ProfessionalDevelopmentProgramme onEnriching

KnowledgeoftheBusiness,AccountingandFinancialStudies

(BAFS)Curriculum<ElectivePart>

Course Title: Marginal and Absorption Costing

1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An illustration of the differences between marginal costing and absorption costing through various operating statements. It includes calculations of product and period costs under both methods, as well as implications for profits and inventory. useful for students and professionals seeking to understand the accounting principles of costing methods.

Typology: Study notes

1 / 70

This page cannot be seen from the preview

Don't miss anything!

Course Title: Marginal and Absorption Costing 1

Learning

Outcomes

Upon^ completion

of^ this^ course,

teacher participants

should^ be^

able^ to:

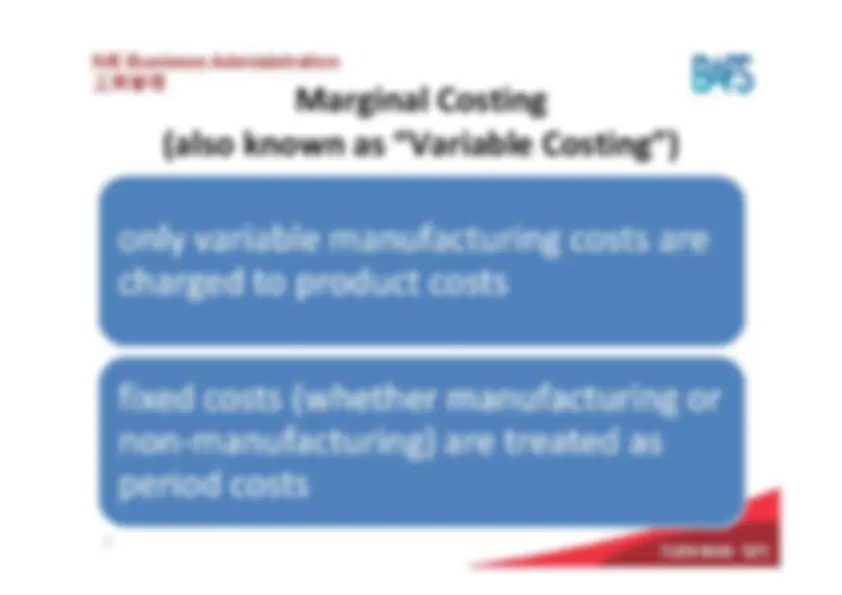

marginal costing^ and

absorption

costing;

present net

profit^ under

marginal

costing^ and

absorption

costing;^ and

uses^ of^ marginal costing^ and

absorption

costing. 2

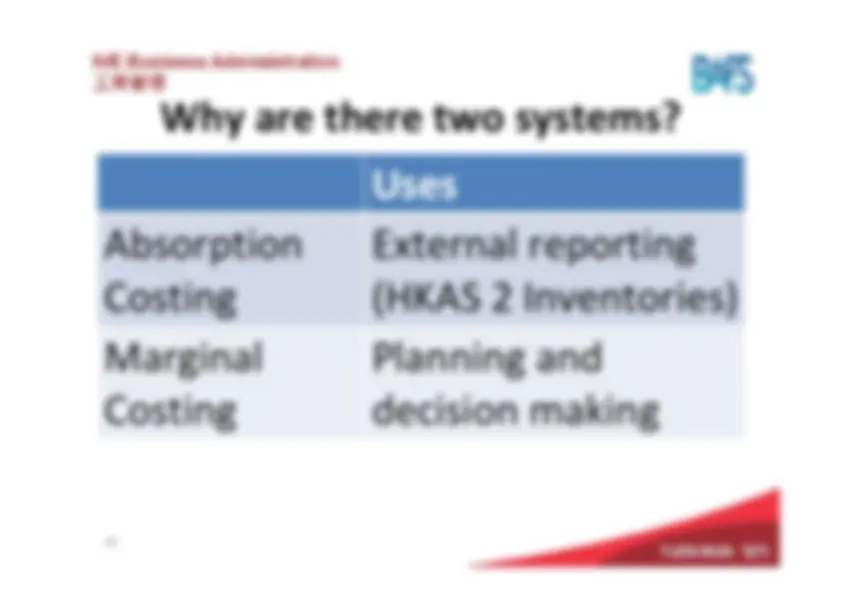

-^ Segregation

of^ cost^ into^ variable

and^ fixed^ elements (Illustration^ 1) • Marginal^ costing

vs.^ absorption

costing^ (Illustrations

2 ‐5)

