Download Engineering Financial and Cost Analysis - Lecture - RefinementsofTransactions and more Lecture notes Financial Management in PDF only on Docsity!

Engineering and Financial Cost Analysis

Refinements of Accounting

Transactions

Prepaids (also called Deferrals)

Cash flows occur BEFORE the revenue or

expense is recognized

Revenues

Unearned Revenues

Unearned Rent

Deferred Income

Expenses

Prepaid Insurance

Prepaid rent

Prepaid taxes

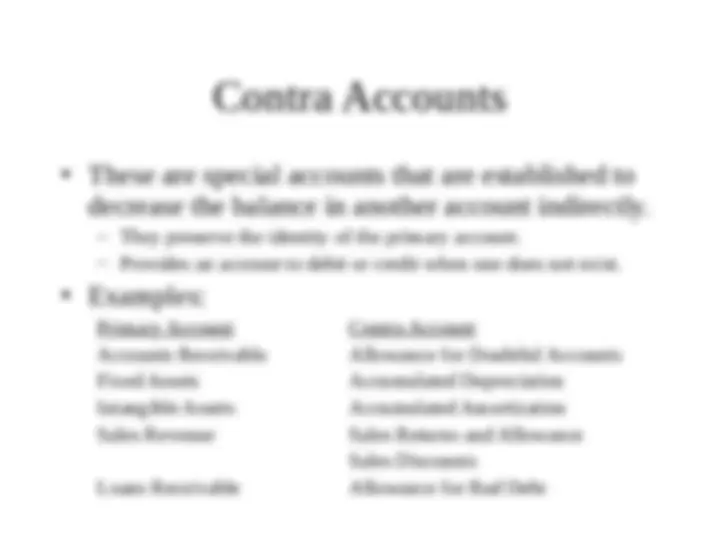

Contra Accounts

• These are special accounts that are established to

decrease the balance in another account indirectly.

- (^) They preserve the identity of the primary account.

- (^) Provides an account to debit or credit when one does not exist.

• Examples:

Primary Account Contra Account Accounts Receivable Allowance for Doubtful Accounts Fixed Assets Accumulated Depreciation Intangible Assets Accumulated Amortization Sales Revenue Sales Returns and Allowance Sales Discounts Loans Receivable Allowance for Bad Debt

Accounting for Allowance Accounts

- (^) Allowance accounts ensure the amount report in the primary

account is as accurate as possible.

- (^) These require estimates

- (^) Example: Allowance for Bad Debt

- (^) This contra-account to Accounts Receivable acknowledges that, with every credit sale, a portion will not be collected. - (^) With a credit sale of $1000 and an estimate of 6.5% bad debt and COGS = $ - (^) When it is clear that a customer will never pay $30 that is owed the Company will record the following entries.

- (^) Now the Expense (Bad Debt) has offset the Sales Revenue in the same period they were earned. Allowance for Bad Debt $ Accounts Receivable $ Allowance for Bad Debt $ Bad Debt Expense $ COGS $ Inventory $ Sales Revenue $ Accounts Receivable $

Calculating the Interest

- (^) Accounts Payable is considered non-interest borrowing but in reality this is only true if the Prompt Payment Discount is taken.

- (^) By not paying within the first 10 days, the customer is essentially borrowing money (the discounted amount) and paying 2 percent interest.

- (^) Calculating the Interest:

- (^) The interest rate is based on 2 percent interest for 20 days of borrowing.

- (^) There are 18 1/4 of these 20 day periods in a year (365/20 = 18 1/4).

- (^) Therefore, the yearly Interest Rate is 36.5% (2% x 18 1/4).

- (^) At this interest rate it would benefit of the company to use the discount.

Accounting for Prompt Payment

Discounts

• There are two methods of accounting for

Prompt Payment Discounts:

– Net Method:

- (^) Used when the Discount is attractive and most

customers are expected to take advantage.

– Gross Method

- (^) Used when the Discount is not attractive or neutral

and most customers are not expected to take

advantage.

Gross Method of Accounting for

Prompt Payment Discounts

It is expected that customers will not take

the discount!

- (^) The sale is recorded at the full, billed amount. Sale = $1000 with terms of 1/2 percent, 10 days/net, 30 days.

- (^) Recording the receipt of cash if the discount is not taken.

