Cost & Management Accouting

MMS-SEM 2

1

Absorption Costing

&

Activity Based Costing

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth analysis of Absorption Costing and Activity-Based Costing, two essential costing methods used in management accounting. Students will learn about the concepts, components, and calculations of both costing methods, including their differences and advantages. The document also includes examples and real-world applications.

Typology: Exercises

1 / 39

This page cannot be seen from the preview

Don't miss anything!

Absorption Costing & Activity Based Costing

NAME ROLL.NO NIKHIL KARNIK 29 KUNAL JAISWAL 21 VIKRANT 45 ASHWINI AGAVNE 02 ANUP NATU 40 NILESH PATIL 42

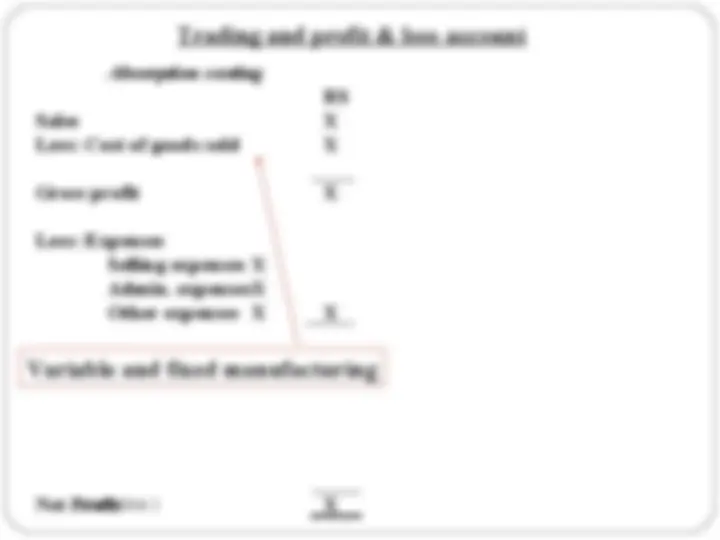

7 MMS-SEM 2 (^) Direct materials :: Those materials that are included in a finished product. (^) Direct labour :: The factory labour costs required to construct a product. (^) Variable manufacturing overhead :: The costs to operate a manufacturing facility, which vary with production volume. Examples are supplies and electricity for production equipment. (^) Fixed manufacturing overhead ::The costs to operate a manufacturing facility, which do not vary with production volume. Examples are rent and insurance.

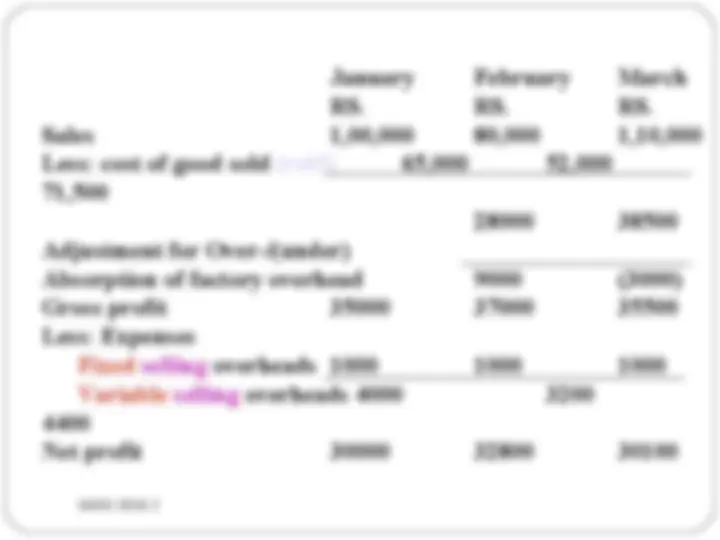

A company started its business in 2014. The following information Was available for January to March 2014 for the company that produ A single product: RS Selling price per unit 100 Direct materials per unit 20 Direct Labor per unit 10 Fixed factory overhead per month 30000 Variable factory overhead per unit 5 Fixed selling overheads 1000 Variable selling overheads per unit 4 Budgeted activity was expected to be 1000 units each month Production and sales for each month were as follows: Jan Feb March Unit sold 1000 800 1100 Unit produced 1000 1300 900

