Download Directors - E-Commerce - Lecture Slides and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

13

Board of Directors as a disciplinary mechanism

13

¨ In 2010, the median board member at a Fortune 500

company was paid $212,512, with 54% coming in stock

and the remaining 46% in cash. If a board member is a

non-‐execuKve chair, he or she receives about $150,

more in compensaKon.

¨ A board member works, on average, about 227.5 hours a

year (and that is being generous), or 4.4 hours a week,

according to the NaKonal Associate of Corporate

Directors. Of this, about 24 hours a year are for board

meeKngs.

¨ Many directors serve on three or more boards, and

some are full Kme chief execuKves of other companies.

14

The CEO o\en hand-‐picks directors..

14

¨ A 1992 survey by Korn/Ferry revealed that 74% of companies relied on recommendaKons from the CEO to come up with new directors; Only 16% used an outside search firm. While that number has changed in recent years, CEOs sKll determine who sits on their boards. While more companies have outsiders involved in picking directors now, CEOs sKll exercise significant influence over the process.

¨ Directors o\en hold only token stakes in their companies. The Korn/Ferry survey found that 5% of all directors in 1992 owned less than five shares in their firms. Most directors in companies today sKll receive more compensaKon as directors than they gain from their stockholdings. While share ownership is up among directors today, they usually get these shares from the firm (rather than buy them).

¨ Many directors are themselves CEOs of other firms. Worse sKll, there are cases where CEOs sit on each other’s boards.

16

Who’s on Board? The Disney Experience -‐ 1997

16

17

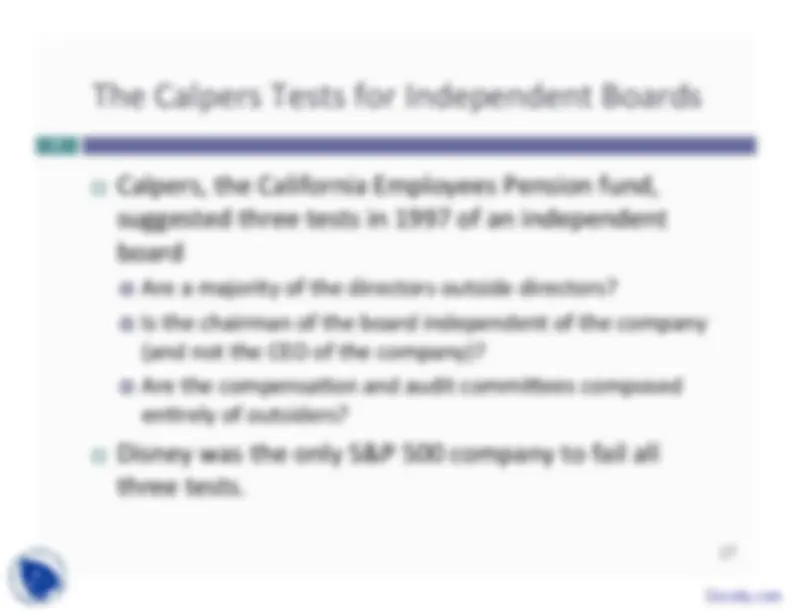

The Calpers Tests for Independent Boards

17

¨ Calpers, the California Employees Pension fund,

suggested three tests in 1997 of an independent

board

¤ Are a majority of the directors outside directors?

¤ Is the chairman of the board independent of the company

(and not the CEO of the company)?

¤ Are the compensaKon and audit commiCees composed

enKrely of outsiders?

¨ Disney was the only S&P 500 company to fail all

three tests.

19

ApplicaKon Test: Who’s on board?

19

¨ Look at the board of directors for your firm.

¤ How many of the directors are inside directors (Employees

of the firm, ex-‐managers)?

¤ Is there any informaKon on how independent the directors

in the firm are from the managers?

¨ Are there any external measures of the quality of

corporate governance of your firm?

¤ Yahoo! Finance now reports on a corporate governance

score for firms, where it ranks firms against the rest of the

market and against their sectors.

20

So, what next? When the cat is idle, the mice

will play ....

20

¨ When managers do not fear stockholders, they will o\en put

their interests over stockholder interests

¤ Greenmail: The (managers of ) target of a hosKle takeover buy out the potenKal acquirer's exisKng stake, at a price much greater than the price paid by the raider, in return for the signing of a 'standsKll' agreement. ¤ Golden Parachutes: Provisions in employment contracts, that allows for the payment of a lump-‐sum or cash flows over a period, if managers covered by these contracts lose their jobs in a takeover. ¤ Poison Pills: A security, the rights or cashflows on which are triggered by an outside event, generally a hosKle takeover, is called a poison pill. ¤ Shark Repellents: AnK-‐takeover amendments are also aimed at dissuading hosKle takeovers, but differ on one very important count. They require the assent of stockholders to be insKtuted. ¤ Overpaying on takeovers: AcquisiKons o\en are driven by management interests rather than stockholder interests.

No stockholder

(^) approval

(^) needed….. Stockholder Approval needed

A case study in value destrucKon:

Eastman Kodak & Sterling Drugs

Kodak enters bidding war

¨ In late 1987, Eastman Kodak entered into a bidding war with Hoffman La Roche for Sterling Drugs, a pharmaceuKcal company.

¨ The bidding war started with Sterling Drugs trading at about $40/share.

¨ At $72/share, Hoffman dropped out of the bidding war, but Kodak kept bidding.

¨ At $89.50/share, Kodak won and claimed potenKal synergies explained the premium.

Kodak wins!!!!

!

23

Earnings and Revenues at Sterling Drugs

23

Sterling Drug under Eastman Kodak: Where is the synergy?

0

500

1,

1,

2,

2,

3,

3,

4,

4,

5,

1988 1989 1990 1991 1992

Revenue Operating Earnings