Download Optimal Debt Structure: Project vs. Firm-wide Financing for Disney Theme Park and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

II. Project Specific Financing

115

¨ With project specific financing, you match the

financing choices to the project being funded. The

benefit is that the the debt is truly customized to the

project.

¨ Project specific financing makes the most sense

when you have a few large, independent projects to

be financed. It becomes both impracGcal and costly

when firms have porfolios of projects with

interdependent cashflows.

DuraGon of Disney Theme Park

116

Duration of the Project = 58,375/2,877 = 20.29 years

III. Firm-‐wide financing

118

¨ Rather than look at individual projects, you could consider the firm to be a porfolio of projects. The firm’s past history should then provide clues as to what type of debt makes the most sense.

¨ OperaGng Cash Flows

n The quesGon of how sensiGve a firm’s asset cash flows are to a variety of factors, such as interest rates, inflaGon, currency rates and the economy, can be directly tested by regressing changes in the operaGng income against changes in these variables. n This analysis is useful in determining the coupon/interest payment structure of the debt.

¨ Firm Value

n The firm value is clearly a funcGon of the level of operaGng income, but it also incorporates other factors such as expected growth & cost of capital. n The firm value analysis is useful in determining the overall structure of the debt, parGcularly maturity.

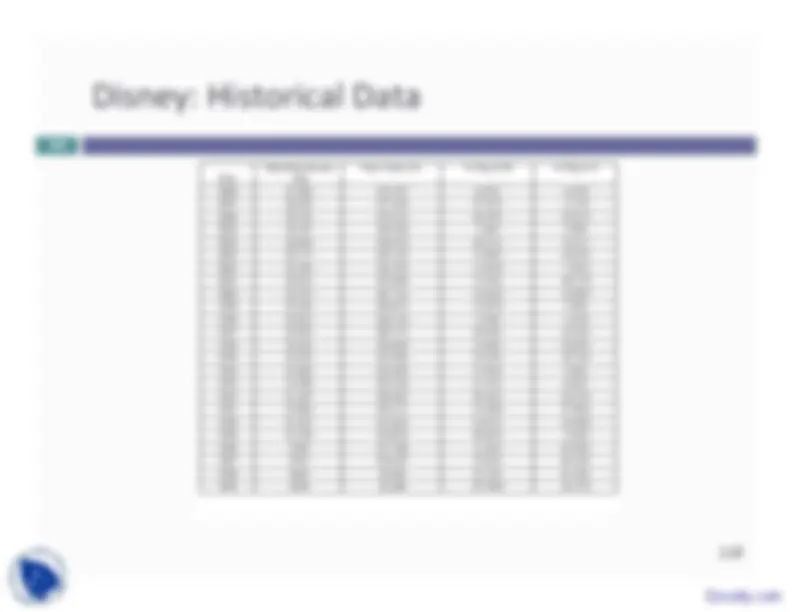

Disney: Historical Data

119

I. SensiGvity to Interest Rate Changes

121

¨ How sensiGve is the firm’s value and operaGng

income to changes in the level of interest rates?

¨ The answer to this quesGon is important because it

¤ it provides a measure of the duraGon of the firm’s projects

¤ it provides insight into whether the firm should be using

fixed or floaGng rate debt.

