Download Dynamic Programming in Continuous Time and more Study notes Calculus in PDF only on Docsity!

Dynamic programming in continuous time

Jes´us Fern´andez-Villaverde^1 and Galo Nu˜no^2 October 15, 2021 (^1) University of Pennsylvania

(^2) Banco de Espa˜na

Basic ideas

Why dynamic programming in continuous time?

- Continuous time methods transform optimal control problems into partial differential equations (PDEs): 1. The Hamilton-Jacobi-Bellman equation, the Kolmogorov Forward equation, the Black-Scholes equation,... they are all PDEs. 2. Solving these PDEs turns out to be much simpler than solving the Bellman or the Chapman-Kolmogorov equations in discrete time. Also, much knowledge of PDEs in natural sciences and applied math. 3. Key role of typical sets in the “curse of dimensionality.”

- Dynamic programming is a convenient framework:

- It can do everything economists could get from calculus of variations.

- It is better than Hamiltonians for the stochastic case.

The development of “continuous-time methods”

- Differential calculus introduced in the 17th century by Isaac Newton and Gottfried Wilhelm Leibniz.

- In the late 19th century and early 20th century, it was extended to accommodate stochastic processes (“stochastic calculus”). - Thorvald N. Thiele (1880): Introduces the idea of Brownian motion. - Louis Bachelier (1900): Formalizes the Brownian motion and applies to the stock market. - Albert Einstein (1905): A model of the motion of small particles suspended in a liquid. - Norbert Wiener (1923): Uses the ideas of measure theory to construct a measure on the path space of continuous functions. - Andrey Kolmogorov (1931): Diffusions depend on drift and volatility, Kolmogorov equations. - Wolfgang D¨oblin (1938-1940): Modern treatment of diffusions with a change of time. - Kiyosi Itˆo (1944): Itˆo’s Lemma. - Paul Malliavin (1978): Malliavin calculus. 3

The development of “dynamic programming”

- Calculus of variations: Issac Newton (1687), Johann Bernoulli (1696), Leonhard Euler (1733), Joseph-Louis Lagrange (1755).

- 1930s and 1940s: many problems in aerospace engineering are hard to tackle with calculus of variations. Example: minimum time interception problems for fighter aircraft.

- Closely related to the Cold War.

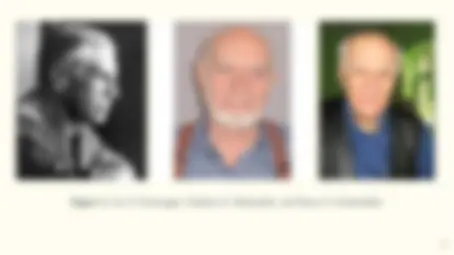

- Lev S. Pontryagin, Vladimir G. Boltyanskii, and Revaz V. Gamkrelidze (1956): Maximum principle.

- Magnus R. Hestenes, Rufus P. Isaacs, and Richard E. Bellman at RAND (1950s):

- Distinction between controls and states.

- Principle of optimality.

- Dynamic programming.

Figure 2. The mathematicians at Steklov: Lev Semyonovich Pontryagin,

Vladimir Grigor’evich Boltyanskii, and Revaz Valerianovich Gamkrelidze

Figure 1: Lev S. Pontryagin, Vladimir G. Boltyanskii, and Revaz V. Gamkrelidze

Hamilton-Jacobi-Bellman

William Hamilton (1805-1865) Carl Jacobi (1804-1851) Richard Bellman (1920-1984)