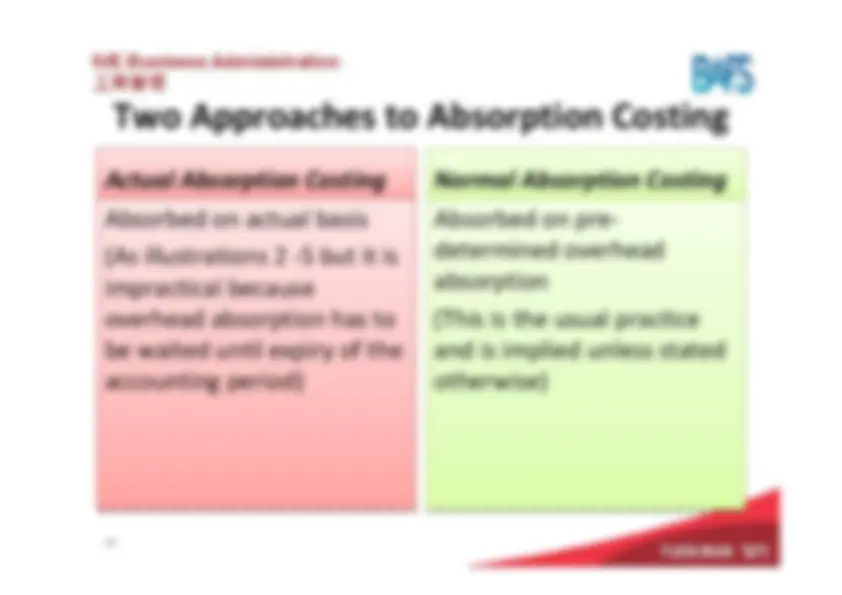

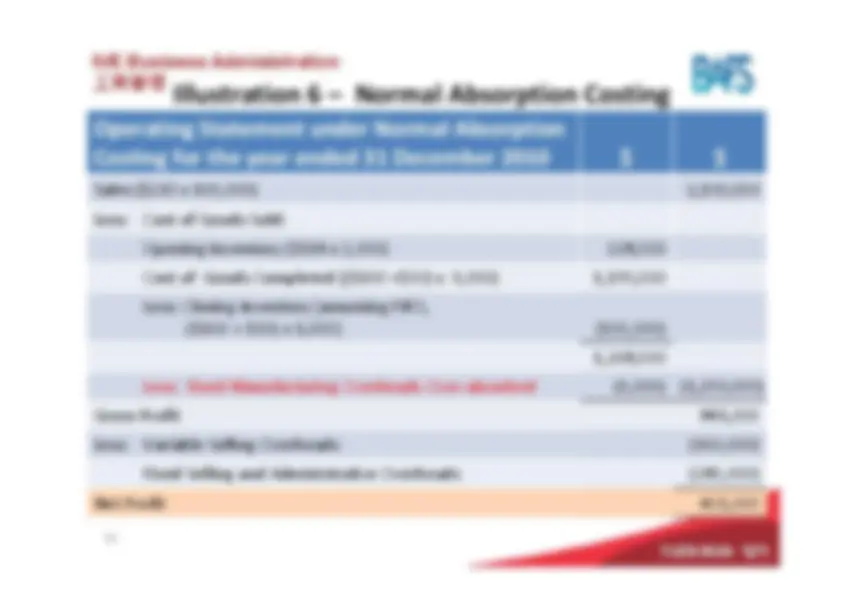

-^ Normal^ absorption

costing^ (Illustration

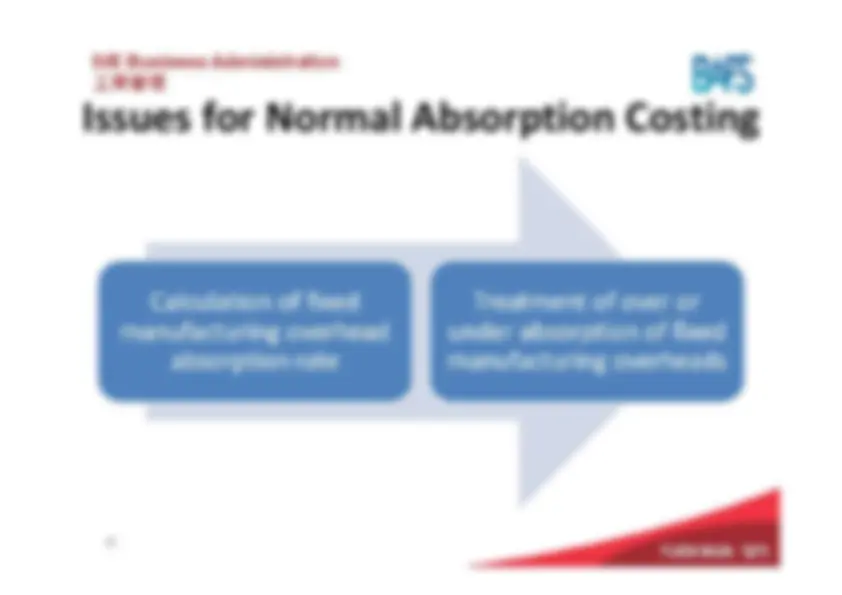

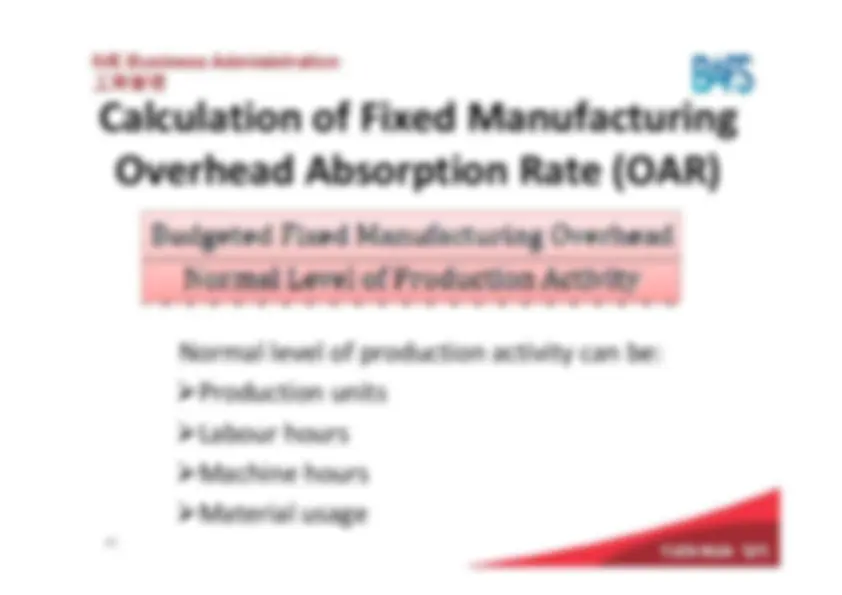

-^ Overhead^ absorption

rate^ (Illustration

-^ Calculation

and^ treatment

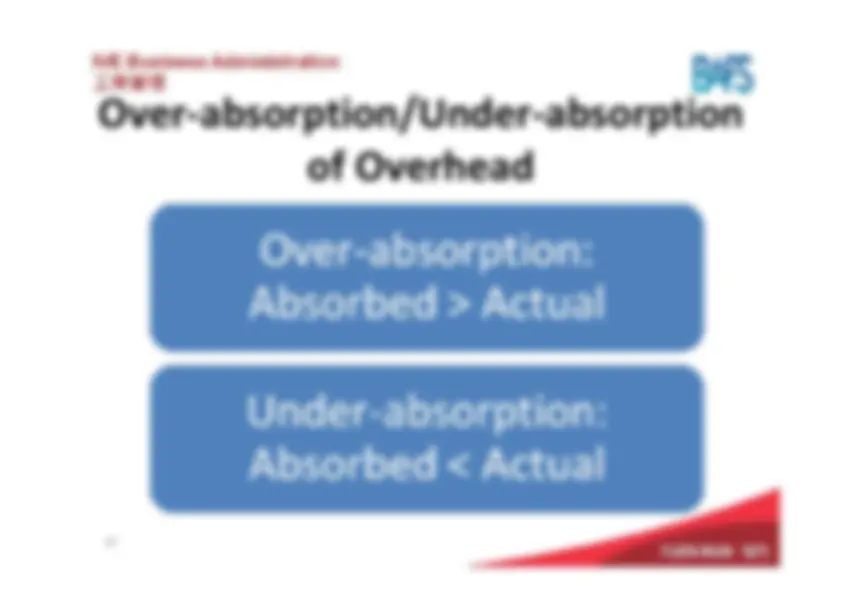

of^ overhead^ over‐ absorbed/under

‐absorbed^ (Illustration

-^ Advantages

and^ disadvantages

of^ marginal^ costing

and

absorption^ costing • Case^ study^ – integrated

illustrative^ question 4

Prior^ Knowledge

Required

5

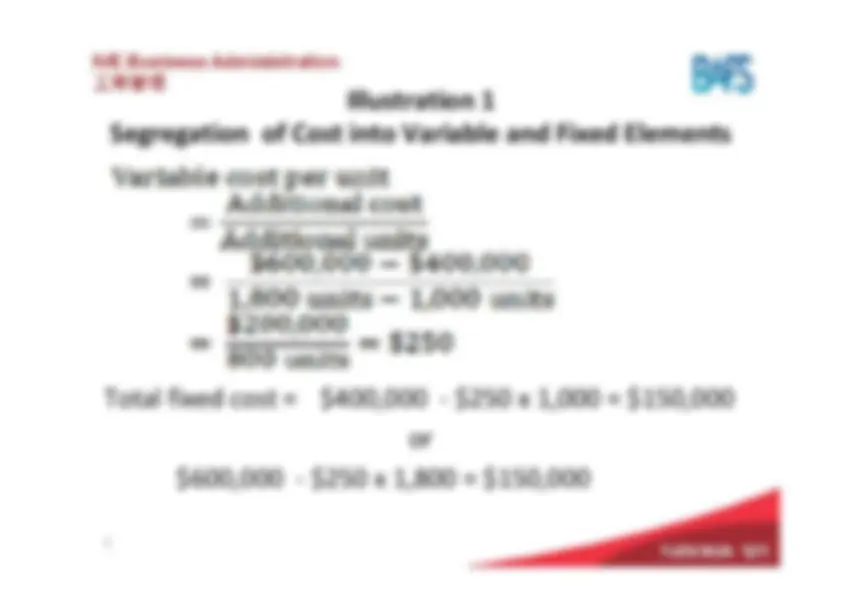

Illustration^1 Segregation^

of^ Cost^ into^ Variable^ and

Fixed^ Elements

The^ manufacturing

cost^ varies

with^ production volumes^ as

follows: Production 7 Volume^

Total^ Manufacturing

Cost

1,000^ units^

$400, 1,800^ units^

$600,

Illustration^1 Segregation^