- (^) When the receipt of cash if the discount is taken. Accounts Receivable $ Sales $ Accounts Receivable $ Cash $ Accounts Receivable $ Cash $ Discounts Allowed $

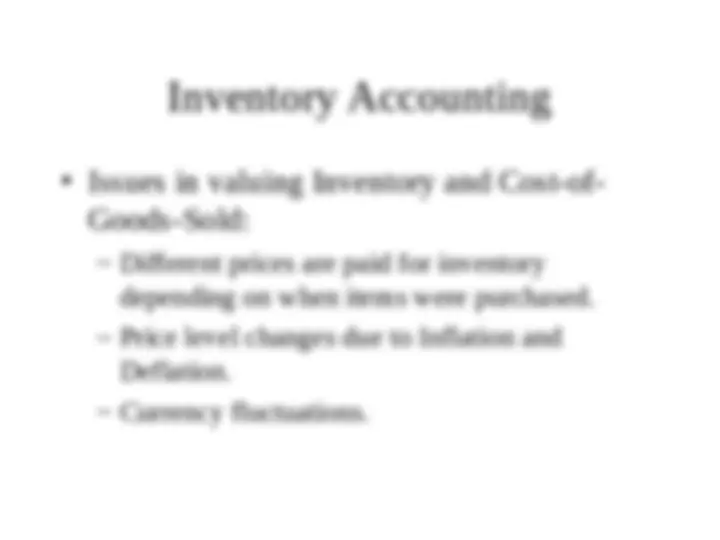

Accounting for Inventory

- (^) Inventory

- (^) Purchased goods on hand to be sold.

- (^) Two systems for valuing inventory that is sold

- (^) Perpetual Inventory System

- (^) Accounts for the cost of goods sold with each sale

- (^) Most precise and highest investment

- (^) Periodic Inventory System

- (^) Tracks inventory purchase but not inventory sold

- (^) Physical inventory count at end-of-period

- (^) Can only estimates the Cost of Goods.

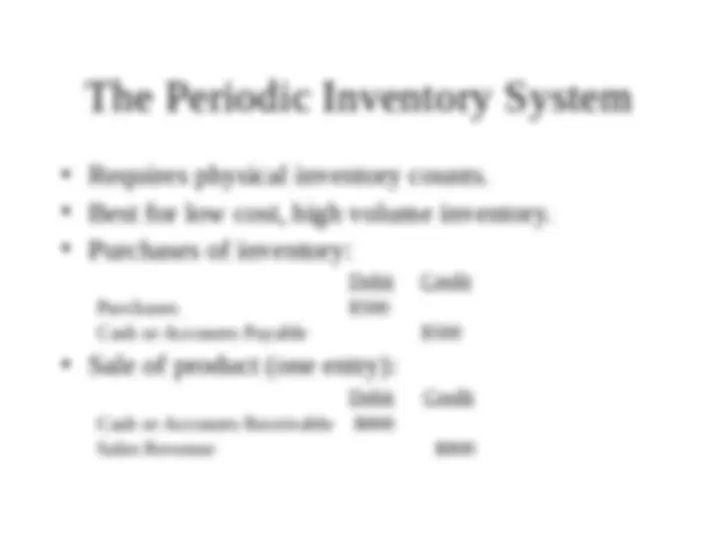

The Periodic Inventory System

• Requires physical inventory counts.

• Best for low cost, high volume inventory.

• Purchases of inventory:

Debit Credit Purchases $ Cash or Accounts Payable $

• Sale of product (one entry):

Debit Credit Cash or Accounts Receivable $ Sales Revenue $

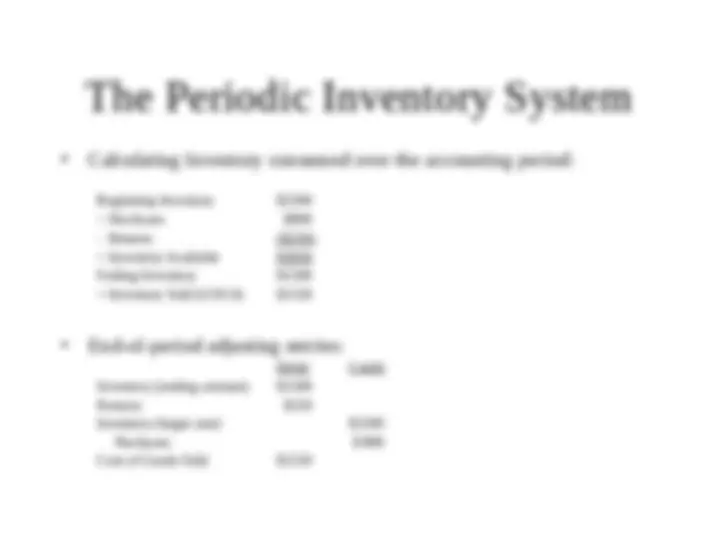

The Periodic Inventory System

- (^) Calculating Inventory consumed over the accounting period: Beginning Inventory $

- Returns ($250) = Inventory Available $ Ending Inventory $ = Inventory Sold (COGS) $

- (^) End-of-period adjusting entries: Debit Credit Inventory (ending amount) $ Returns $ Inventory (begin amt) $ Purchases $ 800 Cost of Goods Sold $

FIFO and LIFO

• The FIFO (First-in, First-out) convention:

- (^) The value of the oldest inventory, the First-in, is the value of the Cost-of-Goods-Sold for current sales, the First-out.