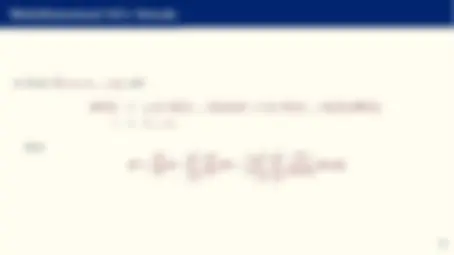

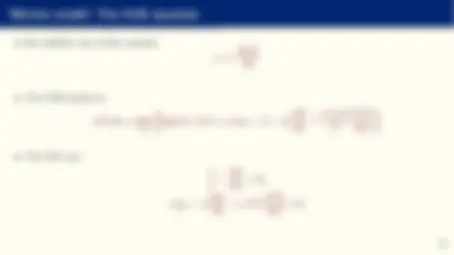

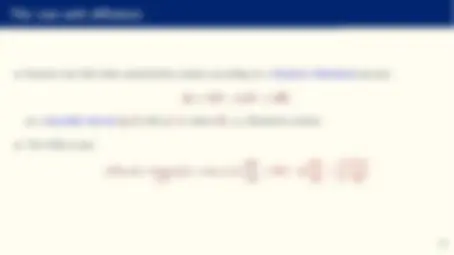

The Hamilton-Jacobi-Bellman equation

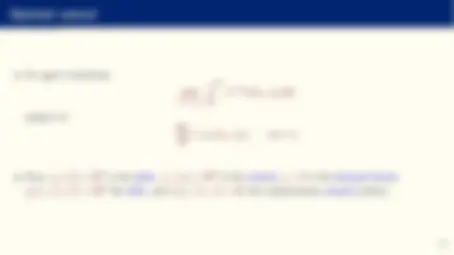

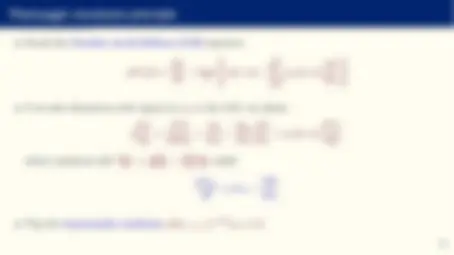

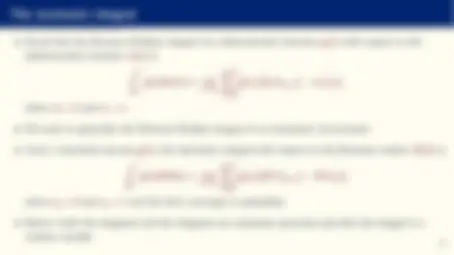

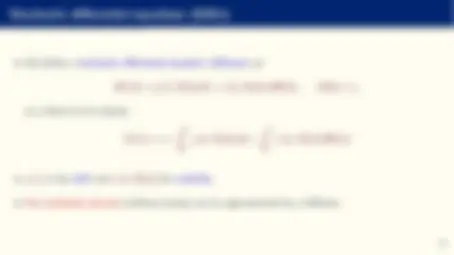

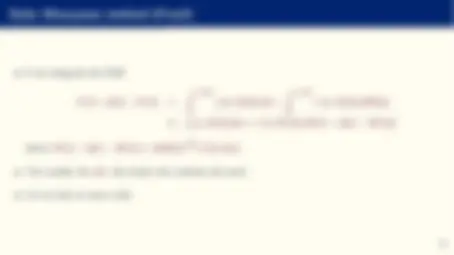

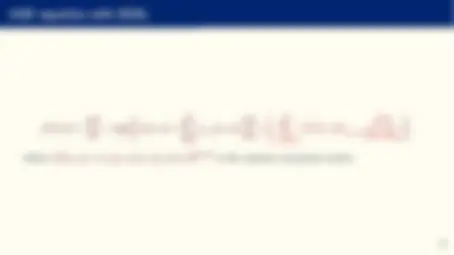

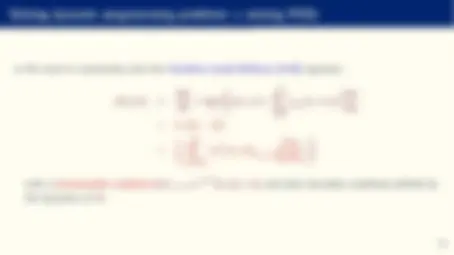

- If we define the value function:

V (t, x) = max {αs }s≥t

t

e−ρ(s−t)u (αs , xs ) ds,

then, under technical conditions, it satisfies the Hamilton-Jacobi-Bellman (HJB) equation:

ρVt (x) = ∂V ∂t

u (α, x) +

∑^ N

n=

μt,n (x, α) ∂V ∂xn

with a transversality condition limT →∞ e−ρT^ VT (x) = 0.

