Macroeconomic Models III

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

This lecture is part of lecture series on Economic Forecasting course. Keywords in this lecture are below: Conditional Forecasting, Macroeconomic Models, Multiple Variable Forecasting Models, Conditional Forecasts, Macroeconomic Forecasting Models, Exogenous Variables, Monetary Policy Variables, Fiscal Policy Variables, Economic Forecasts, Combining Forecasts

Typology: Slides

1 / 25

This page cannot be seen from the preview

Don't miss anything!

Macroeconomic Models III

Conditional Forecasting

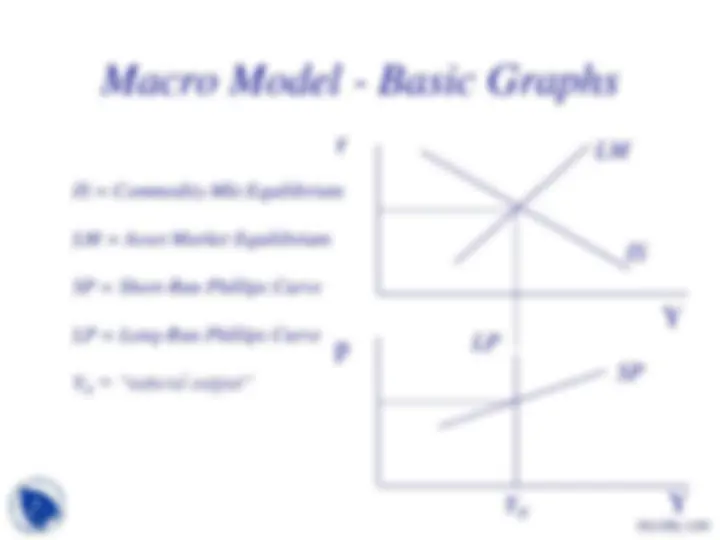

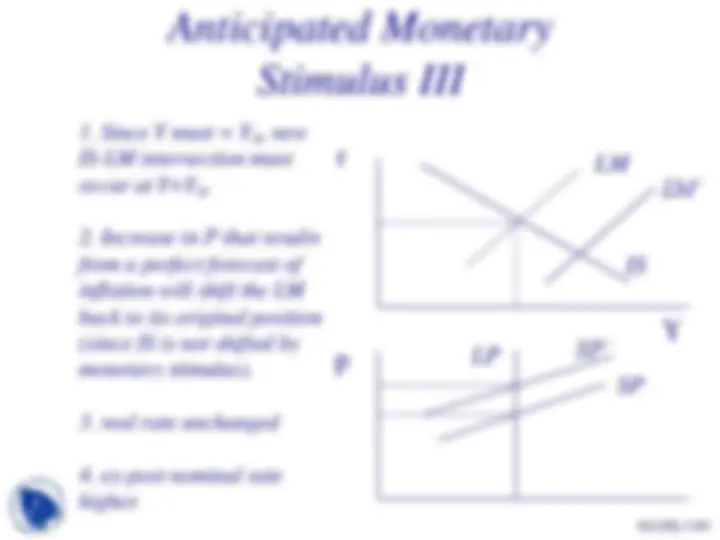

IS = Commodity Mkt Equilibrium

LM = Asset Market Equilibrium

SP = Short-Run Phillips Curve

LP = Long-Run Phillips Curve

YN = “natural output”

Assume:

Alternative initial conditions are possible (e.g. positive inflation and expected inflation); but these parameters keep difficulties to a minimum.

YN docsity.com

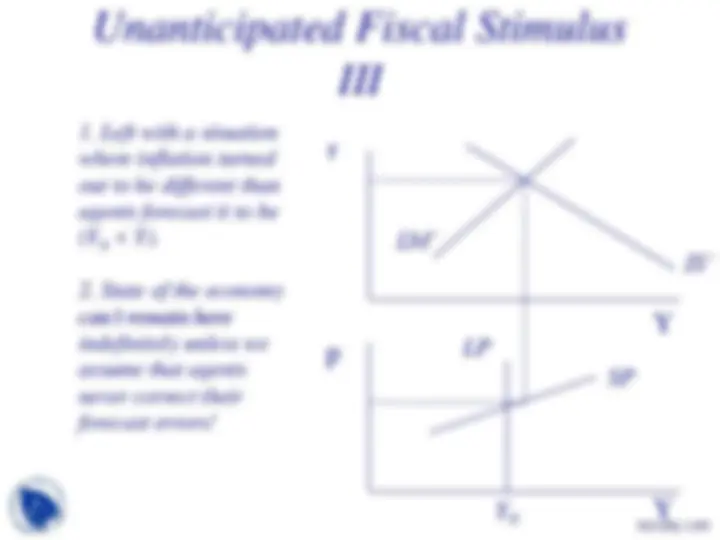

What happens to the economy if the fiscal stimulus is announced in advance of the action.

Depends on whether agents think that the announcement is credible. Talk is cheap; if not believed then it is the same as making no announcement.

If announcement is credible, then effect on economy depends on how agents forecast.

If agents make forecasts based only on history of economy, then the prospective fiscal change is not something they consider in constructing their forecasts.

Their expectations of future inflation do not depend on information about future fiscal policy.

If so: at time of the stimulus, inflation expectations adjust, SP curve shifts.

What is the initial effect of a fiscal shock in an environment where agents make perfect forecasts of inflation, or the ultimate effect in a world where agents make forecasting errors but eventually will correct them?

on real output?

What is the impact of the deficit created by the fiscal stimulus (anticipated or unanticipated) on:

Issues here are the same as in fiscal policy:

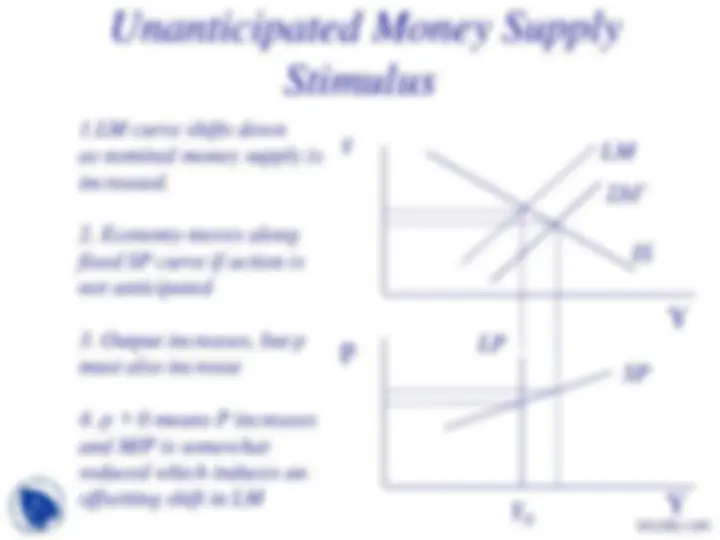

Does this end the story of the response to a monetary stimulus when conditional forecasts of inflation are accurate?

Depends on the nature of the monetary shock