of^ Cost^ into^ Variable^ and

Fixed^ Elements

Total^ fixed^ cost

=^ $400,

‐^ $250^ x^ 1,

=^ $150, or $600,000^ ‐^ $

x^ 1,800^ =^ $150, 8

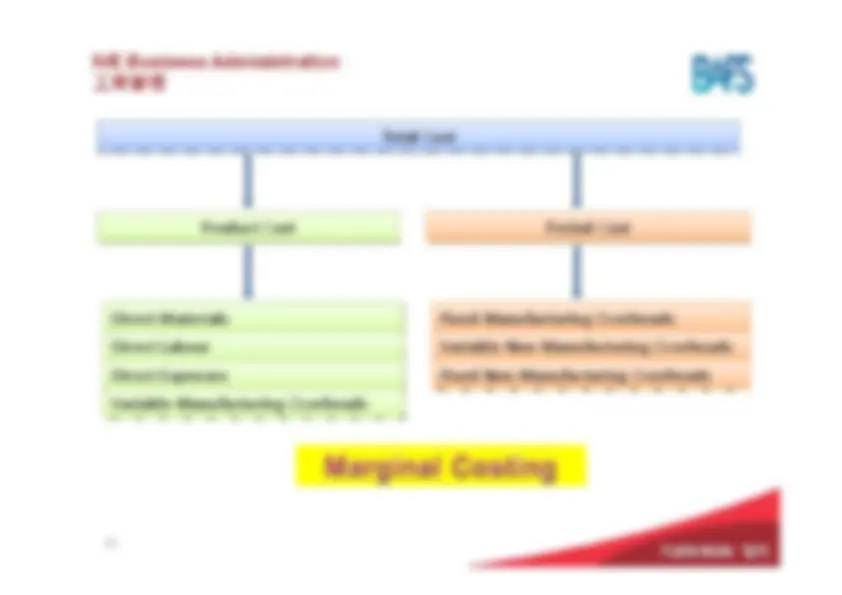

Direct^ MaterialsDirect^ MaterialsDirect^ LabourDirect^ LabourDirect^ ExpensesDirect^ ExpensesVariable^ Manufacturing

Overheads Variable^ Manufacturing

Overheads

Fixed^ Manufacturing

Overheads Fixed^ Manufacturing

Overheads Total^ CostTotal^ Cost Product^ Cost^ Product^ Cost

Period^ CostPeriod^ Cost Variable Non‐Manufacturing^ OverheadsVariable Non‐Manufacturing^ OverheadsFixed Non‐Manufacturing^ OverheadsFixed Non‐Manufacturing^ Overheads

10

11

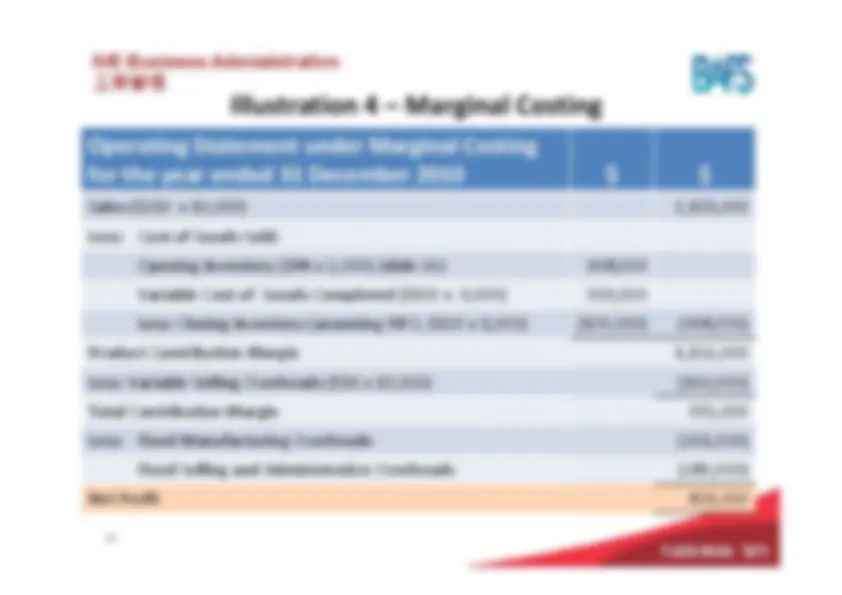

Illustration^2 Marginal^ Costing

vs.^ Absorption

Costing

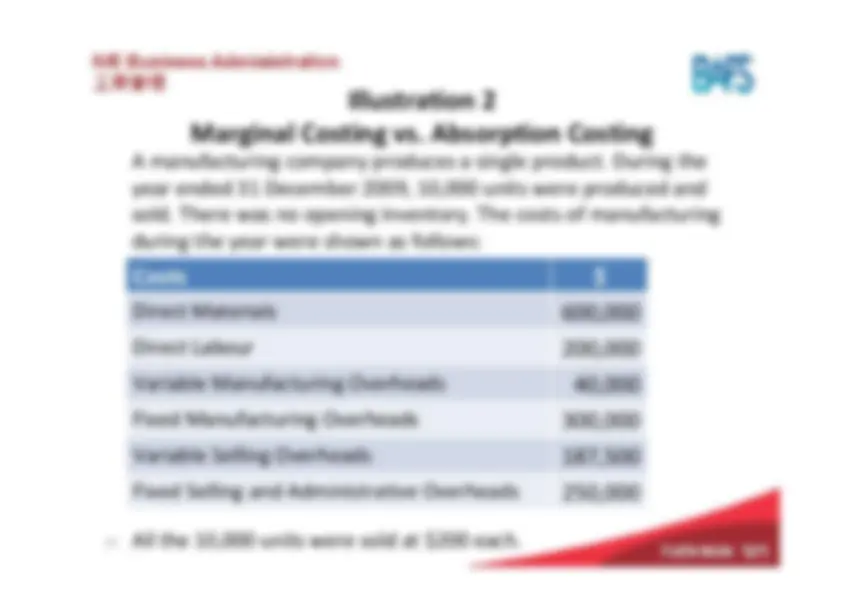

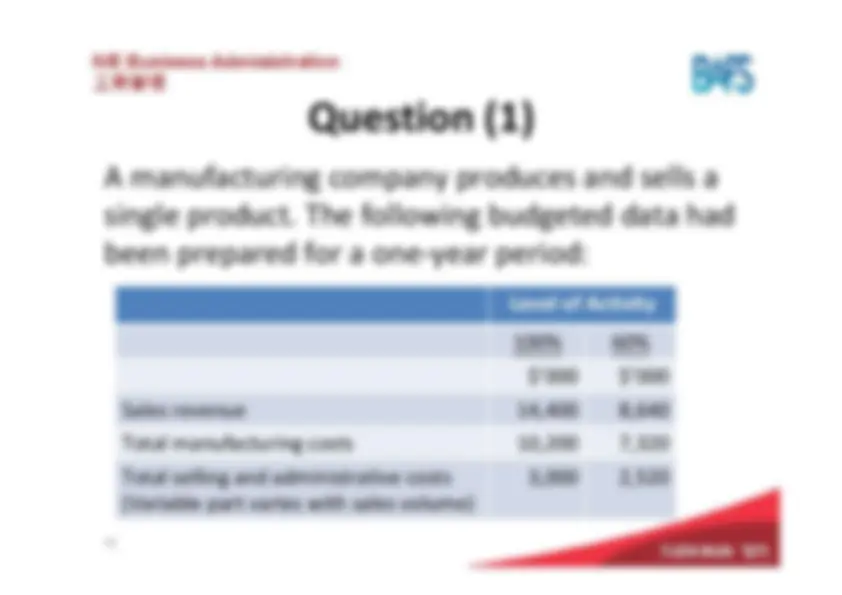

A^ manufacturing

company^ produces

a^ single^ product.