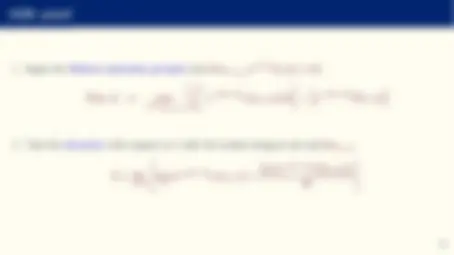

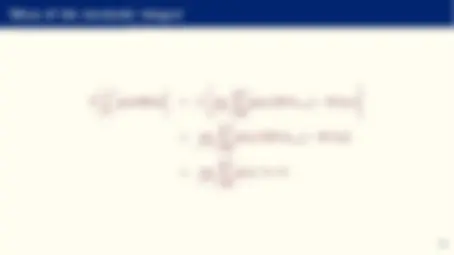

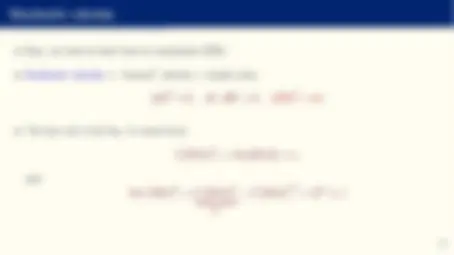

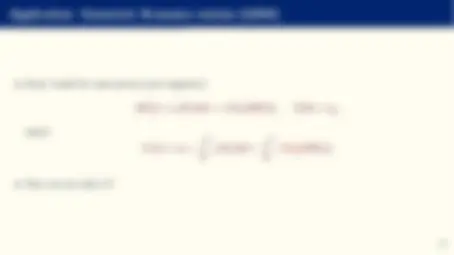

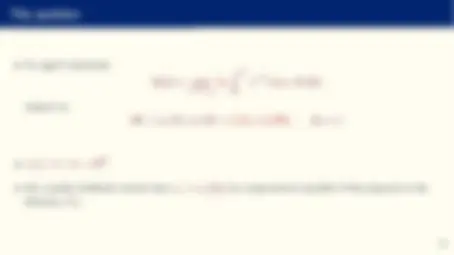

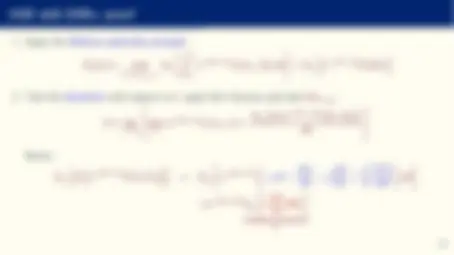

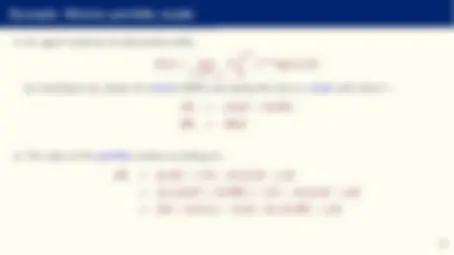

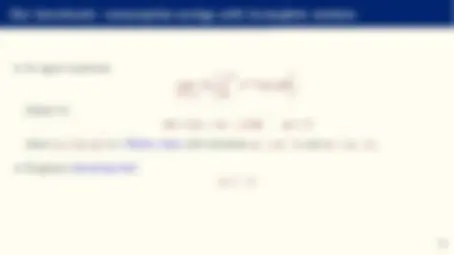

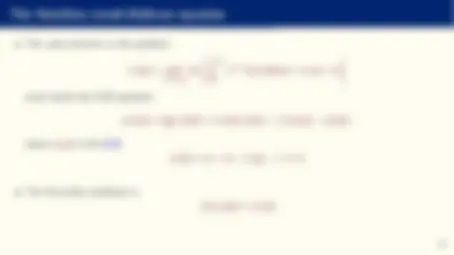

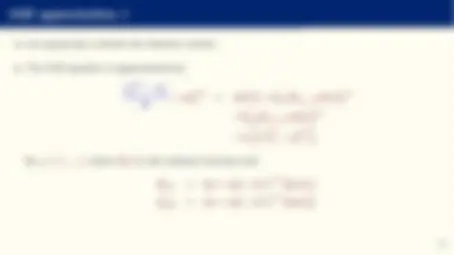

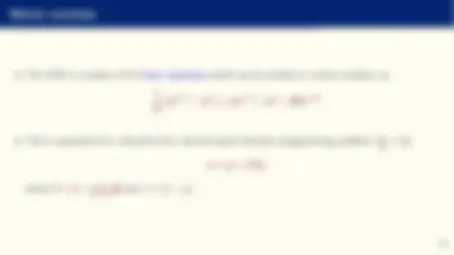