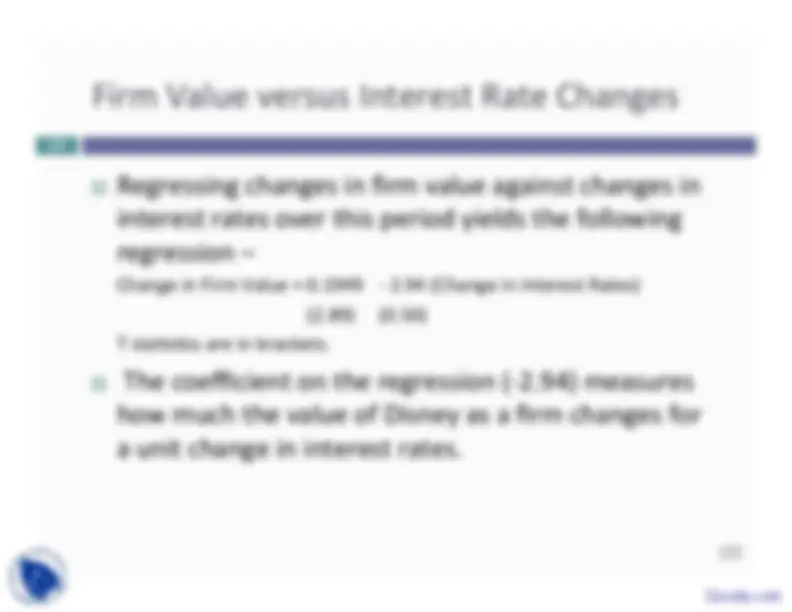

Firm Value versus Interest Rate Changes

122

¨ Regressing changes in firm value against changes in

interest rates over this period yields the following

regression –

Change in Firm Value = 0.1949 -‐ 2.94 (Change in Interest Rates) (2.89) (0.50) T staGsGcs are in brackets.

¨ The coefficient on the regression (-‐2.94) measures

how much the value of Disney as a firm changes for

a unit change in interest rates.

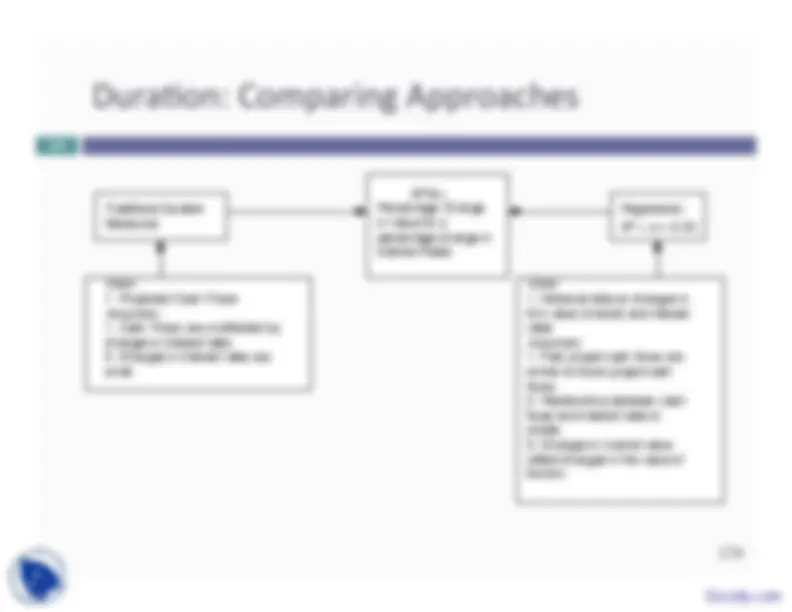

DuraGon: Comparing Approaches

124

δP/δr= Percentage Change in Value for a percentage change in Interest Rates

Traditional Duration Measures

Regression: δP = a + b (δr)

Uses:

- Projected Cash Flows Assumes:

- Cash Flows are unaffected by changes in interest rates

- Changes in interest rates are small.

Uses:

- Historical data on changes in firm value (market) and interest rates Assumes:

- Past project cash flows are similar to future project cash flows.

- Relationship between cash flows and interest rates is stable.

- Changes in market value reflect changes in the value of the firm.

OperaGng Income versus Interest Rates

125

¨ Regressing changes in operaGng cash flow against

changes in interest rates over this period yields the

following regression –

Change in OperaGng Income = 0.1958 + 6.59 (Change in Interest Rates) (2.74) (1.06)

Conclusion: Disney’s operaGng income, unlike its

firm value, has moved with interest rates.

¨ Generally speaking, the operaGng cash flows are

smoothed out more than the value and hence will

exhibit lower duraGon that the firm value.