During^ the

year^ ended^31 December

2009,^ 10,000^ units

were^ produced

and

sold.^ There^ was^

no^ opening^ inventory.

The^ costs^ of^ manufacturing during^ the^ year^

were^ shown^ as^ follows: All^ the^ 10,000^ units

were^ sold^ at^ $

each.

Direct^ Materials

Direct^ Labour^

Variable^ Manufacturing

Overheads^

Fixed^ Manufacturing

Overheads^

Variable^ Selling^

Overheads^

Fixed^ Selling^ and

Administrative^

13

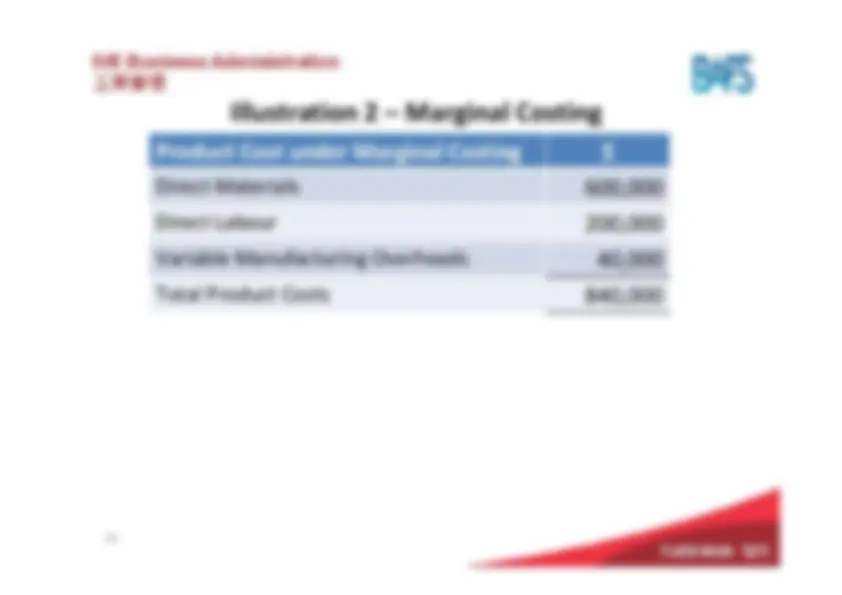