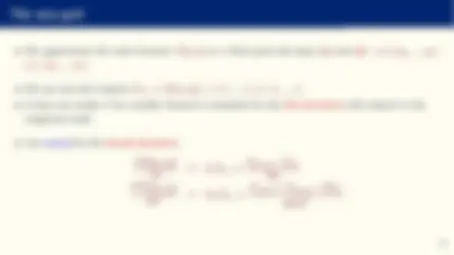

Example: consumption-savings problem

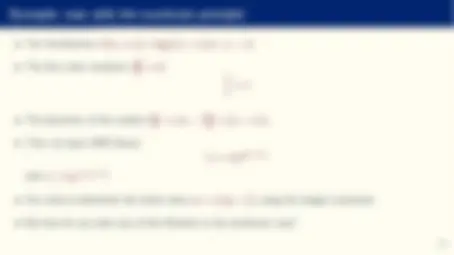

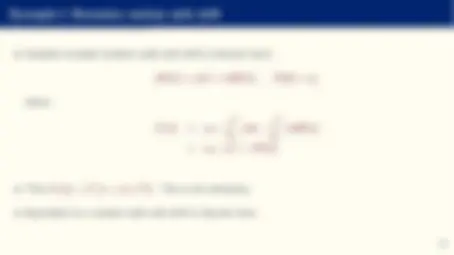

- A household solves: max {ct }t≥ 0

0

e−ρt^ log (ct ) dt,

subject to: dat dt =^ rat^ +^ y^ −^ ct^ ,^ a^0 = ¯a, where r and y are constants.

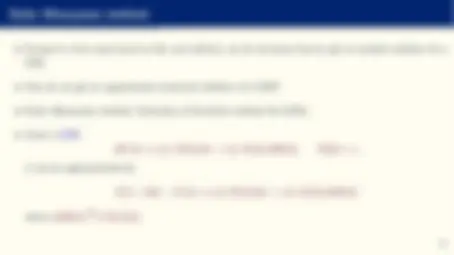

- The HJB is: ρV (a) = max c

log (c) + (ra + y − c) dV da

- Intuitive interpretation.

