Download Coverdrive Ltd: Maximizing Profit with Limiting Factor & Marginal Cost and more Lecture notes Decision Making in PDF only on Docsity!

Decision Making and the Limiting Factor

This third in the series of case studies focusing on Coverdrive Ltd involves the use of decision making techniques based on the limiting factor and the marginal cost model. Coverdrive Ltd is a SME producing cricket bats. It is generally accepted that businesses have one or more limiting factors or, as Professor John Sizer states “a factor in the activities of an undertaking which at a particular point in time or over a period will limit the volume of output”.

Within the planning stage of the budgetary cycle it will be apparent that there will be a factor or factors which will limit the organisational activities. This is often referred to as the key factor or principal budget factor, and its effects on the organisational plans must be fully assessed.

Such factors are often referred to as scarce resources which limit volume and may include:

supply of skilled labour supply of materials factory space finance – working capital availability plant capacity market demand

It is often the case that a business may face a single constraint situation, however, others may experience a multi-constraint scenario. Budgetary plans are usually set some months prior to the period to which they relate. Circumstances alter and situations often arise where limits are placed on a resource or series of resources after the plans have been formulated. Where resources can limit capacity, in the short run, a business must decide on the product mix which will secure maximum contribution (and therefore maximum profit).

This is the decision making process faced by the finance team in which the marginal cost model often features.

The Decision Making Cycle

The following diagram illustrates the decision making cycle:

identify objectives

identify alternative courses of action

obtain information about alternatives

select one of the alternatives

implement the decision

compare actual results

Standard price per unit of material £

Production Overheads

Variable £31000 (absorbed on basis of labour hours) Fixed £

Other fixed overheads £

Early in the first week of the budget period March 2010, a machine in the primary preparation area, suffers a major breakdown and a replacement part from an overseas supplier and will not be available until the month end.

This will effect operating hours adversely by 10% in the budget period.

It will however not effect the employees’ basic working week as the original plan for the month included some overtime working.

The capacity in direct labour hours required to produce the original plan was:

Products “Special” “Super” “Classic” Total

Standard hours per unit 4.0 3.5 3

Production and sales 1200 1150 1200

Standard direct labour hours 4800 4025 3600 12425

The limiting factor is direct labour hours and there will a shortfall of 1242.5 standard labour hours.

The business must therefore make a short-term decision, which will result in the most favourable course of action to minimise the effect of this shortfall in capacity.

The business needs to revise its budget and product mix, so that in the short run, it can secure maximum profit.

The decision making process involves the following steps:

determine the contribution per unit of output/product determine the contribution per limiting factor – the labour hour rank the products per the contribution per limiting factor, to consider the alternatives revise the production and sales mix revise the budget

Firstly let us consider the original plan.

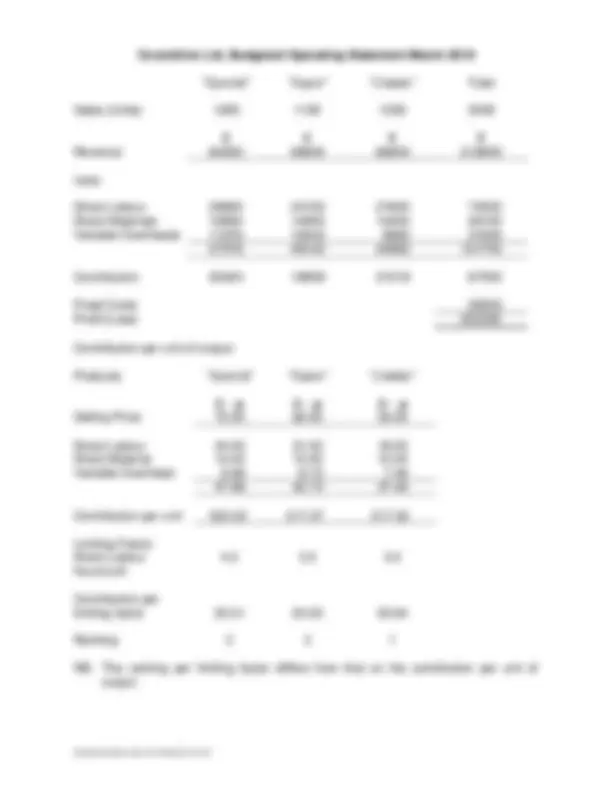

Coverdrive Ltd, Budgeted Operating Statement March 2010

“Special” “Super” “Classic” Total

Sales (Units) 1200 1150 1200 3550

£ £ £ £ Revenue 84000 69000 66000 219000

Less:

Direct Labour 28800 24150 21600 74550 Direct Materials 16800 14950 14400 46150 Variable Overheads 11976 10042 8982 31000 57576 49142 44982 151700

Contribution 26424 19858 21018 67300

Fixed Costs 35000 Profit/(Loss) £

Contribution per unit of output:

Products “Special” “Super” “Classic”

£ - p £ - p £ - p Selling Price 70.00 60.00 55.

Direct Labour 24.00 21.00 18. Direct Material 14.00 13.00 12. Variable Overhead 9.98 8.73 7. 47.98 42.73 37.

Contribution per unit £22.02 £17.27 £17.

Limiting Factor Direct Labour 4.0 3.5 3. hours/unit

Contribution per limiting factor £5.51 £4.93 £5.

Ranking 2 3 1

NB: The ranking per limiting factor differs from that on the contribution per unit of output.

Conclusion

The revised production and sales mix is viewed only from a financial perspective. The business may decide to consider alternative strategies to avoid loss of customer satisfaction in not being able to meet the demand for “super”. They may in the short run be able to buy in a substitute or contract out the work. However they may decide to spread the shortfall across all products to minimise the adverse effect on the customer perspective.