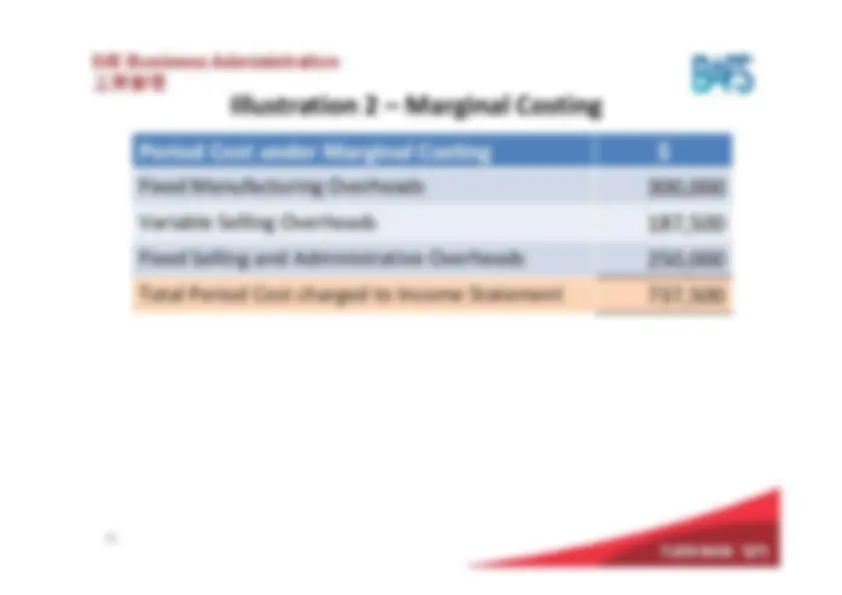

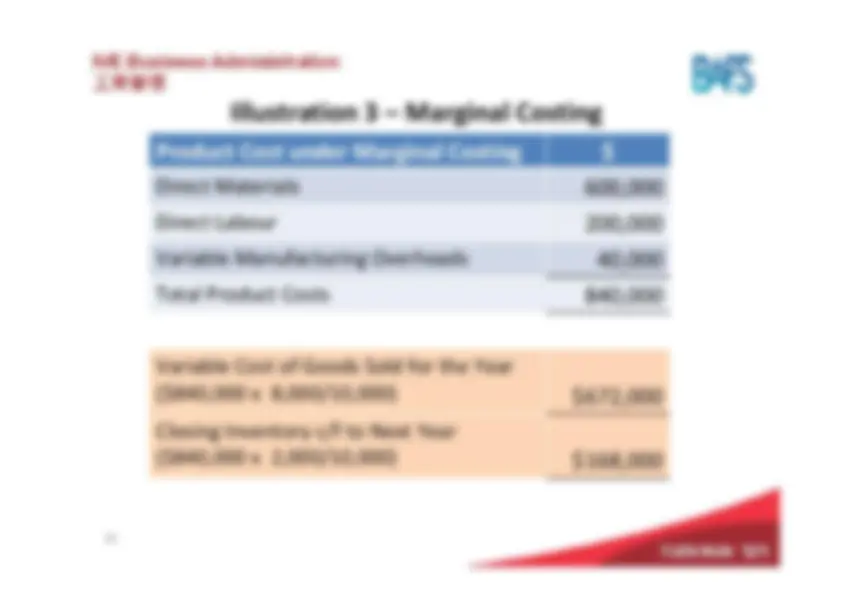

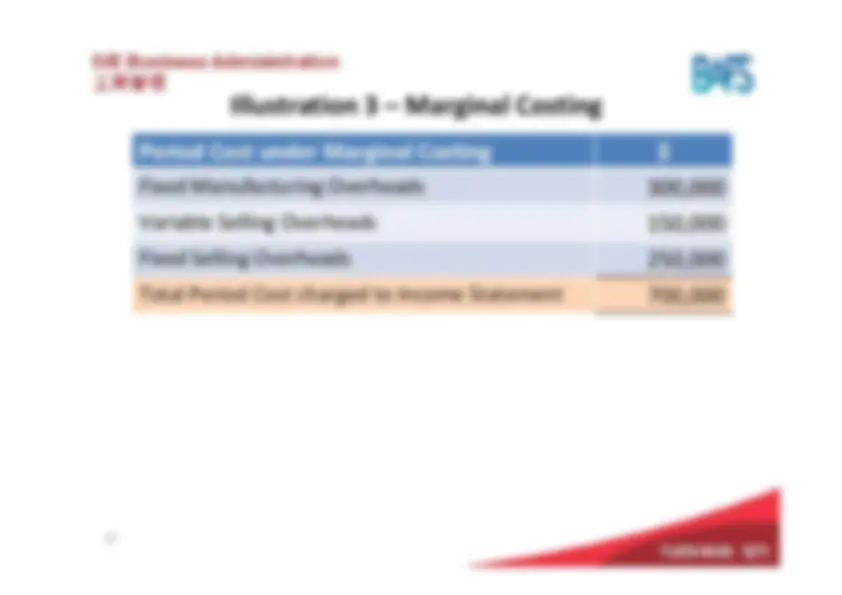

Illustration^2

- Marginal^ Costing

Direct^ Materials

Direct^ Labour^

Variable^ Manufacturing

Overheads^

Total^ Product^ Costs

14

Illustration^2

- Marginal^ Costing

Sales^ (10,000^ units

at^ $200^ each)^

Less:^ Variable^ Cost

of^ Sales^

Product^ Contribution

Margin^

Less:^ Variable^ Selling

Overheads^

Total^ Contribution