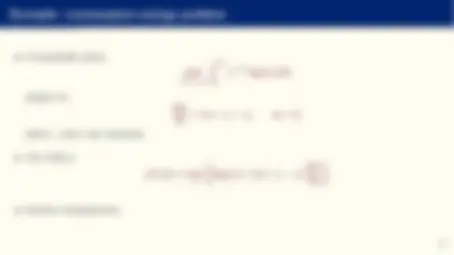

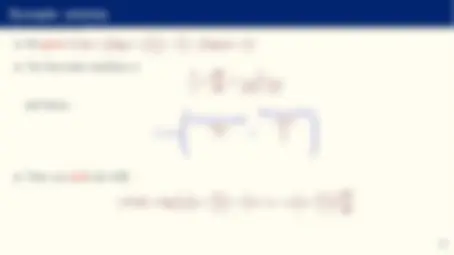

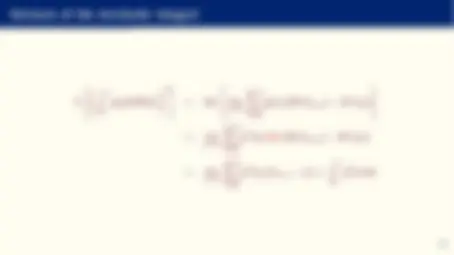

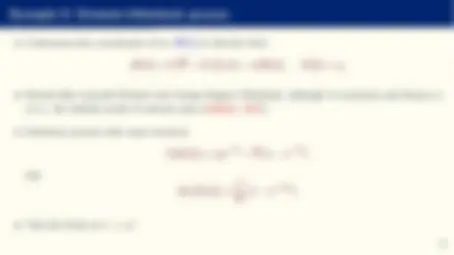

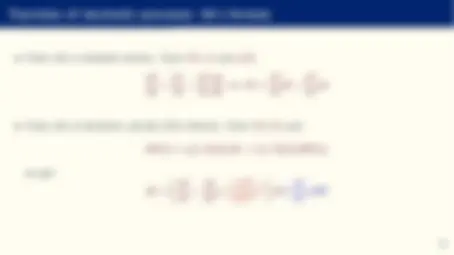

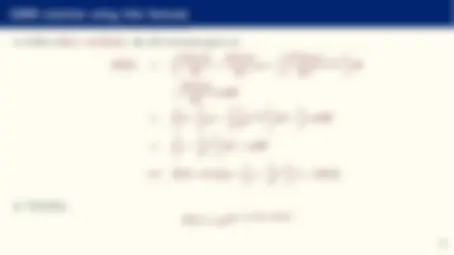

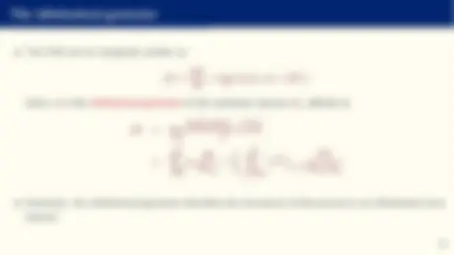

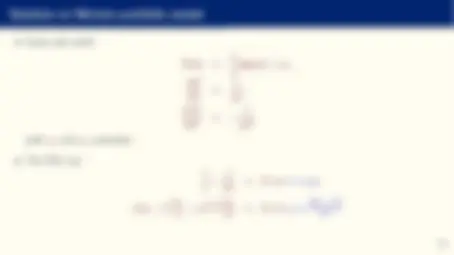

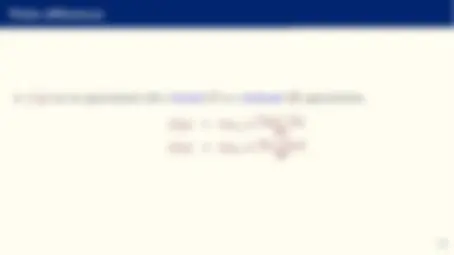

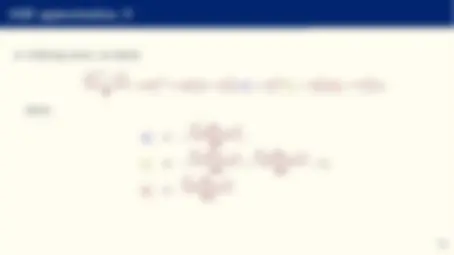

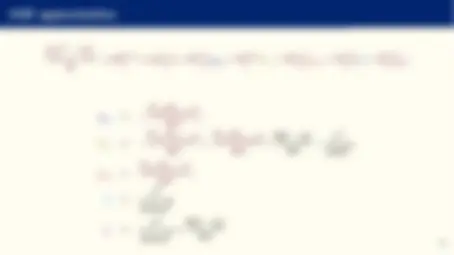

Example: solution

- We guess V (a) = (^1) ρ log ρ + (^) ρ^1

r ρ −^1

a + yr

- The first-order condition is: 1 c

dV da

ρ

a + yr

and hence:

c = ρ

Financial wealth ︷︸︸︷ a +

Human wealth ︷︸︸︷ y r

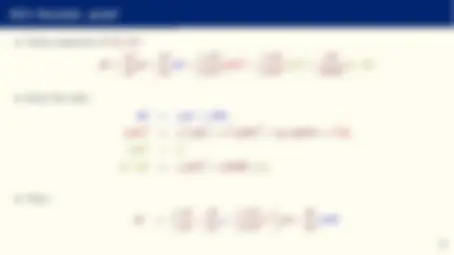

ρV (a) = log

ρ

a + y r

ra + y − ρ

a + y r

)) (^) dV da