Download Chemicals - E-Commerce - Lecture Slides and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

Deutsche Bank in stable growth

¨ At the end of year 5, the firm is in stable growth. We assume that the cost

of equity drops to 8.5% (as the beta moves to 1) and that the return on

equity also drops to 8.5 (to equal the cost of equity).

Stable Period Payout RaEo = 1 – g/ROE = 1 – 0.03/0.085 = 0.6471 or 64.71% Expected Dividends in Year 6 = Expected Net Income 5 (1+gStable ) Stable Payout RaEo = €5,143 (1.03) * 0.6471 = €3,427 million Terminal Value = PV of Terminal Value =

¨ Value of equity = €9,653+ €40,079 = €49,732 million Euros

¨ Value of equity per share=

Stock was trading at 89 Euros per share at the Eme of the analysis.

Expected Dividends 6

(Cost of Equity-g)

= 62, 318 million Euros

Terminal Value n

(1+Cost of Equity High growth )

n

5

= 40, 079 mil Euros

Value of Equity

# Shares

= 104.88 Euros/share

What does the valuaEon tell us? One of three possibiliEes…

¨ Stock is under valued: This valuaEon would suggest that Deutsche Bank is significantly overvalued, given our esEmates of expected growth and risk. ¨ Dividends may not reflect the cash flows generated by Deutsche Bank. The FCFE could have been significantly lower than the dividends paid. ¨ EsEmates of growth and risk are wrong: It is also possible that we have over esEmated growth or under esEmated risk in the model, thus reducing our esEmate of value.

Stable growth and value….

¨ ARer year five, we will assume that the beta will increase to 1 and that

the equity risk premium will decline to 7.5 percent (we assumed India

country risk would drop). The resulEng cost of equity is 11.5 percent.

Cost of Equity in Stable Growth = 4% + 1(7.5%) = 11.5%

¨ We will assume that the growth in net income will drop to 4% and that

the return on equity will rise to 11.5% (which is also the cost of equity).

Equity Reinvestment Rate (^) Stable Growth = 4%/11.5% = 34.78% FCFE in Year 6 = 10,449(1.04)(1 – 0.3478) = Rs 7,087 million Terminal Value of Equity = 7,087/(0.115 – 0.04) = Rs 94,497 million

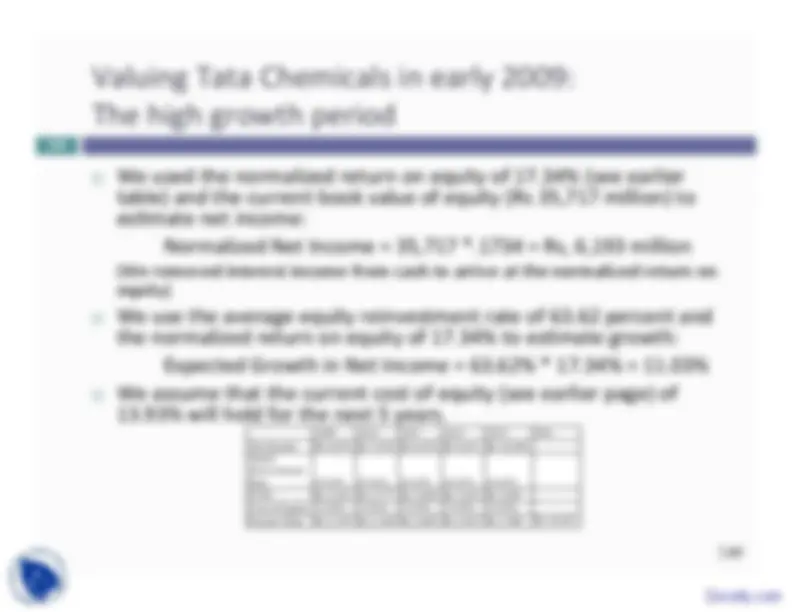

¨ To value equity in the firm today

Value of equity = PV of FCFE during high growth + PV of terminal value + Cash = 10,433 + 94,497/1.13935 +1,759 = Rs 61,423 million ¤ Dividing by 235.17 million shares yields a value of equity per share of Rs 261, about 20% higher than the stock price of Rs 222 per share.

Disney: Inputs to ValuaEon

253

Ways of changing value…

Cashflows from existing assets Cashflows before debt payments, but after taxes and reinvestment to maintain exising assets Expected Growth during high growth period Growth from new investments Growth created by making new investments; function of amount and quality of investments Efficiency Growth Growth generated by using existing assets better Length of the high growth period Since value creating growth requires excess returns, this is a function of

- Magnitude of competitive advantages

- Sustainability of competitive advantages Stable growth firm, with no or very limited excess returns Cost of capital to apply to discounting cashflows Determined by

- Operating risk of the company

- Default risk of the company

- Mix of debt and equity used in financing How well do you manage your existing investments/assets? Are you investing optimally for future growth? Is there scope for more efficient utilization of exsting assets? Are you building on your competitive advantages? Are you using the right amount and kind of debt for your firm?

First Principles