Download Capital Structure Decision at Disney: Cost of Capital and Debt Ratio and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

Disney: Cost of Capital Chart: 1997

52

10.50%!

11.00%!

11.50%!

12.00%!

12.50%!

13.00%!

13.50%!

14.00%!

0.00%

!

10.00%

!

20.00%

!

30.00%

!

40.00%

!

50.00%

!

60.00%

!

70.00%

!

80.00%

!

90.00%

!

Cost of Capital

!

Debt Ratio!

Note the kink

in the cost of

capital graph

at 60% debt.

What is

causing it?

The cost of capital approach suggests that

Disney should do the following…

53

¨ Disney currently has $16.68 billion in debt. The opNmal

dollar debt (at 40%) is roughly $24.75 billion. Disney has

excess debt capacity of $ 8.07 billion.

¨ To move to its opNmal and gain the increase in value,

Disney should borrow $ 8 billion and buy back stock.

¨ Given the magnitude of this decision, you should expect

to answer three quesNons:

1. Why should we do it?

2. What if something goes wrong?

3. What if we don’t want (or cannot ) buy back stock and want

to make investments with the addiNonal debt capacity?

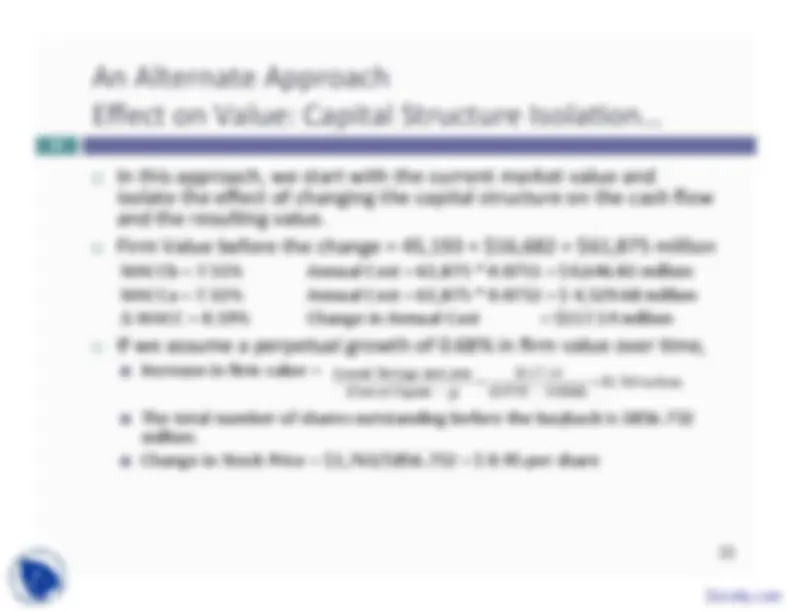

An Alternate Approach

Effect on Value: Capital Structure IsolaNon…

55

¨ In this approach, we start with the current market value and

isolate the effect of changing the capital structure on the cash flow

and the resulNng value.

¨ Firm Value before the change = 45,193 + $16,682 = $61,875 million

WACCb = 7.51% Annual Cost = 61,875 * 0.0751 = $4,646.82 million WACCa = 7.32% Annual Cost = 61,875 * 0.0732 = $ 4,529.68 million Δ WACC = 0.19% Change in Annual Cost = $117.14 million

¨ If we assume a perpetual growth of 0.68% in firm value over Nme,

¤ Increase in firm value =

¤ The total number of shares outstanding before the buyback is 1856. million. ¤ Change in Stock Price = $1,763/1856.732 = $ 0.95 per share