Margin^

Less: Fixed^ Manufacturing

Overheads^

Fixed^ Selling^ and

Administrative^

Overheads^

Net^ Profit^

16

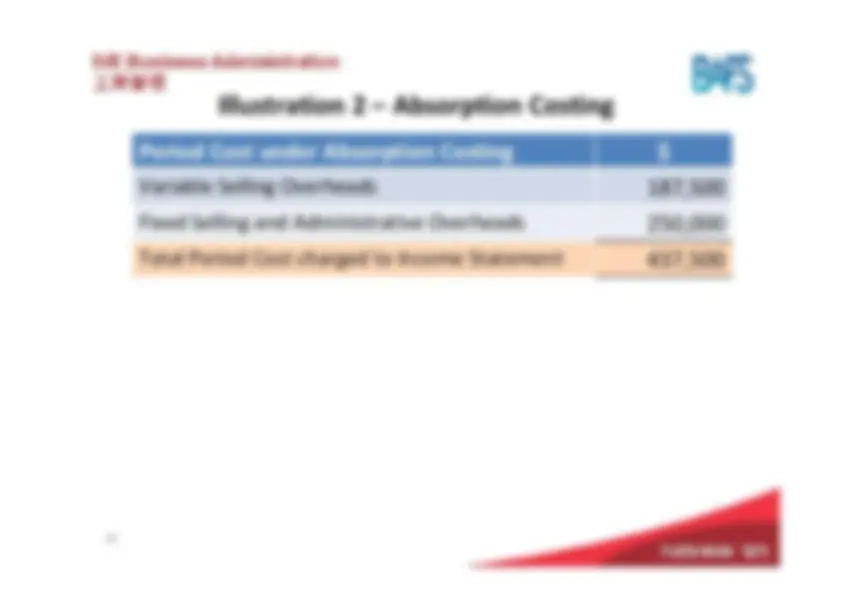

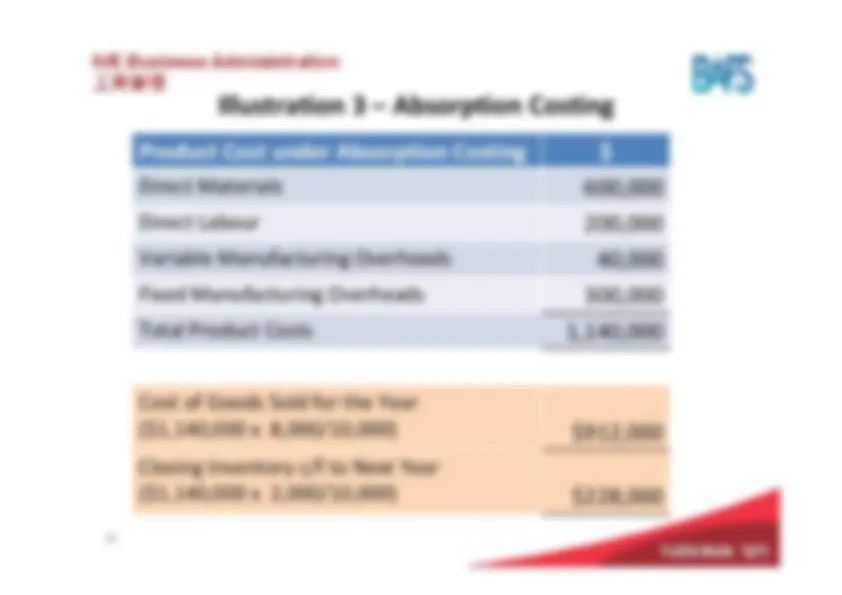

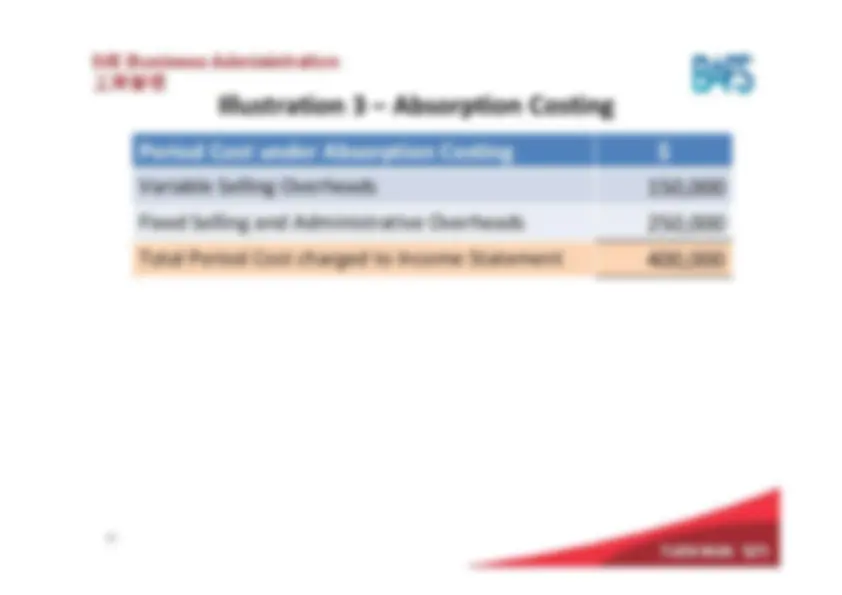

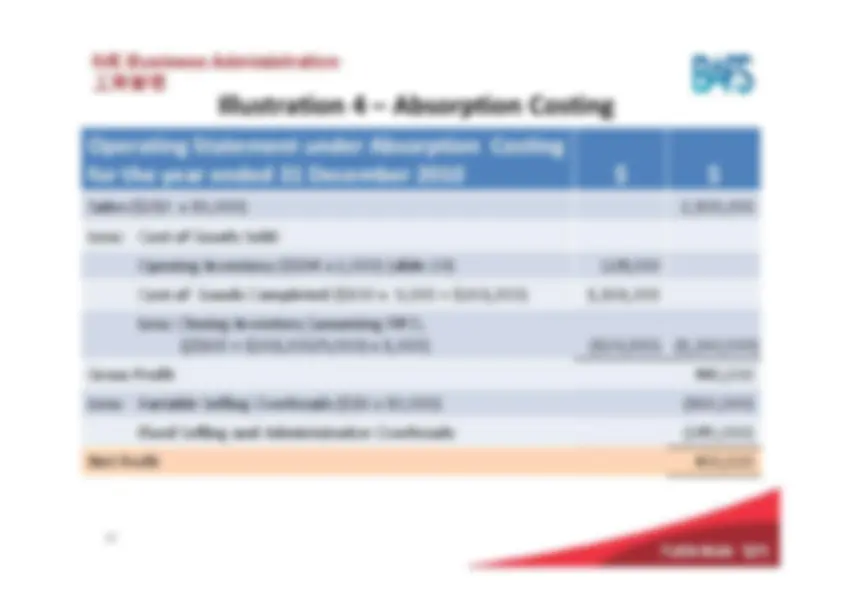

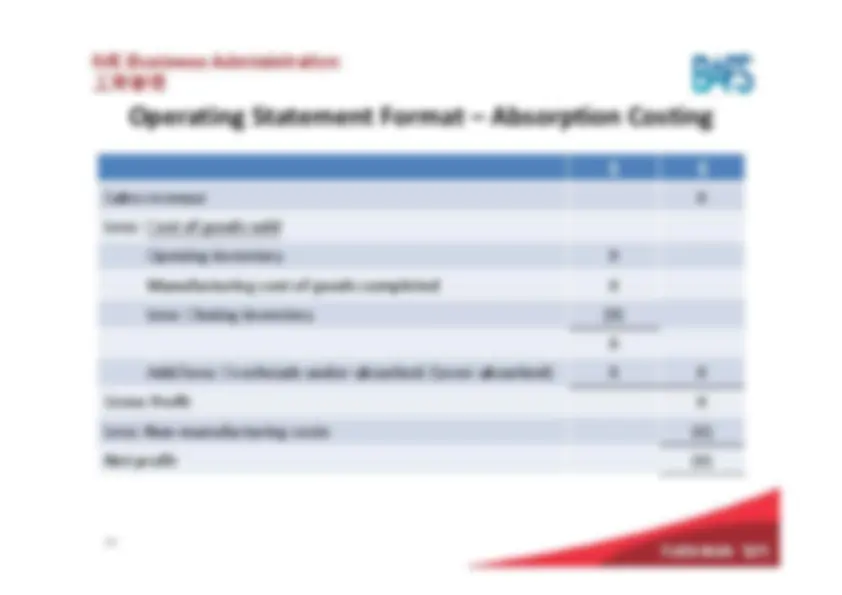

Illustration^2

- Absorption

Costing

Direct^ Materials

Direct^ Labour^

Variable^ Manufacturing

Overheads^

Fixed^ Manufacturing

