Download Continuous-Time Methods in Macroeconomics and more Lecture notes Macroeconomics in PDF only on Docsity!

Continuous-Time Methods in Macroeconomics

Jes´us Fern´andez-Villaverde^1 and Galo Nu˜no^2 October 15, 2021 (^1) University of Pennsylvania

(^2) Banco de Espa˜na

Motivation

- Many interesting questions in macroeconomics require:

- Nonlinear techniques. Examples: How do financial crises arise? Why do countries or firms default? When do firms invest in large, lumpy projects? Why do individuals decide to migrate?

- Heterogeneous agents. Examples: What mechanisms account for changes in income and wealth inequality? Is there a trade-off between inequality and economic growth? How does inequality affect monetary and fiscal policy? What are the consequences of entry-exit in models of industry dynamics?

- Many state variables. Examples: Discrete node models, corporate finance models, rich life-cycle models, models where parameters are quasi-states.

- Often, all three elements come together. Example: heterogeneous agents models with nominal frictions and many assets.

Our goal

- Move to the “feasible” region of the Big-O complexity chart.

- This is relevant both for time and memory complexity.

- In particular, we want to find ways to keep the “curse of dimensionality” under control.

Taming the “curse of dimensionality”

- Three strategies:

- Better numerical algorithms (i.e., continuous-time methods, deep learning).

- Better software implementations (i.e., robust OS, modern programming languages, functional programming, flexible data structures, advances in massive parallelization).

- Better hardware designs (i.e., GPUs, AI accelerators, FPGAs).

- Some of these techniques are relatively new in economics or, at least, less familiar to many researchers.

- A complete treatment of the material would require at least a whole semester.

- In this class, we will focus on better numerical algorithms: continuous-time methods and deep learning.

Why continuous time? I

- Long and illustrious tradition in finance: classical results by Merton and others.

- However, less used in macroeconomics (except in growth and neoclassical investment theories).

- Why?

- Economic data comes in discrete intervals: most time-series is in discrete time.

- Arrival of dynamic programming in the early 1970s.

- Stochastic calculus has some entry cost (notice: in growth theory, you can often skip stochastic calculus because you deal with deterministic models).

- Recent “boom” of continuous-time methods in business cycle research and related areas: Stokey (2009), Brunnermeier and Sannikov (2014), Ahn et al. (2017), ...

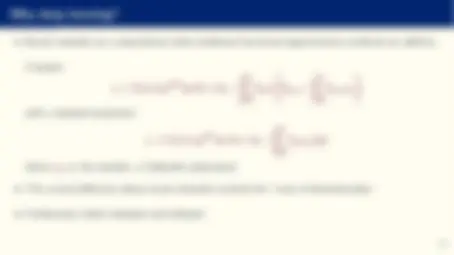

Why continuous time? II

- Itˆo’s Lemma allow us to substitute the integrals of discrete time for derivatives in continuous time). Bellman equation: V (x) = max α

u (α, x) + β

V (x′) p(dx|α, x)

vs. Hamilton-Jacobi-Bellman equation:

ρVt (x) = ∂V ∂t

u (α, x) +

∑^ N

n=

μnt (x, α) ∂V ∂xn

+^1

∑^ N

n 1 ,n 2 =

σ^2 t (x, α)

n 1 ,n 2

∂^2 V

∂xn 1 ∂xn 2

- Why is this so important? Integrals depend on typical sets and typical sets are hard to characterize: the average member of a population with many dimensions (the “Asimov data set”) is an outlier.

- Check: https://mc-stan.org/users/documentation/case-studies/curse-dims.html.

Why deep learning?

- Neural networks are compositional while traditional functional approximation methods are additive.

Compare: y = f (x) ∼= g NN^ (x; θ) = θ 0 +

∑^ M

m=

θmφ

θ 0 ,m +

∑^ N

n=

θn,mxn

with a standard projection:

y = f (x) ∼= g CP^ (x; θ) = θ 0 +

∑^ M

m=

θmφm (x)

where φm is, for example, a Chebyshev polynomial.

- This crucial difference allows neural networks to break the “curse of dimensionality.”

- Furthermore, better hardware and software.

Course outline

- Dynamic programming in continuous time.

- Deep learning and reinforcement learning.

- Heterogeneous agent models.

- Optimal policy with heterogeneous agent models.

... or this

-2 0 2 4

0

1

2

3

4

0.85-2 0 2 4

1

-0.1-2 0 2 4

-0.

0

(^0) -2 0 2 4

Low zHigh z