€

Annual Savings next year (Cost of Capital - g) =^

$117. (0.0732 - 0.0068) =^ $1,763 million

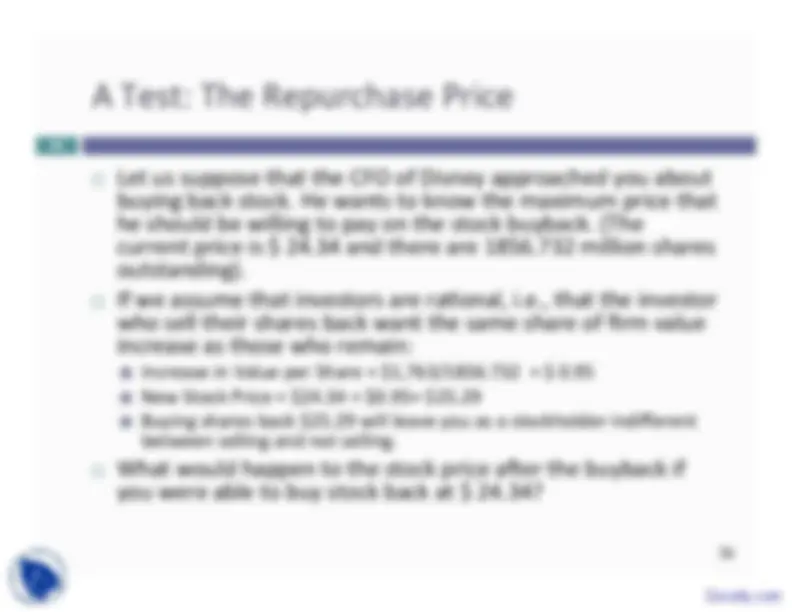

A Test: The Repurchase Price

56

¨ Let us suppose that the CFO of Disney approached you about

buying back stock. He wants to know the maximum price that

he should be willing to pay on the stock buyback. (The

current price is $ 24.34 and there are 1856.732 million shares

outstanding).

¨ If we assume that investors are raNonal, i.e., that the investor

who sell their shares back want the same share of firm value

increase as those who remain:

¤ Increase in Value per Share = $1,763/1856.732 = $ 0. ¤ New Stock Price = $24.34 + $0.95= $25. ¤ Buying shares back $25.29 will leave you as a stockholder indifferent between selling and not selling.

¨ What would happen to the stock price a_er the buyback if

you were able to buy stock back at $ 24.34?

2. What if something goes wrong?

The Downside Risk

58

¨ SensiNvity to AssumpNons

A. “What if” analysis The opNmal debt raNo is a funcNon of our inputs on operaNng income, tax rates and macro variables. We could focus on one or two key variables – operaNng income is an obvious choice – and look at history for guidance on volaNlity in that number and ask what if quesNons. B. “Economic Scenario” Approach We can develop possible scenarios, based upon macro variables, and examine the opNmal debt raNo under each one. For instance, we could look at the opNmal debt raNo for a cyclical firm under a boom economy, a regular economy and an economy in recession.

¨ Constraint on Bond RaNngs/ Book Debt RaNos

AlternaNvely, we can put constraints on the opNmal debt raNo to reduce exposure to downside risk. Thus, we could require the firm to have a minimum raNng, at the opNmal debt raNo or to have a book debt raNo that is less than a “specified” value.

Explore the past:

Disney’s OperaNng Income History

59

Key questions : What does a bad year look like for Disney? How much volatility is there in operating income?

Recession Decline in Operating Income 2008-09 Drop of about 10% 2002 Drop of 15.82% 1991 Drop of 22.00% 1981-82 Increased

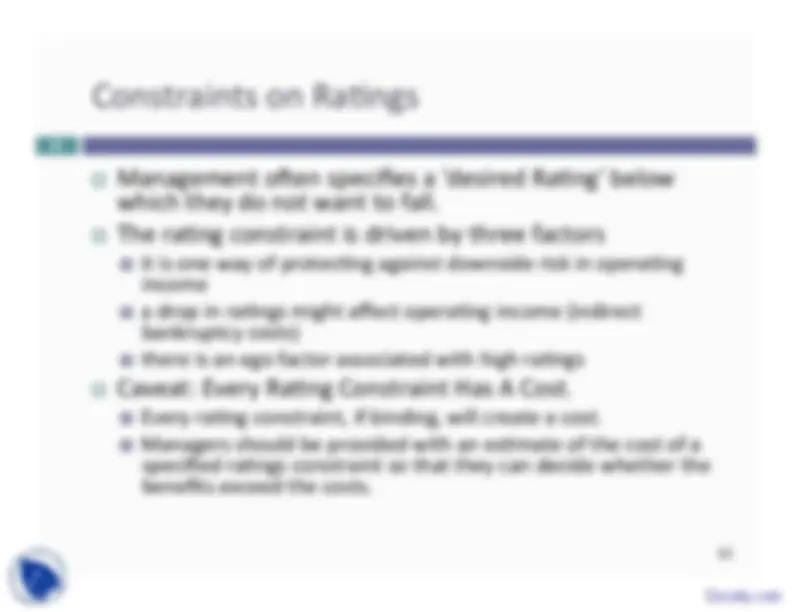

Constraints on RaNngs

61

¨ Management o_en specifies a 'desired RaNng' below

which they do not want to fall.

¨ The raNng constraint is driven by three factors

¤ it is one way of protecNng against downside risk in operaNng

income

¤ a drop in raNngs might affect operaNng income (indirect

bankruptcy costs)

¤ there is an ego factor associated with high raNngs

¨ Caveat: Every RaNng Constraint Has A Cost.

¤ Every raNng constraint, if binding, will create a cost.

¤ Managers should be provided with an esNmate of the cost of a

specified raNngs constraint so that they can decide whether the

benefits exceed the costs.