Overheads^

Total^ Product^ Costs

17

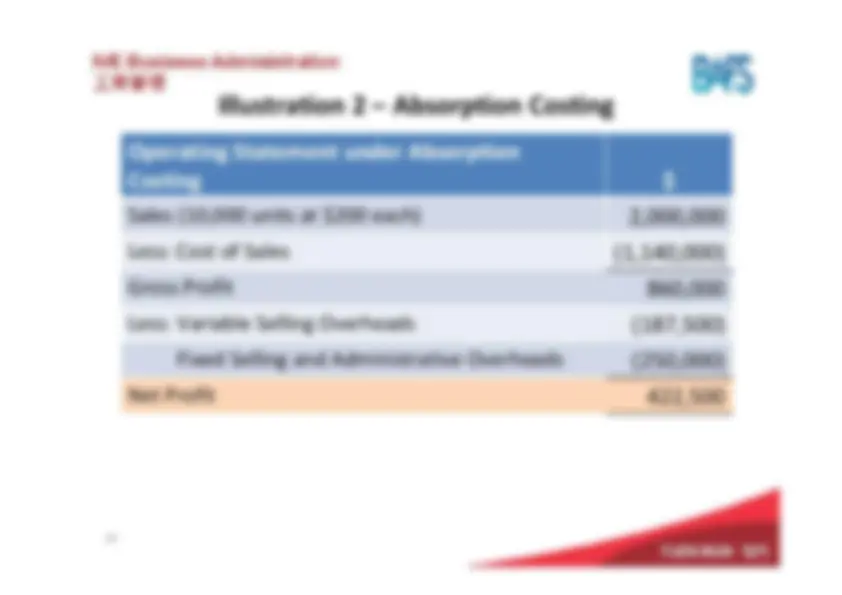

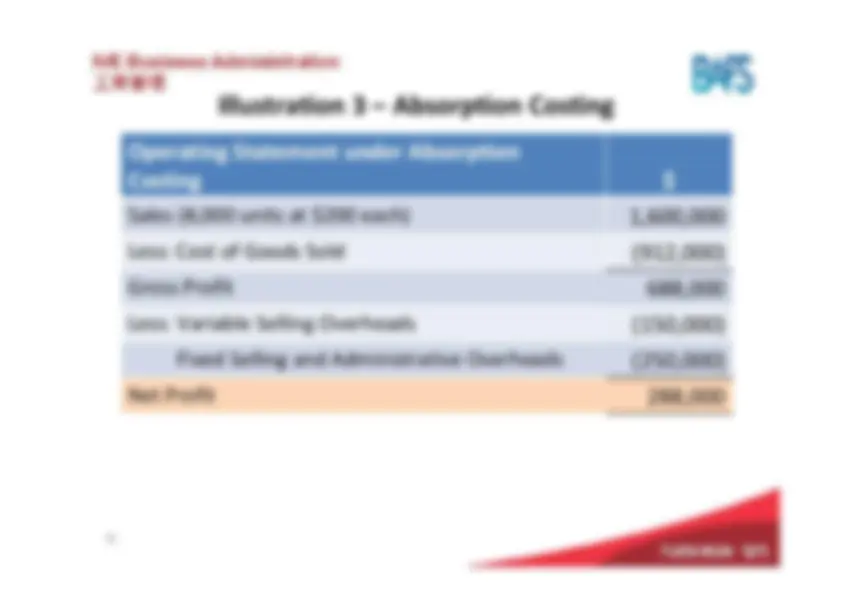

Illustration^2

- Absorption

Costing

Sales^ (10,000^ units

at^ $200^ each)^

Less:^ Cost^ of^ Sales

Gross^ Profit^

Less: Variable^ Selling

Overheads^

Fixed^ Selling^ and

Administrative^

Overheads^

Net^ Profit^

19

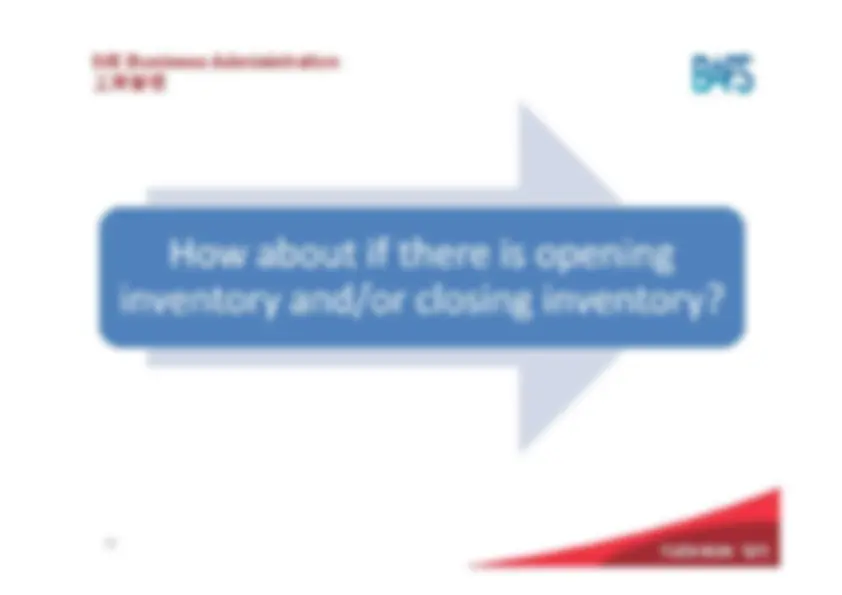

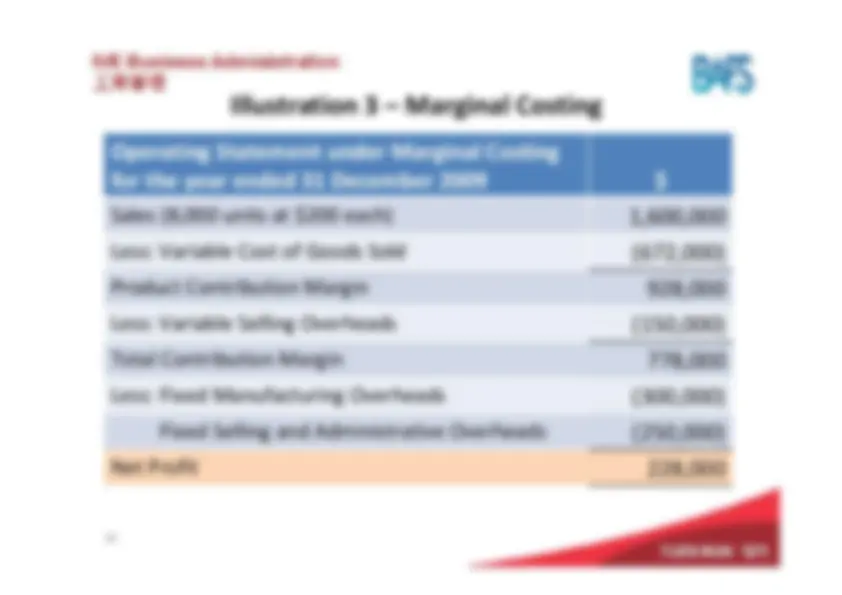

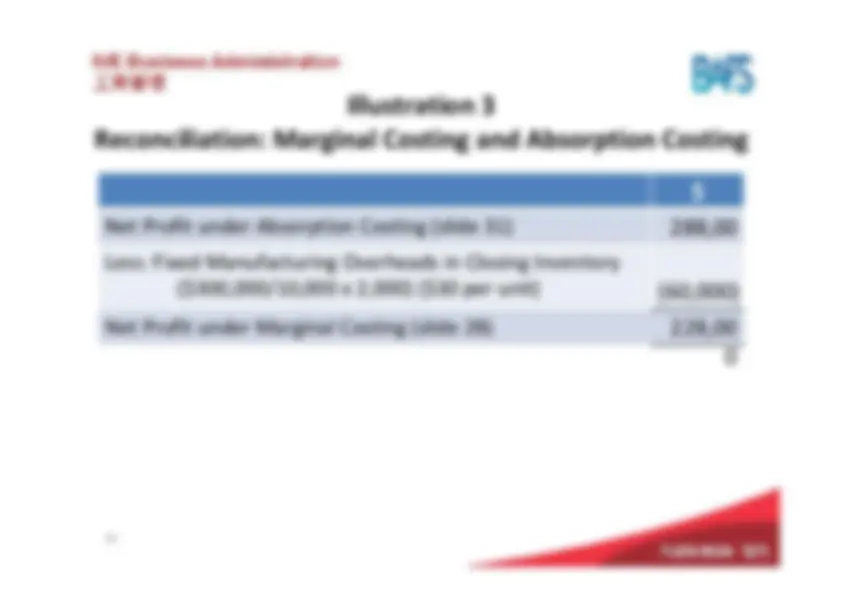