January February March RS. RS. RS. Sales 1,00,000 80,000 1,10, Less: cost of good sold (rs65) 65,000 52, 71, 28000 38500 Adjustment for Over-/(under) Absorption of factory overhead 9000 (3000) Gross profit 35000 37000 35500 Less: Expenses Fixed selling overheads 1000 1000 1000 Variable selling overheads 4000 3200 4400 Net profit 30000 32800 30100

Wk1: Standard fixed overhead rate = Budgeted total fixed factory overheads Budgeted number of units produced = RS. 1000 units = RS.30 units Wk 2: Production cost per unit under absorption costing: RS Direct materials 20 Direct labour 10 Fixed factory overhead absorbed 30 Variable factory overheads 5 65

(^) Assign costs to cost pools : This is comprised of a standard set of accounts that are always included in cost pools, and which should rarely be changed. (^) Calculate usage: Determine the amount of usage of whatever activity measure is used to assign overhead costs, such as machine hours or direct labour hours used. (^) Assign costs : Divide the usage measure into the total costs in the cost pools to arrive at the allocation rate per unit of activity, and assign overhead costs to produced goods based on this usage rate.

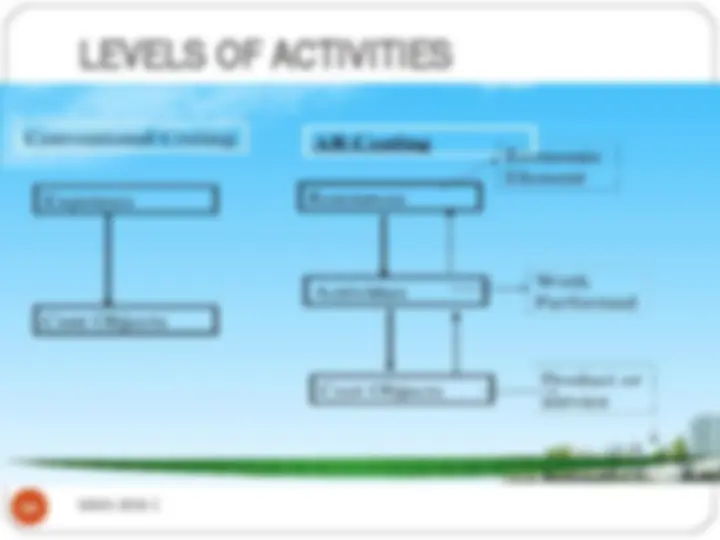

Fixed manufacturing overheads are treated as product costing. It is believed that products cannot be produced without the resources provided by fixed manufacturing overheads.

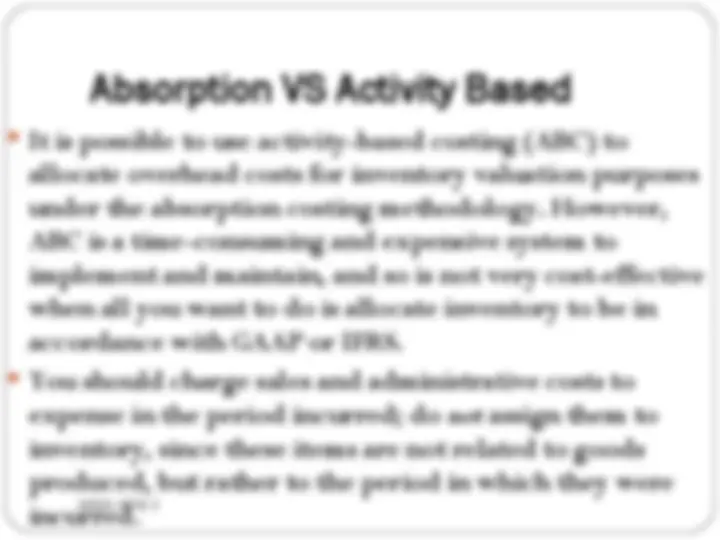

19 MMS-SEM 2 (^) It is possible to use activity-based costing (ABC) to allocate overhead costs for inventory valuation purposes under the absorption costing methodology. However, ABC is a time-consuming and expensive system to implement and maintain, and so is not very cost-effective when all you want to do is allocate inventory to be in accordance with GAAP or IFRS. (^) You should charge sales and administrative costs to expense in the period incurred; do not assign them to inventory, since these items are not related to goods produced, but rather to the period in which they were incurred.