• The LIFO (Last-in, First-out) convention:

- (^) The value of the newest inventory items, the Last-in, is used to value Cost-of-Goods-Sold for current sales, the First-out.

• In periods of high Inflation:

- (^) LIFO will have a higher COGS and better match Expenses to Revenues;

- (^) Profits are lower (more conservative);

- (^) Better matches replacement costs of Inventory;

- (^) Lower Income Taxes thus higher cash flows.

- (^) GAAP allows FIFO or LIFO with restrictions (Riggs 147).

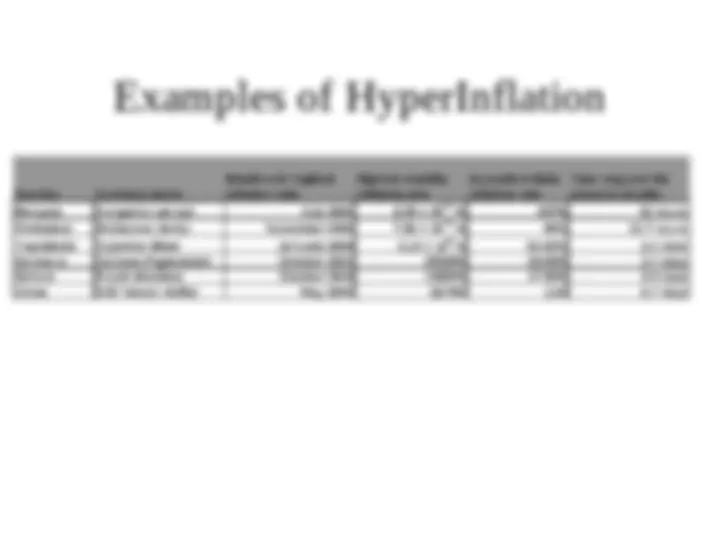

Price Level Changes

• Price level changes due to Inflation and Deflation

are a fact of life.

- (^) Inflation: a decrease in the purchasing power of currency; prices increase to compensate; the value of inventory decreases.

- (^) Deflation: an increase in the purchasing power of currency; prices drop to compensate; the value of inventory increases.

• Two approaches to price-level accounting:

- (^) Specific-price adjustments (SPA)

- (^) General-price-level adjustments (GPLA)

Specific-Price Adjustments

(SPA)

Adjustments are made to specific goods and services; typically

inventory and fixed assets. This identifies that only certain items

may be affected by price changes.

- (^) Several methods can be used to estimate the current value of

assets.

- (^) Time-adjusted value: Estimates the value of revenue streams over time. This method tends to be inaccurate both in estimating the original value as well as the new value.

- (^) Market value: Determines the replacement value of assets and requires good secondary markets to be efficient.

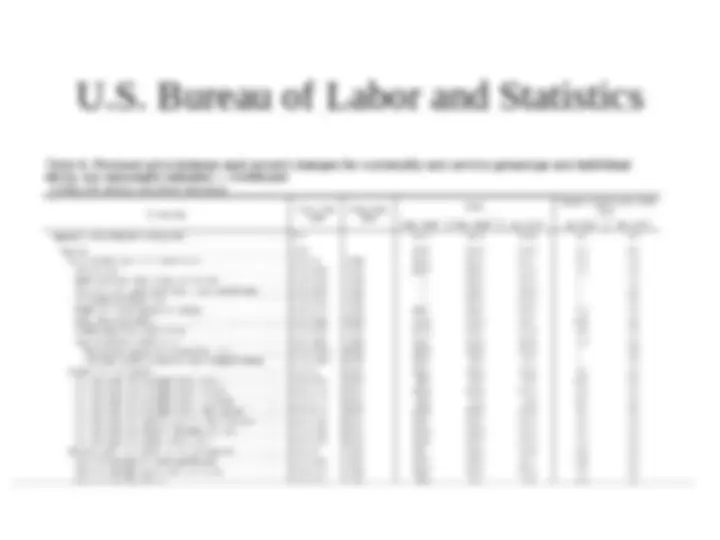

- (^) Price indices: Use of published indices for the asset being re-valued. Multiplying the current value by the index number will establish the current value.

U.S. Bureau of Labor and Statistics