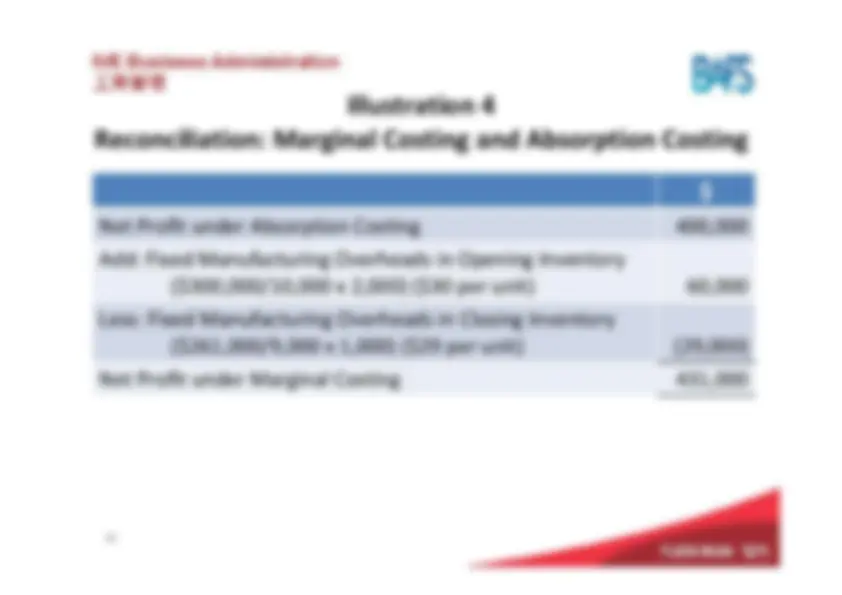

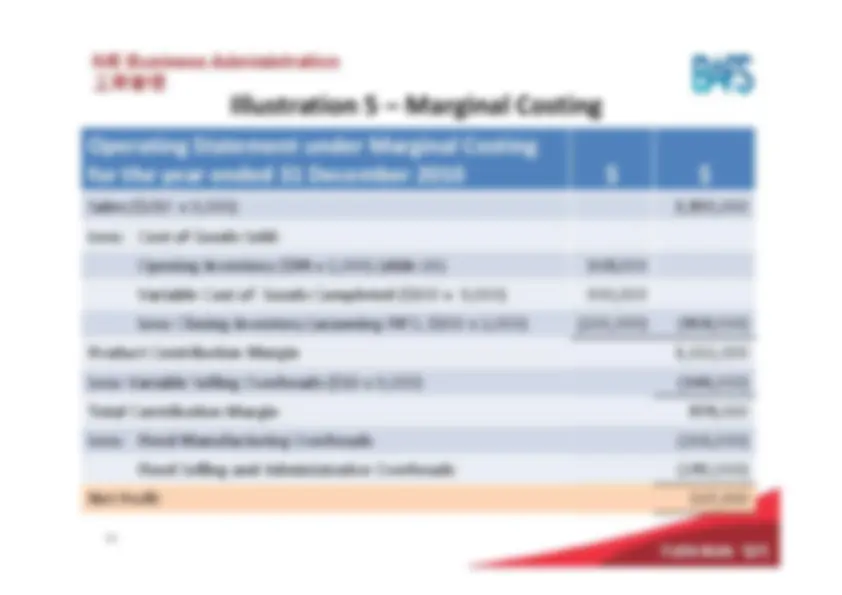

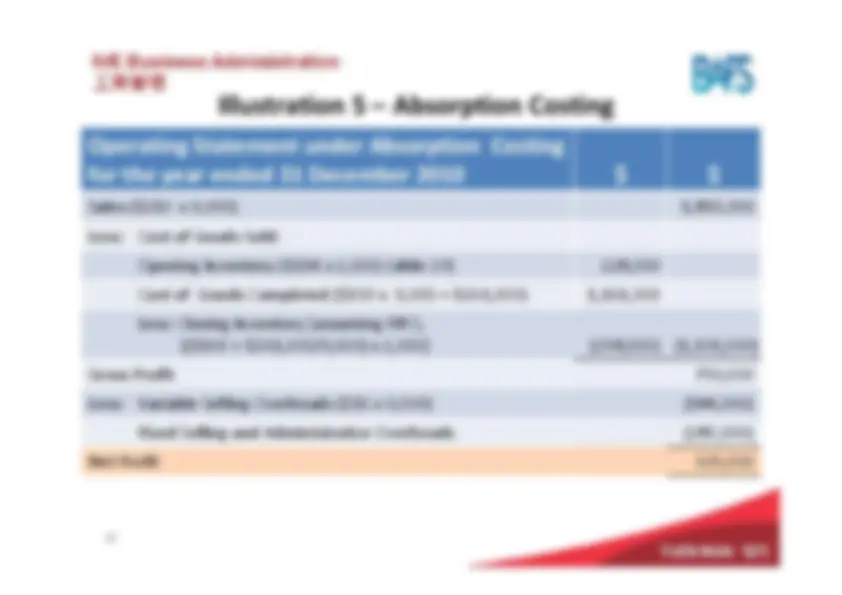

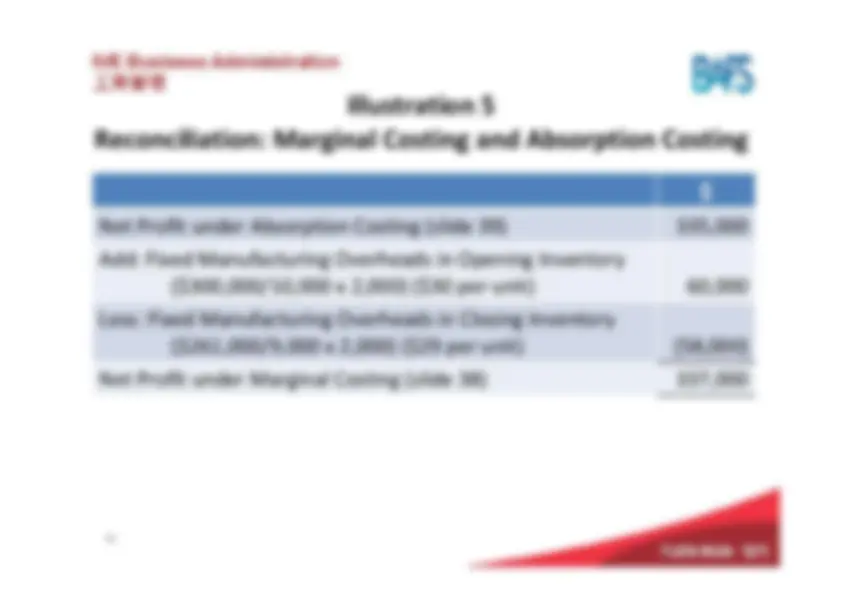

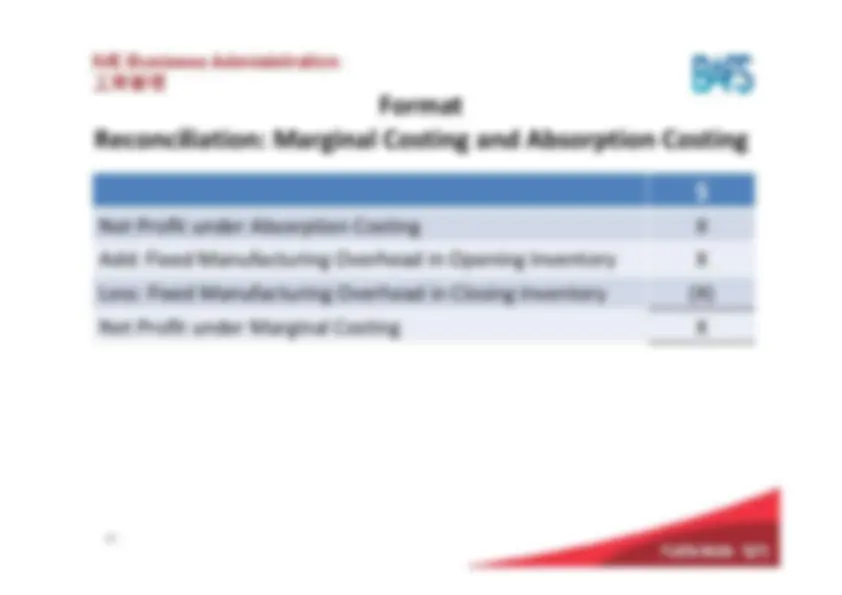

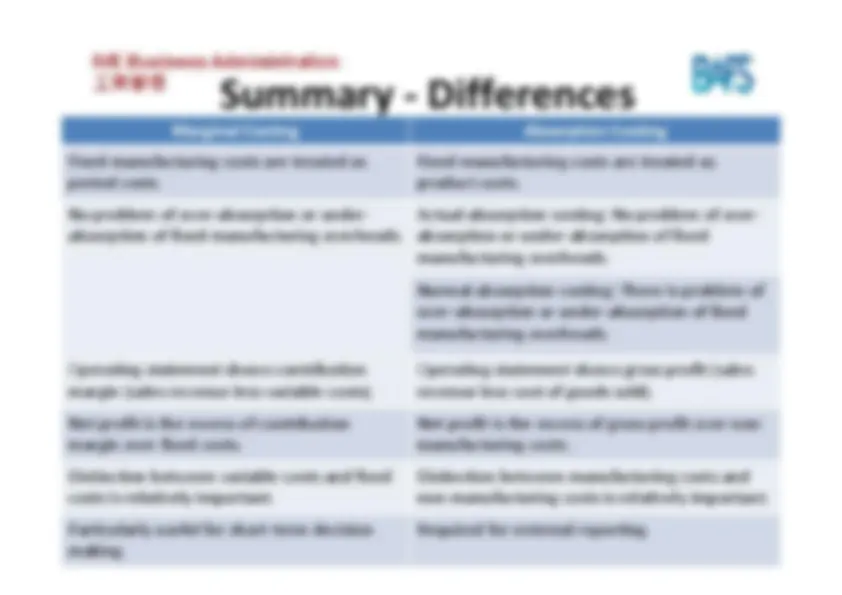

Illustration^2 Marginal^ Costing

and^ Absorption

Costing:^ Implications Hence,^ profits

under^ marginal

costing^ and absorption

costing^ will

be^ the^ same

when

opening^ inventory

and

closing^ inventory. 20