LECTURE EXAMPLE 13

COMPLETE CASH FLOW STATEMENT

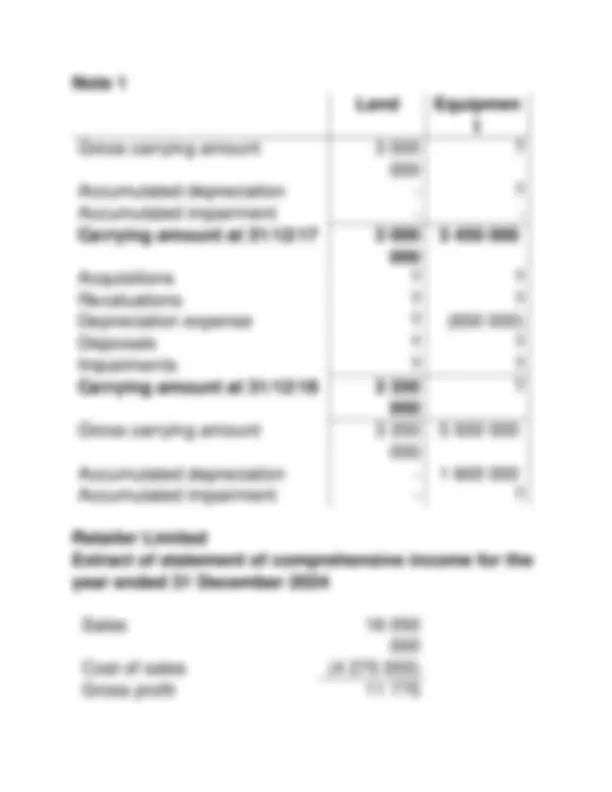

Retailer Limited

Statement of financial position of Retailer Limited as

at 31 December 2024

2024 2023

Assets

Non-current assets

PPE (Note 1) 7 242 700 6 450 000

Current assets

Inventory 5 000 000 4 750 000

Prepaid expenses 400 000 175 000

Trade receivables 5 500 000 2 750 000

Bank 1 897 300 0

20 040 000 14 125 000

Equity

Share capital 1 750 000 1 000 000

Share premium 2 000 000 1 200 000

Revaluation surplus 700 000 500 000

Retained earnings 4 685 000 1 562 500

Non-current Liabilities

Loans 3 000 000 4 000 000

Current liabilities

Trade payables 7 000 000 3 500 000