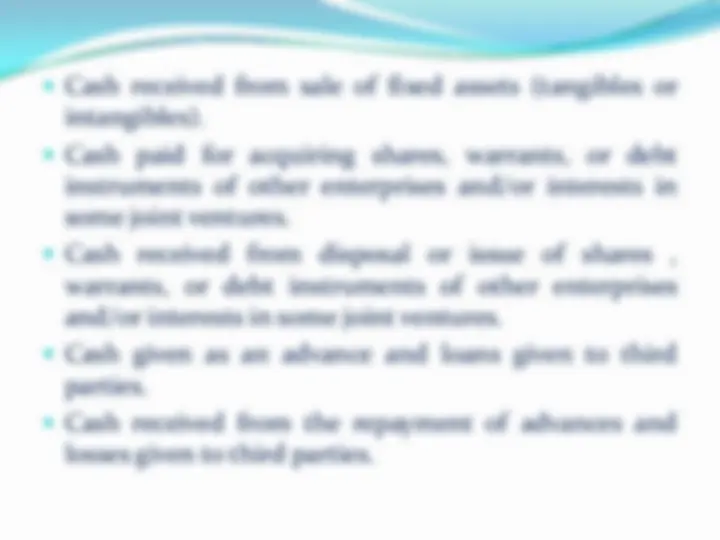

(iii) Amount of cash received on sale of asset must be added under the head “Cash Flow from Investing Activities”

(iv) Amount of cash paid (if any) on purchase of fixed assets must be subtracted from investing activities.